As of July 1, 2026, data from the IT Juzi Unicorn Database shows that China has a total of 517 listed unicorn companies, with a combined valuation of approximately $2.39 trillion. In terms of valuation structure, it presents a typical pyramid distribution—57.3% are concentrated in the $1–$2 billion range, 30.8% in the $2–$5 billion range, 62 companies (12.0%) above $5 billion, with only 5 super unicorns above $50 billion: ByteDance ($600 billion), Ant Group ($87.7 billion), SHEIN ($66 billion), DeepSeek ($61.5 billion), and Xiaohongshu ($50 billion). These top 5 companies contribute about 36% of the total valuation.

Geographically, they are highly concentrated, with Beijing (142), Shanghai (98), and Shenzhen (61), these three cities accounting for 58.2% combined. Hangzhou, leveraging companies like DeepSeek, contributes a valuation of $239.4 billion with 28 companies, ranking fourth as a single city. In terms of industry distribution, Advanced Manufacturing leads with 151 companies (29.2%), followed closely by Artificial Intelligence with 71 companies (13.7%) and Healthcare with 53 companies (10.3%). Robotics, with 44 companies, has surpassed E-commerce/Retail (34 companies) to rise to fifth place, reflecting the industrial shift from internet consumption towards hard tech.

Looking at the pace of listing, 2021–2022 was the peak period for unicorn births (89 and 94 companies respectively), followed by a significant cooling off. The first half of 2026 saw a strong rebound with 67 new unicorns, setting a new semi-annual record for the past five years. This new growth cycle is driven by AI and Embodied AI.

This report focuses on the 67 new unicorn companies listed in the first half of 2026, analyzing them from dimensions such as historical comparison, track distribution, city landscape, valuation structure, and founding time, aiming to present a complete picture and the underlying logic of this wave of unicorn emergence.

I. Overview of New Unicorns in 2026 H1

In the first half of 2026, China added 67 new unicorn companies, with a total valuation of $182.9 billion, an average of $2.73 billion, and a median of $1.409 billion. The highest valuation belongs to DeepSeek (approximately $61.538 billion).

In terms of total volume, the birth of 67 new unicorns within half a year means a new unicorn appeared on average less than every three days. The average valuation of the new unicorns ($2.73 billion) is about half of the average valuation of all listed unicorns ($4.631 billion). The median ($1.409 billion) is slightly lower than the overall median ($1.692 billion), indicating that this batch of new unicorns is generally at an early growth stage. However, the valuations of leading companies are extremely high, pulling up the average.

II. Historical Comparison: A New Growth Cycle Begins

Segmenting the period from 2014 to the first half of 2026 by half-year intervals and counting the number of newly listed unicorns in each cycle clearly reveals the cyclical characteristics of China's unicorn growth.

According to IT Juzi data, measuring unicorn growth speed in half-year dimensions over the past decade, the second half of 2021 set a historical peak with 76 new entrants. Following closely is the first half of this year, 2026 H1, with 67 new entrants—the valuation growth speed of Chinese startups has replicated the glory of five years ago.

Looking back at the entire cycle, 2021–2022 was the peak period for unicorn births, with four consecutive half-years exceeding 50 companies, including 76 in 2021 H2, 58 in 2022 H2, and 56 in 2022 H1.

2023–2024 entered an adjustment period, with a noticeable decline in new listings. The strong rebound occurred in 2026 H1.

The driving forces behind the two peaks are截然不同 (markedly different).

The 2021–2022 peak was primarily driven by new energy, biopharma, and consumer internet, with relatively分散 (dispersed) track distribution;

Whereas the 2026 H1 surge is highly concentrated in AI and robotics两大方向 (two major directions), with 19 in robotics and 17 in AI among the 67 companies, together accounting for over 53%.

This characteristic reflects the decisive role of technology cycles in unicorn births—the previous round was driven by mobile internet and the new energy vehicle industry chain, while this round is driven by large models and embodied AI.

III. Track Distribution: Dual Engines of Robotics and AI

The 67 new unicorns listed in 2026 H1 cover 10 primary tracks. Among them, Robotics (19) and Artificial Intelligence (17) together total 36 companies, accounting for over half, constituting the absolute dual engines.

The robotics track leads with 19 companies, covering humanoid robot本体 (bodies), core components like dexterous hands, embodied AI software platforms, and robot leasing services, indicating the systematic broadening of the industry chain. Among these, the humanoid robot方向 (direction) has 8 companies, including Ziliang Robot ($3.077B), Zhi Pingfang ($3.077B), Qianxun Intelligence ($2.769B), etc., all with valuations above $1.2B.

