15 декабря 2025 года по американскому времени Nasdaq официально подала в SEC форму 19b-4 с просьбой продлить время торговли акциями и биржевыми продуктами до 23/5 (23 часа в день, 5 дней в неделю).

Однако заявленное Nasdaq время торговли — не просто продление, а изменение на две официальные торговые сессии:

Дневная торговая сессия (с 4:00 до 20:00 по восточному времени) и ночная торговая сессия (с 21:00 до 4:00 следующего дня по восточному времени). При этом с 20:00 до 21:00 торговля приостанавливается, и все неисполненные ордера в это время аннулируются.

Многие читатели, увидев новость, обрадовались, подумав, не готовится ли США к круглосуточной токенизированной торговле акциями? Но, внимательно изучив документ, Crypto Salad хочет сказать: не спешите с выводами, потому что Nasdaq в документе указывает, чтомногие традиционные правила торговли ценными бумагами и сложные ордера не применяются в ночной торговой сессии, некоторые функции также будут ограничены.

Мы всегда очень внимательно следили за токенизацией акций США — это один из важнейших объектов токенизации активов, особенно на фоне множества официальных действий SEC (Комиссии по ценным бумагам и биржам США) в последнее время.

Эта заявка вновь вызвала ожидания относительно токенизации акций США, потому что США хотят сделать большой шаг к сближению времени торговли ценными бумагами с круглосуточным режимом рынка цифровых активов.Однако, если присмотреться:

В этом документе Nasdaq вообще не упоминается о токенизации, речь идет только о реформе системы для традиционных ценных бумаг.

Если вы хотите глубже понять действия Nasdaq, Crypto Salad может написать отдельную статью с подробным разбором. Но сегодня мы хотим поговорить о реальных новостях, связанных с токенизацией акций США —

SEC официально «разрешила» гиганту-кастодиану США экспериментировать с предоставлением услуг токенизации.

------【Разделитель】------

11 декабря 2025 года по американскому времени сотрудники Отдела торговли и рынков SEC направили DTCC«Письмо о неприменении мер (No-Action Letter, NAL), которое затем было опубликовано на официальном сайте SEC. В письме четко указано, чтопри соблюдении определенных условий SEC не будет предпринимать принудительных мер в отношении DTC за предоставление услуг токенизации, связанных с его кастодиальными ценными бумагами.

На первый взгляд, многие читатели подумали, что SEC официально «освободила» от использования технологии токенизации для акций. Но при ближайшем рассмотрении реальность сильно отличается.

Так что женаписано в этом письме? До какого этапа дошло последнее развитие токенизации акций США?Давайте начнем с главного героя письма:

1. Кто такие DTCC и DTC?

DTCC, полное название Depository Trust & Clearing Corporation, — это групповая компания США, в которую входят различные учреждения, отвечающие за хранение, клиринг акций и клиринг облигаций.

DTC, полное название Depository Trust Company, — дочерняя компания DTCC, крупнейший в США центральный депозитарий ценных бумаг, отвечающий за хранение акций, облигаций и других ценных бумаг, а также за расчеты и перевод прав. В настоящее время объем хранимых и учитываемых активов ценных бумаг превышает 100 триллионов долларов,можно понять DTC как администратора бухгалтерской книги всего рынка акций США.

2. Какое отношение DTC имеет к токенизации акций США?

