Автор | Yike Shangye, Автор | Цянь Лю, Редактор | И Ань

Согласно сообщению Financial Times в начале мая, Государственный фонд развития интегральных схем ведёт переговоры о лидерстве в первом раунде финансирования DeepSeek, с посленаучной оценкой в 45 миллиардов долларов, что составляет примерно 307,8 миллиардов юаней. Всего за несколько недель эта цифра выросла с 10 миллиардов долларов до 20 миллиардов, а затем до 45 миллиардов — почти пятикратное увеличение.

Ранее, по данным The Information, основатель Лян Вэньфэн планировал лично инвестировать до 20 миллиардов юаней, что составило бы около 40% акций. В апреле Reuters впервые сообщили, что когда DeepSeek начал внешнее финансирование, оценка составляла «всего» более 10 миллиардов долларов.

Как компания, существующая менее трёх лет, с численностью сотрудников всего от 160 до 200 человек, может стоить 300 миллиардов юаней?

Если задать этот вопрос о DeepSeek, а затем о Zhipu, MiniMax и Kimi, ответы будут примерно одинаковыми.

Согласно данным биржи Гонконга, рыночная капитализация Zhipu уже превышает 500 миллиардов гонконгских долларов (около 430 миллиардов юаней), при IPO она составляла всего 52,8 миллиарда гонконгских долларов, выросла почти в 10 раз за 4 месяца. По данным Shanghai Securities News, рыночная капитализация MiniMax превышает 250 миллиардов гонконгских долларов (около 223,5 миллиардов юаней), выросла почти в 4 раза за 4 месяца.

Согласно сообщению «LatePost», в последнем раунде финансирования Kimi на 2 миллиарда долларов лидировал Meituan Longzhu, оценка превысила 20 миллиардов долларов (около 136 миллиардов юаней), за полгода общий объём финансирования составил более 3,9 миллиарда долларов, что сделало её компанией-стартапом в области больших моделей в Китае, привлекшей больше всего финансирования.

Суммарная оценка четырёх компаний превышает 1 триллион юаней.

Это не сольное выступление одной компании, а капитальное цунами, захлестнувшее всю китайскую индустрию искусственного интеллекта. Государственный фонд лидирует в инвестициях в DeepSeek, China Mobile участвует в финансировании Kimi — государственные капиталы активно входят в игру. Проще говоря, это уже не просто игра венчурных фондов и частных инвесторов, а ставка на уровне национальной стратегии.

В то же время интернет-гиганты, такие как Tencent, Alibaba, Meituan, также голосуют реальными деньгами, опасаясь пропустить этот поезд. Tencent ведёт переговоры об участии в финансировании DeepSeek, Alibaba неоднократно инвестировала в Kimi, Meituan Longzhu единолично вложила более 200 миллионов долларов — гиганты, с одной стороны, сами тратят деньги на создание моделей, с другой стороны, инвестируют, чтобы «купить билет на поезд».

Интересно, что в отчёте JPMorgan Chase от 22 апреля был сделан вывод: «окно возможностей для создания портфеля по китайскому ИИ» составляет примерно 6-12 месяцев. Как только Kimi, StepFun и другие последующие компании выйдут на IPO, премия за уникальность Zhipu и MiniMax структурно снизится. Проще говоря: если не купить сейчас, потом может не быть такой возможности.

Что же покупают инвесторы? Этот вопрос стоит того, чтобы его разобрать.

1. Триллионная оценка: инвесторы борются за «право определения»

Для начала посмотрим на несколько острых данных.

Согласно годовому отчёту Zhipu и проспекту эмиссии MiniMax, выручка Zhipu в 2025 году составила 724 миллиона юаней, увеличившись на 131,85%, чистый убыток, относящийся к материнской компании — 4,698 миллиарда юаней, расходы на НИОКР — 3,18 миллиарда юаней, что означает, что на каждый заработанный юань приходится сжигать 4,4 юаня на НИОКР.

