作者:克洛德,深潮 TechFlow

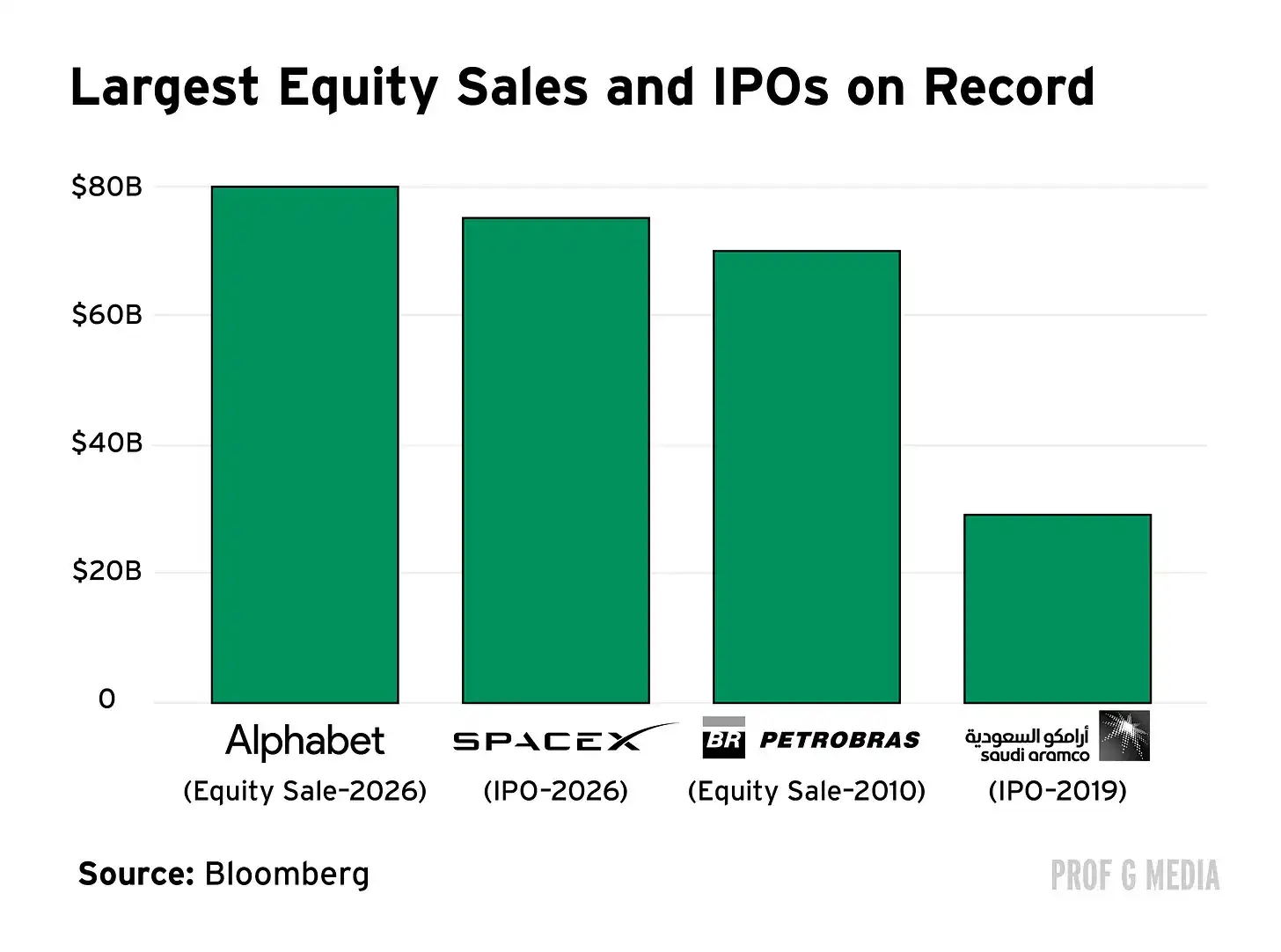

深潮导读: Alphabet 于 6 月 2 日完成 847.5 亿美元股权融资定价,打破巴西国家石油公司 2010 年创下的 700 亿美元纪录。首批发行计划 400 亿美元,因超额认购放大至 450 亿美元;伯克希尔·哈撒韦以 100 亿美元定向认购锚定机构信心。

与此同时,SpaceX 750 亿美元 IPO 定于 6 月 12 日挂牌纳斯达克,Anthropic 和 OpenAI 均已秘密递交 S-1。2026 年 AI 相关股权融资总量可能突破 4000 亿美元,是去年 IPO 市场的 9 倍。

Alphabet 向资本市场投下了一枚重磅炸弹。

据 SEC 文件及彭博报道,Alphabet 于 6 月 2 日完成了总计 847.5 亿美元的股权融资定价,这是有史以来全球规模最大的单次股权发行,超过巴西国家石油公司(Petrobras)2010 年创下的 700 亿美元纪录逾 140 亿美元。CEO 桑达尔·皮查伊在 X 平台发文称,首批发行因超额认购从 400 亿美元扩大至约 450 亿美元。消息公布后,Alphabet 股价下跌约 4%。