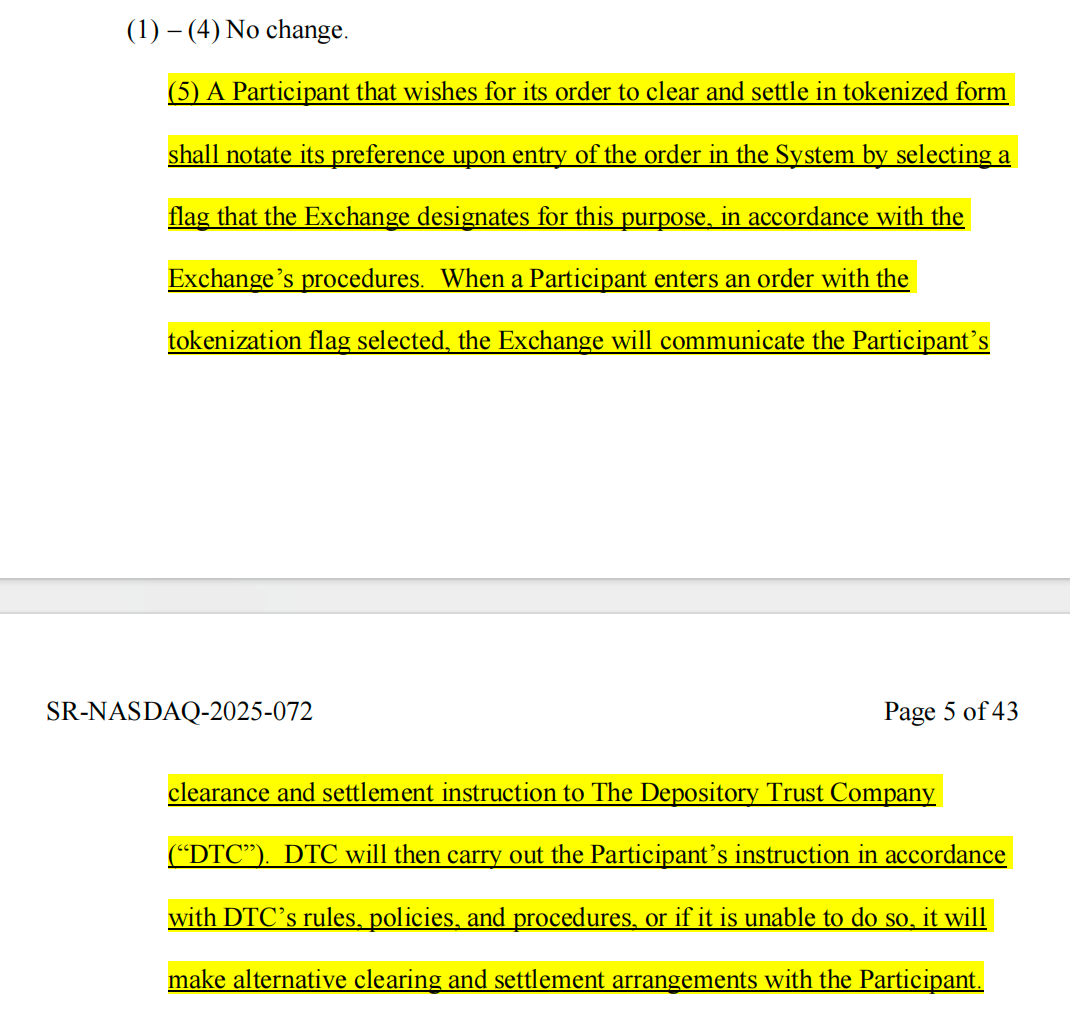

Помните новость начала сентября 2025 года, когда Nasdaq подала заявку в SEC на выпуск акций в токенизированной форме? В той заявке уже фигурировал DTC.

Nasdaq заявила, что единственное отличие токенизированных акций от традиционных заключается в клиринге и расчетах ордеров в DTC.

(Скриншот из заявки Nasdaq)

Чтобы сделать это более понятным, мы нарисовали блок-схему, синяя часть — это то, что Nasdaq хотела изменить в своей заявке в сентябре. Можно четко увидеть, что DTC является ключевым исполнительным и практическим учреждением токенизации акций США.

3. О чем говорится в новом «Письме о неприменении мер»?

Многие напрямую приравнивают этот документ к согласию SEC на использование DTC блокчейна для учета акций США, но это не совсем точно. Чтобы правильно понять это, мы должны знать один пункт в американском Законе о биржевой торговле:

Статья 19(b) Закона о биржевой торговле 1934 года (Securities Exchange Act of 1934) гласит, что любая саморегулируемая организация (включая клиринговые учреждения) при изменении правил или значительных деловых договоренностей должна подать в SEC заявку на изменение правил и получить одобрение.

]Обе заявки Nasdaq были поданы на основании этого положения.