Notably, "spin-off" companies have emerged in this track—Linjiedian AGILINK comes from the dexterous hand department of Zhiyuan Robot, Digua Robot comes from Horizon AIoT's team—showing明显的 (obvious) technology溢出效应 (spillover effect) from large companies.

The AI track has 17 companies, but the valuation structure is highly polarized. DeepSeek alone, at $61.538B, contributes about 59% of the track's valuation. Excluding DeepSeek, the remaining 16 companies total $43.2B, with an average of about $2.7B. The AI track covers large models, multimodal video generation, AI chips & computing power, AI drug discovery, among others. Keling AI ($18B) stands out with its video generation capability, becoming the second-highest valued company in the track after DeepSeek. The AI chip & computing power direction has 4 companies (Xiwang Sunrise, Yixing Intelligence, Jiliu Technology, Wuwen Xinqiong), reflecting持续升温 (continued heating up) of investment in AI infrastructure.

The semiconductor track has 8 companies, covering automotive chips, communication chips, AI chips, autonomous driving chips, advanced packaging, and semiconductor equipment. Among them, autonomous driving chip companies like Shenji Technology (NIO's chip business spin-off) and Xinxin Hangtu perform突出 (prominently), with a clear国产替代 (domestic substitution) logic. The frontier tech track has 7 companies, with quantum computing独占 (solely occupying) 4 (Origin Quantum, Liangxuan Technology, Turing Quantum, Bose Quantum), indicating this field has entered an accelerated产业化 (industrialization) period domestically.

