Автор: Dave

Почему после покупки альткойнов в краткосрочной перспективе всегда не везет? Почему маркет-мейкеры, кажущиеся гигантами, не могут выдержать продажи 10/11?

Почему после 10/11 каждый маркет-мейкер, с которым говорят, спокойно утверждает, что в тот день почти не потерял или даже заработал? Эта статья познакомит вас с книгой заявок и потоком ордеров маркет-мейкера.

1. Книга лимитных заявок (Limit Order Book, LOB)

Поле битвы маркет-мейкера — не график свечей, а LOB.

Ключевые концепции:

-

Глубина (Depth): Объем ордеров на каждом ценовом уровне.

-

Шаг цены (Tick Size): Минимальная единица изменения цены. В высокочастотной среде шаг цены крайне важен для стратегии очереди.

-

Улучшение цены (Price Improvement): Когда вы предлагаете цену лучше текущей лучшей цены покупки/продажи (NBBO), вы создаете ценность для рынка.

Например, если текущая цена bid на BTC составляет 100 000, а ask — 110 000, и вы предлагаете цену 101 000, вы сужаете спред (spread), создавая ценность для рынка.

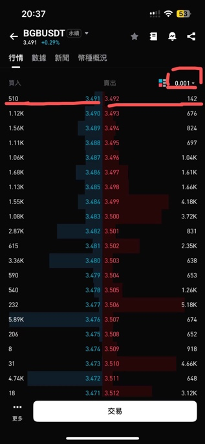

Пока я писал статью, я думал, как лучше объяснить этот раздел, и понял, что нет ничего лучше, чем показать реальный стакан заявок. Сделаю дружескую рекламу для bg, приведу пример с bgb.

Выше представлен стакан заявок для bgb с минимальным шагом. Мы видим, что минимум составляет 0.001, сейчас глубина стакана всего чуть более 1000 долларов, спред контролируется очень маленьким, достигнув минимального tick size. При этом глубина распределена в форме «рождественской елки»: чем дальше от текущей цены, тем больше объем. Однако, если мы увеличим tick size, то обнаружим, что глубина должна распределяться в форме рупора: чем ближе к текущей цене, тем больше объем, ликвидность выше, а чем дальше, тем меньше выставляется ордеров (одна из причин вакуума ликвидности 10/11).

Говоря о рождественской елке, планируемое время публикации этой статьи — 24.12, канун Рождества. Желаю всем счастливого Рождества!

2. Источник прибыли маркет-мейкера: Спред (spread)

Спред — это не только прибыль, он в основном состоит из трех видов затрат:

-

Затраты на обработку ордеров (Order Processing): Комиссии биржи, аппаратные задержки,人力 (трудозатраты).

-

Риск инвентаря (Inventory Risk): Риск неблагоприятного изменения цены во время удержания позиции, о чем мы говорили в предыдущей части.

-

Затраты на неблагоприятный отбор (Adverse Selection): Это ядро — при совершении сделки другая сторона может обладать информацией, которой нет у вас. То есть вас могут «подставить» инсайдеры.

-

Также существуют три типа спреда: Quoted Spread (котируемый спред), Effective Spread (эффективный спред), Realized Spread (реализованный спред). Котируемый спред — это просто разница ask-bid. Реализованный спред измеряет фактическую прибыль маркет-мейкера после корректировки цены: 2 x (P_trade – P_futuremid), где учитывается будущая средняя цена, что-то вроде учета альтернативных издержек.

3. Поток ордеров (Order Flow)

Поток ордеров — это поступающие к маркет-мейкеру заявки. Это очень глубокая тема. Маркет-мейкеры выполняют различные операции с потоком ордеров, такие как хеджирование, matching (совпадение), изменение выставляемых ордеров и т.д., чтобы управлять своей книгой (book). Здесь много профессиональных концепций и операционных приемов,甚至 могут涉及法律问题, например, agency trade (агентские сделки) не могут быть контрагентами для principle trade (принципальные сделки) из-за конфликта интересов. В этой статье мы рассмотрим только токсичность потока ордеров (Order Flow Toxicity) и VPIN. Если какой-нибудь босс-mm возьмет меня на работу, я обновлю для друзей-подписчиков профессиональное управление order flow.