Однакопроцесс подачи заявки на изменение правил обычноочень]долог, может затянуться на месяцы, до240дней. Если каждое изменение требует подачи заявки и одобрения, временные затраты будут слишком велики. Поэтому,чтобы обеспечитьпроведение своегопилотного проекта по токенизации ценных бумаг, DTCпопросил освободить себя от обязанности полностью соблюдать процесс подачи заявки 19b в пилотный период, SECдала на это согласие.

То есть,]SECлишь временно освободилаDTCот части процессуальных обязанностей по подаче заявок, а не дала существенного разрешения на применение технологии токенизации на рынке ценных бумаг.

---【Разделитель】---

Как же дальше будет развиваться токенизация акций США? Нам нужно разобраться со следующими двумя вопросами:

(1) Какие пилотные мероприятия DTC может проводить без подачи заявки?

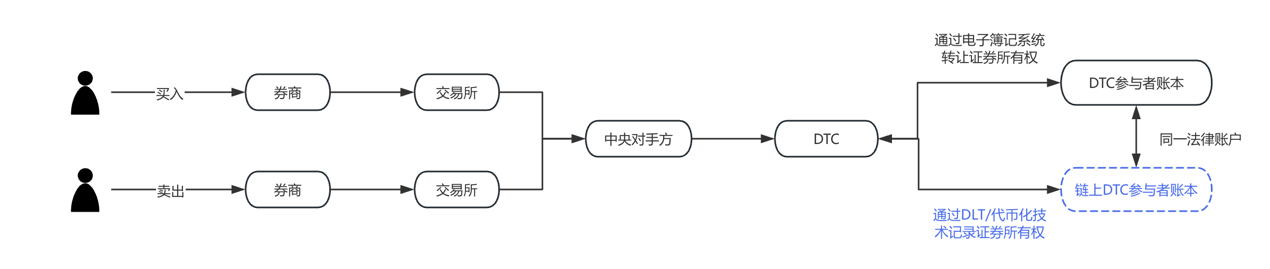

В настоящее время кастодиальный учет акций США работает по такой модели: предположим, у брокера есть счет в DTC, DTC будет использовать централизованную систему для записи каждой купленной и проданной акции и доли. На этот раз DTC предложил: можем ли мы предоставить брокерам выбор, чтобы записать эти записи о владении акциями еще раз с помощью токенов блокчейна?

Практически, сначала участники регистрируют квалифицированный, одобренный DTC кошелек (Registered Wallet). Когда участник отправляет в DTC инструкцию по токенизации, DTC делает три вещи:

a) Перемещает эти акции с исходного счета в общий пул;

b) Чеканит токен в блокчейне;

c) Переводит токен на кошелек этого участника, представляя права этого участника на эти ценные бумаги.

После этогоэти токены могут напрямую передаваться между этими брокерами без необходимости каждый раз проходить через централизованный реестр DTC. Однако все передачи токенов будут отслеживаться и записываться DTC в режиме реального времени через систему LedgerScan, работающую вне блокчейна, и записи LedgerScan будут составлять официальную бухгалтерскую книгу DTC. Если участник хочет выйти из состояния токенизации, он может в любое время отправить в DTC инструкцию «детокенизации», DTC уничтожит токен и вернет права на ценные бумаги обратно на традиционный счет.

В NAL также подробно описаны технические и риск-контрольные ограничения, включая: токены могут передаваться только между кошельками, одобренными DTC, поэтому DTC даже имеет право при определенных обстоятельствах принудительно передать или уничтожить токены в кошельке, системы токенов и основные клиринговые системы DTC строго изолированы и т.д.]

(2) В чем значение этого письма?

С юридической точки зрения, Crypto Salad хочет подчеркнуть, что NAL не эквивалентно юридическому授权(разрешению) или изменению правил, оно не имеет общеобязательной юридической силы, а лишь отражает позицию сотрудников SEC в отношении правоприменения при определенных фактах и условиях.

В американской системе законодательства о ценных бумагах не существует отдельного положения «запрещающего использование блокчейна для учета». Регулирование больше关注(обращает внимание) на то, соблюдаются ли после внедрения новых технологий существующая рыночная структура, кастодиальные обязанности, риск-контроль и обязанности по подаче заявок.

