Author: Gu Yu, ChainCatcher

In the traditional business world, brand equity is a company's lifeline. Frequent name changes are almost equivalent to actively destroying its moat.

NVIDIA wouldn't change its name every few years, Apple wouldn't abandon 'Apple' because of a business pivot, and Nike wouldn't scrap its brand and start over just because of a market downturn.

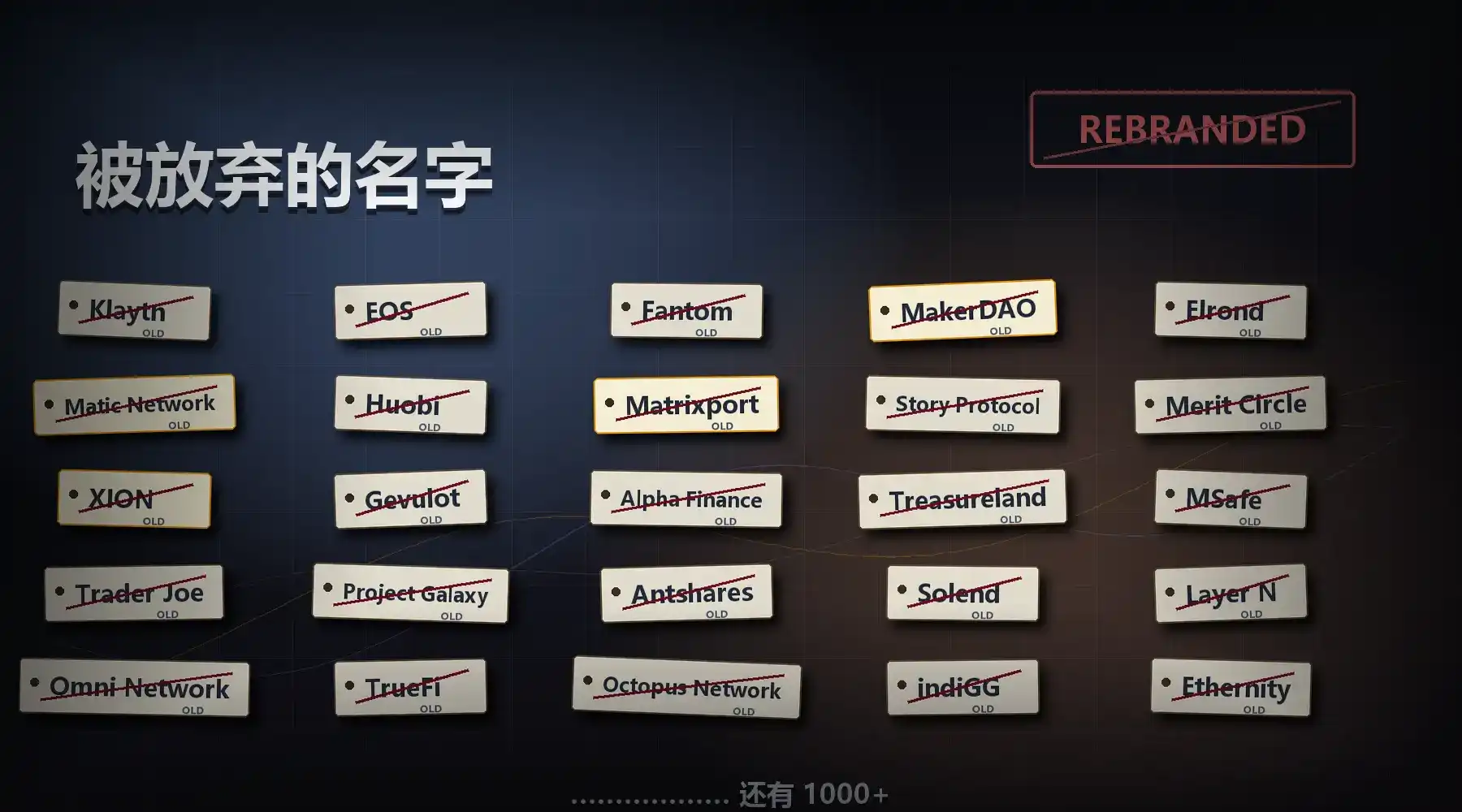

But in the cryptocurrency world, the rules are often reversed. According to RootData statistics, over 16% of crypto projects have changed their names, with many well-known first-tier projects exhibiting frequent name changes.

