Автор: Matt Brown

Компиляция: Deep Tide TechFlow

Введение от Deep Tide: Партнер Matrix VC Мэтт Браун выдвигает контринтуитивный тезис: ИИ делает код все дешевле, но делает действительно трудновоспроизводимые вещи в Fintech — банковские лицензии, данные андеррайтинга, накопленные через кредитные потери, модели управления рисками, обученные на реальных объемах транзакций — более ценными, чем когда-либо.

"Вы не можете получить банковскую лицензию с помощью атмосферного программирования" — эта фраза раскрывает суть всей статьи.

Это не просто анализ Fintech, а скорее карта того, "какие рвы прочнее" в эпоху ИИ.

Полный текст ниже:

Слово "Fintech" долгое время полагалось на арбитраж неопределенности в своем названии.

"Fin" подразумевает массу писем с домена .gov, многомесячные аудиты, compliance-офицеров, которые знают историю ваших SAR-заявлений лучше вас самих, и командировки в Шарлотт или Вашингтон в рабочие дни. "Tech" — это изящное мобильное приложение, UX в 10 раз лучше, и разговоры об инвестициях за кофе в Blue Bottle.

"Fin" и "tech" всегда были спектром, но рынок обычно вознаграждает те компании Fintech, которые максимально похожи на "tech" и как можно меньше связаны с "fin".

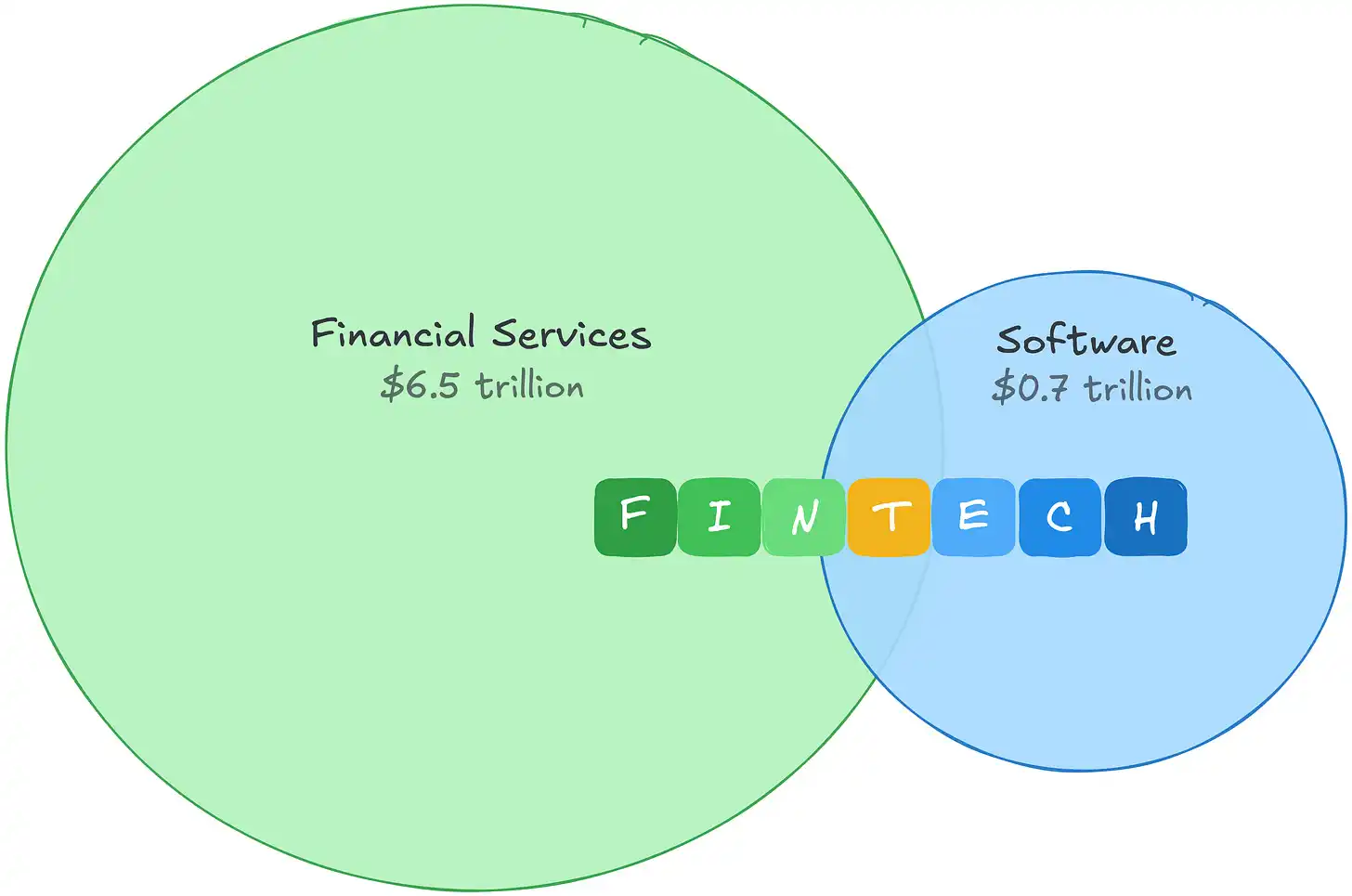

Это понятно. В 2021 году пул валовой прибыли программного обеспечения составлял около $0,7 трлн и пользовался высокими премиями. Пул валовой прибыли финансовых услуг был на порядок больше, но оценки были гораздо консервативнее. Fintech позволял арбитражировать оба конца: экономику финансовых услуг с мультипликаторами оценки software-компаний.