Токсичный поток (Toxic Flow) — это ордера от информированных трейдеров, которые знают о предстоящем изменении цены, поэтому они вызывают потери realized spread, поскольку благодаря инсайду они знают P_futuremid. Поэтому, как «собаки-киты» (крупные игроки), мы также должны быть осторожны, чтобы не быть «подставленными» токсичными инсайдерами.

Нетоксичный поток (Noise/Retail Flow) исходит от розничных инвесторов или фондов, пассивно корректирующих веса. Это любимая «еда» маркет-мейкеров.

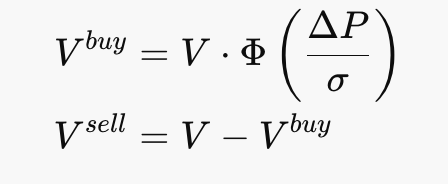

Чтобы защитить себя, защитные механизмы маркет-мейкеровadjust quotes (корректируют котировки). Простой метод защиты от «токсичности» — предположить, что все агрессивные ордера токсичны. Предположим, покупка, тогда mm немедленно понижает reservation price (резервную цену), и котировки в целом смещаются вниз. Это также отвечает на вопрос, оставшийся с предыдущей главы: почему мы всегда покупаем на пиках? Потому что маркет-мейкеры корректируют котировки для риск-менеджмента. Но聪明的 вы обязательно снова зададитесь вопросом: а если инсайдер будет massively покупать?仗着有信息优势直觉头铁冲击盘口怎么办? (Полагаясь на информационное преимущество, упрямо атаковать стакан?) Да, возможно, это то, что произошло 10/11, и причина, по которой крупный mm с активами в миллиарды не выдержал напора.

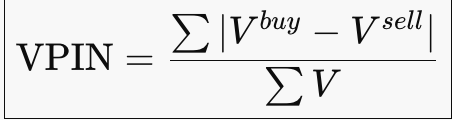

Ключевой показатель: VPIN (Volume-weighted Probability of Informed Trading — Взвешенная по объему вероятность информированной торговли).

VPIN ≈ Вероятность того, что маркет-мейкер в текущем рынке подвергается «постоянным one-sided атакам». При появлении значительного one-sided давления инвентарь mm накакой-то одной стороне накапливается, гипотеза Mean reversion (возврата к среднему) перестает работать. В этот момент mm отзывает ордера (Pull quotes), временно переставая предоставлять ликвидность, чтобы дождаться восстановления симметрии потока ордеров. Но что, если симметрия потока ордеров не восстановится? Или смещение потока ордеров будет слишком экстремальным и приведет к margin call? Это и есть трагедия 10/11. Есть мысли выпустить серию о том, как биржи заработали на 10/11, посмотрим позже.

Возвращаясь к теме, при аномалиях VPIN, MM отзывает ордера (Pull quotes) или расширяет спред (Widen spread), что эквивалентно получению дополнительной комиссии для компенсации убытков от движения цены, а также уменьшает size для контроля скорости накопления инвентаря.

Эта часть завершает первую историю о маркет-мейкерах с точки зрения розничного инвестора. Истина о легендарных манипуляциях «собак-китов» раскрыта. Далее я с точки зрения mm представлю более «институциональные» темы, держитесь крепче.

В конце каждой серии аниме показывают预告 (трейлер следующей серии), сделаем это и в статье: Если мы попадем в мир Jujutsu Kaisen, где поток ордеров — это «проклятая энергия» (Cursed Energy), а операции с котировками — «техники» (Cursed Techniques), то в следующей части мы посмотрим на «развертывание территории» (Domain Expansion) в маркет-мейкинге.

Что будет дальше, узнаете в следующей серии.