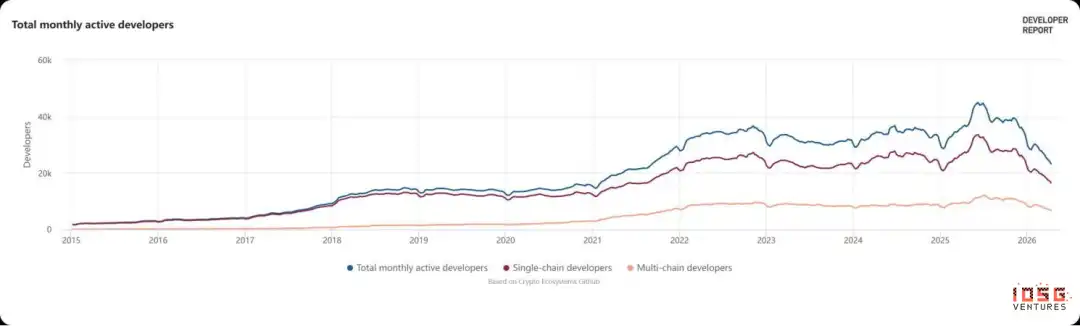

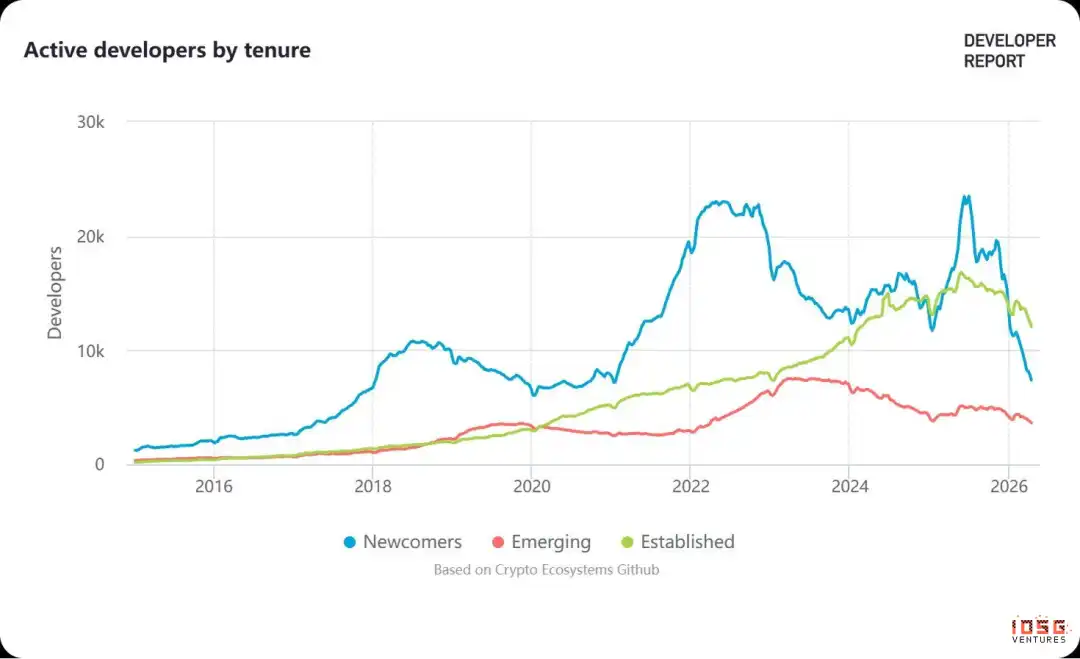

In 2026, the GitHub activity curve of the Crypto open-source community completed a remarkable "base-building." It fell back to about 23K monthly active developers from its peak of 45K in 2022. This halving on paper sparked discussions about "narrative exhaustion" on social media. However, when we dissect the cross-section of this curve, we see not the industry's contraction, but a profound "talent deleveraging."

Who Left? Who Stayed?

The ones who left were primarily newcomers. New developers peaked at 5,462 in February 2024 before plummeting, with a 52% churn rate for those with less than one year of experience. This group mostly rushed in during the bull market, working on NFT minting contracts, forking DeFi protocols, and building frontends for new L2s.