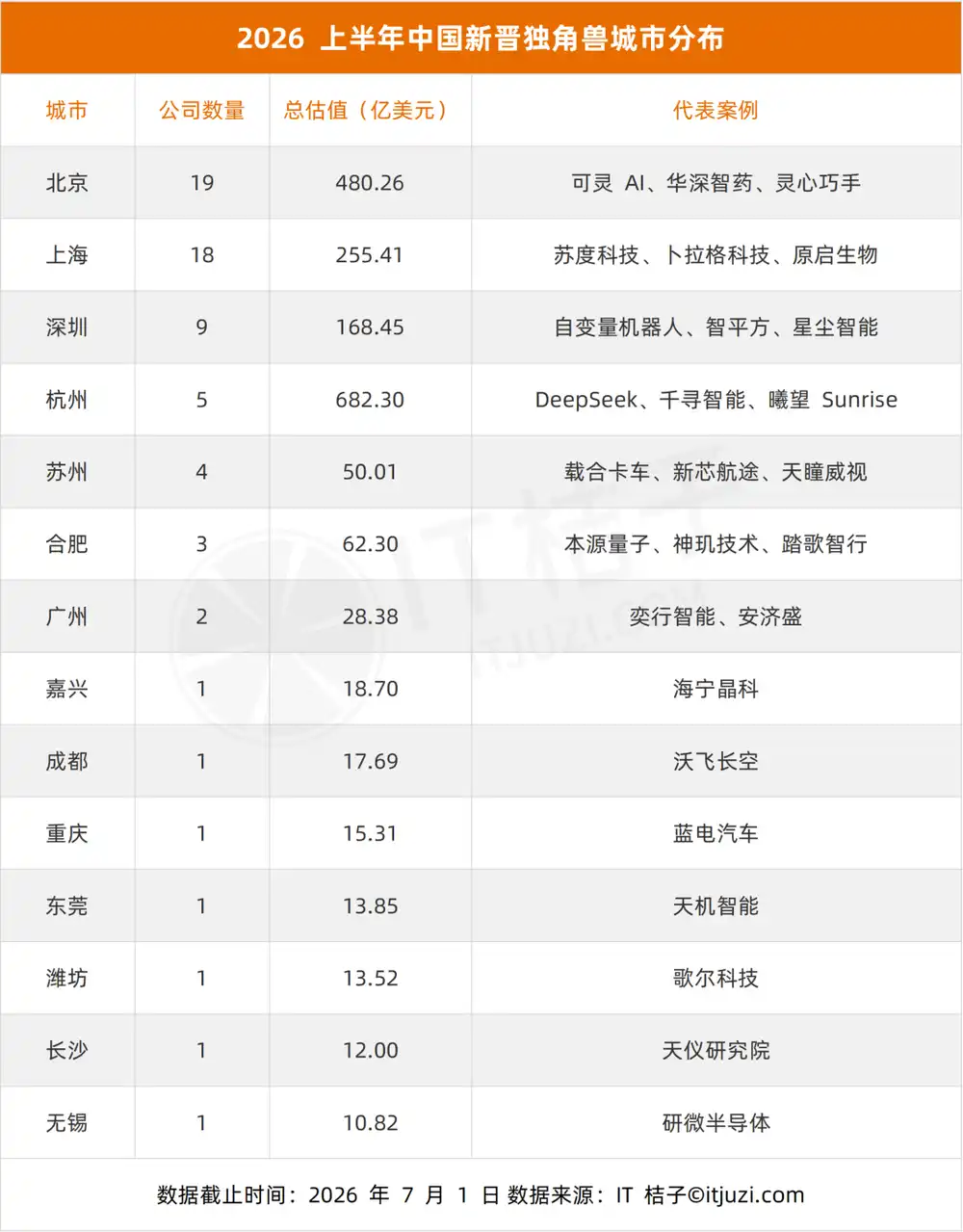

IV. City Distribution: Agglomeration in Four Cities: Beijing, Shanghai, Shenzhen, Hangzhou

The 67 new unicorns are distributed across 14 cities, with Beijing (19), Shanghai (18), Shenzhen (9), and Hangzhou (5)合计 (combined) totaling 51 companies, accounting for 76.1%.

Beijing leads with 19 companies, followed closely by Shanghai with 18, a gap of only 1 company. In terms of valuation, Beijing's $48B is far higher than Shanghai's $25.5B,主要得益于 (mainly benefiting from) the pull of high-valuation companies like Keling AI ($18B) and Huashen Zhiyao ($4B). Hangzhou, with only 5 companies,凭借 (leveraging) DeepSeek's single $61.538B valuation, achieves a total valuation of $68.2B,远超 (far exceeding) Shanghai and Beijing, accounting for 37.3% of the single-city valuation share.

Each city has鲜明的 (distinctive) track characteristics.

Among Shenzhen's 9 new unicorns, 6 are in robotics, making it the most密集 (dense) city for humanoid robot startups domestically.

Hefei's 3 new unicorns are all in hard tech directions (quantum computing, autonomous driving chips, mining无人驾驶 (unmanned driving)),体现 (reflecting) its "Science and Innovation City" positioning.

Among Suzhou's 4 new unicorns, 3 are related to smart vehicles, forming an intelligent connected vehicle industry cluster.

Beijing's advantage is集中 (concentrated) in AI and embodied AI software. Companies like Keling AI, Zhiyan Huisheng, and Huashen Zhiyao further reinforce this特色 (characteristic), while Shanghai is relatively均衡 (balanced) in AI, semiconductors, and biopharma directions.

V. Valuation Scale: Pyramid Structure, Super Unicorns Scarce

The valuations of the 67 new unicorns present a typical pyramid structure,高度集中于 (highly concentrated in) the $1–$5B range, with only 2 super unicorns above $10B.

77.6% of new unicorns have valuations falling within the $1–$2B range, indicating most new unicorns are still in the early成长 (growth) stage, having just crossed the $1B threshold. The $2–$5B range has 13 companies, representing a batch that has gained market validation and possesses a certain scale, including Huashen Zhiyao ($4B), Origin Quantum ($3.538B), Ziliang Robot ($3.077B), etc.

A断档 (gap) appears in the $5–$10B range, with no companies falling into this区间 (interval), reflecting a significant valuation leap between "unicorn" and "super unicorn." There are 2百亿美元级 (ten-billion-dollar level) companies: DeepSeek ($61.538B) and Keling AI ($18B), with DeepSeek's valuation exceeding Keling AI's by over 3 times. This极端分化 (extreme polarization) shows that in the large model track, technological领先性 (leadership) and market expectations can quickly translate into极高 (extremely high) valuation premiums.

Comparing with all listed companies, among the 517 unicorns, 62 (12%) are above $5B, and only 5 are above $50B. Among the 67新增 (newly added) in 2026 H1, 1 entered the $50B+ club (DeepSeek), a命中概率 (hit rate) considered罕见 (rare) among new unicorns.

VI. Founding Time: Polarization of Fast and Slow

Analyzing the founding years of the 67 new unicorns and the time from founding to listing reveals obvious "fast-slow polarization" characteristics.

Companies founded in 2023 are the most numerous (14), followed by 2022 (10) and 2021 (8). Companies founded in the past three years合计 (combined) total 32, accounting for nearly half. This高度吻合 (closely aligns) with the爆发时间 (explosion time) of the AI large model and embodied AI tracks—ChatGPT ignited the industry in 2023, a batch of companies were founded that year, becoming unicorns 2–3 years later.

