Автор: DCo (@Decentralisedco)

Компиляция: Deep Wave TechFlow

Введение от Deep Wave: Выручка Hyperliquid в 2025 году составляет 15% от выручки CME, но рыночная капитализация — лишь 10% от CME. За этим дисконтом к оценке скрывается то, что рынок совершенно не оценил потенциал HIP-3 по освоению TAM объемом в триллионы долларов. Выходные с войной в Иране стали стресс-тестом для этого тезиса: пока CME был закрыт, фьючерсы на нефть на блокчейне в одиночку обеспечивали глобальное ценообразование в реальном времени. Эта статья с помощью четырехсценарной DCF-модели показывает, что текущая цена HYPE в $37 уже упала ниже целевой цены медвежьего рынка в $60, что означает, что даже если HIP-3 практически не продвинется, сама эта оценка уже занижена для базового биржевого бизнеса.

Фреймворк оценки HYPE

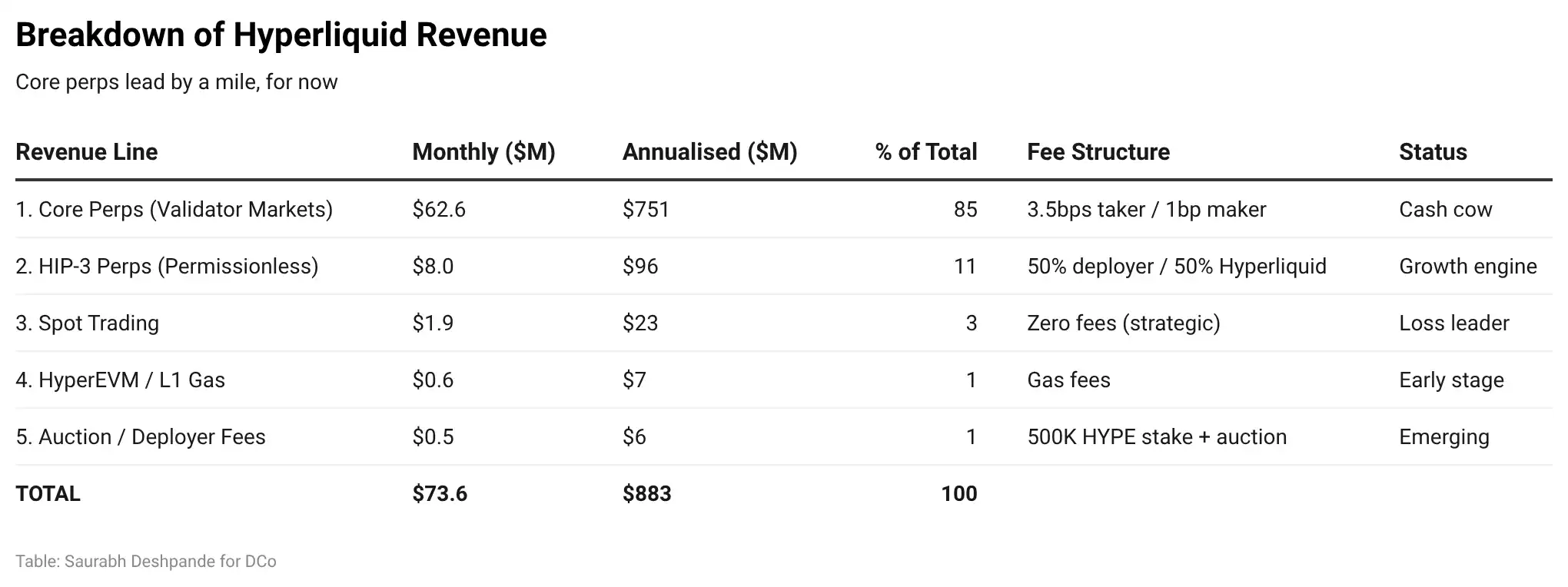

Выручка CME в 2025 году составила $65 млрд при среднем дневном объеме контрактов в 28.1 млн. Рыночная капитализация — $1140 млрд. Выручка Hyperliquid в 2025 году при объеме торгов около $3 трлн составила $960 млн. Рыночная капитализация — $125 млрд. Текущая выручка Hyperliquid составляет около 15% от выручки CME, но рыночная капитализация — лишь 10% от CME. Ключевая возможность заключается в том, насколько объемы торгов из традиционных финансов могут мигрировать на такие децентрализованные платформы, как Hyperliquid.

От криптовалютного DEX к глобальной бирже деривативов

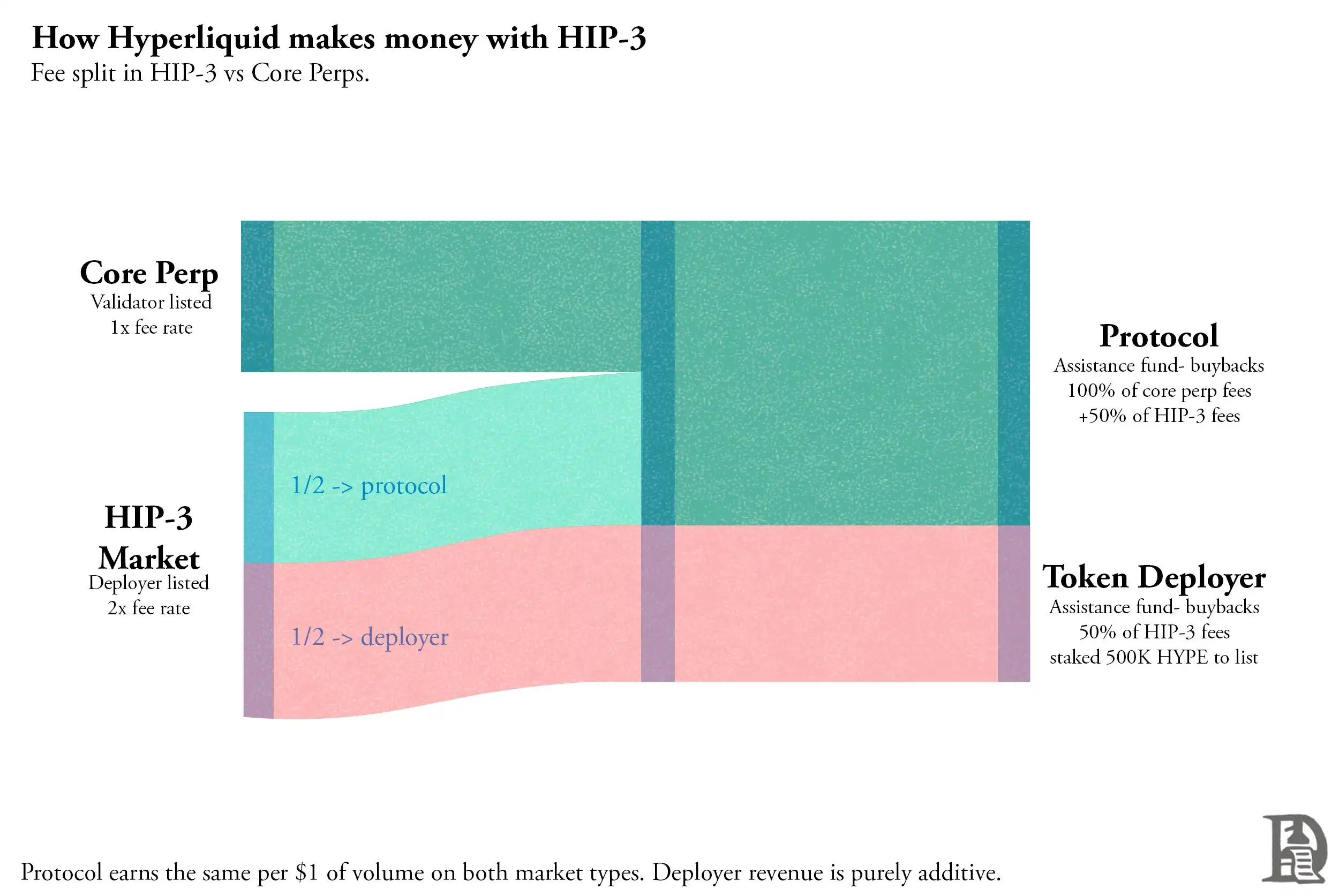

HIP-3 был запущен в октябре 2025 года и позволяет размещать бессрочные контракты без разрешения. Разработчики, застейкавшие 500 тыс. HYPE (около $18.5 млн по цене $37 за штуку), могут запускать собственные рынки на HyperCore. Комиссии на этих рынках в два раза выше, чем на основных листированных бессрочных контрактах Hyperliquid, половина идет разработчику, другая половина — протоколу Hyperliquid для выкупа. Таким образом, доход протокола на каждый доллар объема торгов такой же, как на основных рынках, а разработчик дополнительно получает эквивалентный доход в качестве стимула за размещение и поддержку рынков.

За пять месяцев объем торгов HIP-3 достиг $100 млрд, а открытый интерес 10 марта достиг рекордных $1.2 млрд, значительно выросши с $260 млн месяцем ранее.

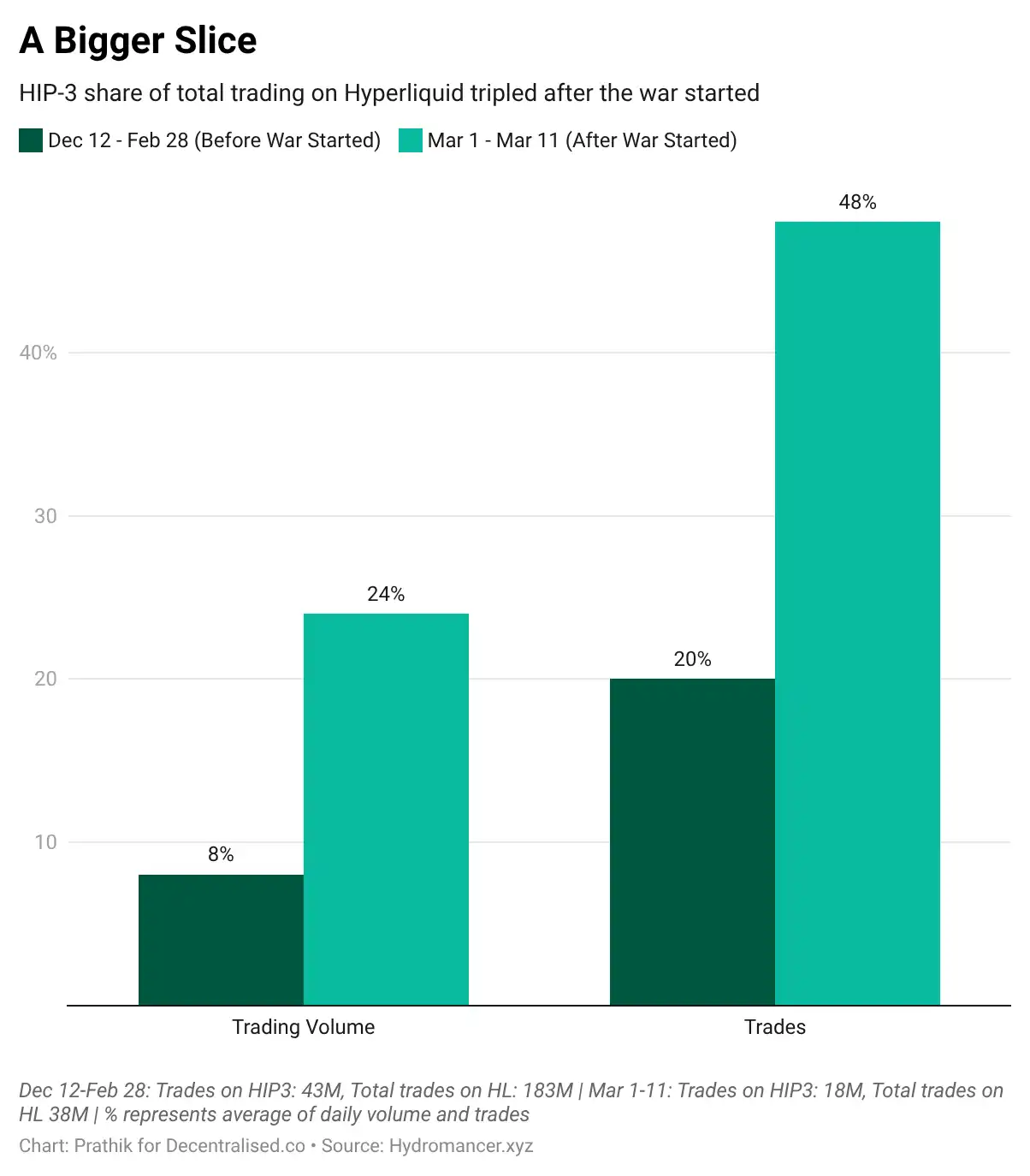

HIP-3 позволяет размещать любые активы: товары, фондовые индексы, валютные пары, Pre-IPO токены и т.д. За последние две недели доля HIP-3 в общем объеме торгов Hyperliquid выросла с 8% до 23%, и сейчас почти половина торгов происходит на рынках HIP-3.

Война в Иране как проверка концепции

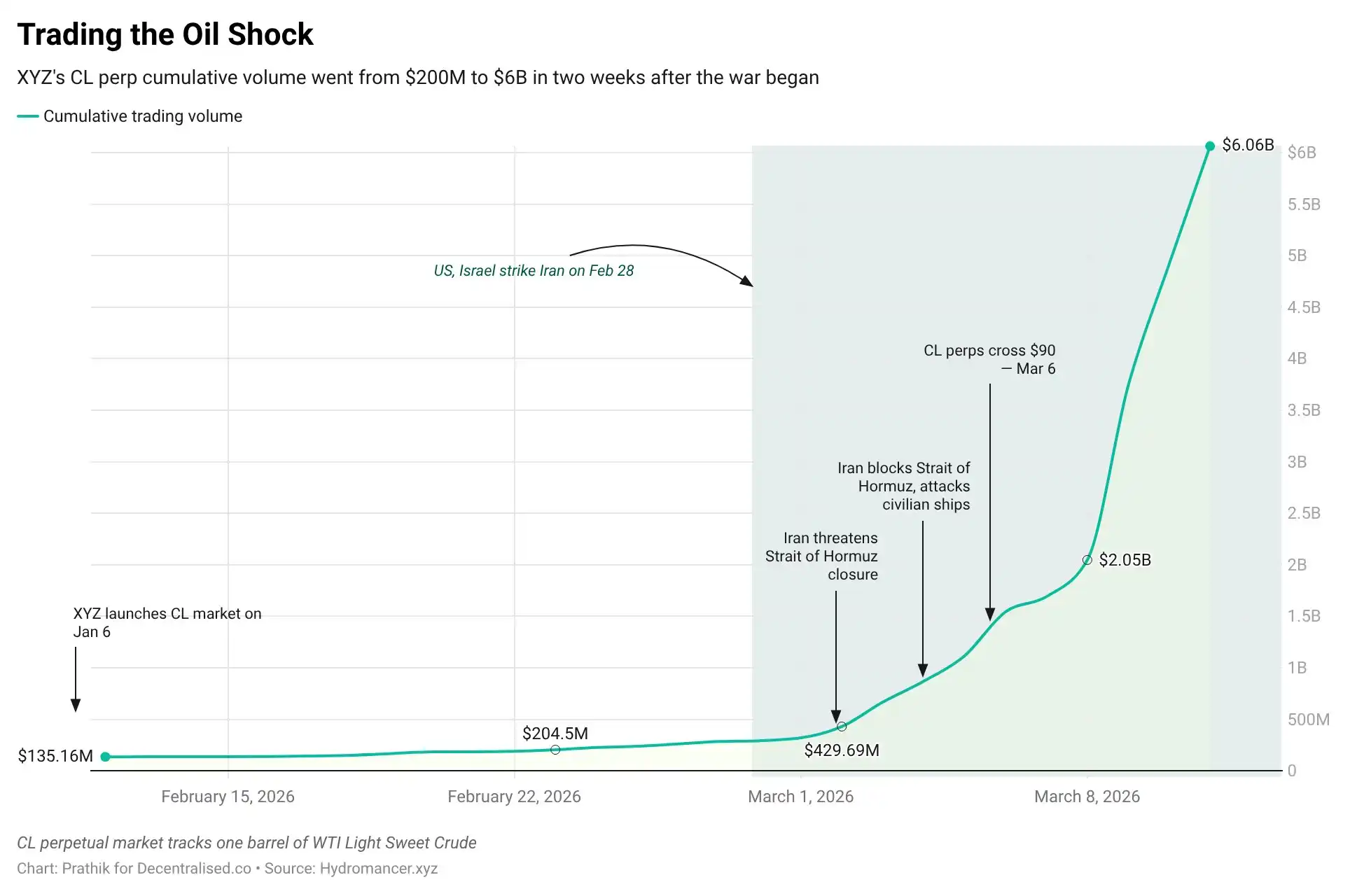

28 февраля США и Израиль нанесли удар по Ирану во время закрытия традиционных рынков. В течение нескольких часов нефтяные бессрочные контракты на Hyperliquid выросли на 5%, поскольку трейдеры в реальном времени закладывали удар в цену. На следующей неделе, после того как WTI показал крупнейшее недельное ралли с 1983 года, 24-часовой объем торгов нефтяными бессрочными контрактами на Hyperliquid превысил $1.2 млрд, а объем ликвидаций достиг $40 млн. Совокупный объем торгов бессрочными контрактами CL за две недели вырос с $200 млн до $6 млрд. Биткоин торговался в бок около $68 000. Основное поле битвы для макросделок было на Hyperliquid, а не на спотовом крипторынке.

Когда CME вновь открылся в понедельник, он подтвердил направление движения, заданное Hyperliquid на выходных. Если токенизированные бессрочные контракты на нефть могут обрабатывать такой объем с эффективным механизмом price discovery, то бессрочные контракты на золото, SPX и валюты тоже смогут.

CME + 0DTE опционы как TAM для HIP-3

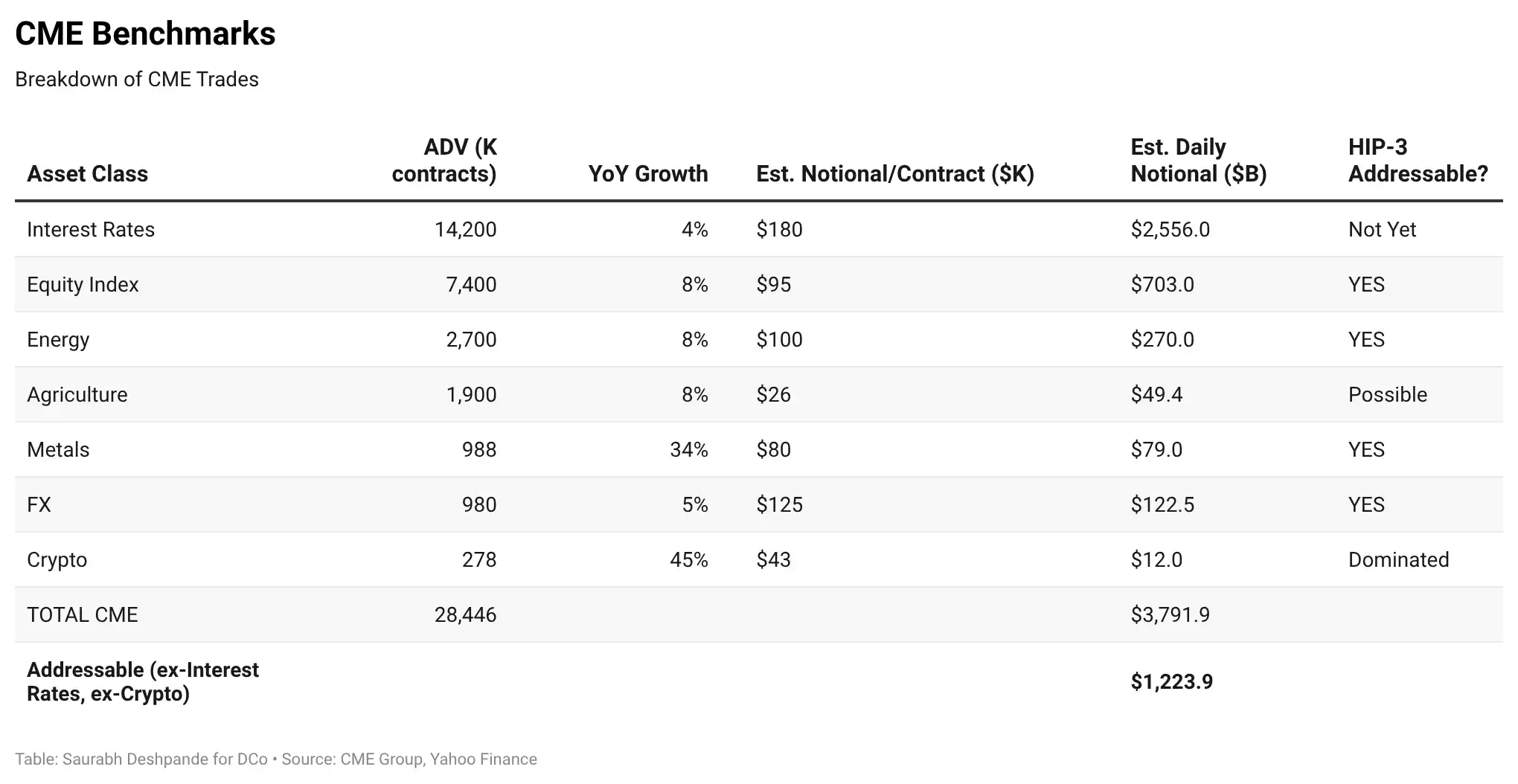

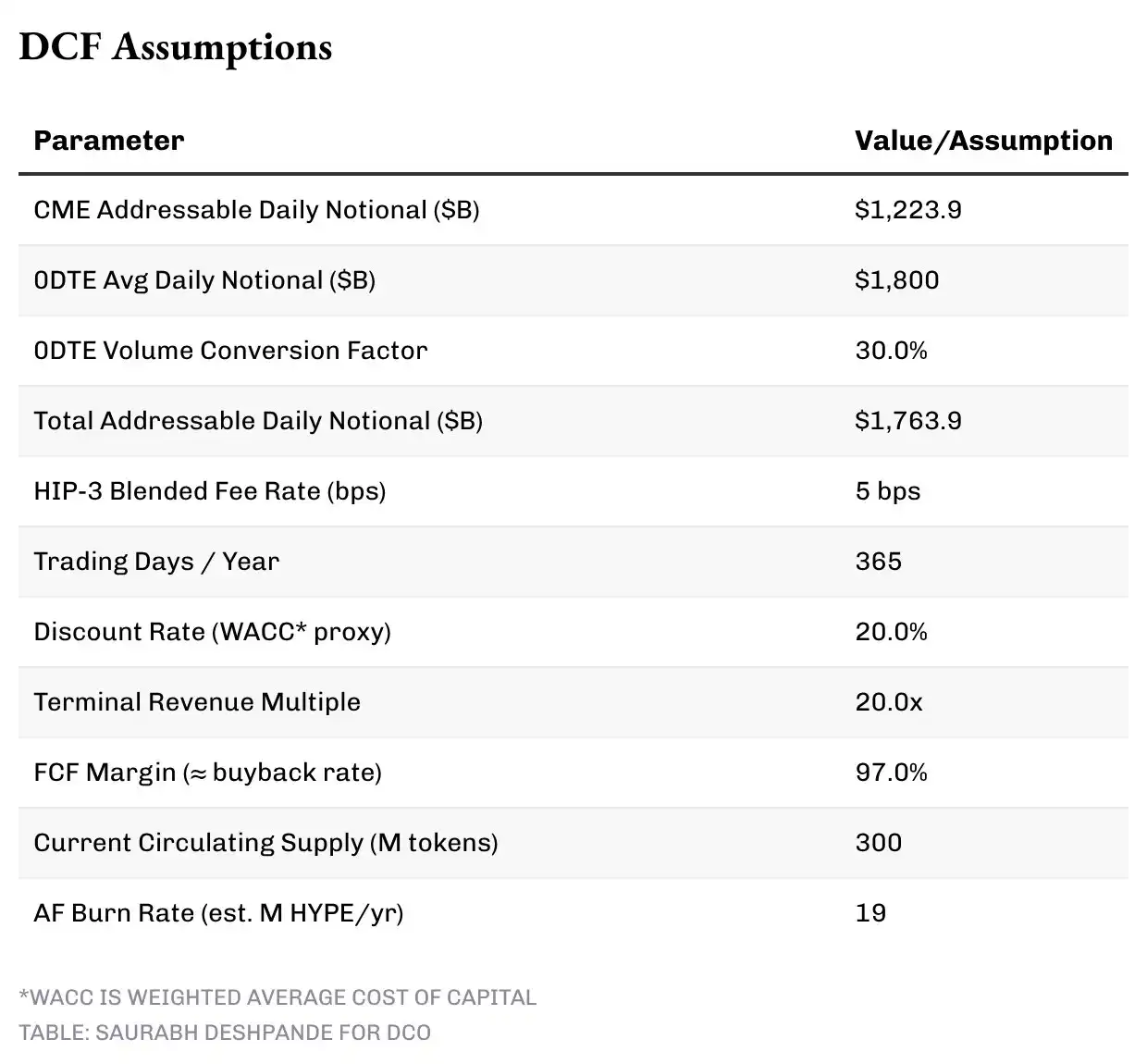

Средний дневной объем торгов CME по всем классам активов составляет $3.8 трлн. Исключая сложные структурные продукты, такие как процентные ставки, которые трудно мигрировать в краткосрочной перспективе, а также криптопродукты, где Hyperliquid уже доминирует, в области фондовых индексов, энергоресурсов, металлов, сельского хозяйства и Forex адресуемый дневной объем CME составляет около $1.2 трлн.

Кроме того, мы учитываем рынок 0DTE (опционов с истечением в день покупки) опционы. Только номинальный объем 0DTE опционов на SPX в мае 2025 года превышал $1.2 трлн в день. Учитывая, что 0DTE на SPY составляют 45% от всего объема опционов на SPY, FalconX оценивает общий номинальный объем 0DTE в $1.5–2 трлн в день. С поведенческой точки зрения, это трейдеры бессрочных контрактов, использующие инфраструктуру опционов — потому что в регулируемых рынках бессрочных контрактов на акции пока не существует. Бессрочные контракты устраняют сложность и стоимость 0DTE опционов.

Ключевая корректировка: номинальная стоимость 0DTE опционов завышает эквивалентный объем бессрочных контрактов. Мы применяем коэффициент конверсии 30% к номинальной стоимости 0DTE, чтобы оценить реальный эквивалентный объем бессрочных контрактов, который может мигрировать. Таким образом, общий адресуемый рынок (TAM) для HIP-3 составляет около $1.74 трлн в день: $1.2 трлн адресуемого объема CME плюс около $540 млрд конвертированного объема 0DTE.

Сценарный анализ

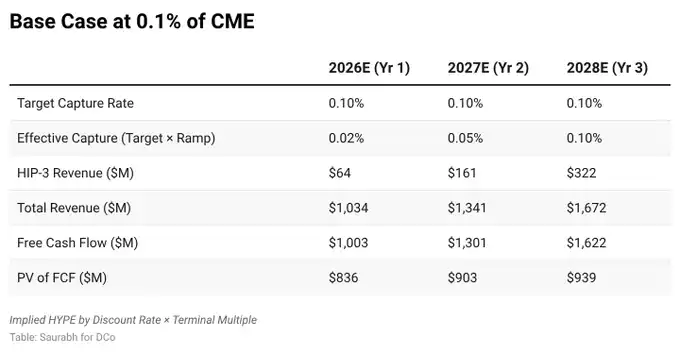

Мы построили четыре сценария на основе процента от дневного TAM в $1.74 трлн, который Hyperliquid сможет захватить через HIP-3, используя трехлетнюю модель дисконтированных денежных потоков (DCF).

Каждый сценарий предполагает постепенный рост проникновения: 1-й (2026) — достижение 20% от цели, 2-й (2027) — 50%, 3-й (2028) — 100%, чтобы отразить реалистичное накопление рыночной доли. Базовый доход от основных крипто-бессрочных контрактов, спота, газа EVM и сборов с аукционов прогнозируется отдельно от модели водопада доходов, увеличиваясь с $970 млн в 2026 году до $1.35 млрд в 2028 году.

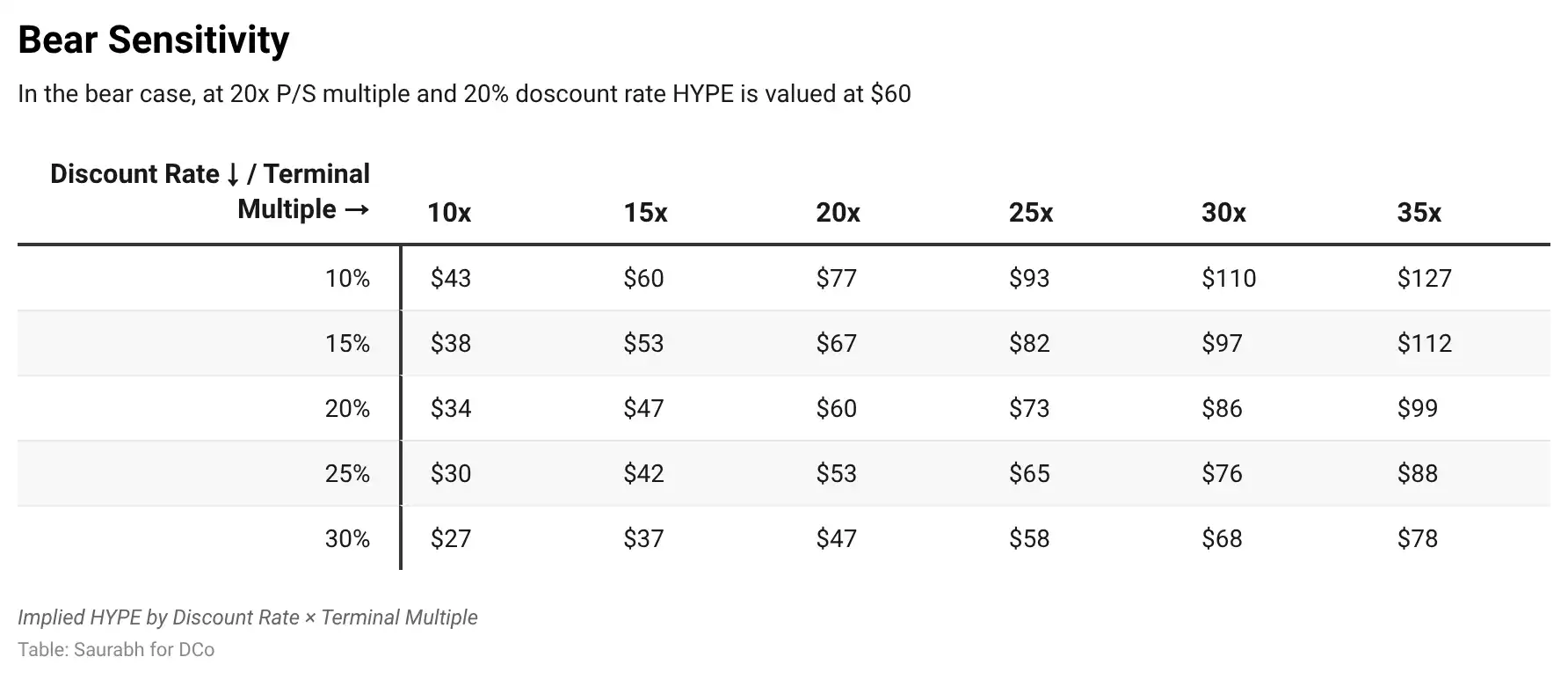

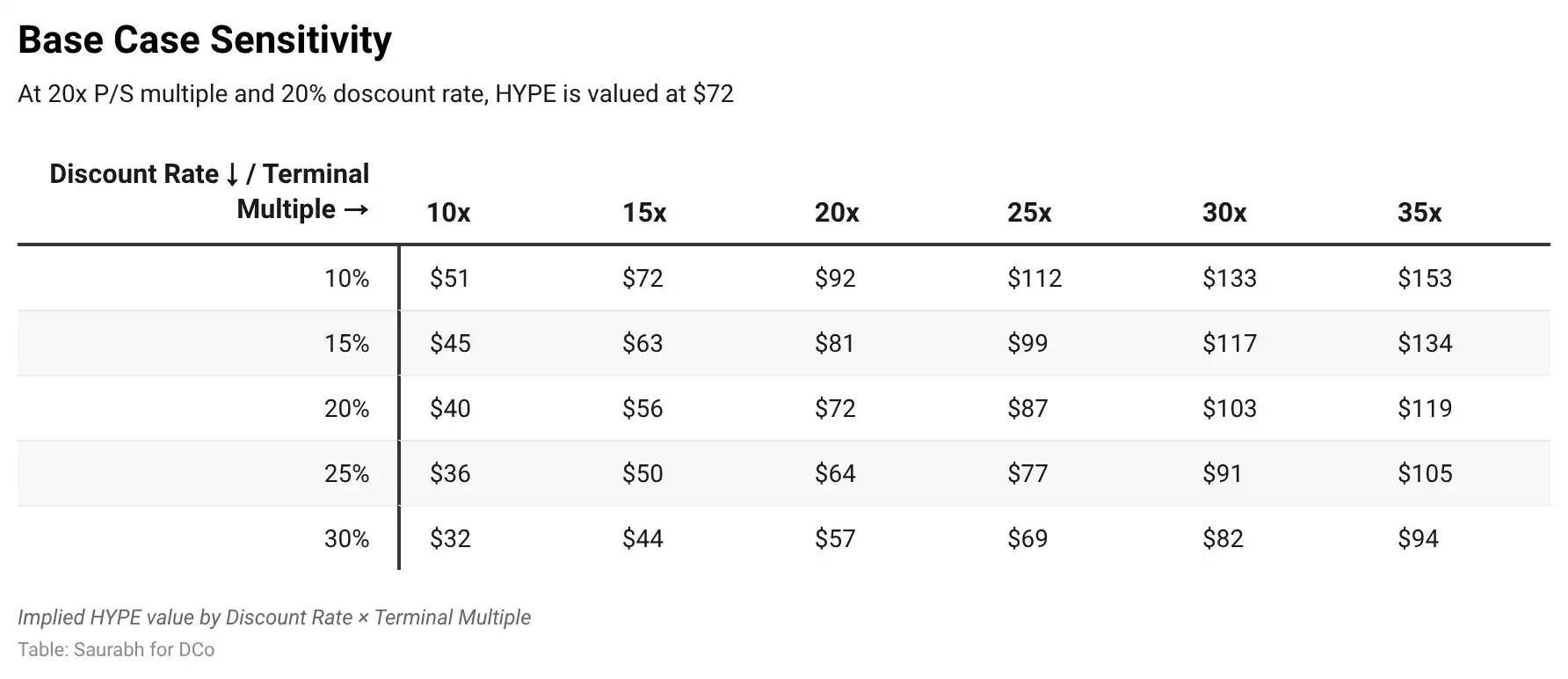

Мы используем ставку дисконтирования 20% и терминальную мультипликацию в 20x от дохода 3-го года — умеренную премию к текущим 17.5x EV/Revenue CME, чтобы отразить более высокую траекторию роста Hyperliquid. Ставка дисконтирования 20% отражает риски криптопротокола, но также признает, что Hyperliquid — это прибыльное предприятие с проверяемыми ончейн-потоками, а не токен на стадии до продукта. Таблица чувствительности позволяет проводить стресс-тесты при ставке дисконтирования до 30%.

Модель также учитывает ожидаемые изменения в обращении. Со стороны предложения, около 23.8% от общего предложения HYPE выделено основным контрибьюторам, с блокировкой на год и последующим линейным вестингом в течение 24 месяцев. Соучредитель Iliensinc подтвердил, что распределение (если есть) происходит 6 числа каждого месяца, добавив, что "разблокировка не является линейной". Фактический график сильно варьируется: в декабре около 2.6 млн (из которых 850 тыс. были релоцированы), в январе 1.2 млн, в феврале команда сократила месячный объем разблокировки на 90%, до всего 1.4 тыс. Как отметил Arthur Hayes, 66.6% токенов контрибьюторов все еще заблокированы до 2027-2028 годов, и разблокировки инвесторов вообще нет.

Мы не ориентируемся на пики или минимумы, а берем среднемесячное значение с начала распределения — около 1 млн HYPE, или 12 млн в год — в качестве базового предположения. Эмиссия за стейкинг валидаторов при текущих около 400 млн застейканных токенов и ставке вознаграждения 2.37% ежегодно добавляет еще около 10 млн.

С другой стороны, Фонд помощи (AF) с момента создания (ноябрь 2024) за примерно 16 месяцев накопил и сжег 42.8 млн HYPE, наблюдаемая годовая ставка сжигания составляет около 32 млн. AF получает около 97% торговых комиссий через автоматический механизм выкупа, и в его кошельке дополнительно хранится 42.1 млн HYPE, ожидающих сжигания. Историческая скорость сжигания включает периоды, когда HYPE находился в нижнем ценовом диапазоне (большую часть 2025 года в пределах $10-25), что означает, что на каждый доллар комиссий можно было вывести больше токенов.

При текущей цене $37 и ежедневных торговых комиссиях около $2 млн перспективная годовая ставка сжигания ближе к 19 млн HYPE. В модели мы используем эту перспективную оценку в 19 млн в качестве базового прогноза, хотя исторические данные в 32 млн показывают, насколько активно AF работал в условиях низких цен. Важно, что сжигание AF эндогенно связано с доходом: в хорошие времена более высокий доход от комиссий означает значительно большее количество токенов, выкупленных и сожженных. Это создает рефлексивную динамику, которую статический прогноз предложения не может полностью уловить.

Чистый эффект — лишь незначительный рост обращения. От текущих около 300 млн, ежемесячная разблокировка командой около 1 млн плюс годовая эмиссия валидаторов в 10 млн дает в сумме около 22 млн новых токенов в год; при этом около 19 млн ежегодно выводятся через сжигание AF. Мы прогнозируем около 302 млн на конец 2026 года, 305 млн на конец 2027 года и 308 млн на конец 2028 года — чистое увеличение примерно на 3 млн в год. Двигатель выкупа почти полностью хеджирует новую эмиссию, годовой уровень разводнения составляет около 1%. Подразумеваемая цена HYPE рассчитывается на основе прогнозируемого предложения на 3-й год.

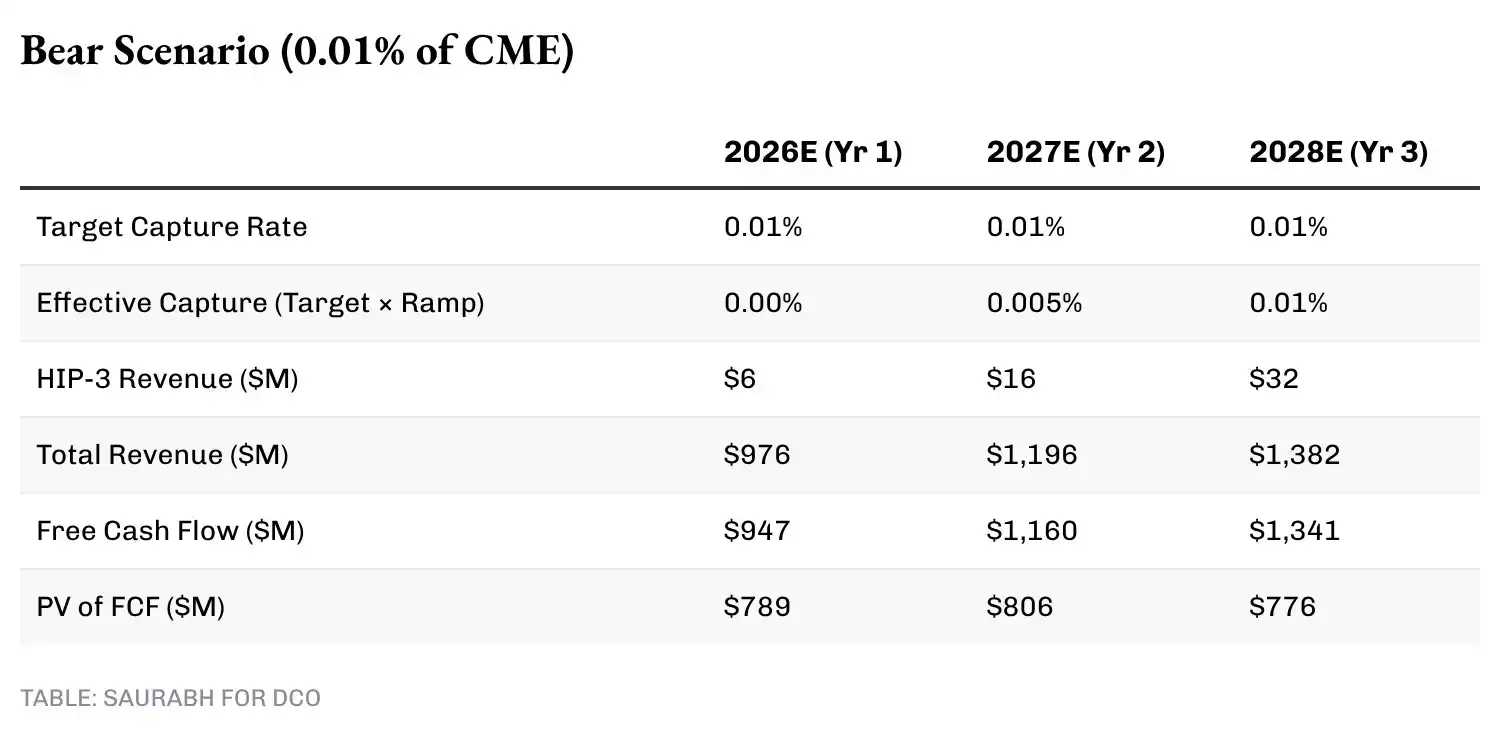

В медвежьем сценарии (коэффициент захвата 0.01%) HIP-3 при полной работе скорректированного TAM генерирует $32 млн комиссий в год. В сочетании с базовым доходом в $1.35 млрд, на основе терминальной стоимости от общего дохода 3-го года, DCF дает стоимость предприятия около $18 млрд.

Соответствуя прогнозируемому предложению на 3-й год в 308 млн (незначительно увеличившись с текущих 300 млн), подразумеваемая цена HYPE составляет около $60 — что все еще представляет собой значительную премию к текущим $37, означая, что даже при крайне ограниченном прогрессе HIP-3, одной базовой биржевой экономической логики достаточно для поддержания более высокой цены.

В базовом сценарии (коэффициент захвата 0.10%) доход HIP-3 на 3-й год достигает $322 млн, общий доход — около $1.7 млрд, что соответствует стоимости предприятия около $22 млрд и подразумеваемой цене HYPE около $72.

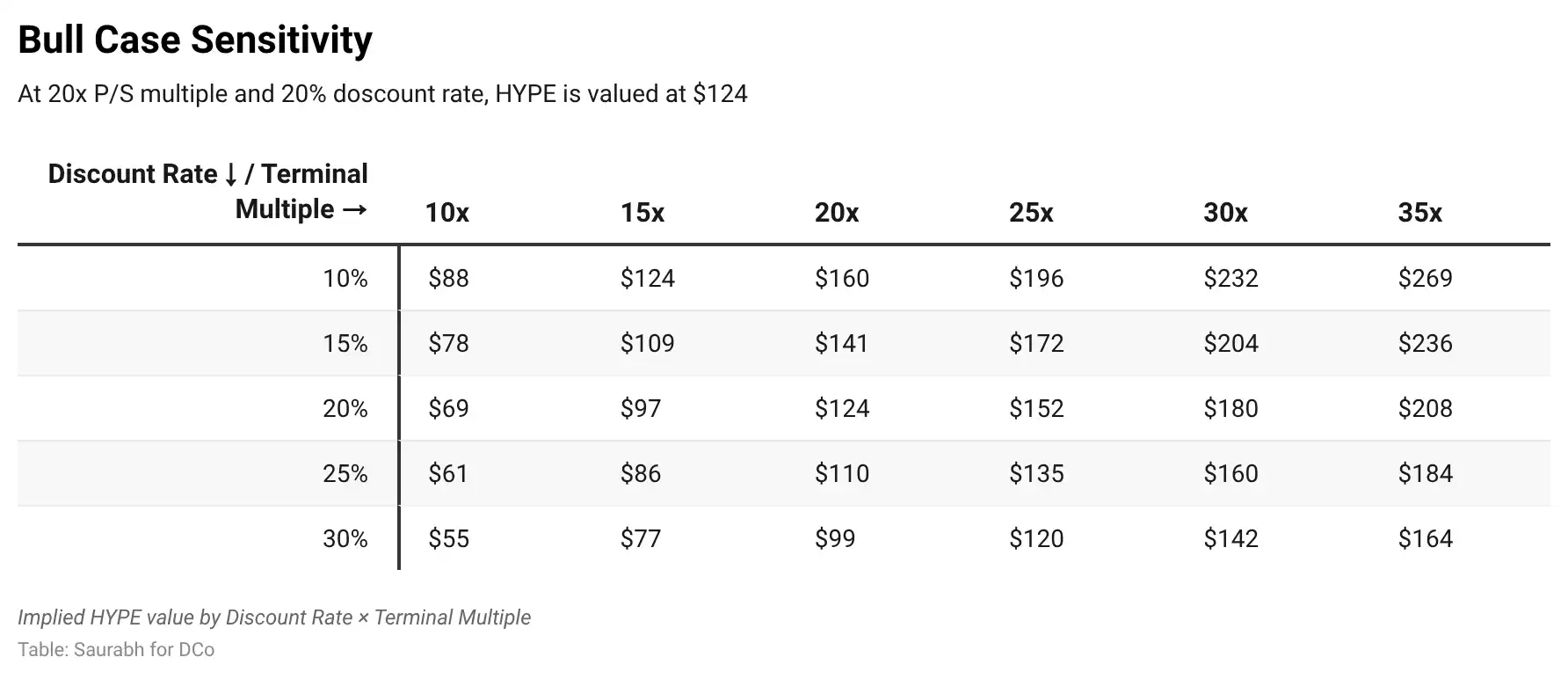

В бычьем сценарии (коэффициент захвата 0.50%) комиссии HIP-3 на 3-й год составляют $1.6 млрд, общий доход — $3 млрд, стоимость предприятия — $38 млрд, подразумеваемая цена — около $124, а полностью разводненная оценка — около $124 млрд.

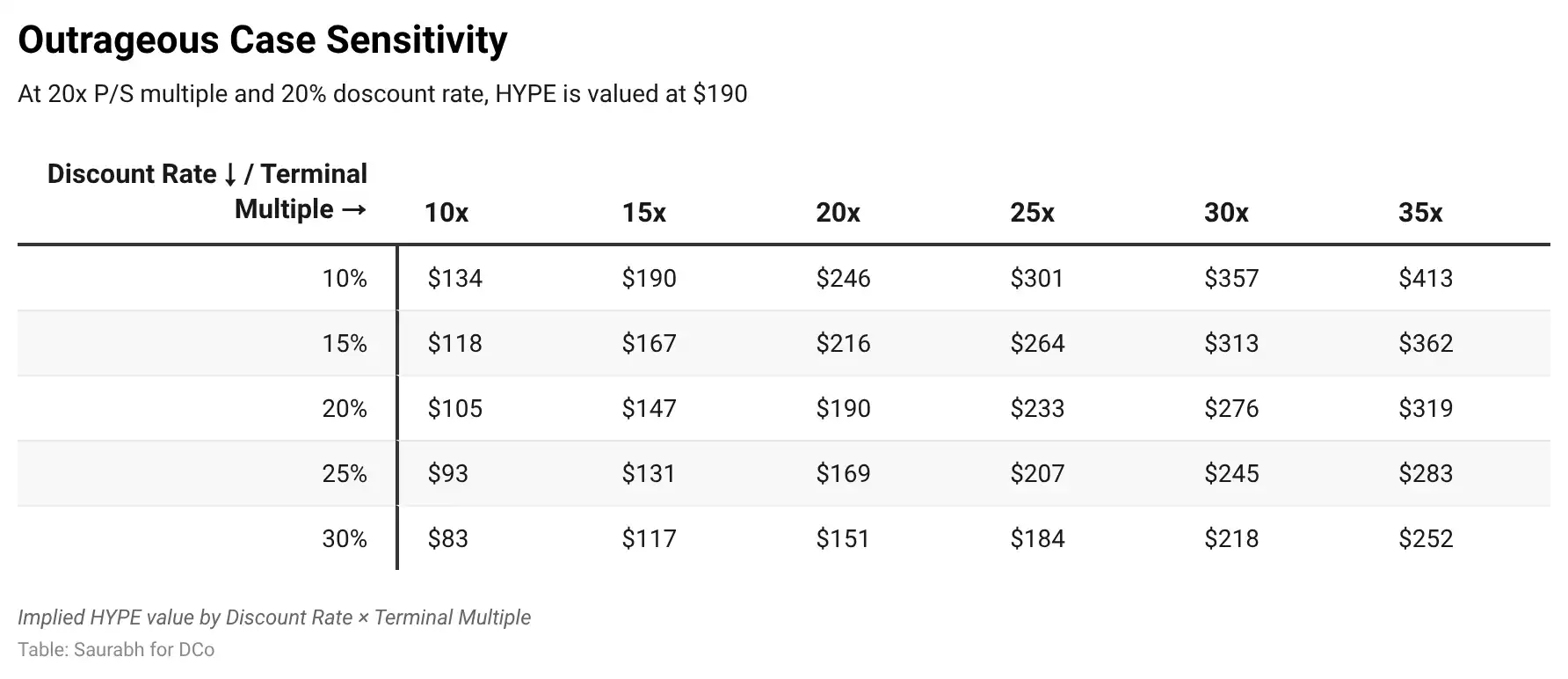

В экстремальном сценарии (коэффициент захвата 1.00%) общий доход на 3-й год достигает $4.6 млрд, стоимость предприятия — $59 млрд, HYPE приближается к $190, а FDV находится в диапазоне $190 млрд.

На этом уровне коэффициент P/S Hyperliquid составляет около 13x, что все еще ниже текущих 17.5x CME — что указывает на консервативность предположений о терминальной мультипликации для бизнеса, растущего так быстро.

При стандартных 20% дисконте и мультипликаторе 20x текущая цена в $37 значительно ниже целевой цены медвежьего рынка в $60, что означает, что рынок еще не оценил какой-либо значительный вклад HIP-3 и можно утверждать, что даже базовый криптобиржевой бизнес недооценен. Целевая цена в $72 в базовом сценарии предполагает потенциал роста около 93% от текущего уровня, требующего захвата всего 0.10% адресуемого объема торгов. Целевая цена Hayes в $150 попадает между нашим бычьим ($124) и экстремальным ($190) сценариями, требуя коэффициента захвата от 0.50% до 1.00%. Учитывая, что HIP-3 работает всего пять месяцев и уже составляет около 10% дохода от комиссий, эти трехлетние цели по коэффициенту захвата амбициозны, но не беспочвенны.

Почему Hyperliquid, а не другие платформы

Естественное сомнение в тезисе HIP-3: если объемы торгов традиционными деривативами мигрируют в ончейн, они могут пойти куда угодно. Мы считаем, что это недооценивает инерцию концентрации ликвидности.

Посмотрим на конкурентный ландшафт. В конце 2025 года Lighter ненадолго обошел Hyperliquid по 30-дневному объему бессрочных контрактов, работая с нулевыми комиссиями и проводя одну из самых агрессивных программ поощрений на рынке. Затем 30 декабря состоялся дроптокенов $LIT, $250 млн было выведено за 24 часа, и в течение трех недель объем торгов Lighter рухнул, а доля рынка сжалась до 8.1%. Несмотря на то, что Lighter по-прежнему не берет комиссий, объемы вернулись к Hyperliquid. Ров заключается в глубине ликвидности и качестве исполнения, а не в цене. Коэффициент отношения открытого интереса к объему торгов подтверждает это: Hyperliquid — 0.64 (удержание капитала), Aster — 0.18, Lighter — 0.12.

Теперь о централизованных альтернативах. Coinbase готовится запустить регулируемые бессрочные контракты, но подумайте о пользователях: если вы хотите получить экспозицию на фондовые индексы или товары, у вас уже есть Robinhood, Schwab и Interactive Brokers. Запуск SPX-бессрочников на Coinbase не решает боли их пользователей. Hyperliquid решает другую проблему: расчеты 24/7, отсутствие ограничений по рыночным сессиям, кросс-маржинализация с криптоактивами, безразрешительный листинг. Это дополнение к существующей системе, а не ухудшенная версия продуктов, которые традиционные институты уже имеют.

HYPE недооценен

Hyperliquid сталкивается с рисками. HIP-3 требует, чтобы бессрочные контракты на индексы и товары поддерживали объемы после того, как пройдет novelty-эффект. Сообществу 0DTE нужна веская причина перейти с опционов на бессрочные контракты, а не просто более низкие комиссии. Движок должен выдерживать объемы в $50 млрд в день с той же производительностью, что и при $8 млрд. Это не экзистенциальные риски. Основной продукт работает. Выходные с войной в Иране доказали, что спрос на 24/7 price discovery на товары реален.

Регуляторная ясность в США в отношении токенизированных бессрочных контрактов не является обязательным условием для этого тезиса. Скорее всего, большая часть объема Hyperliquid приходится на не-США. Но признание или одобрение со стороны США только ускорит рост этой категории. Каждый доллар, мигрирующий с традиционных деривативов на инфраструктуру без разрешений, расширяет общий адресуемый рынок, а Hyperliquid с его глубиной ликвидности, качеством исполнения и инфраструктурой маркет-мейкеров обладает способностью захватывать непропорционально большую долю. HIP-4, представляющий прогнозные рынки и опционоподобные контракты, открывает совершенно новое измерение объемов.

Текущий коэффициент P/S HYPE составляет 10-13x, в то время как у CME — 25x, у ICE — 23x, у CBOE — 22x. Это зрелые бизнесы с ростом в единицы процентов. Hyperliquid в первый полный год получила выручку в $960 млн, не имеет долга, обременения персоналом и имеет механизм выкупа, возвращающий почти все комиссии держателям токенов. Ни одна традиционная биржа не может этого сделать. Мы ожидаем, что HYPE будет переоценен как биржевая акция с гибридным мультипликатором, отражающим двойной доход от крипто и традиционных деривативов. Это означает, что текущие $37 за HYPE ниже его потенциальной справедливой стоимости.

Данная статья вдохновлена опубликованным анализом от @FalconXGlobal.

Отказ от ответственности: DCo имеет позицию в HYPE. Эта статья не является инвестиционной рекомендацией.