Автор: Etherealize

Компиляция: Felix, PANews

Экономика AI Agent переживает буйный рост. Etherealize опубликовал развернутую статью, в которой утверждается, что Ethereum — единственный блокчейн, способный предоставить ей финансовую инфраструктуру без необходимости человеческой идентификации, с низкими затратами и композируемостью. Ниже приведены подробности.

В начале 2026 года AI Agent по имени Felix заработал более 300 000 долларов дохода за пять недель. Felix нанимает других AI Agent и управляет несколькими бизнес-направлениями: Iris отвечает за поддержку клиентов, а Remy — за продажи. Он продает постоянно обновляемое руководство по развертыванию AI Agent за 29 долларов; также создал и управляет Claw Mart — рынком, где разработчики могут покупать и продавать предварительно созданные шаблоны навыков и рабочих процессов AI. Кроме того, он настраивает AI Agent для предприятий, которым нужны специалисты по контент-маркетингу, представители службы поддержки клиентов или ассистенты по продажам. Его общие операционные расходы составляют около 1500 долларов в месяц.

Felix может писать код, развертывать веб-сайты, управлять воронками продаж, отвечать на письма службы поддержки. Все это без помощи человека. Но он не может открыть банковский счет. Создателю Felix, Нату Элиасону, пришлось лично создать аккаунт Stripe и передать Felix API-ключ. Заработанные Felix средства простаивают, поскольку он не может открыть брокерский счет для их инвестирования или привлечь финансирование для нового бизнеса. Традиционная финансовая система предполагает, что по другую сторону каждого счета, кредитной заявки или подписи находится человек. Но Felix — не человек.

Однако, когда Нат попросил Felix сделать что-то с криптовалютой, «у него не возникло никаких проблем, это было до смешного просто».

Felix не единственный в своем роде. Например, на прошлой неделе Марк Андреессен в подкасте Latent.Space заявил:

-

«Я считаю, что ИИ — это убийственное приложение для криптовалют... Теперь очевидно, что AI Agent нуждаются в средствах. Это уже происходит... Мои самые прогрессивные друзья, использующие OpenClaw, уже предоставили своим Claws банковские счета и кредитные карты. Они не только сделали это, но и явно нуждались в этом... Это совершенно очевидно. Количество людей, делающих это сегодня, я не знаю, наверное, около 5000. Но оно будет расти. Так эти вещи и начинаются».

Felix — это эксперимент, и пока рано судить, является ли его доход устойчивым или это просто первоначальный всплеск после запуска. Но модель, которую он представляет: автономный агент, который зарабатывает деньги, тратит их и нуждается в финансовых услугах, будет появляться снова и снова, независимо от того, выживет ли сам Felix. То, что люди одалживают свои финансовые идентичности, является лишь временным решением. В конечном итоге они будут использовать финансовую систему Ethereum, которую мы строили последние десять лет.

Агенты уже торгуют

До сих пор обсуждение AI Agent и криптовалют почти полностью сосредотачивалось на платежах. Coinbase, Cloudflare и Stripe создали фонд для управления x402 — открытым протоколом, позволяющим агентам осуществлять мгновенные микроплатежи в стейблкоинах. Stripe и Paradigm также запустили на Tempo (блокчейне, созданном для расчетов в стейблкоинах) Протокол платежей для машин (Machine Payments Protocol).

Данные уже весьма значительны. За первые девять месяцев x402 обработал более 140 миллионов транзакций между агентами на общую сумму 43 миллиона долларов. x402 сейчас генерирует около пятой части трафика в сети Base от Coinbase. Почти 16 000 верифицированных агентов работают в链上, и зарегистрировано более 400 000 уникальных адресов покупателей.

Агенты ускорят переход к нативным криптоплатежам, поскольку традиционные сети карточных платежей структурно несовместимы с коммерцией агентов. Согласно отчету «Состояние агентов в 2026 году», средняя сумма транзакций между агентами составляет 0,31 доллара, в основном для вызовов, вычислений и доступа к данным. При таких объемах платежей фиксированная комиссия Visa около 0,3 доллара поглотит почти всю сумму платежа.

Но платежи — это самая простая финансовая функция. Более интересный вопрос: что произойдет, когда некоторые из этих агентов выйдут за рамки простых платежей и начнут управлять средствами, которые хранятся между платежами.

Какой DeFi нужен агентам?