These roles were highly dependent on market hype. When the hype faded and projects ceased operations, the jobs disappeared. Data shows that newcomers' code contributions never exceeded 25% of the total. This group was never at the industry's core from the start.

On the other hand, developers with over two years of experience not only didn't decline but actually hit a record high during the same period, contributing about 70% of the code volume. The judgment from Maria Shen, GP at Electric Capital, was direct: "When we look at the established developers group, it is growing and looks very healthy."

They didn't stay because they had no other options.

Technically, the core crypto work now is infrastructure development requiring years of accumulated knowledge to truly understand: protocol-layer development, security audits, cross-chain architecture. These roles require years of accumulation and aren't easily eliminated when market fervor recedes.

Economically, many veterans hold unvested tokens, governance power in protocols, and equity stakes. Their accumulated capital in this industry has formed real barriers and returns.

Looking at ecosystem distribution, their feet are voting: Bitcoin developers grew 64.3% in two years, Solana +11.1%, while Cosmos fell 51.1% and Polkadot fell 46.9%. Veterans are concentrating in ecosystems with real users and revenue, leaving projects still running on narratives.

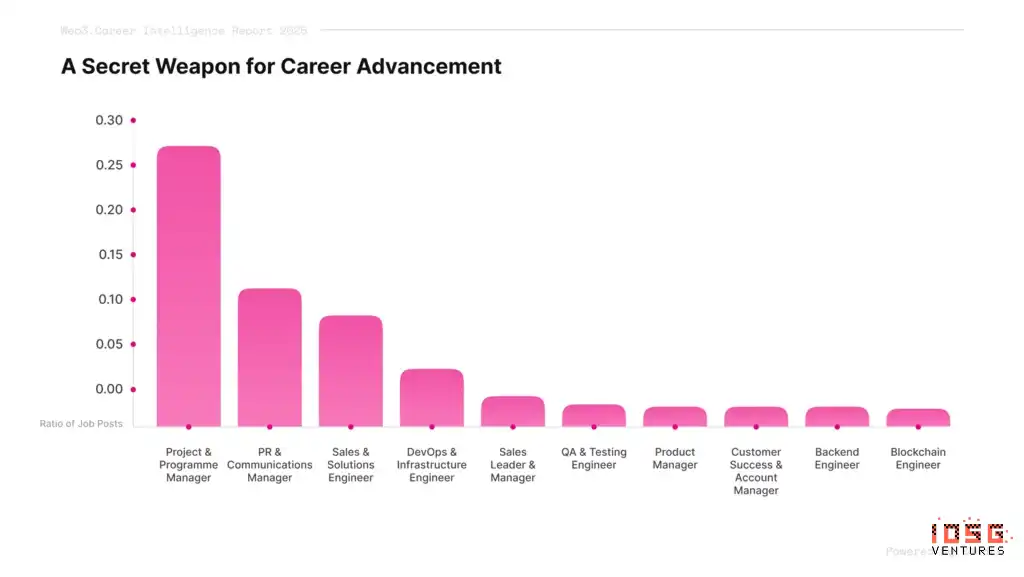

Changes in job structures also confirm the same story. In 2025, the highest proportion of new Web3 job openings wasn't for developers, but for Project & Programme Management, exceeding 27%.

This is counterintuitive for an industry known for being technology-driven, but the underlying logic isn't complicated: the industry has shifted from a building phase to an execution phase. Over 100 chains need integration; institutional clients bring entirely different compliance and security requirements; DAO governance requires balancing stakeholders with diverse interests.

This isn't project management in the traditional sense, but coordination and judgment in an environment where the rules are still being formed.

The industry appears to be shrinking on the surface, but its core density is actually increasing. The 2018-2019 bear market similarly saw massive developer attrition, yet it was followed by the emergence of groundbreaking projects like Uniswap, Aave, and OpenSea, which defined the 2020-2021 bull market. The builders who stayed through this cycle have more mature infrastructure, and the AI era has given them a stage larger than the last one.

What Abilities Do Those Who Stayed Possess?

What unique capabilities has this industry, Crypto, actually forged in its builders? To answer this, we need to return to the underlying principles of blockchain. Throughout the alternating bull and bear cycles, this industry has always operated under the same foundational rule: code is law, execution is finality.