Выручка MiniMax в 2025 году составила 79,038 миллиона долларов, увеличившись на 158,9%, убыток — 1,872 миллиарда долларов, рост убытка на 302,3%.

Хотя Kimi не раскрывает полную финансовую отчётность, её материнская компания Moonshot AI привлекла совокупное финансирование более 37,6 миллиарда юаней, и скорость сжигания денег, очевидно, высока.

Интерфейс продукта AI-ассистента Zhipu Qingyan, Рис./Сайт Zhipu AI

Интересно, что согласно годовому отчёту iFLYTEK, выручка iFLYTEK в 2025 году составила 27,1 миллиарда юаней, чистая прибыль — 839 миллионов юаней, общая рыночная капитализация — около 118,7 миллиарда юаней. Компания, ежегодно зарабатывающая 800 миллионов юаней, стоит менее 120 миллиардов; а компания, теряющая 4,7 миллиарда юаней, стоит более 500 миллиардов.

Как это считать?

Честно говоря, традиционные модели оценки здесь практически неприменимы. DCF (дисконтированный денежный поток) для этих компаний — всё равно что считать траекторию ракеты на счётах — инструмент сам по себе неплох, но не подходит для этой сцены. Инвесторы покупают не сегодняшнюю выручку, и даже не завтрашнюю прибыль, а опцион на «право определять будущее».

В отчёте JPMorgan есть ключевой вывод: у премии за уникальность больших моделей ИИ есть окно возможностей, примерно 6-12 месяцев. Приводится прецедент — Cambricon была единственной чистой компанией по производству ИИ-чипов на китайском рынке акций A, цена её акций в конце ноября 2025 года составляла около 1500 юаней. Затем последовательно вышли на IPO Moore Thread, MetaX, Biren Technology. Хотя прогнозы по выручке и прибыли Cambricon пересматривались в сторону повышения, цена акций с начала года всё ещё упала примерно на 2%, а коэффициент оценки сократился на 25-30%. Как только появляются конкуренты, уникальность исчезает.

Эта логика применима и к «Четырём драконам». Zhipu и MiniMax — в настоящее время единственные в мире публичные компании, чисто занимающиеся передовыми большими моделями ИИ, они пользуются не «премией за результаты», а «премией за уникальность». Как только Kimi выйдет на IPO, как только DeepSeek откроет финансирование, эта уникальность будет размыта. Поэтому сейчас торопятся инвестировать, инвестируют не в определённость, а в «занятие места».

Рис./Сайт MiniMax

Проще говоря, этот триллионный карнавал оценок по сути является аукционом за «право определять будущее». Кто сможет определить технологические стандарты, бизнес-модели, пользовательские привычки в эпоху ИИ, тот может стать следующей Microsoft или Google. То, что сейчас делают «Четыре дракона», — это попытка до закрытия окна с помощью огромных инвестиций выжечь себе место.

2. От «компаний на презентациях» до «компаний с выручкой»: прогресс в технологиях и способности зарабатывать

В 2023 году компании, работающие с большими моделями, ещё высмеивали как «компании на презентациях» — истории рассказывали умопомрачительные, а выручка практически нулевая. Прошло два года, ситуация изменилась.

Согласно сообщению «Народной газеты», в марте 2026 года среднесуточный объём использования токенов в Китае превысил 140 триллионов, тогда как в начале 2024 года эта цифра составляла всего 100 миллиардов, рост более чем в тысячу раз за два года. Токен — это минимальная единица обработки информации большой моделью, а также ключевая расчётная единица для коммерциализации отрасли. Проще говоря, во сколько раз выросло использование токенов, во столько раз поднялся уровень всей отрасли.

Этот уровень напрямую отражается в отчётах о выручке компаний.