Just yesterday, the on-chain IP ecosystem Story Protocol announced a name change to DATA, with IP tokens migrating 1:1 to the new DATA tokens. In the preceding months, Xion rebranded as Verona, Matrixport changed its name to BIT, and the TON token symbol was changed to GRAM. Even earlier, a slew of prominent projects like Klaytn, EOS, Fantom, MakerDAO, Elrond, and Matic Network have undergone name changes.

Some projects, more extreme, have changed names multiple times. For instance, MAITRIX's former names include CENTRAL, X Network, and XLD Finance; BitSafe was previously known as dlcBTC and DLC.Link; TaleX had former names Read2N and Metale Protocol; KGeN was once called indiGG and Kratos Gaming Network. The names keep changing, but most projects haven't gained new life from new names, often fading into obscurity instead.

This raises a question seldom seriously discussed in the crypto industry: Why do crypto projects keep changing their names?

The answer might not be complex: because in the crypto industry, the brand is not the most important asset; attention, narrative, token price, and liquidity are.

I. Crypto Brand Loyalty Is Too Low

Traditional brands fear name changes because user loyalty stems from long-term consumption experiences. A user who has bought iPhones for years, drunk Starbucks for years, or worn Nike for years—their brand perception isn't formed overnight and won't easily change due to a single marketing campaign.

But the user structure of crypto projects is entirely different.

Most early users aren't traditional consumers but investors, airdrop hunters, liquidity providers, node participants, and narrative traders. They use a product not necessarily because it's good, but because there might be an airdrop, potential returns, or upside.

This implies that crypto brand user loyalty is inherently weak.

In traditional industries, users ask, "Is this brand trustworthy?" In crypto, users more often ask, "Can this coin still go up?" As long as prices are stagnant long-term, narratives fail, or ecosystems die down, an old name becomes a liability.

A name associated with a crash, being trapped in losses, hacks, team controversies, or roadmap failures struggles to inspire market imagination. It carries not brand equity, but the scars of price charts and community resentment.

This is the fundamental reason crypto projects dare to change names frequently: often, the old name has no moat, only historical baggage.

II. Name Changes as a Marketing Strategy

Not all name changes should be simplistically viewed as "changing skins." Some projects rename because the original name cannot encompass the new strategic scope. As market buzzwords shift, if a name includes outdated concepts like "Social" or "DAO," or if the name's meaning is no longer fitting, a name change becomes inevitable.

For example, the decentralized social protocol OpenSocial rebranded as Eden after pivoting to AI, the decentralized e-signature platform EthSign dropped "Eth" from its name after business expansion, and the Ethereum sidechain Matic Network changed its name to Polygon (meaning polygon) after building multiple scaling solutions.

When a project's business boundaries fundamentally change, the original brand can limit external perception. A name change at this point is a necessary strategic adjustment.

Of course, there are also many projects proactively "riding the hype," gaining more attention by incorporating trending concepts into their names. During the last metaverse hype, Elrond rebranded as MultiversX, directly adding "Multiverse" to its name, clearly hoping to latch onto the metaverse and multi-dimensional digital world narrative.

Similarly, as AI, RWA, and Perp become industry hotspots, many projects will rename to quickly align with the new concepts. For instance, Vanilla Finance rebranded as Superp, and Function X changed its name to Pundi AI, reshaping their narratives.

After all, in the crypto industry, narrative itself is part of asset pricing. The closer a name aligns with a new narrative, the easier it is to be noticed again by exchanges, KOLs, retail investors, and market-making capital.

