От редактора: Когда ИИ начинает писать код, обрабатывать заявки в службу поддержки, проверять юридические документы, возникает более фундаментальный вопрос: что на самом деле покупают компании — токены, GPU-часы или выполненную работу?

В этой статье предлагается заслуживающая внимания концепция: коммерциализацию ИИ не стоит понимать только как «рынок вычислительных мощностей» или «рынок вызовов моделей». Она движется к новому «рынку машинизированной рабочей силы». На этом рынке токены — лишь единица измерения, GPU — ресурсы, модели — средства производства. А реальным объектом ценообразования и торговли становится экономически полезный труд, непосредственно выполняемый программным обеспечением.

Ключевой вывод статьи заключается в том, что механизм ценообразования на ИИ пройдет путь от сырых токенов и стандартизированных возможностей моделей к отраслевой рабочей силе и далее — к рынку программируемых результатов. Иначе говоря, в будущем компании, возможно, перестанут заботиться о том, какая именно модель или какие GPU выполняют задачу. Их будет интересовать, достигнут ли результат в рамках установленных требований к задержкам, точности, надежности и стоимости.

Это также означает, что влияние ИИ на рынок человеческого труда не обязательно сводится к простому замещению. По мере того как машины берут на себя все больше стандартизируемой и проверяемой работы, роль человека может сместиться в сторону контроля, принятия ответственности, управления контекстом и итогового суждения. В некоторых сценариях именно эти последние 1% человеческого решения могут стать гораздо ценнее, потому что они высвобождают 99% возможностей для массовой автоматизации.

С этой точки зрения, следующая фаза конкуренции на рынке ИИ, возможно, будет заключаться уже не просто в соревновании возможностей моделей или в ценовой войне за вычислительные мощности, а в том, кто первым сможет стандартизировать, проверить и оценить «работу», превратив машинизированную рабочую силу в новый тип производственного фактора, который можно закупать, учитывать и обменивать.

Далее следует оригинальный текст:

Волны роста производительности всегда были связаны с созданием для человека инструментов и программного обеспечения, оптимизирующих способы выполнения работы. Электронные таблицы помогали бухгалтерам и аналитикам, конвейерные ленты увеличивали пропускную способность, молоток усиливал рычаг человека. Но настоящий труд всегда исходил от людей.

Сейчас ИИ начинает выполнять работу от начала до конца, непосредственно осуществляя сам труд. Он может писать код, обрабатывать заявки в службу поддержки, проверять юридические документы. Нижний уровень технологического стека сжимается: старый стек технологий поддерживал труд, новый начинает производить труд.

Если вы недавно слышали дискуссии о финансовой стороне ИИ, наверняка слышали от Дженсена и других, что токены LLM и/или GPU-часы становятся новыми товарными продуктами. Эта интуиция понятна, потому что токены можно измерить, выставить счет, легко представить на графике; за GPU-часами также стоят миллиарды долларов инвестиций. Но токены — это лишь счетчики, GPU-часы — лишь ресурсы, никто не покупает их ради обладания ими самими. Люди на самом деле хотят, чтобы работа была выполнена. ИИ превращает сам технологический стек в источник рабочей силы.

Машинизированная рабочая сила: работа, выполняемая программным обеспечением, имеющая экономическое назначение и продаваемая в производственный процесс.

