Author:Zhou,ChainCatcher

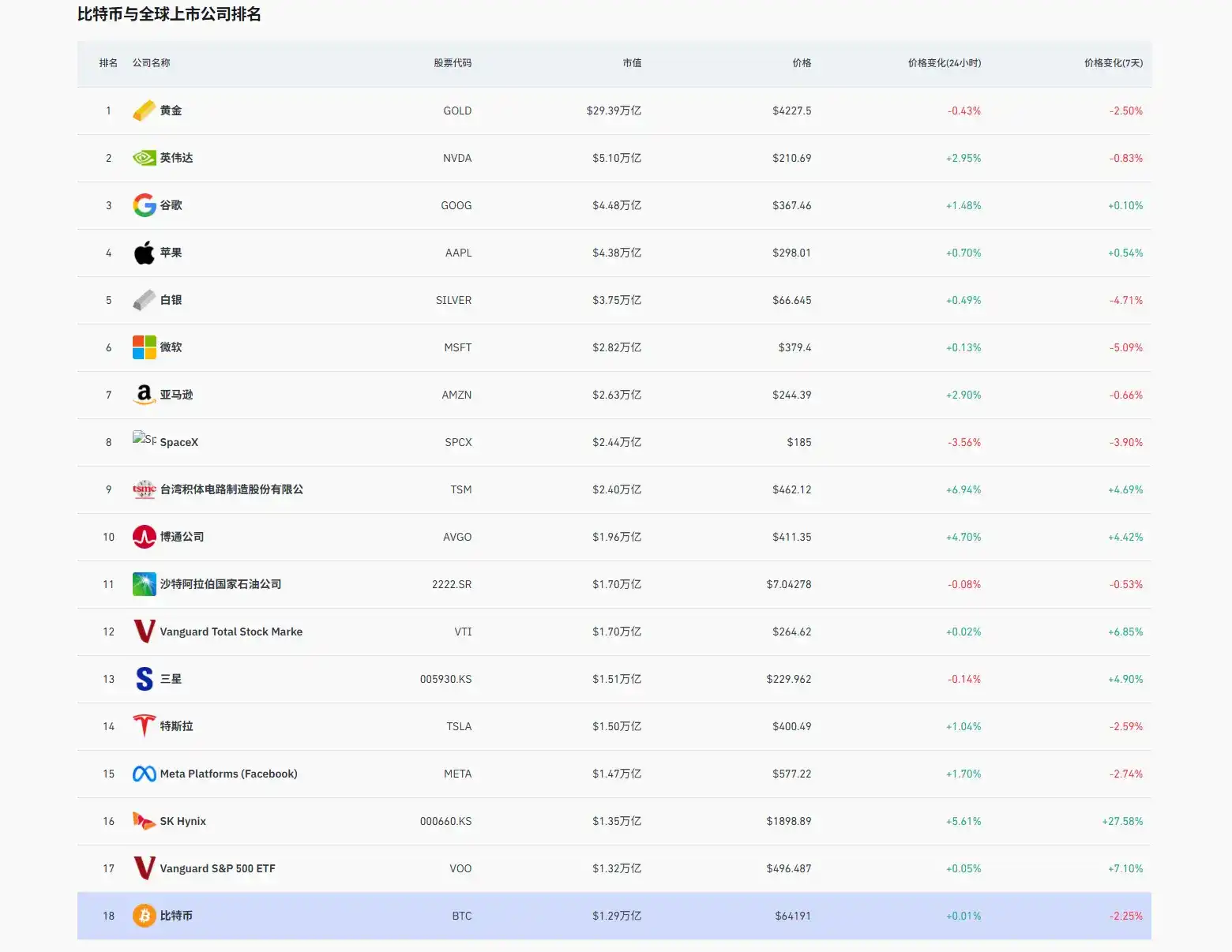

On June 22, a surge in SK Hynix's stock price propelled its market capitalization to $1.35 trillion, surpassing Bitcoin's total market cap of approximately $1.29 trillion. At one point during the trading session, it even overtook Samsung Electronics to become South Korea's highest-valued company.

According to Coinglass data, in the global asset rankings, SK Hynix rose to 16th place, while Bitcoin slid to 18th.

HBM, and a 13-Year Gamble

The core driver of SK Hynix's recent rally is HBM (High Bandwidth Memory). AI training and inference place extremely high demands on memory bandwidth, and SK Hynix is NVIDIA's primary HBM supplier, holding a market share exceeding 60%.