Разрыв в этих пулах прибыли также показывает, где находятся настоящие деньги. Финансовые услуги генерируют наибольшую валовую прибыль среди всех отраслей в мире. Сторона "fin" в Fintech не только более защищена, но и представляет собой гораздо больший рынок.

Затем появился ИИ, и пространство для арбитража исчезло. Поскольку инвесторы переоценивают, "сколько стоит код в мире, где код становится все дешевле", оценки software-компаний сжимаются. Компании Fintech были отнесены рынком к software-компаниям и, следовательно, тоже пострадали.

Но рынок ошибся в классификации. Затраты Fintech, а также его ров, никогда не были в коде, и перед сжатием затрат, движимым ИИ, они выглядят все более антихрупкими.

История двух структур затрат

Программное обеспечение когда-то имело одну из лучших бизнес-моделей в истории: создание кода было дорогим, но一旦 написан, распространение было практически бесплатным. Разрыв между "дорогое создание" и "бесплатное распространение" и был нормой прибыли. Если вы SaaS-компания, тратящая 22-25% выручки на R&D, эти расходы одновременно являются вашим барьером для входа. Конкуренты не могут легко скопировать то, на создание чего ушли годы и десятки миллионов долларов.

ИИ сжимает этот разрыв сверху. Если код дешев в создании и дешев в распространении, норма прибыли сужается. Стена, сдерживающая конкурентов, становится ниже, выходит больше игроков, и ценовая власть размывается.

Если ваш бизнес — это software, это реальная проблема. Но расходы Fintech — не инженерные расходы. Следуйте за деньгами, и разница быстро станет очевидной.

PayPal тратит 9% выручки на R&D, Block — 12%. Это не потому, что инженерия в Fintech не важна — инженерные возможности Stripe мирового уровня и являются реальным конкурентным преимуществом. Просто большая часть денег уходит не на инженерию.

Деньги уходят в "fin". В отличие от расходов на R&D, эти затраты не просто производят продукт, они создают ров:

Кредитные потери покупают данные андеррайтинга

Affirm тратит 35% выручки на кредитные потери и стоимость funds до того, как заплатить инженеру. Каждый убыток по плохому кредиту — это данные о погашении, которые не достаются конкурентам. Новичок, тренирующий модель на синтетических данных, не имеет реальных benchmark-данных. Только синтетическими данными нельзя построить надежную историю потерь.

Расходы на compliance покупают регуляторные разрешения

Wise в рамках более 65 регуляторных лицензий направляет треть сотрудников на compliance и предотвращение финансовых преступлений. Лицензии на денежные переводы в 50 штатах, программы compliance BSA/AML, требования банковского устава. Это не преимущества, которые вы строите, а разрешения, которые вы постоянно зарабатываете. Вы не можете получить банковскую лицензию с помощью атмосферного программирования.

Объем транзакций покупает проприетарные данные

Валовая маржа платежного блока Toast составляет около 22%, что значительно ниже 70% его SaaS-блока, но генерирует почти вдвое большую валовую прибыль. Эти затраты换来 данные о транзакциях на уровне merchants, которые, в свою очередь, питают Toast Capital, выдавший на累计 более $1 млрд кредитов. Модель рисков Adyen обучена на шаблонах транзакций на более чем 30 рынках.

Маржа Fintech никогда не была высокой, и в этом ключ

Валовая маржа платежных компаний составляет 20-50%, а не 80%. Но низкая маржа не равна слабому бизнесу. Маржа Fintech низка, потому что значительные затраты создают преимущества со сложным процентом. И даже те затраты, которые не создают преимуществ, находятся вне досягаемости сжатия затрат, движимого ИИ.

ИИ делает каждый такой ров сильнее. Лучшие модели снижают уровень потерь, лучшее обнаружение мошенничества сокращает chargebacks, лучшие инструменты compliance позволяют меньшим командам удерживать больше лицензий. ИИ не заменяет ров, он вознаграждает компании, которые выбирают строительство в самых сложных местах Fintech: движение денег, принятие рисков, проприетарные данные и регулирование.

Таким образом, реальный тезис не просто "ИИ помогает Fintech", а то, что ИИ смещает ценность от поверхности продукта к проприетарным данным, способности принимать риски, регуляторным разрешениям и каналам дистрибуции, встроенным в реальные денежные потоки. Если вы строите в этих областях, ИИ начисляет сложный процент в вашу сторону. Если ваша дифференциация в коде, ИИ начисляет сложный процент в обратную сторону.

Спрос также продолжает расти. Каждый процесс checkout, созданный атмосферным программированием, — это новый вектор мошенничества, каждый самостоятельно действующий AI Agent — это риск chargeback. Чем больше строится на инфраструктуре Fintech, тем более незаменимой становится сама эта инфраструктура.

"Fin" — это победитель

Это осознание уже заставляет умных основателей Fintech переосмысливать свое место в спектре "fin" и "tech":

Мы сами принимаем и оцениваем риск или передаем его партнерам и позволяем им забирать прибыль?

Мы владеем регуляторными отношениями или арендуем их у тех, кто ими владеет?

Каждая транзакция делает нашу собственную модель рисков точнее или тренирует чужую модель?</p

Наш ledger — это источник真实数据 или неполное отражение чужого ledger?

Это различие делит ландшафт Fintech надвое. Компании, владеющие регуляторными отношениями, самостоятельно несущие кредитные риски, накапливающие данные о транзакциях, строят рвы, которые ИИ углубит. Те, кто арендует "fin" — используют лицензии банков-партнеров, ledger BaaS-провайдеров, чужие модели рисков с лучшим интерфейсом — сталкиваются с exactly такими же проблемами, как и SaaS-компании. Их дифференциация в коде, а код только что подешевел.

Старый арбитраж применения software-мультипликаторов к экономике финансовых услуг мертв. Новый арбитраж проще: владеть "fin".