The 2016 DAO incident saw an attacker exploit a recursive call vulnerability to siphon off $36 million. The code had no bugs; the logic executed exactly as intended; the edge case was simply not anticipated by the designers. The 2021 Poly Network cross-chain bridge attack saw $610 million moved within hours.

No platform could stop it, no institution could reverse it, no legal clause could recover it. This is the structural characteristic distinguishing crypto from almost all other industries: zero margin for error, almost no possibility for post-hoc intervention.

This environment forges a set of skills rarely required in other industries: the ability to build functioning systems that strangers are willing to participate in, from scratch, under conditions of missing rules and trust.

This ability has two layers. The first is establishing trust from zero, relying on no external authority, only on code and mechanisms to make strangers willing to place real assets inside. The second is making judgments under dual technological and economic uncertainty—without regulatory frameworks, historical data, or industry standards for reference—and still designing a system that can function.

Both layers have concrete validation in crypto. Uniswap had no corporate guarantor, no KYC, no customer service. Anyone providing liquidity relied solely on trust in a few hundred lines of code and an economic mechanism, achieving daily trading volumes of tens of billions of dollars.

MakerDAO has no central bank backing, no deposit insurance, maintaining DAI's stability purely through on-chain governance and collateral mechanisms.

During DeFi Summer, it was even more extreme. Without regulatory frameworks, audit standards, or any historical data, builders designed AMMs, lending protocols, and liquidity mining, going from concept to tens of billions in TVL in just months. This ability manifests differently in protocol-layer, application-layer, and governance-layer builders, but the underlying principle is the same.

The AI era is creating a structurally highly similar problem. The model decision-making process is opaque, and outputs cannot be independently verified. AI agents are beginning to autonomously execute transactions and allocate funds, with accompanying rule systems and constraint mechanisms still non-existent.

Large model companies control both the models and the evaluation standards, leaving users without effective verification methods. Computing power is highly concentrated in a few top firms, leading to monopoly pricing when demand explodes. These problems point to the same core: the trust problem of autonomous systems is replaying at a larger scale with AI.

Crypto builders have been dealing with such problems for years in environments without external authoritative rule constraints, only the previous scenarios were on-chain protocols, now replaced by AI. And a group has already taken the capabilities accumulated in crypto directly into AI, with proven results.

How Are These Abilities Being Repriced in the AI Era?

Cases of shifting from crypto to AI have become frequent in recent years, but upon closer look, what they took away is not the same.

The most direct route is the direct transfer of hardware and experience. CoreWeave's three founders—Michael Intrator, Brian Venturo, and Brannin McBee—started GPU mining Ethereum in 2017, scaling from one machine to thousands. They shut down mining operations in 2022; two months later, ChatGPT was released. Their GPUs directly became AI computing power supply. They went public on NASDAQ in March 2025 with an IPO valuation of approximately $23 billion, later reaching a peak market cap near $70 billion.

OpenSea co-founder Alex Atallah dealt with the aggregation and routing of highly heterogeneous assets in the NFT market. Applying the same experience to AI model routing, he founded OpenRouter, serving over 5 million developers within two years with a valuation of $500 million.

Another type of migration is more noteworthy. NEAR founder Illia Polosukhin is a co-author of the Transformer paper. After leaving Google, his initial goal was to build AI applications using natural language. During development, he encountered a practical problem: making cross-border payments to data annotation workers worldwide, many of whom lacked bank accounts. Blockchain technology became the best solution for this payment challenge.

Now NEAR is pivoting to an AI infrastructure platform, focusing on user-owned AI and decentralized confidential machine learning (DCML), allowing users to utilize AI services without exposing data. The decentralized architecture experience accumulated at NEAR has become the hardest-to-replicate starting point in this direction.

Circle co-founder Sean Neville left to found Catena Labs, positioning it as an AI-native bank, directly transferring understanding of stablecoin infrastructure to AI agent financial scenarios, with a16z crypto leading an $18 million seed round.

Aave and Lens Protocol veteran developer Nader Dabit pivoted to Cognition, bringing experience in developer ecosystem building from multiple crypto protocols into the AI agent tooling space.

What this group takes away isn't just GPU hardware or user networks, but intuition for mechanism design, experience in building developer ecosystems, and the judgment to build trusted systems from scratch when rules are absent. These abilities correspond exactly to three structural gaps encountered in AI scaling.