The average time taken is 4.7 years, with a median of 3.7 years. Those listed within 3 years account for 34.3%, within 5 years account for 67.2%, meaning over half of the new unicorns completed their蜕变 (transformation) within 5 years.

Fast unicorns (within 3 years) are集中 (concentrated) in AI and robotics tracks, mostly spin-offs from large companies or startups by明星创始人 (star founders).

Borage Technology was founded by Lin Junyang, former head of Alibaba's Qianwen large model team, and became a unicorn仅 (only) 1 month after成立 (founding);

Linjiedian AGILINK is a spin-off from the dexterous hand department of Zhiyuan Robot;

Xiwang Sunrise is a spin-off from SenseTime's large chip department;

Zhiyan Huisheng was founded by Associate Professor Dai Jifeng from Tsinghua University's Department of Electronic Engineering and reached unicorn status in about 5 months.

These companies come with inherent technical积累 (accumulation) and resource advantages, securing high funding in a short period.

Slow unicorns (8+ years) are集中 (concentrated) in hard tech tracks.

Goertek (14 years), Yingchuang Huizhi (12 years), Gateland (12 years), Tianji Intelligence (11 years), Yuanqi Biotech (11 years)—fields like semiconductors, biopharma, and advanced manufacturing have high technical壁垒 (barriers), long R&D cycles, and lengthy validation periods, requiring长期投入 (long-term investment) to reach the unicorn valuation threshold.

This constitutes two截然不同的 (distinctly different) unicorn paths: AI and robotics rely on风口 (trends) and team溢价 (premium) for速成 (rapid success), while hard tech relies on时间积累 (time accumulation)慢慢磨 (slow grinding).

VII. Trends and Outlook

The集中涌现 (concentrated emergence) of 67 new unicorns in the first half of 2026标志着 (marks) the entry of China's unicorn growth into a new cycle. Compared with the previous cycle (2021–2022), this round presents several显著不同 (notable differences):

• The driving engine has shifted from多元分散 (diverse and dispersed) to高度集中 (highly concentrated). The previous peak was driven by multiple tracks like new energy, biopharma, and consumer internet, whereas this round高度依赖 (heavily relies on) the two major directions of AI and robotics, together accounting for over 53%. This concentration means capital's judgment on technology trends is highly一致 (consistent), but it also implies risks of赛道拥挤 (track crowding) and valuation泡沫 (bubbles).

• The speed of unicorn births has显著加快 (significantly accelerated). Those listed within 3 years account for 34.3%, mostly spin-offs from large companies or direct startups by star entrepreneurs. This "born as a unicorn" model, while reflecting the转化效率 (conversion efficiency) of technological积累 (accumulation), also means valuations for some companies are based more on team溢价 (premium) and market expectations rather than actual商业化验证 (commercial validation).

• The proportion of hard tech has increased, but分化加剧 (differentiation has intensified). New unicorns have emerged in frontier tech directions like semiconductors, quantum computing, and核聚变 (nuclear fusion). However, companies in these fields generally have longer founding times (8+ years), with valuation growth paths截然不同 (distinctly different) from the AI track. This coexistence of two speeds may persist.

• City agglomeration effects have further强化 (strengthened). The four cities of Beijing, Shanghai, Shenzhen, and Hangzhou account for 76.1%, a further increase compared to 58.2% of all listed companies. Entrepreneurship in new tracks高度依赖 (heavily depends on) talent density and industry chain support; this trend may accelerate the边缘化 (marginalization) of non-core cities.

Looking ahead to the second half of the year, AI and robotics tracks will likely remain the main sources of unicorns.

As embodied AI moves from labs to mass production, more robot本体 (bodies) and core component companies are expected to cross the $1B threshold. The国产替代 (domestic substitution) logic in semiconductor and quantum computing directions remains unchanged, but the节奏 (pace) may be influenced by policy expectations and financing environment.

Attention should be paid to whether rapidly born "lightning unicorns" can fulfill commercialization expectations within 1–2 years and whether track crowding will trigger valuation回调 (corrections).

Overall, the 2026 H1 unicorn surge is a缩影 (microcosm) of China's科技 (technological) innovation shift from internet consumption to hard tech. The birth of 67 new unicorns not only刷新了 (broke) historical records but also折射出 (reflects) that AI large models and embodied AI are transforming from technical concepts into industrial reality, a转化速度 (transformation speed) far exceeding any previous technology cycle.

Appendix: Complete List of Newly Listed Chinese Unicorns in 2026 H1

This article is from WeChat Official Account: IT Juzi , Author: Judy, Original Title: "China Added 67 New Unicorns in Half a Year, with AI and Robotics Accounting for Over Half | Interpretive Report"