Every Monday, Wednesday, and Friday, we review the market with data and seize opportunities through trends, covering macroeconomics, US stocks, precious metals, crude oil, and crypto assets, to gain insights into key changes in the global market. Produced by PANews.

Macro Market

The US and Iran are reportedly set to halt further military actions and plan to hold talks in Doha, Qatar, on June 30 to discuss navigation issues in the Strait of Hormuz. Just 11 days after the ceasefire agreement led by Trump took effect, the market has shifted back from the extreme scenario of "Hormuz Strait closure" to the trading logic of "oil prices returning to fundamentals."

WTI crude oil fell to $68.46, with a weekly drop of nearly 10%, breaking below $70 for the first time since the US-Iran war began. Brent crude also retreated to near pre-war levels. Tariq Zahir, managing member of Tyche Capital Advisors, warned that although the oil price decline is rapid, the ceasefire agreement remains fragile, and the situation in the Strait of Hormuz is still uncertain. JPMorgan believes the rapid pullback in oil prices is not due to supply recovery but rather a contraction in Asian demand, especially from China, far exceeding market expectations.

Although spot gold rebounded 1.36% to $4096 on Friday, it repeatedly fell below the $4000 psychological barrier last week and saw its first "death cross" since September 2023, where the 50-day moving average fell below the 200-day moving average. A stronger dollar and rising real interest rates remain the core logic suppressing precious metals.

Additionally, the US Bureau of Economic Analysis (BEA) announced that it will adjust the methodology for three components of the PCE price index—computer software, portfolio management, and legal services—in September, systematically lowering core inflation. UBS economist Alan Detmeister criticized the move, citing a lack of transparency and potential political manipulation, pointing out that the revision series tilts toward the upper end of the inflation contribution distribution, seemingly designed to artificially lower inflation. Goldman Sachs estimates the new rules could lead to a downward revision of the May core PCE year-on-year by 0.2 percentage points to 3.2%, and lower the forecast for core PCE in December 2026 to 3.0%.

Key upcoming events to watch:

-

June 30: US and Iranian delegations plan to hold high-level technical talks in Doha, Qatar. Whether they can fully resolve the dispute over international navigation lanes in the Strait of Hormuz will directly determine the lifeline of international oil prices.

-

July 1, 21:30 Beijing Time: The European Central Bank's Global Central Banking Forum in Sintra, Portugal, commences. Fed Chair Wash will make his first overseas appearance since taking office, engaging in debates with Lagarde, Bailey, and Macklem. Markets should be wary of signals beyond inflation regarding tightening and geopolitical risk premiums.

-

September 30: The BEA's new PCE price index statistical methodology officially takes effect. The "digital shrinkage" of the core inflation rate will fundamentally reshape the future path of Federal Reserve monetary policy games.