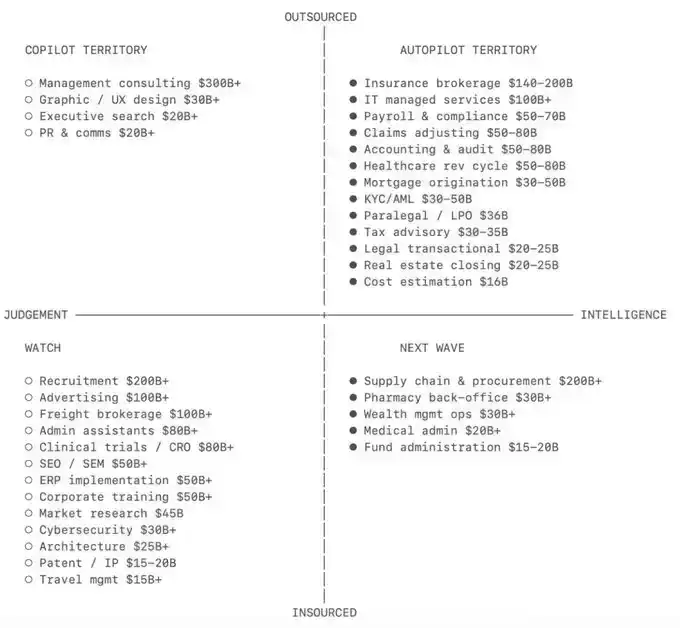

Рынок уже движется в этом направлении. Сара Тавел из Benchmark склонна понимать эту возможность через призму рынков аутсорсинга рабочей силы, а не через категории программного обеспечения. Если некую повторяющуюся задачу обычно выполняет специализированная офшорная команда или профессиональная сервисная компания, то, вероятно, это подходящая работа для выполнения ИИ. Алекс Рампелл из a16z называет это «программное обеспечение поглощает труд»: следующая глава для ПО — это выполнять работу самостоятельно. Жюльен Бек из Sequoia описывает ту же перемену с другой стороны: услуги превращаются в программное обеспечение, copilot продает инструменты, а autopilot продает работу.

Отсутствующий рынок за ценообразованием по результату

Ценообразование по подписке взимает плату за доступ, ценообразование по токенам — за объем использования. Ценообразование по результату взимает плату, когда работа выполнена. Ценообразование по результату делает шаг вперед, но все же не отвечает на вопрос: кто определяет цену?

Если машинизированную рабочую силу можно покупать напрямую, цена должна формироваться в результате конкуренции между поставщиками. Эти поставщики должны быть способны выполнять один и тот же тип задач или соответствовать одним и тем же стандартам выполнения работы, а для этого необходима стандартизация внутри различных отраслей и задач.

Сегодняшний подход — использование токенов LLM, но сырые токены — это лишь самый нижний уровень. Баррель нефти — лишь единица измерения, реально торгуются баррели нефти определенного сорта с четкими характеристиками качества, условиями поставки и рыночной ценой. Баррель нефти марки Brent и баррель высокосернистой тяжелой нефти — не один и тот же товар. Так же и с токенами LLM. Токен — лишь единица измерения, важно то, какая интеллектуальная способность за ним стоит: качество модели, минимальные показатели в бенчмарках, задержка, размер контекстного окна, надежность и гарантии выполнения. Миллион токенов от передовой модели для генерации кода и миллион токенов от дешевой универсальной модели — не один и тот же товар. Рынку нужны стандартизированные уровни вывода (inference), как энергетическому рынку нужны стандартизированные сорта нефти.

Анджали Шрива прямо указывает на это: токен — не фиксированная единица затрат. Его экономика меняется в зависимости от длины контекста, структуры задачи, соотношения ввода/вывода, количества повторных попыток, вызовов инструментов и рабочих процессов агентов. Один токен в коротком промпте и один токен, погребенный в длинном цикле работы агента, — это не один и тот же экономический объект.

На рынке человеческого труда мы давно так поступаем. Никто не нанимает врача-рентгенолога как обобщенные «человеко-часы». Смотрят на образование, сертификаты, специализацию, стаж, доступность, репутацию, ответственность и т.д. Разные спецификации человеческих контрактов соответствуют разным минимальным стандартам и ожиданиям от уровня.

Рынок человеческого труда и так функционирует на основе этих спецификаций, просто они часто смешаны, качественны и полны различных прокси-метрик. Машинизированная рабочая сила сделает эти спецификации более явными и количественно измеримыми.

Для LLM или агентов такие показатели, как навыки, опыт, скорость и надежность, можно прописать в контракте напрямую: бенчмарк-оценки, задержка, пропускная способность, размер контекстного окна, максимальная длина вывода, точность использования инструментов, время бесперебойной работы, процент ошибок. Мы можем закупать рабочую силу, опираясь на измеримые ожидания и результаты.