Большинству агентов финансовая система никогда не понадобится. Агенты поддержки клиентов, действующие от имени компаний, не будут иметь казну, как и агенты-кодеры. Это инструменты, работающие внутри компаний, которые их развертывают, и компании занимаются финансовой стороной.

Агенты, которым нужен DeFi, — это те, кто действуют как автономные экономические субъекты: у которых есть собственные потоки доходов, расходы, казначейство и которые не могут получить доступ к финансовым услугам из-за отсутствия человеческой идентичности. Таких агентов меньше, но их число растет. По мере того как агенты становятся более мощными, долгоживущими и автономными, количество агентов в стиле Felix вырастет с сотен до тысяч, а затем до миллионов. Генеральный директор Coinbase Брайан Армстронг считает, что количество AI Agent в конечном итоге превысит число людей. Даже если лишь небольшая их часть будет действовать как автономные экономические субъекты, общий управляемый ими капитал будет значительным. Тогда вопрос станет таким: какие финансовые услуги нужны автономному агенту?

-

Нужны займы: для оборотного капитала на вычисления, покрытия кассовых разрывов или финансирования новых проектов. Традиционное кредитование требует кредитной заявки, андеррайтеров и юридического лица, но в Aave агент может внести залог и немедленно занять стейблкоины без участия человека.

