Вчера Base официально выпустила Base MCP. Подключив Base Account к AI Agent через Base MCP, вы можете, используя разговорную речь, как в чате, давать команды агенту для выполнения таких операций, как свап, перевод средств, отслеживание позиций, запрос истории транзакций и т.д.

Игроки, знакомые с Base, знают, что главной темой в сети Base сейчас является ИИ, поэтому такое обновление не стало для них сюрпризом. Некоторые игроки даже ожидают, что в сети Base появятся новые механики, подобные AI мем-коину $SHIT в Ethereum раньше, когда можно будет через Base MCP в чате давать команды агенту участвовать в листингах новых монет в блокчейне.

Но если отвлечься от точки зрения дегенов блокчейна и посмотреть с точки зрения конкуренции в области платежей между агентами (Agent to Agent), возможно, мы получим новый ответ на вопрос, почему ИИ стал основной темой Base.

Быстро развивающиеся платежи через агентов

Вернемся к сентябрю 2024 года. Тогда у людей по сути был только один выбор, чтобы заставить AI Agent оплатить что-либо: использовать инструменты автоматизации браузера (такие как безголовые браузеры Playwright, Selenium и др.), чтобы AI Agent имитировал действия человека и завершал процесс оплаты на веб-странице.

Поскольку для этого требовалось предоставить агенту платежные реквизиты (полный номер карты, CVV, срок действия и т.д.), этот единственный выбор был небезопасным.

К маю 2025 года Coinbase выпустила x402, предоставив AI Agent криптокошелек и криптонативный способ решения этой проблемы. Но Coinbase была не единственной, кто осознал потенциал этого рынка, и способы решения не ограничивались только криптонативными. В 2025 году Google выпустила AP2, разрешив пользователям делегировать агентам права на совершение платежей. Visa расширила свои существующие каналы оплаты картами, выпустив Visa Intelligent Commerce, которая вместо предоставления агенту чувствительных данных (номер карты, CVV) дает агенту специальные ограниченные токены для завершения платежа.

На сегодняшний день через x402 было обработано 176 миллионов транзакций от AI Agent на общую сумму более 70 миллионов долларов. Эта сумма может показаться небольшой, но ни Coinbase, ни традиционные гиганты не недооценивают конкуренцию в этой новой форме платежей:

- 22 января 2026 года Capital One (шестой по величине банк США, активы — 470 миллиардов долларов, депозиты — 330 миллиардов долларов, третий по объему выпуска кредитных карт в США) объявил о приобретении Brex за 5.15 миллиардов долларов для улучшения возможностей AI-платежей.

- В марте 2026 года Mastercard приобрела инфраструктурную компанию для стейблкоинов BVNK за 1.8 миллиарда долларов.

- В феврале 2025 года Stripe приобрела платформу для платежей стейблкоинами Bridge за 1.1 миллиарда долларов.

Хотя они прямо об этом не заявляли, приобретение компаний, связанных со стейблкоинами, было ответом на грядущую эпоху платежей через агентов. И стейблкоины действительно имеют решающее значение для таких платежей.

Почему стейблкоины важны для платежей через агентов?