Согласно информации партнёра Meituan Longzhu Ван Синьюя, после обновления модели K2.5, ARR (годовая регулярная выручка) Kimi в марте этого года превысил 100 миллионов долларов, а в апреле увеличился до 200 миллионов долларов. Четыре раунда финансирования за полгода, совокупно более 3,9 миллиарда долларов — это само по себе признание рынком её коммерческого потенциала. Модель K2.6 поддерживает параллельную работу 300 суб-агентов, 4000 шагов коллаборации, сделав большой шаг вперёд в способностях к коду и кластеризации агентов.

Рис./Сайт Kimi

Данные Zhipu ещё более впечатляющие. Согласно раскрытой компанией информации, ARR её платформы MaaS API составляет около 1,7 миллиарда юаней (примерно 250 миллионов долларов), увеличившись в 60 раз, с начала года рост в 6,4 раза. В течение 24 часов после выпуска GLM-5, такие ведущие платформы, как TRAE от ByteDance, Qoder от Alibaba, CodeBuddy от Tencent, CatPaw от Meituan, Wanqing от Kuaishou, Baidu Intelligent Cloud и WPS Office, официально интегрировались, 9 из 10 крупнейших интернет-компаний Китая активно используют модель GLM.

По состоянию на март 2026 года, количество зарегистрированных предприятий и пользователей на платформе Zhipu превысило 4 миллиона, обслуживая более 218 стран и регионов мира. В феврале 2026 года Zhipu самостоятельно повысила цены на API на 30% и отменила скидку на первую покупку, спрос по-прежнему превышает предложение — это редкий сигнал в глобальной индустрии ИИ: он показывает, что клиенты готовы платить за более определённую производительность. Согласно наблюдениям отчёта JPMorgan, ценовая политика API Zhipu становится «намного более стабильной», ценовая среда гораздо здоровее, чем год назад.

Платформа Zhipu AI BigModel, Рис./Сайт Zhipu AI

Подход MiniMax немного другой. Согласно годовому отчёту MiniMax, выручка в 2025 году составила 79,038 миллиона долларов, доля зарубежных доходов превышает 70%, валовая прибыль уже перешла из отрицательной в положительную зону — 25,4%. На стороне потребителей она создала два глобальных продукта — Talkie и Conch AI, идёт по пути «нативных приложений ИИ». По состоянию на конец 2025 года, продукты MiniMax обслужили около 236 миллионов пользователей, накопленное количество корпоративных клиентов и разработчиков превысило 214 тысяч. Основатель Янь Цзюньцзе публично заявлял, что ожидается взрывной рост потребления токенов на один-два порядка, ARR компании может войти в диапазон 1 миллиарда долларов.

Интерфейс приложения MiniMax Conch Video, Рис./Сайт MiniMax

Прогресс на технологическом уровне является фундаментальной поддержкой взрывного роста доходов.