这笔钱的去向明确:AI 基础设施。皮查伊将其定义为「多年投资战略的一部分,以抓住 AI 带来的机遇」。Alphabet 2026 年资本支出指引已上调至 1800 亿至 1900 亿美元,接近 2025 年全年 914 亿美元的两倍。

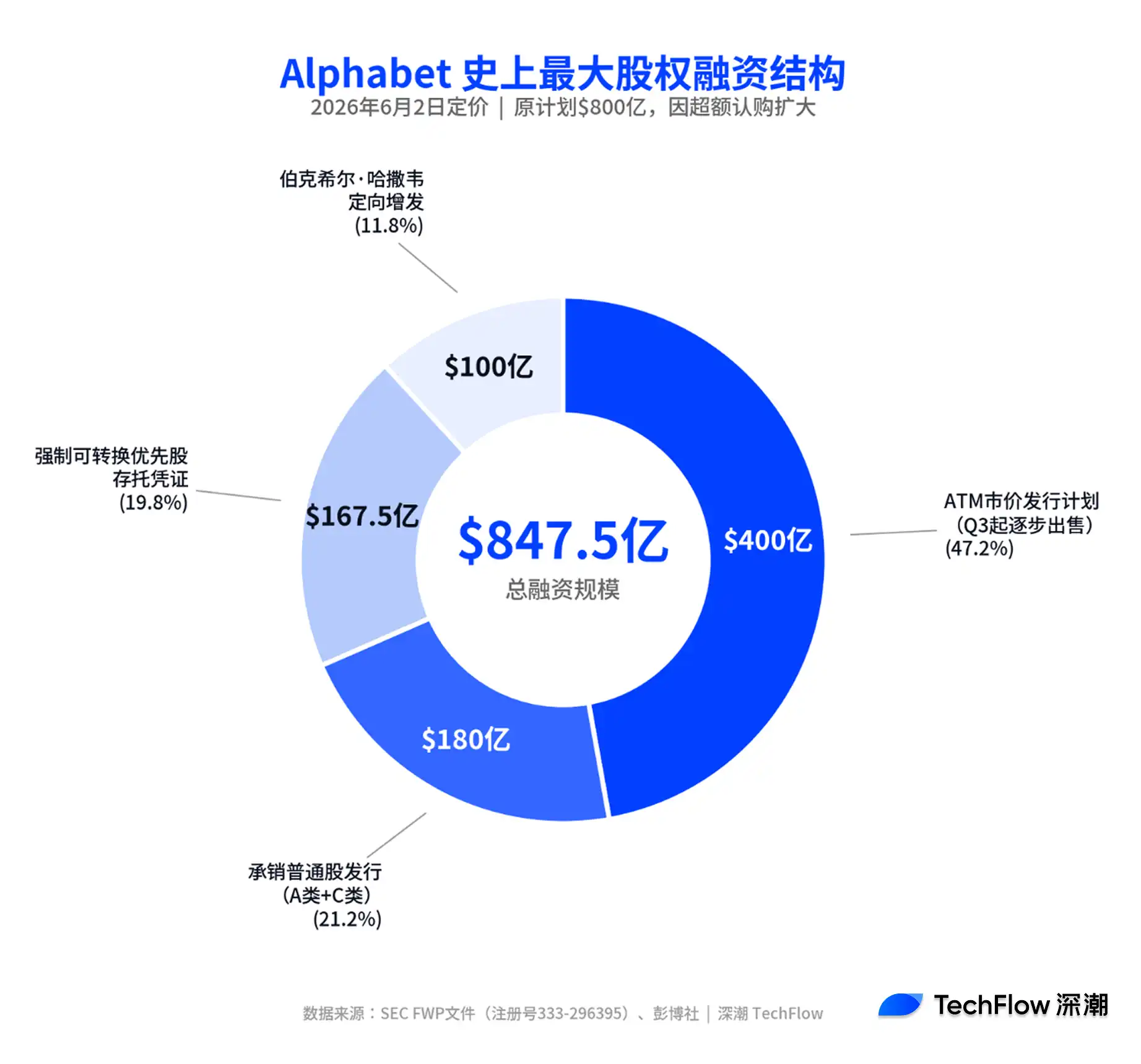

847.5 亿美元怎么筹的:四层结构拆解

此次融资并非简单的公开市场增发,而是由四个组件拼成的复合结构。

据 SEC 提交的 FWP 文件,具体构成为:180 亿美元的 A 类普通股和 C 类资本股承销发行(从原计划 150 亿美元扩大);167.5 亿美元的强制可转换优先股存托凭证(从原计划 150 亿美元扩大),附带 6.25%固定股息率;400 亿美元的市价发行计划(ATM),将从第三季度起逐步向市场出售股份;以及伯克希尔·哈撒韦 100 亿美元的定向增发。

承销部分定价为 A 类股每股 355.20 美元、C 类股每股 351.80 美元。普通股和存托凭证发行分别于 6 月 4 日和 6 月 5 日完成交割。

以 Alphabet 约 4.2 万亿美元的总市值计算,此次融资规模不到市值的 2%。据 Seeking Alpha 分析,考虑到发行结构和员工期权税务义务,实际稀释效应可能低于账面数字。

巴菲特 100 亿美元认购:价值投资者给 AI 基建投了信任票

伯克希尔·哈撒韦的 100 亿美元定向认购是本轮融资中最受关注的单笔交易。

据 SEC 文件,伯克希尔以约 6.5%的折扣认购了等量的 A 类和 C 类股份。这家以价值投资闻名的公司,长期以来被视为科技投资领域的保守派。但从重仓苹果到如今直接参与 AI 基建融资,伯克希尔的出手意味着一个信号:即便最谨慎的机构资本,也已将 AI 基础设施视为值得下注的资产类别。

据 TechCrunch 报道,皮查伊在 X 平台专门提及伯克希尔的参与,强调其「对价值投资的长期承诺」与 Alphabet 的投资逻辑一致。

Google 的底气:Q1 收入 1100 亿,云业务积压订单超 4600 亿

Alphabet 敢在此刻开出 850 亿美元的融资支票,底气来自一组硬数据。

2026 年一季度,Alphabet 总收入达 1100 亿美元,同比增长 22%。其中 Google Cloud 收入 200 亿美元,同比增长 63%,合同积压订单从上季度近乎翻倍至超过 4600 亿美元,约 50%预计在未来 24 个月内确认为收入。Google 搜索及其他业务收入同比增长 19%至 604 亿美元,Google 付费订阅用户达到 3.5 亿。据 Prof G Media 报道,Gemini 月活跃用户已接近 9 亿。

皮查伊在一季度财报电话会上直言:「我们在短期内受到算力供给的约束」,CFO 阿纳特·阿什肯纳齐补充称,2027 年资本支出预计将「再次大幅增长」。换言之,1800 亿至 1900 亿美元的年度资本支出只是起点。

Alphabet 总裁兼首席投资官鲁思·波拉特在此轮融资中扮演关键角色。Prof G Markets 主持人斯科特·加洛维评价称,Alphabet 完全可以用自身资产负债表上的现金完成这笔投资,但波拉特选择了更聪明的做法:用低成本外部资本融资,同时在 Anthropic 和 OpenAI 上市之前抢先锁定投资者额度。「每一种资源都是有限的,包括投资者对 AI 基建的胃口。Google 刚刚从桌上拿走了 850 亿美元,」加洛维写道。

AI 融资超级周期:SpaceX、Anthropic、OpenAI 排队上市

Alphabet 的增发并非孤立事件,而是 2026 年 AI 资本市场超级周期的开场。

SpaceX 已于 5 月 20 日公开提交 S-1 招股说明书,计划以每股 135 美元发行 5.566 亿股,融资 750 亿美元,对应估值约 1.75 万亿美元。据彭博报道,该公司预计 6 月 11 日定价、6 月 12 日在纳斯达克以「SPCX」为代码正式挂牌交易。路演已于 6 月 4 日启动,获得超额认购。若完成,这将是全球 IPO 史上最大的首次公开发行。

Anthropic 于 6 月 1 日向 SEC 秘密递交 S-1 草案。此前 5 月 28 日,该公司刚完成 650 亿美元的 H 轮融资,投后估值 9650 亿美元,超过 OpenAI 的 8520 亿美元,成为硅谷估值最高的 AI 公司。据多家媒体报道,Anthropic 的 IPO 目标窗口为 2026 年 10 月前后,首日估值突破 1 万亿美元被视为基本预期。

OpenAI 也不甘落后。据 CNBC 5 月 20 日报道,OpenAI 正准备秘密提交 IPO 招股书草案,高盛和摩根士丹利担任主承销商,目标估值超过 1 万亿美元,上市窗口在 2026 年 9 月至 11 月之间。

4000 亿美元融资潮的供给冲击:市场能消化吗?

将这些数字加总,2026 年正在上演的资本市场融资规模前所未有。

据加洛维测算,历史上 IPO 融资规模最大的年份是 2021 年,全年约 1400 亿美元。仅 Google 增发加上 SpaceX、Anthropic、OpenAI 三家 AI 巨头 IPO,融资总额已远超这一纪录。若再算上 Cerebras 等其他 AI 相关上市项目和整个 2026 年融资管线,全年股权发行总量可能突破 4000 亿美元,是去年 IPO 市场规模的约 9 倍。

加洛维提出了一个令人清醒的历史数据:过去 30 个重大 IPO 中,上市一年内的平均最大回撤幅度为 55%。「IPO 时刻是炒作的顶点、需求的顶点。你在与全球每一个基金经理争夺每个人都想要的股份,」他写道,「更聪明的做法通常是等待炒作退潮,在恐惧高于贪婪的时候找到入场点。」

对投资者而言,加洛维给出了一个简洁的框架:想要 AI 敞口但不确定 Anthropic 或 OpenAI 是否值那个估值?买 Google。它已经是有史以来最伟大的商业之一,估值相对合理,提供上行空间但风险远低于纯 AI 公司。如果 AI 最终令人失望,Alphabet 不会消失,但其他公司不一定。