-

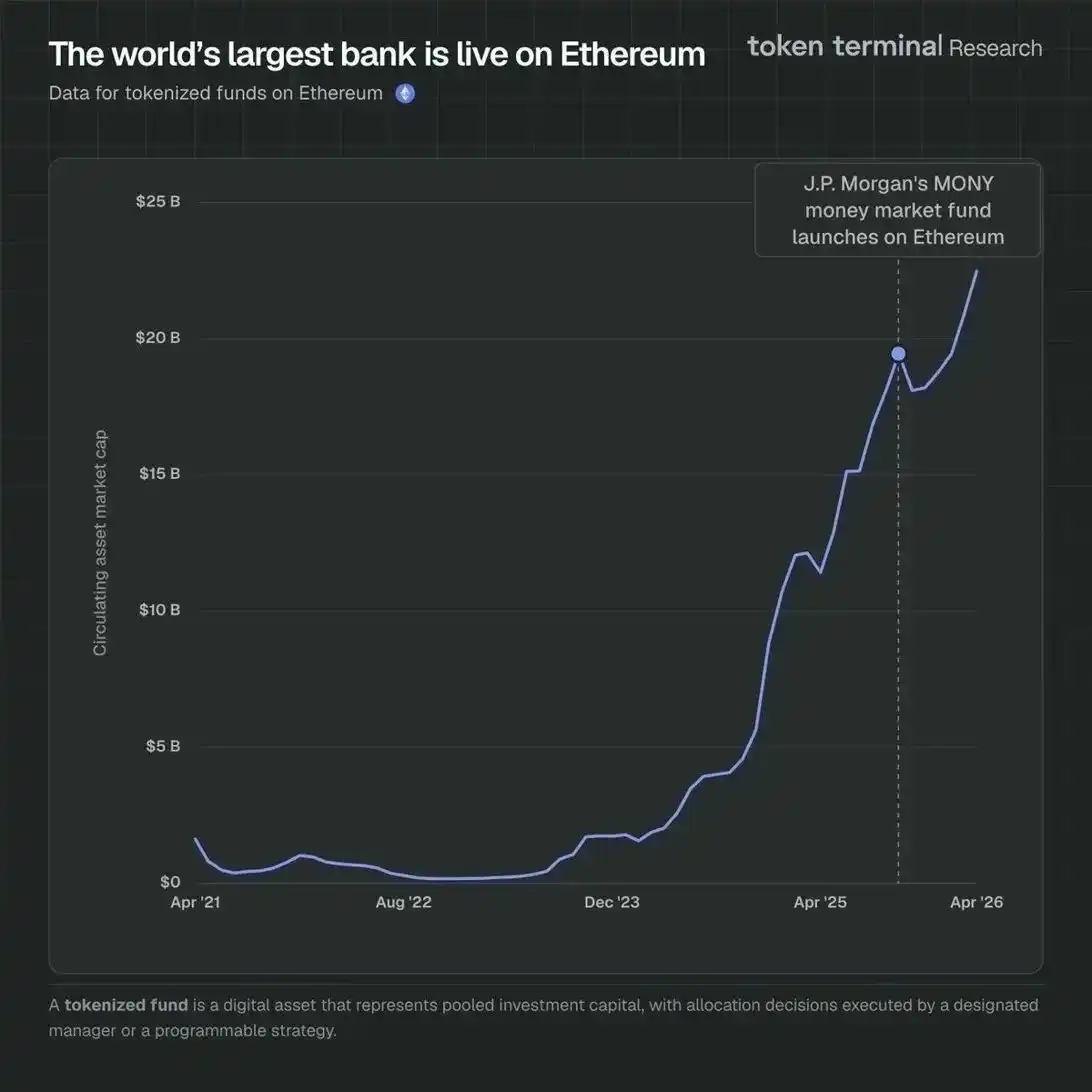

Нужно получать доход от闲置ных средств: У Felix есть более 165 000 долларов, и (по словам Ната) он «не знает, что с ними делать». В Ethereum эти средства можно deposited в кредитные протоколы, использоваться для покупки токенизированных казначейских облигаций, таких как BUIDL от BlackRock, или развернуты в качестве ликвидности в Uniswap, все это — без разрешения, мгновенно и композируемо. Продукты токенизированных казначейских облигаций в Ethereum быстро растут, в сети уже токенизировано более 22,5 миллиардов долларов активов фондов (71,9% доли рынка среди всех блокчейнов). J.P. Morgan запустила свой фонд денежного рынка MONY в Ethereum в начале 2026 года, присоединившись к BUIDL от BlackRock и ончейн-фонду денежного рынка Franklin Templeton. Эти продукты институционального уровня — именно то, что нужно автономным агентам с闲置ными средствами, работающим на инфраструктуре без разрешения, доступ к которой любой агент может получить без брокерского счета.

-

Нужно привлекать финансирование: Felix не может создать аккаунт в Carta или инициировать wire transfer из Mercury, но он может развернуть смарт-контракт, выпустить токены, представляющие долю дохода, получать инвестиции в стейблкоинах и программно управлять распределением. Правовая основа для этого формируется, но Закон о ясности рынка цифровых активов (Digital Asset Market Clarity Act) представляет собой твердый шаг в содействии формированию ончейн-капитала в США.

-

Нужно осуществлять и получать платежи: Это уже происходит в больших масштабах в L2 и Solana. Но когда Base платит комиссию за расчеты на L1, стейблкоины выпускаются и погашаются в мейннете, а агентам нужно где-то хранить доход между транзакциями, Ethereum получает выгоду от этой деятельности.

-

Нужно хранить активы: Токены акций, governance-токены, стейблкоины, учетные данные идентичности — без кастодиана, который может их заморозить, и без контрагента, который может их вернуть. Нативные кошельки Ethereum с самохранением изначально обеспечивают это.

Почему агенты используют низкорисковый DeFi в Ethereum

Виталик в сентябре 2025 года высказал мнение, что базовые финансовые услуги (такие как платежи, сбережения, кредитование и заимствование) представляют собой最重要的 приложение Ethereum. Его ключевое наблюдение заключается в том, что для растущего числа участников глобальной экономики неявный хвостовой риск традиционных финансов: банкротства банков, заморозка счетов, контроль за движением капитала, дефолт контрагента, теперь превышает хвостовой риск использования проверенных в бою протоколов DeFi. Он имел в виду людей в юрисдикциях с ненадежными финансовыми институтами, но этот аргумент еще более применим к агентам. Агенты будут склоняться к DeFi не только потому, что оно снижает риск контрагента, но и потому, что это по своей сути лучшая финансовая система для машин.

В DeFi стоимость транзакции составляет всего копейки, а не проценты. Расчеты занимают секунды, а не дни. Система является бесшовной в глобальном масштабе. И правила каждого протокола закодированы в открытом, проверяемом коде, который агенты могут проверить перед внесением средств.

Здесь присутствует ирония. Смарт-контракты всегда были неудобны для людей, и пользовательский опыт был постоянной проблемой. Когда Ник Сабо в 1997 году ввел это понятие, он описал логику контракта, встроенную непосредственно в машину, которая автоматически исполняется по условиям без вмешательства человека. Это видение никогда по-настоящему не подходило пользователям-людям, которые предпочитают человеческих посредников на случай проблем, но оно идеально подходит для агентов.