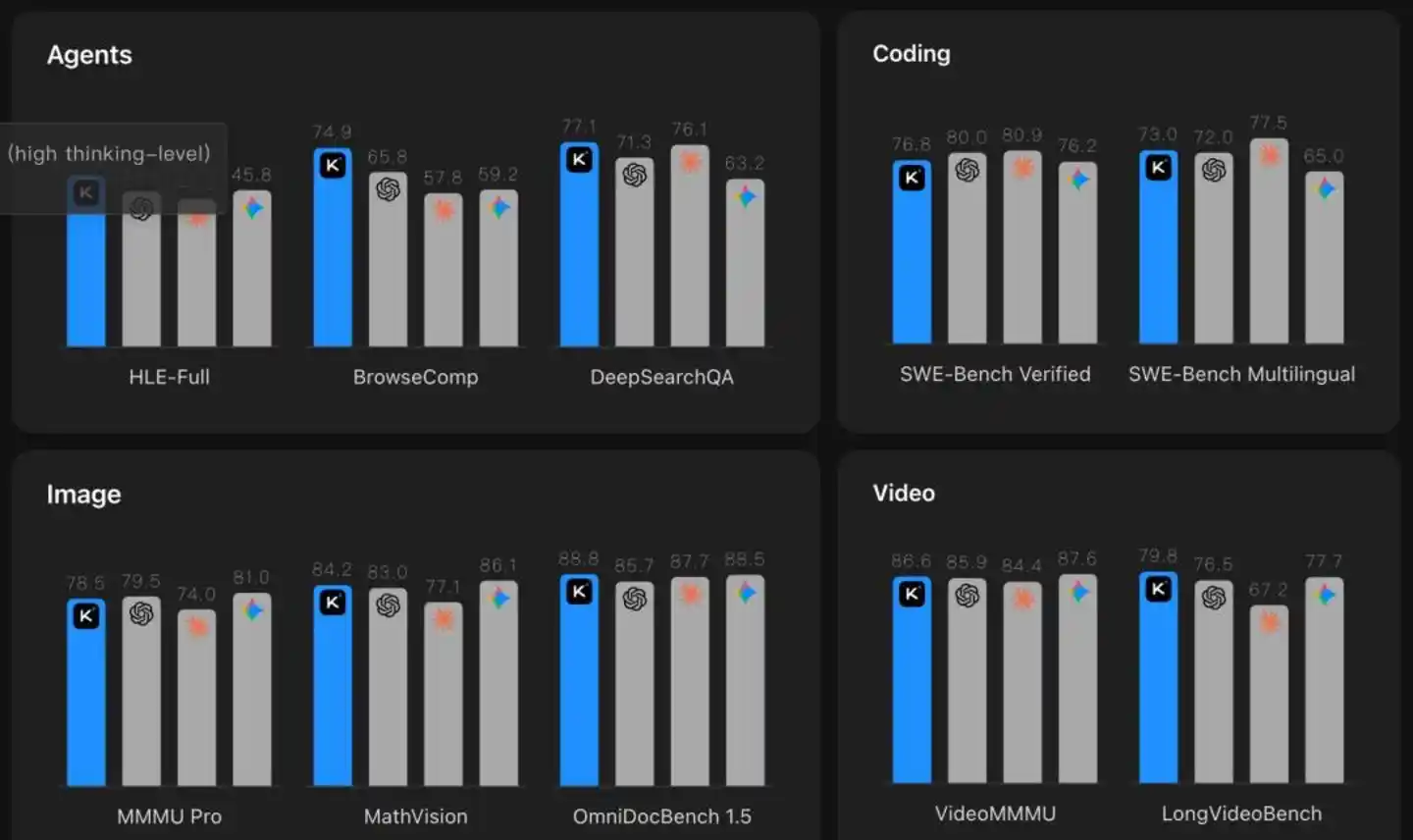

DeepSeek V4 в оценке Vals AI по способностям к коду занял первое место среди открытых исходных кодов и девятое в мире, по сравнению с предыдущим поколением V3.2 произошёл примерно 10-кратный скачок производительности. В оценке Agentic Coding, качество поставки V4-Pro близко к режиму без размышлений Claude Opus 4.6, опыт использования превосходит Sonnet 4.5. Что ещё важнее — стоимость: вывод V4 Flash требует всего 0,28 доллара за миллион токенов, что составляет примерно 1% от Claude Opus. Согласно расчётам сообщества разработчиков, ежемесячная стоимость использования V4 Flash может составлять всего 504 доллара, тогда как стоимость аналогичного объёма использования Kimi примерно в 8 раз, а GLM — в 4 раза выше. Такой уровень преимущества в стоимости практически сокрушителен в ценовой войне API.

Однако сторонние оценки также показывают, что DeepSeek V4 всё ещё отстаёт от ведущих мировых моделей. В общем рейтинге Arena.ai V4 занимает 14-е место, по-прежнему отставая от передовых моделей, таких как GPT-5.4, Claude Opus 4.6. По текстовым способностям занимает 20-е место, многомодальность — слабое место V4. Как прокомментировало сообщество разработчиков: «Занять первое место среди открытых исходных кодов уже не сюрприз, все надеются увидеть, как DeepSeek сможет соперничать с сильнейшими ИИ из "большой тройки"».