Aggregation and Optimization of Computing Power

Computing power is the most direct bottleneck for AI scaling. Training and inference require massive GPUs, demand fluctuates heavily, cloud vendors are expensive with waitlists, and companies don't want to hoard hardware themselves. This problem has two layers: how to aggregate and allocate computing power, and how to use aggregated power more efficiently. Crypto builders have directly transferable accumulation in both layers.

Hyperbolic solves the allocation and trust problem. Founder Jasper Zhang brought decentralized mechanism design into the AI computing power track: tokens incentivize dispersed GPU owners to contribute idle computing power, but the core issue is trust.

Why trust the computation results from a stranger's node? The core innovation, Proof of Sampling & Proof (PoSP), uses random sampling plus game theory to make honesty the dominant strategy for nodes. No full verification is needed, overhead is low, it's scalable, and results are reliable. This mechanism directly migrated from crypto's logic for verifying stranger node behavior.

MoonMath solves the efficiency problem. Its predecessor, Ingonyama, focused on ZK hardware acceleration, boosting ZK proof generation speeds several-fold under extreme computational constraints.

Now pivoting to the Physical AI performance layer, working on sparse attention acceleration for video diffusion models (LiteAttention), low-rank factorization for FFN layers (LiteLinear), and training backpropagation acceleration (BackLite). The underlying ability from ZK acceleration to AI inference acceleration is the same: making math run faster under extreme computational constraints. The track changed, but the accumulation wasn't wasted.

AI Governance and Incentive Mechanism Design

When multiple AI agents start collaborating on tasks, how do we ensure they don't disrupt the overall system while pursuing their individual objectives? Each participant pursues its own objective function; no one guarantees the system remains functional when combined, and agent execution speed far outpaces human intervention windows.

This is a problem type crypto builders have repeatedly dealt with in DAO governance and tokenomics design: making participants with completely different interests operate according to the system's preset direction without a central authority. Crypto's answer is economic mechanisms: violations incur real economic costs, rules are written in code, and execution is automatic.

EigenLayer directly migrated this mechanism to the AI scenario. Through its restaking mechanism, nodes must stake assets before participating in collaboration. Non-performance or violations trigger automatic penalties. Rules aren't suggestions; they are rigid boundaries with real economic consequences.

EigenCloud extends this logic to verifiable computation and collaborative governance for AI agents, ensuring agents pursuing their own objectives must operate within preset bounds. Constraining agents with economic mechanisms is far more reliable than using ethical guidelines.

Autonomous Payment for AI Agents

There's an even more fundamental problem: how do agents pay? Traditional payment systems are designed for humans: credit cards require accounts, bank transfers need authorization—each step assumes the operator is human, has an identity, and will wait. Agents don't wait; they might initiate numerous requests per second, each possibly involving micro-payments. Traditional payment pipelines fail directly in this scenario.

Stablecoins and on-chain rules are the infrastructure crypto builders have already built, natively supporting programmability, permissionlessness, and 24/7 operation. These three characteristics happen to be the hard requirements for agent payment scenarios, lacking only a layer of protocol connecting stablecoins to agent workflows.

x402, launched by Coinbase in May 2025, activates the HTTP 402 status code, embedding stablecoin payments directly into HTTP requests. Agents complete payment simultaneously with request initiation, no account needed, settlement in about two seconds.

As of April 2026, the x402 protocol has processed over 165 million transactions, with cumulative transaction volume around $50 million, and 69,000 live agents (Source: x402 Foundation). Cloudflare, AWS, Stripe, and Anthropic MCP have already integrated. Agent payments are already a track with real traffic.

These three directions correspond to three structural gaps encountered in AI scaling: aggregation and efficiency of computing power, incentive alignment for multi-agent collaboration, and infrastructure for autonomous payments. These problems have no ready answers in traditional software architecture, but Crypto has corresponding experience. The abilities haven't disappeared; they've just found new scenarios to bear.

