На рынках опционов хеджирующие потоки дилеров играют ключевую роль в формировании краткосрочного ценового поведения. Гамма-экспозиция (GEX) используется для определения того, где эти хеджирующие потоки, вероятно, стабилизируют ценовое действие, а где могут усиливать движения. Хотя GEX хорошо зарекомендовала себя в акционных и индексных опционах, прямое применение её к крипторынкам проблематично.

Крипто-опционы существенно отличаются по поведению участников, мотивации сделок и доступности данных. Чтобы учесть это, мы воссоздаём меру GEX, основанную на потоках и адаптированную для рынков крипто-опционов, предназначенную для отслеживания эволюции позиционирования дилеров по страйкам и срокам экспирации. Мы показываем, как эту структуру можно использовать для интерпретации режимов волатильности и определения ценовых зон, где хеджирование дилеров может существенно повлиять на рыночную динамику.

Что такое гамма-экспозиция и почему это важно

Гамма-экспозиция (GEX) измеряет, как хеджирующие потоки маркет-мейкеров опционов реагируют на движения базового актива.

Маркет-мейкеры, которые обычно поддерживают дельта-нейтральные позиции, должны постоянно хеджировать свою гамма-экспозицию, покупая или продавая фьючерсы или спот, чтобы компенсировать дельту проданных или купленных ими опционов. Когда цена движется, дельты опционов меняются (это и есть гамма), вынуждая дилеров перебалансироваться. Эти потоки перебалансировки создают структурные петли обратной связи на рынке и являются источником некоторых из наиболее значительных механически обусловленных потоков, наблюдаемых на фондовых рынках.

В основе этой динамики тейкер является конечным пользователем — трейдером или инвестором, покупающим или продающим опционы, в то время как дилер (или маркет-мейкер) — это контрагент, предоставляющий ликвидность. Их позиции являются зеркальным отражением друг друга: когда тейкер покупает колл, дилер его продаёт.

Почему GEX полезна?

- На ценовых уровнях с высокой положительной гаммой дилеры хеджируют таким образом, что это tends to поглощать ценовые шоки. Они обычно покупают на падениях и продают на ростах, что сглаживает волатильность и может удерживать цену near определённых страйков: явление, часто описываемое как «гамма-гравитация» или «приколачивание» (pinning).

- На ценовых уровнях с высокой отрицательной гаммой хеджирующие потоки дилеров работают в противоположном направлении и усиливают ценовые движения. Дилеры продают при падении цен и покупают при росте, часто увеличивая краткосрочную волатильность.

Короче говоря, GEX выделяет области, где хеджирование дилеров, вероятно, стабилизирует или дестабилизирует рынок, превращая поверхность опционов в карту потенциальных режимов волатильности, а не в пассивный снимок позиционирования.

Истоки TradFi: Расчёт гамма-экспозиции в традиционных финансах

Метрики гамма-экспозиции возникли на рынках акционных и индексных опционов (например, SPX). Классическая конструкция такова:

Где:

- OI — это открытый интерес по этому страйку

- Γ — гамма опциона

- S — спотовая цена базового актива

- sign_dealer — предполагаемый знак позиции дилера (лонг или шорт)

Поскольку традиционные наборы данных по акциям не маркируют, кто является тейкером в сделке, эта структура опирается на простое эвристическое правило о том, кто обычно держит какую сторону рынка опционов:

- Колл-опционы продаются инвесторами и покупаются дилерами

- Пут-опционы покупаются инвесторами и продаются дилерами

В классическом контексте фондового рынка инвесторы обычно пишут коллы для увеличения доходности и используют путы в качестве страховки от падения.

Почему эвристика фондового рынка не работает в крипто

В крипто-опционах предположения в стиле фондового рынка не работают. Большая доля участников активно покупает коллы для спекуляции на росте, а не систематически продаёт их для получения дохода. В то же время путы часто торгуются тактически, а не используются исключительно в качестве хеджей для лонг-онли портфелей. Если мы продолжим предполагать, что «коллы = инвестор в шорте, дилер в лонге» и «путы = инвестор в лонге, дилер в шорте», мы построим профиль дилера, который не отражает фактическое позиционирование.

Есть вторая, более тонкая проблема. Классический подход рассматривает открытый интерес по каждому страйку как единый блок позиции с одним знаком. На практике OI страйка формируется как из потоков покупки, так и продажи тейкерами. В простом случае, когда 50% OI поступило от тейкеров, покупающих (дилеры в шорте), и 50% от тейкеров, продающих (дилеры в лонге), чистая экспозиция дилера близка к нулю — однако эвристика всё равно покажет большую экспозицию. Вместо этого нам фактически нужно:

- Реалистичное определение знака позиционирования дилера (лонг vs шорт);

- Реалистичный чистый размер этой позиции после неттинга противоположных потоков.