Кроме того, в американской системе регулирования ценных бумаг такие письма, как NAL, долгое время рассматривались как важный индикатор регуляторной позиции, особенно когда объектом являются системно значимые финансовые учреждения, такие как DTC, их символическое значение фактически больше, чем сама конкретная деятельность.

------【Разделитель】------

Судя по раскрытому содержанию, предпосылка освобождения SEC на этот раз очень ясна: DTC не выпускает и не торгует ценными бумагами напрямую в блокчейне, а токенизирует представление прав на существующие ценные бумаги в своей кастодиальной системе.

Этот токен фактически является «отображением прав» или «выражением в реестре», используемым для повышения эффективности обработки в бэк-офисе, а не для изменения юридических атрибутов или структуры владения ценными бумагами. Соответствующие услуги работают в контролируемой среде и на разрешенном блокчейне, участники, scope(сфера) использования и техническая архитектура строго ограничены.

Crypto Salad считает, что такая регуляторная позиция очень разумна. Легче всего в активах в блокчейне возникают отмывание денег, незаконное集资(привлечение средств) и другие финансовые преступления, технология токенизации — это новая технология, но она не должна быть пособником преступлений. Регуляторам необходимо, признавая потенциал применения блокчейна в инфраструктуре ценных бумаг, придерживаться границ существующего законодательства о ценных бумагах и кастодиальной системы.

4. Последний прогресс в развитии токенизации акций США

Обсуждение токенизации акций США начало постепенно переходить от «соответствует ли нормам» к «как реализовать». Если разобрать текущую практику на рынке, можно увидеть, что формируются как минимум два параллельных, но логически разных пути:

· Представленный DTCC и DTC, этопуть токенизации,主导(ведущий) официальным мнением,его основная цель — повысить эффективность расчетов, сверки и流转та(оборота) активов, обслуживая в основном институциональных и оптовых участников рынка. В этой модели токенизация几乎是(почти) «невидима», для конечного инвестора акции остаются акциями, просто backend(бэк-офисная) система прошла техническое обновление.

· В противовес этому —возможная前端(фронтенд) роль брокеров и торговых платформ. Например, Robinhood, MSX Maitong в последние годы持续(постоянно) исследуют продукты в области加密(крипто) активов, фрагментированной торговли акциями и продления времени торговли. Если токенизация акций США постепенно созреет с точки зрения соответствия нормам, такие платформы天然(естественно) обладают преимуществом стать пользовательским входом. Для них токенизация не означает перестройку бизнес-модели, а скорее может быть техническим расширением существующего инвестиционного опыта, например, более接近(приближенное) к реальному времени расчеты, более гибкое дробление активов и интеграция межрыночных продуктовых форм. Конечно, все это при условии постепенного прояснения регуляторных рамок. Такие исследования обычно идут near(рядом) с регуляторными границами, риск и инновации сосуществуют, их ценность заключается не в краткосрочном масштабе, а в проверке形态(формы) рынка ценных бумаг следующего поколения. С практической точки зрения, они更像是提供(предоставляют) образцы для институциональной эволюции, а не直接替代(прямо заменяют) существующий рынок акций США.

Чтобы было более直观но(наглядно), можно посмотреть на следующую сравнительную диаграмму:

С более макроэкономической точки зрения, то, что токенизация акций США действительно пытается решить, — это не «превратить» акции в «монеты», а как повысить эффективность оборота активов, снизить операционные расходы и预留(зарезервировать) интерфейсы для будущей межрыночной synergy(синергии) при сохранении юридической определенности и системной безопасности. В этом процессе соответствие нормам, технологии и рыночная структура будут长期(долгосрочно)并行(параллельно)博弈(соревноваться), и путь эволюции必然(непременно) будет постепенным, а не радикальным.

Можно预期(ожидать), что токенизация акций США не изменит коренным образом способ работы Уолл-стрит в краткосрочной перспективе, но она уже является важным项目(проектом) в повестке дня финансовой инфраструктуры США. Это взаимодействие SEC и DTCC больше похоже на «пробы» на институциональном уровне, очерчивающие初步(предварительные) границы для последующих более широких исследований. Для участников рынка это, возможно, не конечная точка, а отправная точка, за которой стоит持续(постоянно)观察(наблюдать).