US Stock Market Dynamics

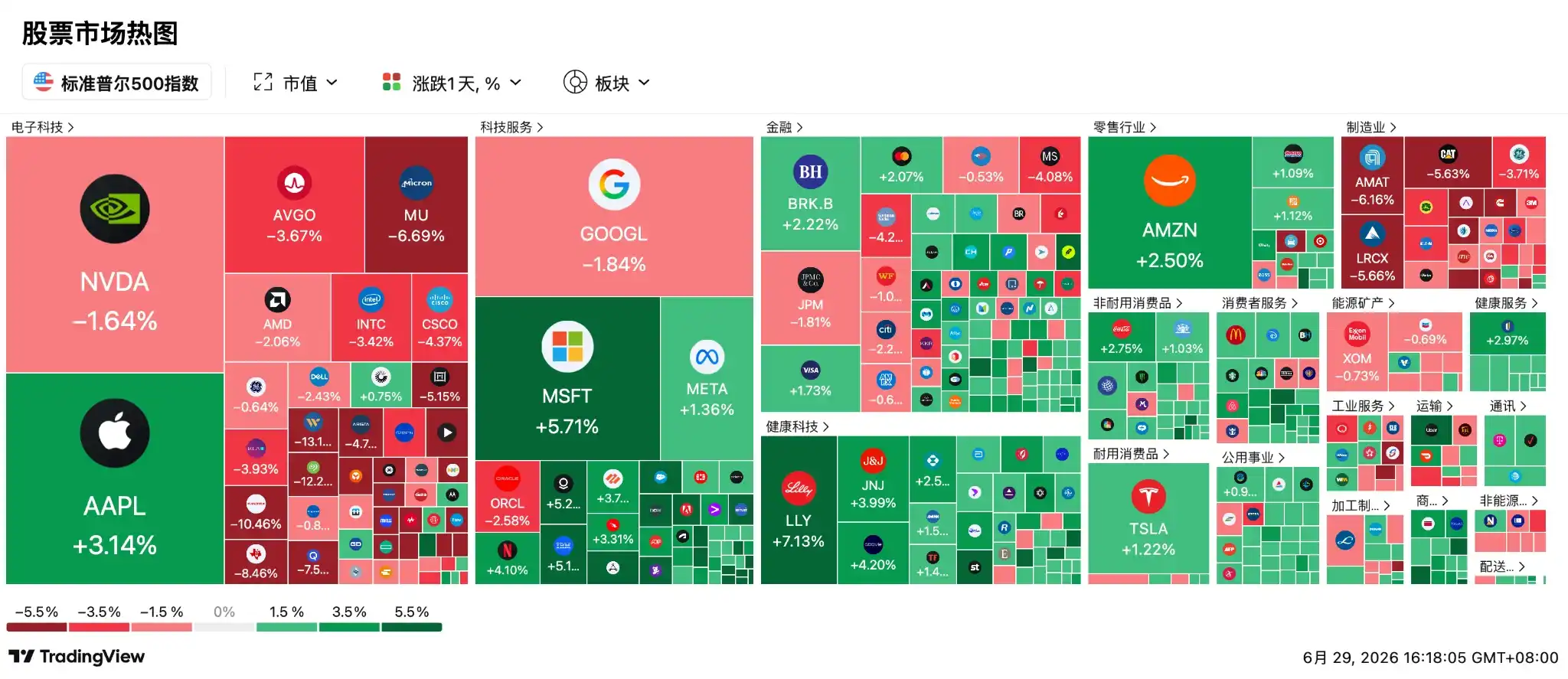

The major US stock indices barely closed flat on Friday. The S&P 500 edged down 0.05%, marking its fifth consecutive decline and the longest losing streak since August last year. The Nasdaq Composite fell 0.24%, also declining for the fifth straight session, its longest losing streak since January this year.

The frenzy over AI premiums is facing unprecedented liquidity unwinding, with hedge funds dumping US tech stocks at the most aggressive pace in a decade. Goldman Sachs PB data shows that as of the week ending June 25, the information technology sector experienced extreme selling at a 4-standard-deviation level, with a sell-to-buy ratio of 1.3 to 1. The semiconductor sector saw net selling for eight consecutive trading days, and the "Magnificent Seven" tech giants suffered continuous reductions for five weeks, with overall holdings nearing a three-year low. EPFR data corroborates this, showing a massive exodus of institutional funds from US tech funds last week following substantial prior inflows.

The Philadelphia Semiconductor Index plummeted 5.3% on Friday, with all 30 component stocks falling. Among them, onsemi plunged 23%, and Qualcomm dropped 7.57%. Although Micron Technology rose over 4% for the week, supported by strong earnings, it still succumbed to market pressure and fell 6.7% on Friday. Related memory stocks also declined: SanDisk fell 10.5%, while Western Digital and Seagate Technology dropped 13.17% and 12.24%, respectively. Forex.com analyst Fawad Razaqzada noted that investors have become highly sensitive to stretched AI valuations and high infrastructure costs, suggesting expectations for this sector have far exceeded commercial reality.

Funds are pouring into defensive sectors like healthcare, utilities, and real estate, with the Healthcare ETF and Biotech ETF leading gains. Mark Hackett of Nationwide stated that investor sentiment has turned pessimistic due to sharp rotations, but this looks more like a consolidation phase beneath the surface rather than the beginning of a significant downturn. John Belton, a manager at Gabelli Funds, also believes this is merely a pause, not a sell-off, and the AI platforms built by hyperscale cloud providers will continue to proliferate in the coming years.

SpaceX (SPCX) triggered a Nasdaq rule less than a month after its IPO and will be historically fast-tracked for inclusion in the Nasdaq 100 Index. JPMorgan estimates this will attract approximately $4.3 billion in passive fund inflows within a short period. However, Morningstar strategists indicate the stock is severely overvalued, and S&P Global has explicitly stated it will not follow suit, waiting at least 12 months before considering inclusion. Additionally, expectations for IPOs from OpenAI and Anthropic are heating up, with potential valuations exceeding $1 trillion.

Key upcoming events to watch:

-

After the close on July 6: $800 billion in passive funds tracking the Nasdaq 100 will begin concentrated allocations to SpaceX stock, which is expected to cause significant supply-demand oscillations in the semiconductor and tech sectors.

-

Before the market opens on July 7: SpaceX will officially begin trading as a component of the Nasdaq 100.

-

Throughout July: US stocks are entering the seasonally strongest "July window" of the year. Since 2015, the Nasdaq 100 has averaged a return of 4.4% in July with a historically high win rate, potentially ushering in strong allocation repairs following pension fund rebalancing.

Cryptocurrency

Bitcoin is experiencing its worst monthly performance since 2022. With less than two days left in June, the cumulative decline has reached 18.42%, making it one of the largest monthly drops since the 2022 bear market.

Currently, BTC price is fluctuating around the $60,000 mark, with the market focusing on its rebound potential in July. Since falling from $120,000, BTC has failed to reclaim the 200-week moving average (approx. $62,600) for the first time, turning this key support level into resistance and further increasing the risk of a decline to $55,000.

Historically, July is one of Bitcoin's best-performing months, with an average gain of 7.6% since 2013, and even reaching an average of 10.3% in midterm election years. If historical patterns repeat, BTC's theoretical target lies between $64,500 and $66,100, with an optimistic scenario possibly challenging $75,000.