Подход, ориентированный на потоки, к гамма-экспозиции (GEX) в крипто

В отличие от традиционных фондовых рынков, площадки крипто-опционов раскрывают, кто является тейкером в каждой сделке. Для каждой транзакции мы можем наблюдать, покупал или продавал тейкер колл или пут. Затем мы делаем чёткое модельное предположение: мейкер на другой стороне сделки — это дилер, предоставляющий ликвидность.

Это позволяет нам рассматривать тейкера как конечного пользователя и выводить позиционирование дилера как зеркальное отражение совокупного потока тейкеров, страйк за страйком и срок экспирации за сроком. Со временем это создаёт реалистичную картину того, как дилеры позиционированы по всей волатильной поверхности.

На этой основе мы строим методологию, которая отслеживает инвентарь дилера во времени и преобразует этот инвентарь в гамма-экспозицию с использованием греков опционов и спотовой цены. В результате получается структурная мера GEX, основанная на фактических торговых потоках, а не на статических эвристиках. Полное описание этого процесса приведено в Приложении в конце.

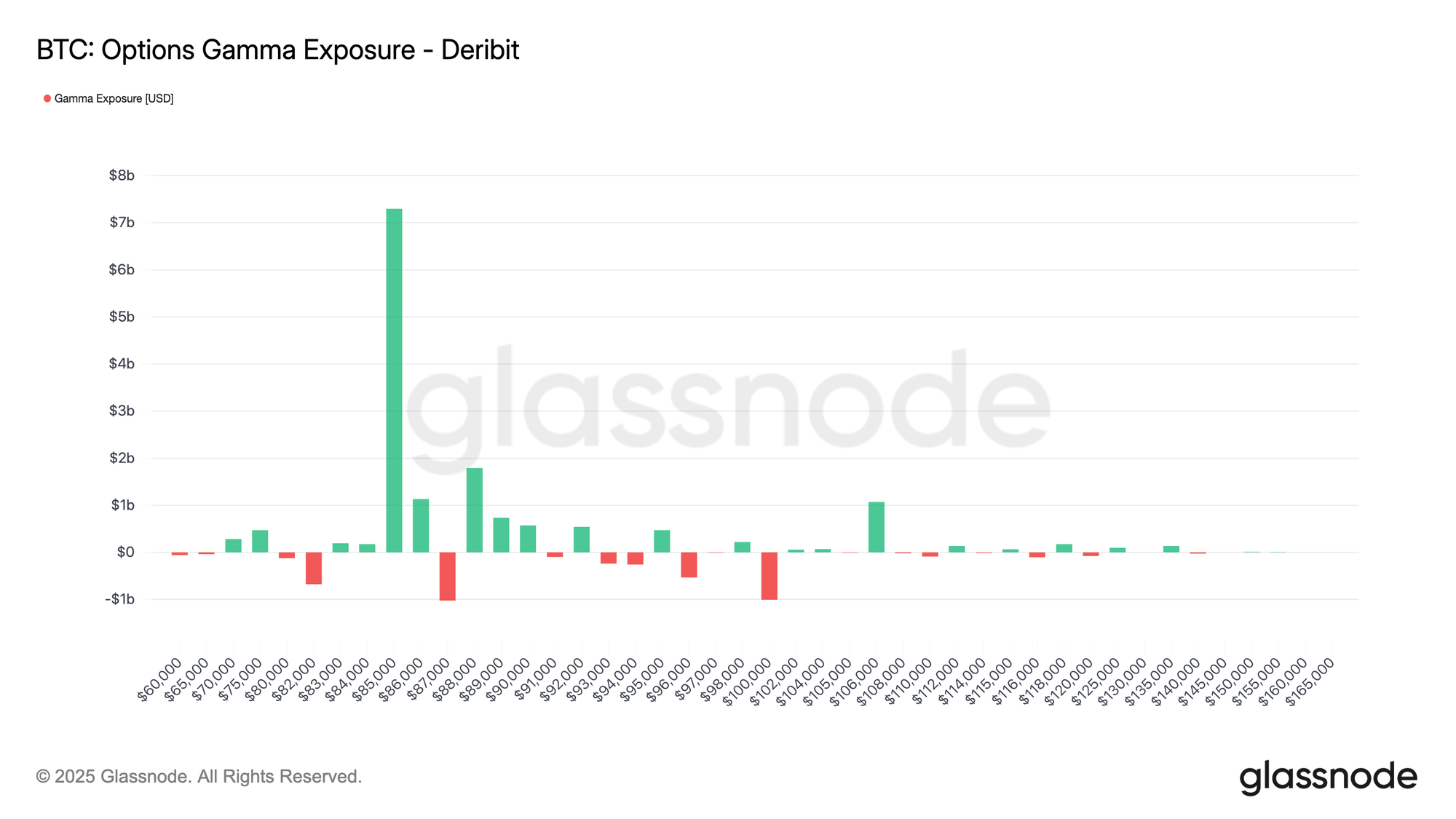

На приведённом ниже графике показана гамма-экспозиция опционов BTC по страйкам на Deribit. Каждый столбец представляет собой чистую гамма-экспозицию (в USD), сконцентрированную на этом страйке: зелёный цвет указывает на положительную экспозицию, красный — на отрицательную. Распределение показывает доминирующий кластер положительной гаммы вокруг ~$86k–$87k, с меньшими карманами отрицательной экспозиции вокруг ~$83k и ~$101k.