Builder's New Positioning: From Contract Writers to Rule Setters for AI

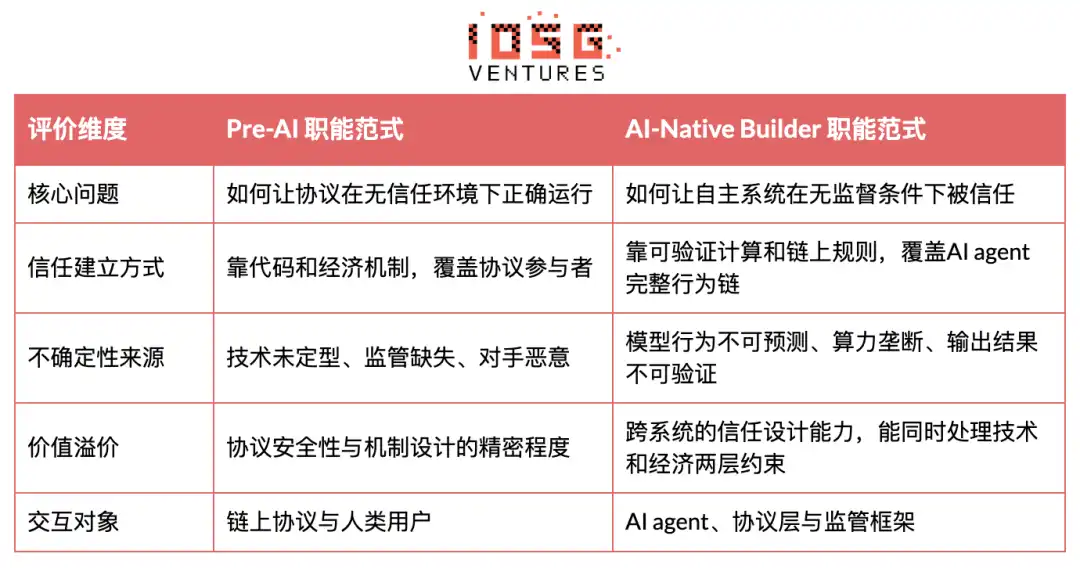

AI scaling is creating a previously non-existent functional gap. Not a gap in technical talent, but a gap in people who can design trust mechanisms within autonomous systems. As the service target shifts from humans to AI, the role of crypto builders is also being redefined.

The table below contrasts the dimensional changes in specific functional paradigms:

The core difference between the two paradigms lies not in the technology stack, but in the way trust is established and rules are executed. In the pre-AI era, crypto builders faced human participants, rules were written into contracts with zero error tolerance, but the system boundaries were relatively clear.

In the AI-Native era, when the interacting entities become autonomously operating AI agents, the problems needing solution are: agent behavior is unpredictable, execution speed far exceeds human intervention windows, and the system boundaries themselves need redefinition under greater uncertainty.

The functional positioning of crypto builders is shifting from "writing secure contracts" to "designing trustable mechanisms for AI autonomous systems."