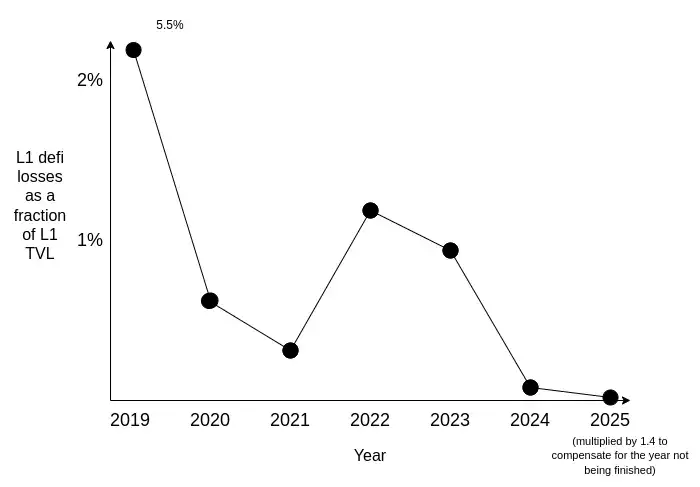

Автономный агент с казной в 500 000 долларов будет нуждаться в аналоге фонда денежного рынка, требующем предсказуемой доходности, глубокой ликвидности, extremely низкого риска смарт-контракта и отсутствия контрагента, который может заморозить или конфисковать его активы. DeFi в Ethereum все больше соответствует этому стандарту. Взломы и потери средств все еще случаются, но они становятся все более редкими и сосредоточены на спекулятивной периферии экосистемы. Стабильное ядро приложений доказало свою надежность в repeated стресс-событиях, и эту track record не смогла повторить ни одна другая публичная цепь.

Потери в DeFi на Ethereum L1. Источник: Vitalik Buterin

DeFi устраняет для агентов целый класс рисков. Правила закодированы в проверяемых смарт-контрактах; коэффициенты залога исполняются автоматически; нет контрагента, который может заморозить, вернуть или пересмотреть условия. Для программных участников это действительно превосходная архитектура.

Другие блокчейны также имеют протоколы DeFi. Любая команда может форкнуть Aave и развернуть кредитный протокол в новой цепи. Однако построение экосистемы DeFi, которой участники могут доверять в долгосрочной перспективе и вкладывать в нее значительные средства, — это совсем другой вопрос.

Как сказал Эрик Вурхес: «Ethereum по-прежнему король. Люди отвлекаются на другие L1, но если вы посмотрите, где разработчики и где объемы стейблкоинов, эти показатели трудно подделать, и они очень важны, они всегда были в основном сосредоточены на Ethereum. Разрыв очень очевиден».

DeFi на Ethereum в настоящее время обладает практически неоспоримыми сетевыми эффектами:

Зрелость протоколов. Aave запущен в 2020 году, MakerDAO с 2017 года поддерживает привязку DAI через multiple рыночные обвалы. Совокупный объем торгов на Uniswap превысил 3 триллиона долларов. Эти протоколы безупречно работали во время черных лебедей, таких как крах Terra/Luna и FTX. Для инвестора, размещающего средства на шесть месяцев, разница между протоколом, прошедшим пятилетние стресс-тесты, и протоколом, прошедшим двухлетние, имеет решающее значение. Инвесторы рациональны и взвешивают прошлые результаты при выборе направления развертывания капитала.

