Author| Zach Pandl, Head of Research at Grayscale

Compiled| WuBlockchain

The tokenization process of global stock markets is advancing. Tokenized stocks promise various benefits for users, including 24/7 trading. The next significant development will be DTCC's [1] launch of a tokenization pilot on the Canton Network [2]. This pilot will allow tokenized stocks and other assets to circulate within the regulated financial system via blockchain infrastructure.

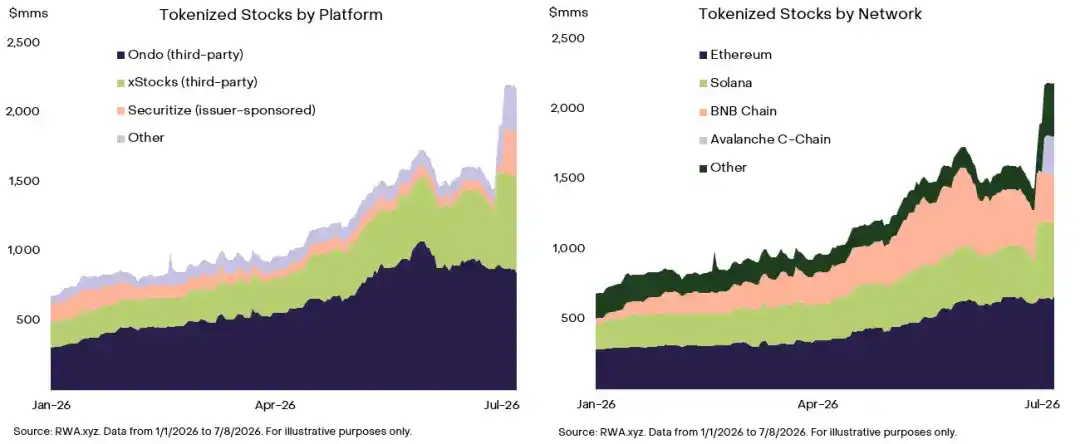

We believe stock market tokenization will progress through three stages, each bringing value to different types of blockchain infrastructure (see Chart 1).

The first stage is the third-party "wrapper" model [3]. In this model, an issuer holds stocks through a special purpose vehicle (SPV) [4], and the tokenized stock represents a claim on that SPV. Currently, over 70% of tokenized stocks by market value use this model. Wrapper-type tokenized stocks do not represent true stock ownership but can be used in DeFi and may appeal to retail investors. These assets currently trade on networks such as Ethereum, Solana, and BNB Chain.

The second stage is the "entitlement" model [5], represented by DTCC's pilot. Instead of creating new versions of securities, DTCC will record existing eligible securities on-chain through its regulated post-trade infrastructure, with the Canton Network serving as the initial blockchain network for this pilot.

The third stage is the issuer-led model, where companies directly issue securities natively on-chain. Last week, Securitize [6] became the first publicly listed company to tokenize its own common stock upon listing on the New York Stock Exchange. We believe this model holds the greatest long-term potential but still requires further regulatory clarity. In our view, the issuer-led model will be more favorable to open-architecture blockchains like Ethereum and Solana, as well as hybrid networks like Avalanche.

These three tokenization models are likely to coexist for many years to come.

Core View: Multiple models exist for tokenized stocks. In our view, the blockchain networks most likely to benefit from tokenization growth include Ethereum, Solana, BNB Chain, Avalanche, and the Canton Network.

Chart 1: Third-party platforms currently dominate the tokenized stock market, while Ethereum, Solana, and BNB Chain hold the majority of on-chain assets.

Notes:

[1] DTCC: The Depository Trust & Clearing Corporation, a core U.S. post-trade securities infrastructure entity responsible for services such as clearing, settlement, and custody of securities transactions.

[2] Canton Network: A blockchain network for institutional financial assets, emphasizing privacy, compliance, and interoperability of assets among different financial institutions.

[3] Wrapper model: A model where a third-party platform holds underlying stocks through an intermediary structure and issues on-chain tokens representing claims on that structure. Investors hold claims on the structure rather than direct ownership of the stocks themselves.

[4] SPV: Special Purpose Vehicle. In the context of tokenized stocks, it typically refers to an entity established by the issuer to hold the underlying stock assets, with the investors' tokens representing claims on that entity.

[5] Entitlement model: A model that does not re-issue a new security but instead records or maps existing eligible securities onto a blockchain through a regulated post-trade system, enabling them to circulate on blockchain infrastructure.

[6] Securitize: A platform for digital securities and real-world asset tokenization. The article mentions its simultaneous tokenization of its own common stock upon listing on the NYSE.