Article compiled by: Block unicorn

The company has earned billions in interest income by holding Treasury reserves as collateral for its stablecoin, and pays fees to other platforms for distributing and settling USDC throughout the payment system. For every dollar Circle earns, it pays out about 60 cents to its USDC partners. As long as the profit margin was large enough, it could afford this cost. But with the arrival of a low-interest-rate environment, the USDC issuer lost too much profit. For most of its existence, Circle had only one product: USDC.

In its recently released Q1 2026 earnings report, the USDC issuer announced several initiatives aimed at enhancing the value captured within its operational scope. These include: a $222 million presale for its native Layer-1 token ARC at a fully diluted valuation of $30 billion; the launch of AI agent infrastructure; and the expansion of its Circle Payments Network, enabling banks to facilitate stablecoin payments by bypassing the volatility of digital assets. However, achievements from the past few quarters will change this status quo.

In summary, these moves signal Circle's attempt to transform from a single-layer company into a full-stack financial platform capable of operating and capturing value across multiple layers of the payment stack.

Today, I will assess whether Circle can use vertical integration to offset the erosion of its yield-generating business, which shrinks with every Federal Reserve rate cut.

The Vanishing Float

In Q1 2026, Circle's total revenue was $694 million, a 20% year-over-year increase. This growth was entirely due to the expansion of stablecoin circulation, with no improvement from USDC itself. The circulating stablecoin supply grew from $235 billion in March 2025 to $315 billion in March 2026, an increase of over 30%. During the same period, USDC's market share declined by 62 basis points.

Circle faces a bigger problem. The era of low interest rates has arrived, with the Fed rate dropping from 4.5% a year ago to the current 3.75%.

Despite a 39% year-over-year increase in the average circulating supply of USDC through Q1 2026, Circle's reserve income only grew 17% year-over-year to $653 million. This is because the average reserve yield decreased by 66 basis points year-over-year, dropping from 4.16% in Q1 2025 to 3.50% in Q1 2026, significantly offsetting the aforementioned growth.

This is not a one-time phenomenon. The gap between Circle's reserve revenue growth rate and USDC supply growth rate has been narrowing for the past four quarters.

Circle's primary revenue source is not growing proportionally with its circulating stablecoin supply.

The company also faces a value leakage problem.

The 60-Cent Wake-Up Call

This means the cost of platforms holding and distributing USDC exceeds 60 cents per dollar earned. Of the $405 million in distribution and transaction costs paid by Circle in Q1 2026, approximately $330 million (about 80%) went to Coinbase. Out of the quarter's $653 million in reserve income, Circle paid $405 million to partners for distribution and transaction costs.

In an industry where new players are constantly emerging and integrating across all layers of the tech stack, this is a massive amount of money left on the table.

At this point, the signs are clear that Circle should face reality. Interest rates keep falling, dragging down its reserve income; distribution costs remain high, causing constant value leakage; and Circle's core business remains a proxy for yield, shrinking in value with each Fed rate cut. Under the leadership of U.S. President Donald Trump, market expectations for a dovish Fed are growing stronger.

What is Circle's response? The answer: capture more value across the entire business chain through vertical integration and reduce reliance on interest rate income.

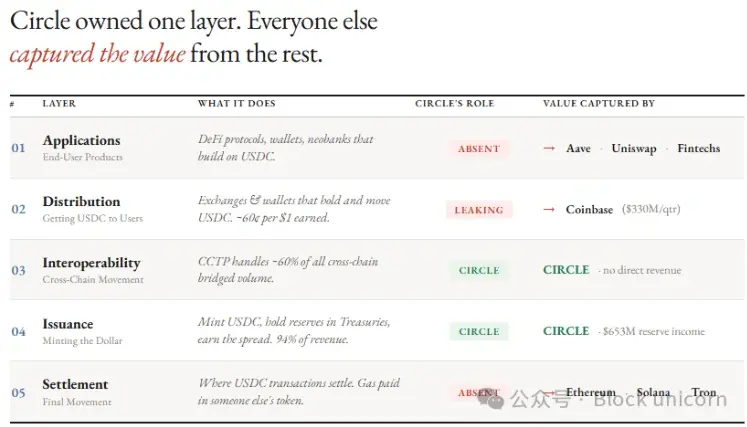

To understand what Circle is building, consider what it currently possesses.

The USDC issuer started at the bottom layer of the stablecoin stack—the issuance layer—and for years watched others capture value at every layer above it.

At the issuance layer, Circle issues USDC and EURC, holds U.S. Treasury reserves via the BlackRock-managed Circle Reserve Fund, manages the 1:1 peg, and handles issuance and redemption through Circle Mint. 94% of its total revenue comes from government bond reserve yields.

Subsequently, Circle expanded into the interoperability layer via its Cross-Chain Transfer Protocol (CCTP), which transfers USDC between blockchains and handles about 60% of cross-chain bridging volume. Although this mechanism routes USDC across chains, CCTP itself runs on chains owned by others. Therefore, Circle cannot derive significant direct revenue from it.

All other layers in the stack belong to others.