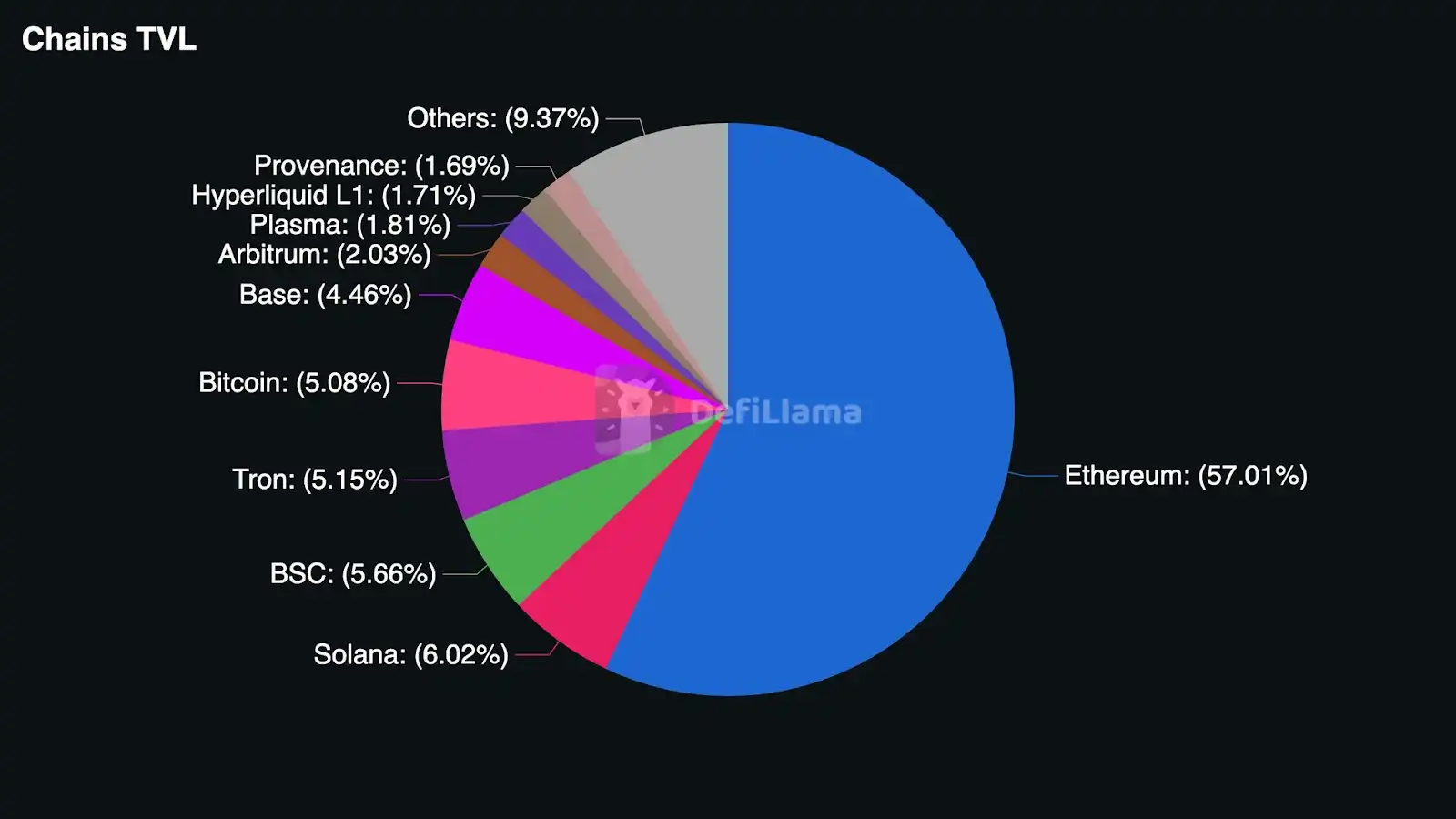

Глубина ликвидности. Низкорисковое кредитование требует глубоких пулов. Если агент вносит залог в 10 миллионов долларов в Aave и занимает 7 миллионов стейблкоинов, пул должен быть достаточно глубоким, чтобы справиться с этим без значительного проскальзывания или влияния на процентные ставки. Пулы DeFi в Ethereum в разы больше, чем у любого конкурента. По состоянию на апрель 2026 года TVL DeFi в Ethereum превышает 55 миллиардов долларов, что почти в 10 раз больше, чем у Solana, и составляет 57% доли рынка всех цепей.

Участие институтов. BlackRock выбрала Ethereum для запуска своего BUIDL. Franklin Templeton выбрала Ethereum для своего ончейн-фонда денежного рынка. Ethereum размещает около 71% токенизированных фондов. Эти институты провели широкую due diligence при выборе блокчейна. Их участие создает самоподкрепляющийся эффект: более глубокая ликвидность привлекает больше институционального капитала, что еще больше углубляет ликвидность. Институты, ищущие среду DeFi с наименьшим риском, будут склоняться к блокчейну, где институциональный капитал наиболее сконцентрирован, поскольку его присутствие создает более глубокие рынки, более完善的 протоколы аудита и более ясную регуляторную среду.

Надежность сети. Ethereum за более чем десятилетнюю историю работы никогда не испытывал простоев. Безопасность обеспечивают сотни тысяч нод-валидаторов, что делает цензуру отдельной транзакции практически невозможной.

Композируемость. В Ethereum трейдер может deposited ETH в Aave, занять USDC и развернуть эти USDC в токенизированный фонд казначейских облигаций — все в одной транзакции. Если какой-либо шаг fails, вся последовательность откатывается. Нет частичного выполнения между шагами, нет риска контрагента. Эта композируемость существует потому, что все основные протоколы DeFi находятся в одной цепи и разделяют одно состояние, и ее ценность накапливается по мере того, как трейдеры выполняют все более сложные многошаговые финансовые стратегии.