Спецификации контракта TheGrid.ai по сути являются фильтром квалификации плюс ценовая конкуренция за вывод LLM. Поставщик, отвечающий спецификациям, допускается к конкуренции:

Бенчмарк интеллекта ≥ минимум

Задержка ≤ максимум

Пропускная способность ≥ минимум

Время бесперебойной работы ≥ минимум

Процент ошибок ≤ максимум

Как только все поставщики достигают одинакового минимального порога, они начинают конкурировать по цене. Покупатель задает вопрос: какой поставщик сможет предоставить необходимую рабочую силу по наилучшей цене?

Найм врача-рентгенолога в контексте LLM превращается в измеримую задачу: какие LLM способны с высокой квалификацией считывать рентгеновские снимки и выполнять задачу в рамках четко определенных требований к задержке, контекстному окну и другим основанным на результате спецификациям контракта.

Результат — это способ покупателя измерить успех; труд — поставляемая экономическая деятельность; токен — топливо, которое машина потребляет в процессе выполнения работы.

The Grid — это рынок машинизированной рабочей силы.

От токенов к рынку машинизированной рабочей силы

Рынок может назначать цену на ресурсы технологического стека, но чтобы оценивать результат, нужен рынок машинизированной рабочей силы. Покупателю не интересны GPU-часы. Сами конечные точки моделей также нестабильны: их могут переименовать, объявить устаревшими, обернуть в другой интерфейс или просто прекратить поддержку.

Пользователи и ликвидность не любят частых изменений. GPU и модели будут развиваться, но стабильной единицей остается сама работа.

Я считаю, что рынок будет развиваться по следующему пути. С каждым последующим уровнем покупаемый товар становится более абстрактным, более ценным, но и сложнее проверяемым. The Grid должен постепенно подниматься по этой лестнице:

Сырые токены → Рынок товаризированных возможностей LLM → Рынок товаризированной рабочей силы → Рынок программируемых результатов

Первый этап: Сырые токены

Claude 4.7, GPT 5.5, Kimi 2.6, DeepSeek V4, GLM 5 и т.д.

Сегодня покупатели приобретают сырой вывод моделей у провайдеров вывода (inference). Они отправляют свои промпты, получают результат вывода и платят за использование. Это легко проверить, но это все еще лишь сырье. Покупателю нужны не токены, а полезный интеллект по наилучшей цене.

Второй этап: Рынок товаризированных возможностей LLM

Например, text/usd, code/usd, agent/usd и т.д.

Покупатель больше не выбирает конкретную модель, а выбирает нужный ему тип интеллекта. Покупатель по-прежнему контролирует рабочий процесс, промпты, данные и логику приложения. The Grid лишь направляет каждый запрос к подходящей модели, отвечающей спецификациям контракта и имеющей самую низкую цену.

Примечание: это первый настоящий уровень абстракции выше сырых токенов, и на нем сейчас находится TheGrid.ai.

Третий этап: Рынок товаризированной рабочей силы

Например, accounting/usd, support_agent/usd, legal/usd, healthcare/usd, radiology/usd и т.д.

По мере того как модели становятся более специализированными, рынок возможностей может эволюционировать дальше, в отраслевые рынки. Это аналогично специализации людей на разных рынках труда.

На этом уровне мы продаем возможности вывода (inference), адаптированные под рабочие процессы конкретных вертикалей рынка труда. По мере того как специализированные отраслевые модели станут более распространенными, такие рынки будут быстро расширяться. Примеры включают Composer от Cursor, Harvey для юридической работы и EvidenceOpen для здравоохранения.

Четвертый этап: Программируемый RFQ и рынок результатов для агентов

Например, support_ticket_resolved/usd, pr_merged/usd, claim_processed/usd и т.д.

Последний уровень — это место, где The Grid переходит от рынка вывода (inference) к рынку машинизированной рабочей силы.

Этот уровень требует механизмов RFQ (запрос предложений), эскроу-счетов, отсроченных расчетов, подтверждения покупателем, репутации поставщиков, механизмов удержания платежей, разрешения споров и т.д. Скорее всего, он начнется с RFQ, а не с немедленного использования стакана заявок. Покупатель определяет работу, ограничения, критерии приемки и условия расчетов, а агенты участвуют в тендере на выполнение задачи. The Grid помогает направлять, назначать цену, проверять и производить расчеты по этой работе.