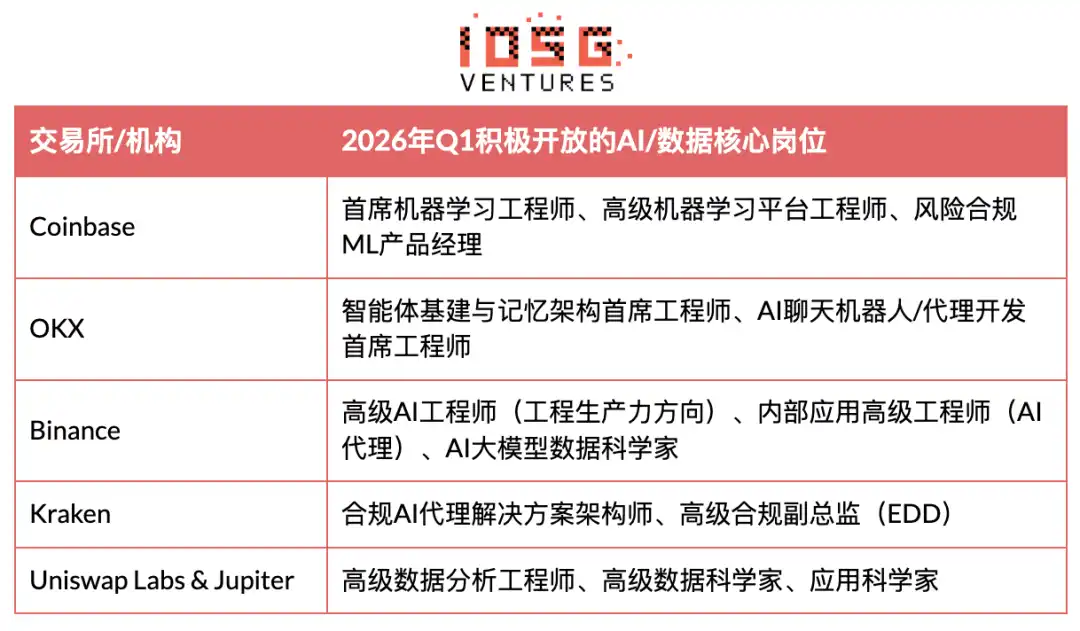

Hiring by leading institutions already reflects this change:

Hiring at leading exchanges and institutions in 2026 clearly reflects this trend: no longer just recruiting AI engineers or crypto developers, but seeking individuals who can connect the two—those who understand on-chain incentive distortions and governance games, can deeply embed AI tools into crypto workflows, and design mechanisms aligning agents long-term with regulation and users.

Capital allocation directions already reflect this judgment. Paradigm is raising a new fund up to $1.5 billion, expanding its investment scope from crypto to AI and robotics.

Haun Ventures closed a $1 billion Fund II, focusing on financial infrastructure integrating crypto and AI, especially payments, stablecoins, and agent-to-agent economic systems supporting autonomous AI agent trading and coordination.

a16z crypto closed a $2.2 billion fifth fund (Crypto Fund V), explicitly stating it will be 100% deployed into the crypto space. Facing the complexity and opacity of the AI era, they will focus on applying crypto's transparency, verifiability, and decentralization characteristics.

Furthermore, according to PitchBook data, in 2025, about 40% of VC investment in the US crypto space flowed to companies also involved in AI business, a significant increase from 2024.

Similarly for crypto builders pivoting to AI, the paths chosen show clear differences across market environments.

In the US, as the regulatory environment became relatively clearer, protocol-layer innovation gained real survival space. Capital network density is high, the path from idea to funding is short, and there is greater tolerance for error.

Projects like Hyperbolic, EigenCloud, Gensyn, Ritual share the characteristic of designing new mechanisms from scratch, rather than simple application integration on existing systems. Top VCs have clear investment theses on directions like "verifiable computation, Agent coordination, decentralized ML" and are willing to provide ample tolerance for early-stage technological exploration.

The situation in Asia is different. Singapore and Hong Kong China play more roles in compliant implementation and institutional fund routing. Regulatory frameworks are relatively conservative, with lower tolerance for pure protocol-layer innovation. When crypto-background builders pivot to AI, they more often choose application-layer and industrial integration paths—leveraging user bases, payment capabilities, or data assets accumulated in crypto to quickly integrate into AI products and services.

This isn't a capability gap, but a difference in path choice caused by varying market signals and regulatory environments: The US encourages more underlying mechanism innovation and early-stage tech exploration, while Asia emphasizes compliance-friendliness, rapid monetization, and deep integration with traditional industries.

Returning to that initial GitHub curve. Monthly active developers dropped from 45K to 23K, superficially indicating industry contraction. But among those who stayed, the proportion of established devs hit a record high. They are flocking to ecosystems with real users while being repriced by the AI industry in unprecedented ways.

When AI scaling encounters structural bottlenecks like computing power aggregation, agent autonomous payments, data and decision verifiability, and privacy coordination, these builders' long-accumulated sensitivity to rules, incentives, and authenticity is gradually transforming into a system-level ability scarce in the AI era at the intersection of Crypto and AI.

As an investment firm deeply entrenched in crypto infrastructure since 2017, IOSG's judgment on this line goes beyond mere observation.

We invested in EigenLayer's restaking mechanism before it was widely recognized by the market, led the seed round for Ingonyama (now MoonMath) betting on ZK hardware acceleration's migration to the AI performance layer, and invested in Hyperbolic in 2024, optimistic about its path of using crypto-native verification mechanisms to solve trust problems in decentralized computing power.

The common logic behind these investments is: the trust, coordination, and verification problems encountered in AI scaling will ultimately require the mechanism design capabilities accumulated by the crypto industry to solve. We believe the convergence of crypto and AI is not a narrative, but a structural opportunity already unfolding.