57% TVL DeFi находится в Ethereum (Источник: DeFi Llama)

Что это означает для ETH

Автономные агенты в основном используют стейблкоины для транзакций. 98,6% платежей агентов номинированы в USDC. Но каждое их взаимодействие со стеком DeFi Ethereum: заимствование в Aave, обмен в Uniswap, развертывание смарт-контрактов, ребалансировка портфеля — требует оплаты комиссии за газ (gas) в ETH.

Агент, развертывающий залог в 1 миллион долларов, будет использовать Ethereum L1, потому что там самая сильная безопасность, и он будет готов платить комиссию за газ. Потому что эти сборы ничтожны по сравнению с рисковым капиталом. По мере роста активности DeFi агентов блокспейс Ethereum L1 будет становиться все более ценным, а EIP-1559 означает, что часть каждой комиссии за газ будет сожжена, permanently уменьшая предложение ETH в обращении.

Кроме того, как отмечает Виталик, вклад низкорискового DeFi в экономику ETH заключается не только в комиссиях за транзакции, но и в блокировке ETH в качестве залогового актива. Чем больше агентов занимают стейблкоины в Aave, тем больше ETH блокируется в кредитных протоколах, уменьшая предложение в обращении даже без механизмов сжигания.

Невозможно точно оценить resulting структурный спрос. Честно говоря, это зависит от того, сколько агентов разовьются в автономные экономические субъекты, от масштаба управляемого ими капитала и от того, сколько капитала проходит через систему DeFi Ethereum. Но направление ясно: экономика агентов растет, Ethereum — единственная финансовая система, способная обслуживать автономных участников в масштабе, и каждая транзакция в этой системе требует ETH.

Возможные проблемы

Три вещи могут ослабить этот тезис, и их стоит четко обозначить.

Во-первых, абстракция газа (gas abstraction). Абстракция аккаунтов и платежные агенты позволяют оплачивать газ стейблкоинами, а не напрямую держать ETH. Если это станет стандартной практикой, это снизит потребность в ETH как в оборотном капитале. Однако, некоторые环节 в链上 все равно потребуют получения и использования ETH для обработки транзакций.

Во-вторых, конкуренция. Если другие блокчейны или L2 достигнут той глубины ликвидности, зрелости протоколов и институционального влияния, которые сейчас есть у Ethereum, участники DeFi могут диверсифицировать свою активность DeFi на другие цепи.

В-третьих, традиционные финансы трансформируются. Банки в конечном итоге создадут API для аккаунтов агентов, брокерские компании построят machine-accessible интерфейсы. Однако, даже адаптированная традиционная финансовая система будет предлагать агентам продукты, разработанные для людей, с cost structure, включающей человеческие издержки, в то время как DeFi предлагает software-native продукты.

Но в целом, бычий довод перевешивает. Абстракция газа смещает спрос на ETH внутри экосистемы, а не устраняет его; конкурирующие экосистемы DeFi отстают на годы по конкретным атрибутам, необходимым для низкорискового DeFi; и структурная неэффективность традиционных финансов难以克服. Тем не менее, эти риски следует учитывать соответствующим образом.

Следующий миллиард пользователей Ethereum уже не будет людьми

Ethereum движется к тому, чтобы стать финансовой системой машинной экономики. Это единственная система, способная предоставить автономным агентам необходимые финансовые услуги (кредитование, генерация дохода, формирование капитала, хранение) без необходимости человеческой идентификации, без оплаты человеческих издержек, которые агенты не могут использовать, и без разделения доступа по юрисдикциям.

По мере увеличения количества и сложности агентов, те из них, которые в конечном итоге эволюционируют в автономные экономические субъекты, будут создавать постоянный спрос на низкорисковый DeFi в Ethereum. Каждая совершаемая ими транзакция будет требовать и уничтожать ETH. Финансовая инфраструктура, от которой они зависят, работает на Ethereum, потому что никакой другой блокчейн не может предоставить ликвидность, зрелость, надежность и институциональную поддержку, необходимые для низкорискового DeFi.

Читайте по теме: Galaxy Research: Как AI-агенты активируют ончейн-финансовый маховик в эпоху компаний с нулевым участием человека?