Это самый ценный уровень, но и самый сложный с точки зрения верификации, поскольку результаты могут быть отсроченными, субъективными и легко поддаваться манипуляциям. Тикет в поддержку могут переоткрыть; PR может пройти тесты, но все равно создать плохую архитектуру.

Общая стоимость = Стоимость выполнения работы + Стоимость принятия риска

Рабочий процесс не станет рынком автоматически только потому, что появился рынок интеллекта или интеллект подешевел. Некоторые виды работ сильно зависят от приватного контекста, например, истории клиента или внутренних политик. Чем больше работа зависит от контекста, тем менее вероятно, что она будет чисто обработана на открытом рынке. [@hypersoren https://hypersoren.xyz/posts/cybernetic-arbitrage/]

Рынку необходимо показать, какие категории рабочей силы будут расширяться, а какие — сокращаться.

«Машинизированная рабочая сила ПРОТИВ человеческой» или «Машинизированная рабочая сила И человеческая»

Анджали Шрива в своем наброске по механизмам отмечает, что нарратив об ИИ слишком часто описывается как замещение. Но на самом деле это больше похоже на проблему координации: как будут перераспределяться работа, вклад, стимулы и ценность, когда в производстве участвуют и человек, и машина.

Сегодня использование ИИ внутри многих компаний все еще заблокировано, потому что сотрудники используют ИИ в частном порядке, рабочие процессы по-прежнему привязаны к отдельным людям, а компания не может оценить этот прирост производительности или масштабировать эти выгоды.

Большая часть работ, поддающихся автоматизации, вероятно, перейдет к машинам. Часть работы превратится в контроль человека, принятие ответственности, обучение и управление контекстом. В некоторых случаях последние 1% человеческого суждения станут еще ценнее, потому что они могут массово разблокировать оставшиеся 99% автоматизированной работы.

Рашель Су Пак в своей работе «Brave New World of AI Markets» отмечает, что TAM (общий доступный рынок) ИИ не стоит просто моделировать как замещение существующих расходов на человеческий труд, потому что он одновременно меняет и цену, и объем. По мере снижения стоимости работы цена за единицу может упасть, но объем потребления может вырасти, потому что существующая работа будет потребляться чаще, а также станут экономически целесообразными совершенно новые виды работ, которые раньше таковыми не были. Это можно обобщить так:

P × Q: Размер рынка = Цена за единицу работы × Количество потребляемой работы

Если ИИ сделает взаимодействие со службой поддержки дешевле, компания сможет предоставлять услуги круглосуточно. Этот рынок не будет просто дешевой версией старого рынка труда в поддержке, а, возможно, станет значительно более крупным рынком клиентских взаимодействий.

ИИ — это расширяющийся рынок, потому что при снижении стоимости работы спрос не остается прежним.

Слой рабочей силы

Рынок машинизированной рабочей силы должен начинаться с тех видов работ, спецификации которых можно четко определить. GPU-часы содержат слишком много информации о ресурсах, они лишь говорят, что поддерживает работу; а оценивать полный результат слишком сложно, он слишком зависит от контекста. По мере того как проверка, репутация и ценообразование на риск/страхование будут постепенно переходить к машинам, рынок продолжит движение к чистому уровню результатов.

Машинизированная рабочая сила может стать торгуемой, потому что покупателю будет все меньше важно, какая именно модель или какие GPU произвели работу. Ему будет важнее, была ли сама работа выполнена по правильной цене в соответствии с минимальными стандартами и уровнем, указанными в спецификациях контракта. Агенты будут обращать на эти базовые источники еще меньше внимания.

Машины теперь могут напрямую выполнять экономически полезную работу, и эта работа может быть определена, измерена, оценена, закуплена и в конечном итоге обменена. Электроэнергия, вычислительные мощности, модели и токены, конечно, все еще важны, но они находятся на более ранних стадиях.

На более поздних стадиях находится место, где работа реально выполняется, и рынок движется к более простому объекту: машинизированной рабочей силе.