Financial reports show SK Hynix's Q1 revenue was 52.58 trillion won, with operating profit at 37.61 trillion won, achieving a profit margin of 72%. Analysts' current consensus for SK Hynix's Q2 operating profit is around 62~65 trillion won, with some brokerage houses' optimistic forecasts already revised upwards to over 68 trillion won.

In early April this year, most market expectations for Q2 were still in the 50 trillion won range. Since then, with persistently strong memory prices, brokerages have generally made significant upward revisions. Management stated during the earnings call that the structural memory shortage driven by artificial intelligence would last for at least several years and plans to significantly increase capital expenditure to expand advanced capacity.

Reportedly, SK Hynix began betting on HBM technology as early as 2009, a time when almost no one paid attention to this complex technology with limited initial demand. From the first generation of HBM to HBM3E, this all-or-nothing gamble lasted nearly 13 years, only reaching its coronation moment with the advent of ChatGPT.

Image Source: AI Generated

SK Hynix's journey to this point cannot be separated from a critical external rescue. After the dot-com bubble burst in 2001, Hynix was deeply mired in a debt crisis, its stock price once falling to junk levels. It even negotiated a sale to Micron Technology, which ultimately failed. For the following decade, the company remained under creditor control.

In 2012, SK Group Chairman Chey Tae-won overrode board opposition and acquired the company for approximately $3 billion through its investment holding subsidiary SK Square, renaming it SK Hynix and injecting substantial R&D funding. This investment enabled the company to continue advancing the then-niche HBM technology. Currently, SK Square holds about 20% of SK Hynix shares, making it the largest single shareholder.

It is worth noting that SK Square itself once attempted to enter the crypto market. In 2021, it acquired a 35% stake in the Korean crypto exchange Korbit for about 90 billion won and planned to issue its own token, SK Coin. According to public reports, after the Terra/LUNA crash in 2022, the market cooled sharply, and the SK Coin issuance plan was subsequently shelved, with no substantial progress since.

According to a Reuters report citing informed sources, SK Hynix plans to list on NASDAQ as early as August this year, which would lower the trading threshold for U.S. institutional and passive funds and potentially attract further capital inflows. NVIDIA CEO Jensen Huang recently stated that NVIDIA's collaboration with SK Hynix is expected to bring South Korea business opportunities worth hundreds of billions of dollars in the future.

Why is Capital Buying In? Crypto AI in the Mirror

In this wave of AI, the market is more willing to pay a premium for segments that already have real orders and visible supply bottlenecks. Assets directly involved in the AI supply side—computing power, memory, and electricity—have received priority allocation due to their quantifiable revenue and verifiable barriers.

HBM production capacity is highly concentrated in the hands of SK Hynix, Samsung, and Micron, with expansion cycles taking 2 to 3 years. This physical scarcity is not built on narratives; it is locked in by production cycles and technological barriers. The valuation logic of the memory industry is also shifting from "cyclical stock" to "growth stock."

SK Hynix's market cap surpassing Bitcoin is the capital market's public statement on two types of scarcity. With such high barriers already formed at the physical layer, the situation of Crypto AI is worth re-examining.

The Crypto AI sector has been telling a story for the past two years: decentralized computing power will reshape AI infrastructure, and open networks will surpass closed enterprise data centers. The potential of this direction is real, but standing before the market cap figure of SK Hynix today, several realities are worth confronting directly.

The IC3 report jointly released by Cornell University and 12 other universities points out that the convergence of Crypto and AI is still in its early stages, and the noise surrounding this intersection has overshadowed practical progress. Decentralized computing power, data markets, and governance mostly remain at the conceptual stage.

At the project level, taking Bittensor, one of the most representative projects in the Crypto AI sector, as an example, its token TAO has fallen 20% over the past 3 months. Bittensor co-founder const posted on platform X, stating that the project's economic incentive layer is still dominated by the core team, who chose to prioritize rapid iteration at the cost of maintaining centralization, and it is estimated to take another year and a half to complete the core mechanism construction. In other words, their underlying mechanisms are still being patched.