Li Hua Yi, founder of Liquid Capital, stated this is the last major decline of this cycle, and July to August will present the most perfect buying opportunity for the next three years, with the potential downside limit between $51,000 and $43,000. CrypNuevo pointed out that Monday's market performance is crucial. Stabilizing above $61,000 will confirm a reversal, while falling below $57,000 could lead to a further decline to $52,000. The market is currently in a state of extreme oversold conditions, with a daily RSI divergence forming on the lows. July's performance will be a critical moment to test whether bulls can leverage seasonal effects to reclaim the 200-week SMA (approx. $62,445).

Key points for today:

-

Data: Tokens like SUI, EIGEN, FF are set for significant unlocks, with SUI's unlock valued at approximately $9.4 million.

-

SharpLink to be included in Russell 2000 and 3000 indices, effective June 29.

-

Spain's CNMV issued an urgent warning ahead of the end of the MiCA transition period on June 30.

-

0xPPL will cease trading functionality starting June 6 and fully shut down on June 30.

-

Base ecosystem project Seamless Protocol announced a gradual shutdown, with the UI interface going offline on June 30.

-

Falcon Finance (FF) will unlock approximately 102 million tokens on June 29, valued at around $6.9 million.

-

Collector Crypt (CARDS) will unlock approximately 28.84 million tokens on June 30, valued at around $6.7 million.

-

Upbit 24-hour trading volume leaders: SLX, BTC, XRP, POWER, HUNT.

-

Bitcoin Spot ETF: Net outflows of $1.79 billion last week, the third-highest weekly net outflow in history.

-

Ethereum Spot ETF: Net outflows of $273 million last week, marking seven consecutive weeks of net outflows.

-

HYPE Spot ETF: Net inflows of $111 million last week.

-

XRP Spot ETF: Net inflows of $22.99 million last week.

Top gainers among top 100 cryptocurrencies by market cap today: VELVET up 8.4%, JTO up 6.8%, 9BIT up 3.9%, NIGHT up 3.5%, FET up 3.3%.

Asia-Pacific Market

South Korean stocks opened under pressure from memory giants. Despite Aletheia Capital significantly raising DRAM price expectations due to global AI-driven supply shortages, absolute leverage in the market has reached historical highs of 2x-5x. SK Hynix and Samsung Electronics opened nearly 5% lower due to forced liquidation pressure, dragging the KOSPI index down over 3% intraday.

At a critical moment, the South Korean government and President Lee Jae-myung unveiled positive news, announcing the largest industrial investment plan to date, designating semiconductors, physical AI, and AI data centers as the "triangular pillars" of industrial upgrading. President Lee announced an investment of approximately 800 trillion won to build four chip factories in the southwest, with Samsung and SK Hynix each building two, aiming to double DRAM production capacity within five years. Additionally, South Korea plans to invest over 1,000 trillion won in AI data centers by 2035 and spend 81 trillion won to build an advanced packaging cluster in the Chungcheong region.

Buoyed by this news, the KOSPI index, Samsung, and SK Hynix share prices all rebounded.

The Japanese market found support from consumption recovery. May retail sales grew 5.3% year-on-year and 1.9% month-on-month, marking the third consecutive month of growth, with wage increases beginning to outpace inflation. Although the Nikkei 225 index ultimately fell about 0.15%, the consumption recovery narrative remains solid.

The Chinese market entered a phase of style rebalancing. The Shanghai Composite rose 1.16%, the STAR Composite Index climbed 3.12%, the Shenzhen Component edged up 0.19%, and the ChiNext gained 0.54%.

Innovative drugs were the biggest winners. The CRO sector surged 7%, with over 20 stocks hitting the daily limit-up; BeiGene rose over 10%, Baili Tianheng advanced 12%, WuXi AppTec gained 6%, and Hengrui Pharmaceuticals increased 8%. The catalyst was the National Healthcare Security Administration's announcement of 557 drugs passing the preliminary review for the national reimbursement drug list.

Consumer stocks also recovered. Kweichow Moutai rose over 3%, Dongpeng Beverage climbed 10%, and Bright Dairy & Food hit the daily limit-up. Institutions believe stable wholesale prices for Feitian Moutai indicate channel inventory adjustments are largely complete.

Hong Kong stocks clearly benefited from tech sentiment repair. The Hang Seng Index rose nearly 2%, the Hang Seng Tech Index jumped 3.23%, and the Hang Seng Biotech Index soared 7%. Alibaba surged nearly 6%, Meituan and Baidu gained over 7%, while Lenovo Group bucked the trend, falling over 10%.

Key upcoming events to watch:

-

June 30, 09:30: NetEase will officially transition to a dual primary listing on the Hong Kong Exchange, which will profoundly impact the capital structure and valuation system of the Hong Kong tech sector.

-

June 30: The 2026 China Intelligent Computing Industry Ecology Development Annual Conference officially opens, focusing on GW-level Token factory construction. Guidance on the second half of the AI hardware hype, including glass substrates and CPO, will be finalized at the conference.