Проще говоря, «Четыре дракона» сейчас делают две вещи одновременно: первое — догнать по возможностям моделей, второе — снизить стоимость вывода. Первое определяет, готовы ли клиенты использовать, второе — определяет, сколько клиенты могут себе позволить использовать. Если оба пункта выполнены, выручка — это не вопрос «есть ли она», а вопрос «как быстро она растёт».

Конечно, проблема в том, что убытки также растут одновременно. Расходы на НИОКР Zhipu в 2025 году составили 439% от выручки, скорректированный чистый убыток MiniMax — 250 миллионов долларов. Для большинства предприятий такая скорость сжигания денег неустойчива — но «Четыре дракона» как раз и являются тем особым образцом вне этого «большинства». Их логика проста: сначала создать технологический разрыв, затем построить преимущество в стоимости, и только потом наступает время подсчётов.

Анонс продукта Agent Kimi OK Computer, Рис./Сайт Moonshot AI

3. Смешанная война больших и малых компаний: холодные размышления за карнавалом

Чем выше растёт оценка «Четырёх драконов», тем сложнее настроение у интернет-гигантов.

13 мая 2026 года Tencent провела общее собрание акционеров. Согласно сообщению National Business Daily, на вопрос о прогрессе в бизнесе ИИ Ма Хуатэн сказал следующее: «Год назад мы думали, что сели на корабль, потом обнаружили, что тот корабль течёт, теперь чувствуем, что поднялись на него, но ещё не можем сесть, всё ещё надеемся, что скорость корабля увеличится». В тот же день Alibaba опубликовала квартальную отчётность, генеральный директор У Юнмин на телеконференции заявил: «Первый квартал 2026 года для Alibaba — это квартал, где "посев" значительно превосходит "урожай"».

Два больших босса, один говорит «корабль течёт», другой — «посев больше, чем урожай». В любой другой отрасли инвесторы, возможно, не оценили бы это. Но на трассе ИИ рынок, наоборот, встречает это понимающими аплодисментами — потому что все знают, что это битва, которую нельзя проиграть.

Tencent вложила 18 миллиардов юаней в новые продукты ИИ в 2025 году, в 2026 году планирует как минимум удвоить инвестиции. В четвёртом квартале 2026 финансового года (первый квартал 2026 календарного года) скорректированный EBITA Alibaba упал на 84%, Non-GAAP чистая прибыль почти исчезла, деньги были вложены в инфраструктуру ИИ. Что получили два гиганта взамен огромных инвестиций? Получили трёхзначный рост доходов от ИИ в облачном бизнесе, получили экспоненциальный рост вызовов моделей — но до настоящего «урожая», очевидно, ещё далеко.

Метафора Ма Хуатэна «корабль течёт» точно описывает путь Tencent за последний год. Когда в начале 2025 года взорвался DeepSeek, Tencent быстро подключила свою внешнюю модель к своему ИИ-ассистенту «Yuanbao», который на некоторое время возглавил бесплатные чарты магазинов приложений. Но после шума выявились проблемы: ранняя модель Hunyuan имела недостаточную комплексную способность к внедрению, коэффициент удержания приложения Yuanbao за 30 дней составил всего 18,7%, 18 миллиардов юаней, вложенные в 2025 году, в основном были направлены на доходы, затраты и расходы новых продуктов ИИ, что сократило операционную прибыль Tencent в первом квартале 2026 года на 8,8 миллиарда юаней. «Корабль» Tencent действительно тек, но теперь они пересели на новый корабль и отправились заново.