Интерпретация метрики

Гамма-экспозиция помогает определить, где хеджирующие потоки могут повлиять на ценовое действие. Большая положительная GEX near ~$85k–$86k suggests зону, где хеджирование дилеров, вероятно, будет mean-reverting (покупка на падениях и продажа на ростах), способствуя приколачиванию или более медленному движению цены вокруг этих страйков. Напротив, карманы отрицательной GEX отмечают области, где хеджирование становится усиливающим импульс (продажа в слабость / покупка в силу), увеличивая вероятность более быстрых, более направленных движений, если спот торгуется в них.

Доступно для:

- Разрешение: 10-минутное

- Активы: BTC, ETH, SOL, XRP, PAXG

- Биржи: Deribit

Торговые варианты использования: Как использовать GEX на практике

С торговой точки зрения, GEX превращает поверхность опционов в карту того, где потоки дилеров, вероятно, усилят или ослабят ценовые движения.

Определение «липких» vs «скользких» ценовых зон

- Высокая положительная GEX near спота: Когда GEX сильно положительна вокруг полосы страйков near спота, дилеры находятся в лонге по гамме в этой зоне. Поскольку рынок торгуется внутри этой полосы, их хеджирующие потоки tend to покупать на падениях и продавать на ростах, что создаёт эффект приколачивания: движения затухают, пробои struggle, а реализованная волатильность often оказывается ниже implied. Это typically mean-reverting, «липкий» режим, где шорт-гамма керри-сделки могут работать, если волатильность действительно остаётся сдержанной.

- Высокая отрицательная GEX near или below спота: Когда GEX сильно отрицательна around или just below спота, верно обратное: дилеры в шорте по гамме, поэтому, когда спот торгуется в этом регионе, хеджирующие потоки продают в слабость и покупают в силу. Вместо того чтобы сглаживать движения, они усиливают их. Ценовое действие становится более «скользким»: внутридневные колебания могут расширяться, стаканы могут казаться тоньше, а ликвидации или squeezes становятся более вероятными. В этой среде трейдеры often реагируют снижением leverage, более широкими стопами и большим уважением к моментум.

Наблюдение за гамма-переворотами

Особенно важной динамикой является гамма-переворот, когда чистая GEX around спота меняет знак. Например, если цена выходит из зоны положительной гаммы и перемещается в карман отрицательной гаммы ниже, рынок может перейти от приколоченного, mean-reverting режима к тому, где движения начинают самоусиливаться.

Приложение – Наша методология: GEX на основе потока тейкеров

Мы строим Гамма-Экспозицию на 10-минутной сетке для каждого актива, биржи, страйка K, срока экспирации M. Ключевая идея — восстановить инвентарь дилера с течением времени из потоков тейкеров, а затем преобразовать этот инвентарь в гамма-экспозицию с использованием греков опционов.

Мы определяем чистый поток тейкеров в контрактах за каждый 10-минутный интервал:

В предположении, что дилеры в основном на пассивной стороне, поток дилеров является просто зеркальным отражением потока тейкеров:

Затем мы аккумулируем эти потоки с течением времени, чтобы получить инвентарь дилера в количестве контрактов. Для коллов это:

и аналогично для путов:

Здесь Δt — это 10-минутный шаг. Положительные значения инвентаря соответствуют тому, что дилеры находятся в чистом лонге по контрактам на этом страйке и сроке экспирации; отрицательные значения соответствуют чистому шорту.

Чтобы преобразовать этот инвентарь в гамма-экспозицию, мы combine it с греками опционов и ценой базового актива. Пусть m обозначает множитель контракта (например, BTC за контракт), а S — спотовая цена в момент времени t. Для каждого бакета мы определяем нотиональную экспозицию:

Используя гаммы опционов Γcall(K,M,t) и Γput(K,M,t) из нашей опционной цепи, гамма-экспозиция каждого плеча составляет:

Γcall(K,M,t) — это гамма колл-опциона на этом страйке и сроке экспирации. Это показывает, как быстро дельта опциона меняется при движении базовой цены.

И тогда общая гамма-экспозиция на этом страйке/сроке экспирации просто: