Author: @BirchHill_io

Compiled by: AididiaoJP, Foresight News

"Asset-backed credit is the only category of on-chain credit that can solve the adverse selection problem. Tokenized fund wrappers cannot do this. Birch Hill's theory for solving this at the vault level."

Three Markets, Not One

When discussing on-chain credit, it's essential to separate the three things people often refer to by the same name.

The first is overcollateralized crypto lending. Aave, Morpho, Compound, Spark. Borrowers post $1.50 of ETH as collateral to borrow $1 of stablecoin. The liquidation mechanism is automated. The collateral is highly liquid 24/7. This category has matured into one of the most reliable yield primitives in DeFi, with current stablecoin supply rates ranging from 3.5% to 7%. It works, but it also cannot scale beyond crypto-native collateral risk.

The second is unsecured lending. This has been the holy grail of DeFi since 2017 but has consistently failed in its permissive form because the protocol layer cannot answer the three questions any credit business must answer: who is the borrower, how to price their default, and what happens when they don't repay. The history of this category so far is a graveyard.

The third is asset-backed credit. Loans secured by real, identifiable collateral, with off-chain legal claims, third-party appraisals, and recovery rights. This is currently the fastest-growing category and the only one with a credible answer to the adverse selection problem that has plagued on-chain credit.

The label "asset-backed credit" has been growing on-chain, primarily in wrapped forms. Most of the current on-chain presence is tokenized fund shares: a fund holds the loans, and tokens represent shares of the fund. The fund's structure determines whether the adverse selection problem is truly solved. In most cases, the protocol layer merely passes through the risks built into the fund sponsor.

Asset-backed credit is the fastest-growing category of on-chain credit, but its current mode of growth—via tokenized fund wrappers—does not actually solve the problem. Fund wrappers inherit the sponsor's structure. What we are implementing is solving the problem at the smart contract layer: appraisal, structuring, and recovery are coded into the vault itself, not inherited from an off-chain fund manager.

Where Growth Actually Is

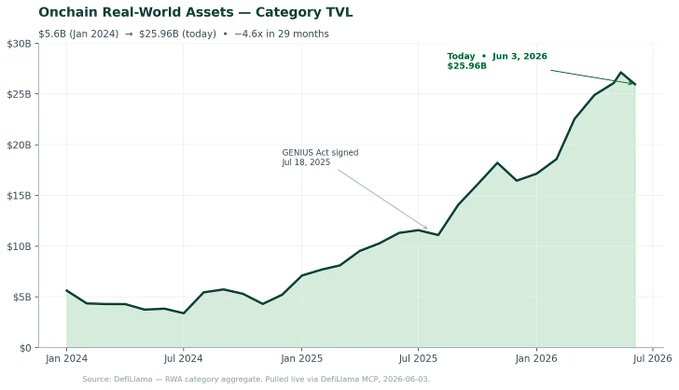

The on-chain real-world asset (RWA) category has grown from $5.6 billion at the start of 2024 to $259.6 billion as of June 3, 2026. This represents approximately a 4.6x expansion in 29 months, concentrated almost entirely in the last 12 months. The pullback after the May peak is minor relative to the overall trajectory and consistent with normal category volatility.

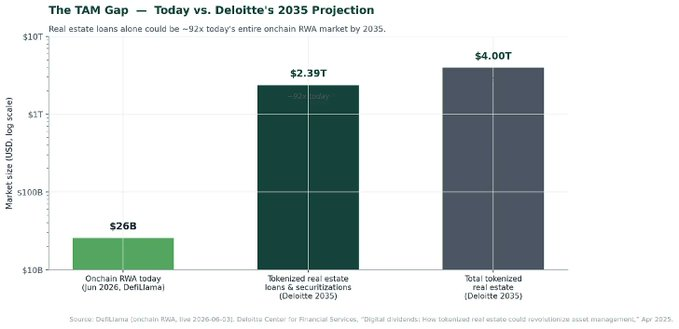

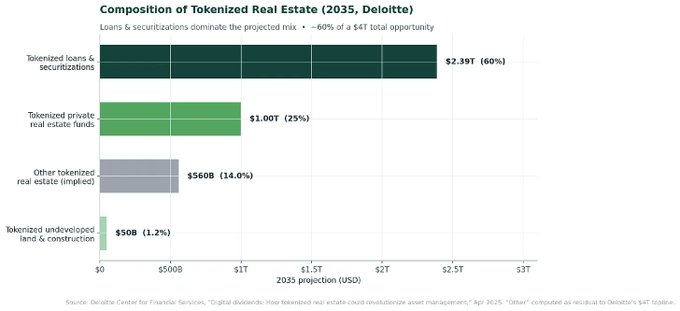

It's worth contextualizing this growth. Even with a 4.6x expansion in 29 months, the entire on-chain RWA market today remains negligible compared to the size the market believes the category can reach. Deloitte's April 2025 forecast shows tokenized real estate alone reaching $4 trillion by 2035, with tokenized loans and securitization being the largest subsegment at $2.39 trillion.

The composition is more important than the headline. The first wave was tokenized US Treasuries: BlackRock's BUIDL, Franklin Templeton's BENJI, Ondo, Superstate, and now JPMorgan's MONY and BNY Mellon's competing products. These are essentially money market funds with a blockchain wrapper. They proved institutions can and will custody on-chain, but they didn't solve credit; they just ported existing products.

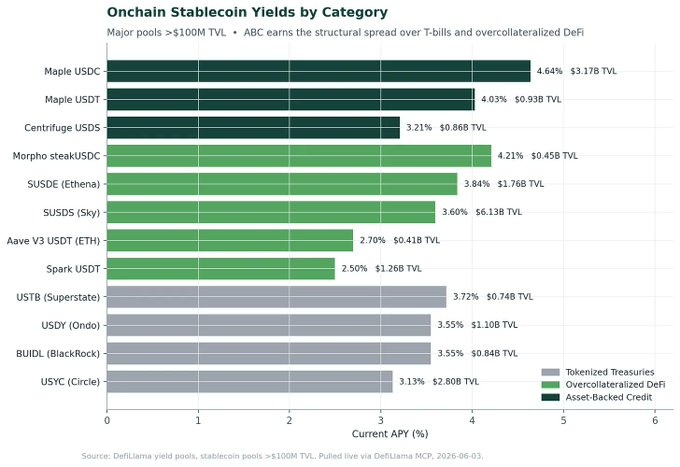

The second wave we're currently in is tokenized private credit. On-chain private credit is up about 180% year-over-year and is now the largest non-stablecoin RWA segment. Maple Finance has $3.17 billion in its USDC lending vault and approximately $926 million in its USDT vault, totaling about $4.1 billion in stablecoin deposits. Centrifuge has surpassed $1.38 billion in TVL. New entrants keep emerging, including Centrifuge's USDS vault with approximately $865 million.

These are credit funds with an on-chain conduit. Borrowers are KYC'd, loans have off-chain legal documents, third-party appraisal is done by humans with credit committees, and recovery proceeds in court like any other private credit fund. Blockchain contributes distribution, transparency of the wrapper, and increasingly, a regulatory containment layer.

Stablecoins are the demand side, and they're growing even faster.

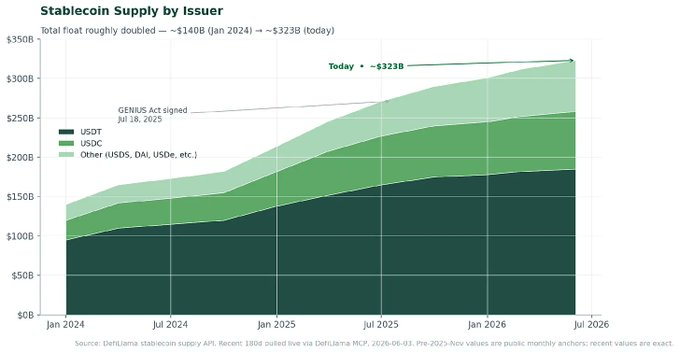

Total stablecoin supply has reached approximately $323 billion today. USDT is about $190 billion. USDC is about $73 billion. Other yield-bearing and crypto-backed stablecoins (USDS, DAI, USDe, etc.) add another roughly $65 billion. The overall pool of on-chain dollars seeking compliant yield, by our estimation, far exceeds $250 billion and is growing at a high single-digit percentage monthly. The question is no longer whether there's on-chain capital that wants yield, but what that capital is permitted to do.

What Asset-Backed Credit Actually Is, and Why It Works

When we say asset-backed credit, we mean something specific. A loan is asset-backed when (a) the borrower pledges identifiable real-world collateral, (b) the lender has a perfected security interest in that collateral, (c) recovery does not require the borrower's cooperation, and (d) loan-to-value ratios, tenor structure, and recovery waterfalls are documented in legal papers and remain valid upon default. This is ordinary in traditional private credit. In on-chain credit, it's the single feature that separates a working structure from a failed one.

The types of collateral that work in asset-backed credit have three properties: they are identifiable (not commingled), have an active secondary market for liquidation, and the lien process is well-understood in the borrower's jurisdiction. Examples include: trade receivables, equipment financing, real estate-backed bridge loans, invoice factoring, structured consumer finance. Things that don't work (or only work at much wider spreads) include: future cash flows from an operating business without a specific asset pledge, intangible intellectual property, illiquid private equity stakes. The discipline is collateral first, borrower second.

Real estate-backed lending deserves specific focus as it's projected to be the largest segment of the entire tokenization opportunity. Deloitte's breakdown is unequivocal on this point: by 2035, tokenized loans and securitization are expected to dominate the tokenized real estate portfolio, roughly three times the size of tokenized private real estate funds and far exceeding the tokenized equity of undeveloped or under-construction projects.

The spread is earned by the work done before deployment. Every loan goes through credit appraisal, pricing default probability, loss given default, and the recovery process. Every loan has covenants, reporting obligations, and documentation of trigger events. Every pool has a curator or appraisal partner with skin in the game, both reputationally and financially. Every vault has a clear waterfall: who gets paid first upon asset liquidation, what triggers a pool freeze, how losses are allocated. The mechanism does the work; marketing does none of it.

This is also why the spread persists. While tokenized T-bills cluster around ~3.5% and overcollateralized DeFi clusters between 2.5% and 4.2%, well-structured ABC pools consistently sit in the 4-5% range with multi-billion-dollar capacity. This premium is compensation for the credit work experts must perform. The protocol layer doesn't do this work; it's built to enable external experts to curate it.

The Adverse Selection Problem, and Why Most On-Chain Credit Hasn't Solved It

Anyone who has worked in private credit knows that who self-selects into your offering tells you almost everything. The cheapest capital flows to the strongest borrowers. The credit you end up with is the credit rejected by everyone earlier in the stack. This is the adverse selection problem, and it's the only one that truly matters in private credit.

On-chain credit, in its permissive form, historically inverted the solution to this problem. Early protocols offered capital to anonymous wallets willing to pay the highest rates. No identity. No recourse. No appraisal layer beyond pool statistics. The stress period of 2022 made the consequences clear: pools marketing themselves as "institutional-grade" found their borrowers were correlated, undisclosed, and in some cases, insolvent. Recovery on defaulted loans was effectively zero because loans were unsecured and jurisdictions unclear.

The working version—permissioned pools with KYC, off-chain documentation, dedicated curators, and a real appraisal layer—is now the dominant structure of the on-chain credit market that survived. Market leaders on-chain have converged on essentially the same answer: credit work happens off-chain, the pool encodes the outcome. This is a marked improvement over permissive unsecured lending. But it's not the end of the design space.

Here is a key point the market hasn't internalized yet: when asset-backed credit sits inside a fund wrapper, and the fund decides underwriting, recovery, and waterfalls, the adverse selection problem moves one level up. If the fund manager has misaligned incentives, levered exposure, or insufficient appraisal, then the on-chain vault is just a more transparent way to deliver bad risk.

The Regulatory Inflection: GENIUS, CLARITY, and the Yield Question

If market structure is reason one for what we're building now, US regulation is reason two, and over the last twelve months, it has shifted in ways most operators are still catching up to.

The GENIUS Act, the first federal stablecoin framework, was signed into law on July 18, 2025. It establishes a federal regime for payment stablecoin issuers, requires 1:1 reserves, and most importantly for our thesis, it prohibits stablecoin issuers from paying interest or yield to holders in any form. The OCC published proposed implementing rulemaking on February 25, 2026. The statutory deadline for final rules is July 18, 2026. The full operational regime is expected to be in place no later than January 2027.

The GENIUS Act left a loophole: it prohibited issuers from paying yield but didn't fully address yield paid on stablecoin balances by exchanges or affiliated platforms. The Digital Asset Market CLARITY Act, advancing in the Senate and passed in the House, closes that gap. The latest draft prohibits offering yield on stablecoin balances, directly or indirectly. The White House's April 2026 paper, "The Impact of a Stablecoin Yield Ban on Bank Lending," makes the policy logic clear: Washington wants stablecoins to be payment rails, not deposit replacements, and wants yield to flow through clearly defined investment products, not through the stablecoin itself.

This is the regulatory window most of the market is mispricing. The set of products that can legally offer yield on on-chain dollars is being explicitly narrowed. The set of structures that will survive (registered funds, properly disclosed lending vaults, tokenized credit products) is being implicitly elevated. The next twelve months will be a sorting event.

The Vault Is the Architecture That Matters

If stablecoin issuers can't pay yield, and exchanges can't pay yield on stablecoin balances, then the only legal way to convert on-chain dollars into income is through a discrete, identifiable investment product. On-chain, that product is the vault. ERC-4626 and its successors have become the de facto standard for tokenized yield-bearing positions, and the vault is now the chassis for almost all compliant on-chain credit products in the US market.

In traditional asset-backed lending, the wrapper is incidental. You raise LP commitments, draw into a fund, deploy into loans, distribute.

On-chain, the vault does far more work than its TradFi counterpart. The vault is simultaneously an issuance mechanism (it mints shares representing claims on underlying loans), a disclosure mechanism (its accounting is publicly verifiable), a distribution mechanism (anyone with a wallet can interact with permission), a recovery mechanism (waterfalls and trigger events are coded), and increasingly, a regulatory containment vessel (permissions can enforce KYC, accredited investor thresholds, and jurisdiction restrictions in ways a stablecoin cannot). When yield is banned at the stablecoin layer, the vault layer becomes where compliant, regulated, transparent yield is delivered.

This is why we believe the design of an on-chain vault—its permissions, its accounting, its disclosure standards, its compliance posture, and most importantly, how it encodes credit work—will become the most important architectural choice in this market over the next eighteen months. In traditional ABC, you can have a mediocre fund wrapper and excellent credit work and still produce a great product. On-chain, in a post-GENIUS/CLARITY world, a poorly designed vault becomes a regulatory liability. A vault that's just tokenized fund equity merely relocates the adverse selection problem rather than solving it.

Where We Stand

We are focused on asset-backed credit because it's the only category of on-chain credit with a structurally defensible answer to adverse selection, and the data is unequivocal about demand.

We are US-facing with a compliance-first posture because we believe the post-GENIUS, post-CLARITY US regulatory framework will set the standard for how on-chain yield is delivered globally. The cost of retrofitting compliance onto non-compliant structures far exceeds the cost of designing it in from day one.

We treat the vault layer as a first-order design problem, not a packaging exercise, because we believe the architecture is where regulatory, technical, and operational complexity will compound over the next eighteen months. We are not interested in being another tokenized fund equity. We are interested in encoding appraisal, structuring, and recovery into the vault itself at the protocol layer in ways the current generation of products does not.

The Next Twelve Months

By July 2026, the OCC's final GENIUS Act rules will be in place. By the end of 2026, the CLARITY Act framework will likely be enacted or close to enactment. By January 2027, the full payment stablecoin regime will be operational. Sometime in that window, a generation of yield products designed for the pre-2025 regulatory environment will need to be sunset, and a generation designed for the post-CLARITY environment will need to be ready.

The on-chain capital base already exists. The stablecoin float has reached ~$323 billion. On-chain credit demand is growing at triple-digit rates. The regulatory framework is being finalized and, with appropriate caveats, is moving in a direction favorable to well-structured, compliant, US-based, vault-based asset-backed credit.