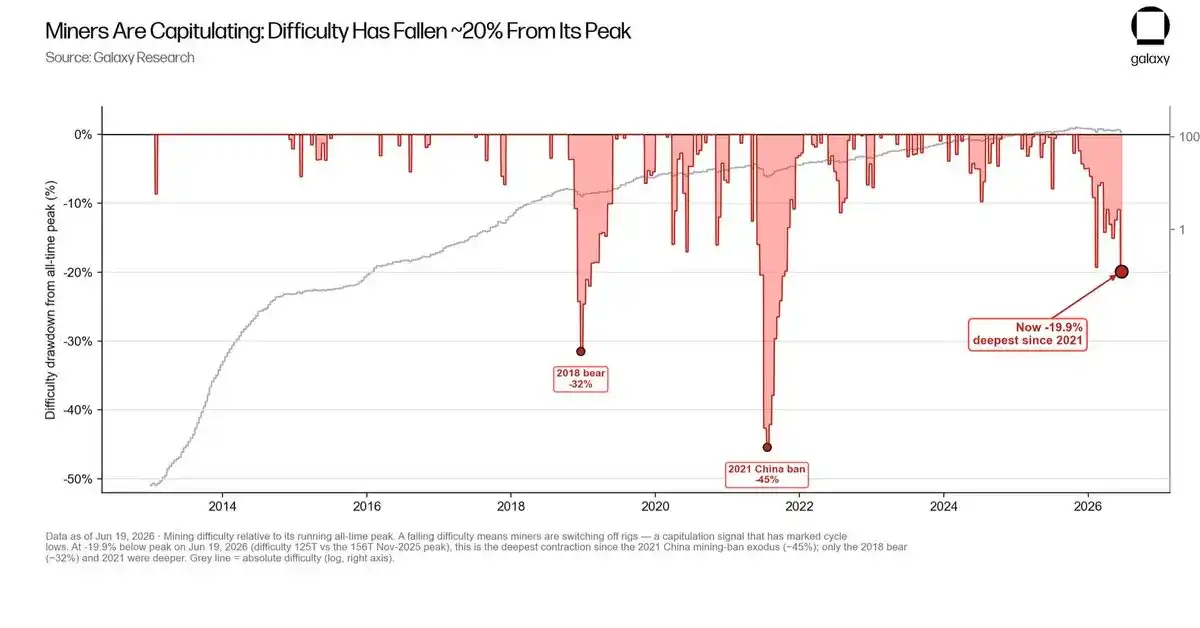

Crypto mining companies, which are closer to the hardware layer, are also facing challenges. According to Galaxy Research data, Bitcoin miners are entering a "capitulation period." The current network mining difficulty has dropped more than 20% from its historical high, marking the largest decline since China's crackdown on Bitcoin mining in 2021, with some miners continuing to exit the network or shut down equipment.

Seeking transformation, mining companies like Core Scientific, TeraWulf, and Hut 8 have announced moves into AI and high-performance computing. However, according to a VanEck report, this transformation faces a short-term funding gap of about $50 billion, with long-term capital needs around $221 billion. Furthermore, the industry has only delivered about 25% of the leased AI capacity—companies missing construction milestones already face investor downgrades.

The IC3 report jointly released by Cornell University and 12 other universities mentions that the convergence of Crypto and AI is still in its early stages, and the noise surrounding this intersection has overshadowed practical progress. Decentralized computing power, data markets, and governance mostly remain at the conceptual stage.

In terms of funding, Arthur Hayes pointed out in his recent article "Reality Test" that since the release of ChatGPT in 2022, the AI industry has cumulatively issued about $1.5 trillion in debt, roughly equivalent to the increase in U.S. M2 money supply during the same period—AI has absorbed almost all new liquidity; Bitcoin never had a chance. Hayes believes this is not a logic of "if AI falls, funds will flow back to crypto." The upcoming large-scale IPOs of Anthropic and OpenAI will further siphon market funds. Once the AI bubble bursts, bank credit contraction will simultaneously tighten liquidity, and Bitcoin will be sold off alongside AI.

Since the second half of last year, many traders previously active in the crypto market have shifted their attention to U.S. and South Korean stocks, chasing the AI hardware trend. The logic of capital flowing into AI infrastructure is also straightforward: real orders, physical barriers, quantifiable profit margins.

This certainty is the fundamental reason capital is willing to pay a high premium today, whereas the AI narrative in the crypto market lacks precisely this kind of certainty.

In other words, the dividends of AI infrastructure are currently more inclined to be captured by entities with technological barriers and real supply capabilities. In this process, crypto networks need to more clearly define their position in the value chain.