Для «Четырёх драконов» тревога гигантов как раз и является возможностью. Tencent ведёт переговоры об инвестировании в DeepSeek, Alibaba неоднократно инвестировала в Kimi, Meituan Longzhu лидировал в последнем раунде финансирования Kimi — гиганты, с одной стороны, сами тратят деньги на создание моделей, с другой стороны, инвестируют, чтобы «купить билет на поезд». Эта стратегия «двойного страхования» говорит об одной проблеме: никто не может быть уверен наверняка. Гиганты не знают, сможет ли их модель выйти вперёд, поэтому инвестируют в «Четырёх драконов», чтобы хеджировать риски; «Четыре дракона» также не знают, смогут ли они самостоятельно дойти до финиша, поэтому с радостью принимают деньги и ресурсы гигантов. Обе стороны получают то, что им нужно, но как долго продлится эта тонкая конкурентно-партнёрская динамика, никто не знает.

Но за этим карнавалом есть несколько настораживающих сигналов.

Первый сигнал: окно уникальности закрывается. В отчёте JPMorgan чётко указано, что если Kimi и StepFun выйдут на IPO, влияние на Zhipu и MiniMax будет аналогично случаю с Cambricon — краткосрочный приток капитала от деятельности IPO, но премия за уникальность каждой компании структурно снизится. Перевод: нынешние заоблачные оценки частично объясняются тем, что «выбора нет», когда выбор появится, цены естественным образом вернутся к рациональности.

Второй сигнал: узкое место вычислительной мощности. Согласно данным «Народной газеты», среднесуточный объём использования токенов в Китае превысил 140 триллионов, но все основные поставщики LLM заявляют, что вычислительные мощности для вывода не поспевают за ростом спроса. Это приводит к неинтуитивному выводу: нынешние темпы роста ARR на самом деле являются нижним пределом, а не верхним — как только узкое место вычислительной мощности будет устранено, подавленный спрос может напрямую превратиться в подтверждённый доход. Alibaba Cloud уже 18 апреля объявила о повышении цен на вычисления ИИ на 34%, цены на API Zhipu с начала года практически удвоились — рост цен при сохранении высокого спроса показывает, что ценовая политика действительно переходит к производителям моделей, но также означает, что стоимость вычислительной мощности в конечном итоге станет узким местом для всей отрасли.

Третий сигнал самый тонкий: низкозатратный путь DeepSeek по сути является «снижением размерности удара». Для большинства предприятий, экономия на вычислениях за счёт глубокой оптимизации одного звена эффективна в краткосрочной перспективе, но в долгосрочной перспективе потолок очевиден. Стоимость DeepSeek V4 Flash составляет всего 1/4-1/8 от стоимости конкурентов, это преимущество проистекает из инженерной оптимизации и адаптации к отечественным чипам, а не из бесконечного снабжения вычислительными ресурсами. Как только в цепочке поставок вычислительной мощности возникнут колебания или конкуренты догонят в инженерной оптимизации, преимущество в стоимости будет ослаблено.

История «Четырёх драконов», в конечном счёте, является четырьмя версиями одной и той же истории: использовать огромные инвестиции для поддержки интенсивных НИОКР, использовать технологические итерации для стимулирования роста доходов, использовать рост доходов для поддержки более высокой оценки, а затем использовать более высокую оценку для привлечения большего финансирования. Если этот цикл заработает, это будет следующая Microsoft; если он рухнет, это будет следующий WeWork.

Разница в том, что на этот раз государственная сила глубоко вмешалась. Государственный фонд лидирует в инвестициях в DeepSeek, China Mobile участвует в финансировании Kimi, государственные капиталы перестали быть «зрителями», а стали «главными героями». Это означает, что выживание «Четырёх драконов» — уже не только коммерческий вопрос, но и стратегический.

Карнавал продолжается, но счёт рано или поздно придётся оплатить. Для инвесторов сейчас вопрос в следующем: когда окно уникальности закроется и премия за уникальность исчезнет, смогут ли эти высокооценённые компании поддержать свою рыночную капитализацию собственными доходами?

Ответ может стать ясным в течение следующего года.