Settlement systems run on Ethereum, Solana, and Tron. Every USDC transaction pays gas fees in other tokens (ETH, SOL, TRX), and Circle has no control over congestion, fees, or governance on these chains.

Distribution channels rely heavily on Coinbase, exchanges, and wallets. Circle must pay revenue shares, incentive program fees, and integration costs to get USDC into users' hands.

Third parties, such as DeFi protocols, fintech companies, neo-banks, and prediction markets, build applications and products that use USDC. This means end customers, whether retail or institutional, do not need to transact directly with Circle.

This structure results in Circle capturing only about 40 cents of every dollar it generates.

Controlling the Stack

On May 11, Circle announced three investment plans aimed at vertically integrating different layers of the business it previously did not own.

First, settlement. Circle owns the native Layer-1 blockchain, Arc, designed to capture the fees currently generated when USDC is transferred on chains like Ethereum, Solana, and Tron.

The EVM-compatible Arc offers sub-second finality and uses USDC as its native gas fee token, with each transaction costing about $0.001. To make its chain more attractive to institutional users, Circle offers configurable privacy and quantum-resistant architecture. In contrast, general-purpose public chains like Ethereum and Solana are completely transparent and cannot provide privacy for sensitive transactions like institutional payments.

Circle raised $222 million through an ARC token presale, reaching a $3 billion valuation. This funding round was led by a $75 million investment from a16z, with other investors including BlackRock, Apollo Global Management, Intercontinental Exchange (owner of the NYSE), Standard Chartered, ARK Invest, SBI Group, IDG Capital, Bullish, and Haun Ventures.

Second, distribution. The Circle Payments Network (CPN) helps the USDC issuer reduce its dependence on Coinbase.

CPN connects financial institutions directly to Circle's network, enabling them to mint, redeem, and route USDC without going through exchanges. The network has 136 registered institutions (up 36% quarter-over-quarter), an annualized transaction volume of $8.3 billion (up 17% quarter-over-quarter), and facilitates fiat payments in over 50 countries.

Consequently, the percentage of USDC based on Circle's own infrastructure nearly tripled, from about 6% a year ago to 17.2%. Even with declining reserve yields, the RLDC margin (revenue minus distribution and transaction costs as a percentage of revenue) steadily recovered from 38% in Q2 2025 to 41% in Q1 2026.

Circle has not yet commercialized CPN, prioritizing user growth over charging fees. But once commercialized, for every additional dollar of CPN usage, Circle will gain usage-based revenue, independent of interest rates.

Third is the application layer. Through products like Agent Wallets, Nanopayments (supporting gas-free USDC transfers as low as $0.000001 [one millionth of a dollar]), Agent Marketplace (where agents can discover and pay for services), and Circle CLI (accelerating agent registration and wallet configuration), Circle is building a full agent economy.

Through this third layer, Circle aims to capture ongoing value across the agent economy by charging small fees on high-volume transactions executed by AI agents.

How big is the market opportunity for agent payments? Last month, Circle's Head of Marketing, Peter Schroeder, posted that USDC accounted for 98.6% of the 140 million transactions completed by AI agents within nine months.

The Stack Race

Circle's expansion into the payment stack is not easy. The payment giant Stripe started at the top and worked its way down through a series of acquisitions and product launches. Acquiring Bridge gave Stripe control over authorization, custody, forex, and card issuance layers. Launching Tempo brought Stripe into the settlement layer. Today, Stripe controls all seven payment layers, serving 5 million merchants.

Tether uses Plasma, incubated by the USDT issuer, as its settlement chain. However, Tether's regulatory scrutiny still falls short of USDC's.

Stripe dominates human-to-human transactions, while Tether leads in dollar transactions in emerging markets and crypto trading. Therefore, Circle is positioning itself in institutional settlement and machine-to-machine transactions, where regulatory credibility and programmable infrastructure may be more critical than the checkout integrations Stripe dominates.

CRCL's Fight Back

Although Circle raised $222 million by preselling ARC tokens to institutional investors, the initial development funding for ARC actually came from CRCL shareholders. Ironically, the biggest resistance Circle may face is internal.

What does the appreciation of the Arc token mean for a public company? I pointed out this issue last November.

"The nature of the native token will cause some controversy in public markets. Why should the market recognize or value a native token that captures the value created by Arc and CPN, instead of having that value flow back to Circle's P&L? Why should Circle's surplus be used to fund a cost center not expected to return profits to shareholders? Existing shareholders would never tolerate this. Public market investors bought CRCL for its reserve yield. They are unlikely to watch a new asset absorb the appreciation from the infrastructure they invested in."

How will Circle resolve this? Is a separate listing for Arc justified? We will only know the answer after Arc's mainnet launches and its first quarter of operation.

For now, Circle's long-term goal is to capture as much value as possible by expanding its reach across these layers. Every time USDC settles on Arc, Circle earns settlement fees. When institutions transact through CPN, Circle retains the distribution profits. Finally, when agents transact via Nanopayments on Arc, Circle also hopes to capture fees at that layer.