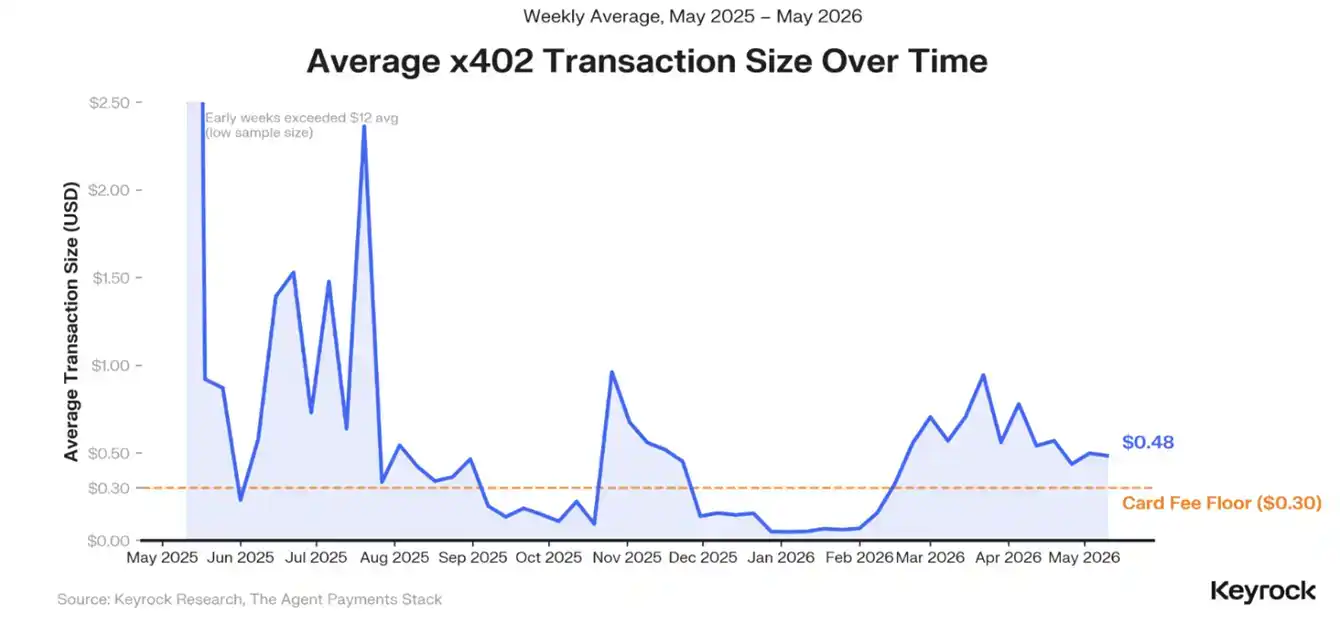

Согласно статистике Keyrock, медианная сумма транзакций агентов, обработанных через x402 на сегодняшний день, составляет от 0.01 до 0.10 доллара, причем 76% транзакций имеют сумму менее 0.30 доллара.

0.30 доллара — это самая распространенная фиксированная комиссия за операцию в США и на большинстве основных рынков. Эта комиссия подобна стене, делающей микроплатежи на сумму менее 1 доллара крайне невыгодными. Например, вызов API стоимостью 3 цента с комиссией 0.3 доллара увеличивает стоимость вызова в 10 раз. Если агент будет платить кредитной картой, накопленные затраты станут запредельно высокими.

Блокчейн отлично решает эту проблему. В сети Base стоимость расчета транзакции составляет 0.0001 доллара. Благодаря такому огромному преимуществу, стейблкоины практически гарантированно выигрывают конкуренцию у традиционных платежных гигантов в сфере платежей через агентов.

Из 176 миллионов транзакций агентов, обработанных через x402, 98.6% были рассчитаны в USDC. Учитывая тесные отношения Coinbase и Circle, можно сказать, что Coinbase также является крупным победителем на уровне расчетов.

Но уровень расчетов — это лишь один из уровней в системе платежей через агентов. В гонке за решение этой проблемы криптонативным способом у Coinbase есть соперник — Stripe.

Вызов от Stripe

В марте этого года Stripe выпустила протокол платежей для агентов MPP, что сделало архитектурную картину Stripe в этой сфере почти неотличимой от Coinbase.

- На уровне расчетов: у Coinbase есть Base, у Stripe — Tempo

- На уровне кошельков: у Coinbase есть Agent Wallet, у Stripe — Privy

- На уровне маршрутизации: у Coinbase есть встроенная соответствующая инфраструктура, у Stripe — приобретенная за 1.1 миллиард долларов Bridge

- На уровне платежных протоколов: у Coinbase есть x402, у Stripe — MPP

Теперь вернемся к упомянутому в начале статьи Base MCP. Поскольку у обоих соперников есть все четыре уровня инфраструктуры, следующим полем битвы, естественно, становится уровень приложений.

Вот главная причина, почему ИИ стал основной темой Base — Base стремится обеспечить, чтобы ИИ (по крайней мере, в сфере криптовалют) работал на базе Base. Это делается не столько для предоставления удобств дегенам в сети Base, сколько для расширения сценариев использования платежей через агентов, чтобы больше агентов совершало больше транзакций для большего числа приложений, тем самым обеспечивая лидирующие позиции в этой гонке.

Когда будет сформировано доминирующее преимущество масштаба, Coinbase сможет выиграть еще больше, когда платежи через агентов перейдут в коммерческую сферу.

С этой точки зрения запуск Base MCP позволяет почувствовать, что это всего лишь маленький шаг в грандиозных амбициях Coinbase.