For many projects, the core reason for a name change is that the old brand has sunk into a trust abyss.

In crypto history, hacks, contract vulnerabilities, cross-chain bridge exploits, and team scandals can rapidly destroy a project's brand credibility. Once users associate a name with "hacked," "collapsed," "rugged," or "poor compensation," continuing with the old name means constantly carrying negative PR.

Thus, rebranding becomes the project team's most direct PR tool, euphemistically termed "brand repositioning."

Anyswap's rebrand to Multichain after a hack, and Alpha Finance's name change to Stella after a $37 million exploit, carry similar undertones. Superficially, they are adjusting product lines and strategic positioning; but from a market perception standpoint, the name change also serves, to some extent, the function of "cutting ties with the old memory."

III. The Gray Area of Name Changes and Token Swaps

If it were just a name change, the impact would be limited. What's truly worth being vigilant about is that many crypto project name changes often come with token swaps.

A token swap means old tokens need to migrate to new ones. Exchanges issue announcements, deposits/withdrawals are suspended, old trading pairs are delisted, and new ones are listed. For project teams, this is a rare opportunity for a "second listing."

Many projects also conduct token splits. For instance, 1:100 or 1:1000 splits, breaking higher-priced tokens into a larger quantity to make the unit price appear cheaper. Projects like SKY and BEAM have employed similar tactics. A stock split itself doesn't change company value, but a lower unit price often attracts more retail attention.

More crucially, after a name change and token swap, exchange historical price charts are often reset to zero.

For many old tokens, the historical burden is immense. Years of trapped positions, downtrends, negative news, and resistance levels are all embedded in the old price charts. After the new token launches, it superficially possesses a brand-new chart—no historical highs as resistance, no long-term bearish shadow, and no immediate memory of trapped positions.

This is extremely advantageous for project teams and market makers. When old tokens migrate to new ones, many exchanges suspend deposits/withdrawals. At this point, the actual circulating supply on secondary markets can become very light. On the few platforms where trading remains open, market-making capital might only need relatively little money to pump the new token price, creating the market illusion of a "post-upgrade surge."

Subsequently, the project team, early participants, or market makers might use the restored liquidity and user FOMO to complete distribution.

This is the most dangerous aspect of name changes with token swaps: it superficially appears as a brand upgrade but is, in essence, potentially a liquidity reset.

Going further, many projects redesign tokenomics during the swap process. Ordinary users see a 1:1 migration and think their rights aren't harmed. But the project team might simultaneously add new validator rewards, ecosystem funds, team incentives, node subsidies, and strategic reserves, thereby creating a large number of new tokens out of thin air.

FRONT's rebrand to Self Chain and TVK's change to Vanar Chain are classic cases. Both drastically increased token supply under the pretexts of node rewards and ecosystem building, diluting the value for existing token holders.

IV. The Real Problem Isn't Renaming, But Evading History

Crypto projects can certainly change their names; that in itself isn't a grave issue.

Changes in technical roadmap, expansion of product boundaries, shifts in market trends, or cutting legal risks can all bring about reasonable brand repositioning. Cases like Matic's rebrand to Polygon show that a good name can indeed help a project embrace a larger strategic vision.

But in more instances, crypto project name changes aren't about building brand equity; they're about escaping from it.

Escaping old price charts, escaping trapped positions, escaping hacks, escaping failed narratives, escaping user skepticism, escaping stories that have run their course.

This is precisely the biggest difference between the crypto industry and the traditional business world: traditional companies fear losing brand memory, while many crypto projects fear users remembering too much.

Therefore, when a project announces a name change, the market shouldn't only ask what the new name is, but should probe three questions:

What real new capabilities or strategies has it actually added? Has its tokenomics changed? What old history is it most trying to make users forget?

If behind the name change lies real products, real revenue, real users, and a clearer strategy, then it might be the start of a new chapter. But if the name change is merely accompanied by a token swap, trend-chasing, token inflation, and chart resetting, then it's likely just a repackaged old game.