At 1:12 AM EST on February 28, during the exchange's off-hours, trading volume on Polymarket's prediction contract regarding whether the U.S. would strike Iran surged.

At 1:13 AM, the first open-source intelligence about the airstrike appeared on Twitter.

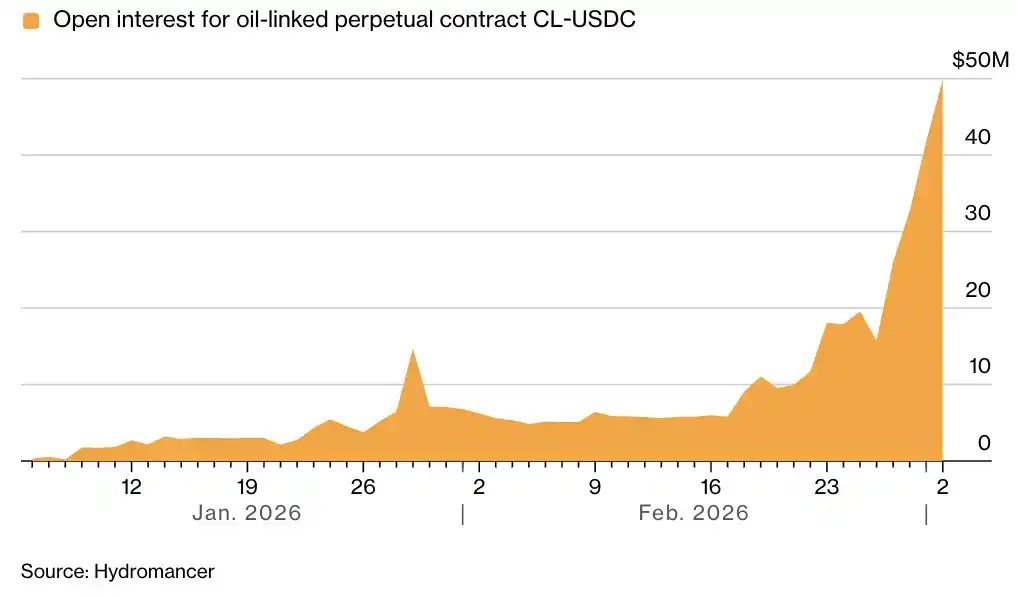

One minute later, the price and trading volume of crude oil perpetual contracts on Hyperliquid's Trade.xyz followed with unusual movements.

After the headline news developed, the crude oil perpetual contract on the Hyperliquid platform rose by 5%, with open interest (OI) climbing to $50 million. The price of HYPE increased by 13%, leading the gains among the top 25 tokens by market cap.

24/7 Trading

Of the ten high-volatility macroeconomic events over the past year, eight erupted on weekends. Hyperliquid's around-the-clock price discovery mechanism is attracting attention from traditional financial markets.

In two recent reports on Hyperliquid, Bloomberg pointed out that as the crypto market becomes increasingly intertwined with traditional finance, Wall Street has begun closely monitoring platforms like Hyperliquid. During weekends when traditional markets are closed, on-chain derivatives provide continuous risk pricing capabilities. Bloomberg cited market participants' views, stating that this全天候 pricing mechanism is a structural upgrade that enhances market efficiency. The unusual market movements over the weekend validated a trend: around-the-clock on-chain trading for all asset classes is an inevitable direction for financial market development.

Decoupling

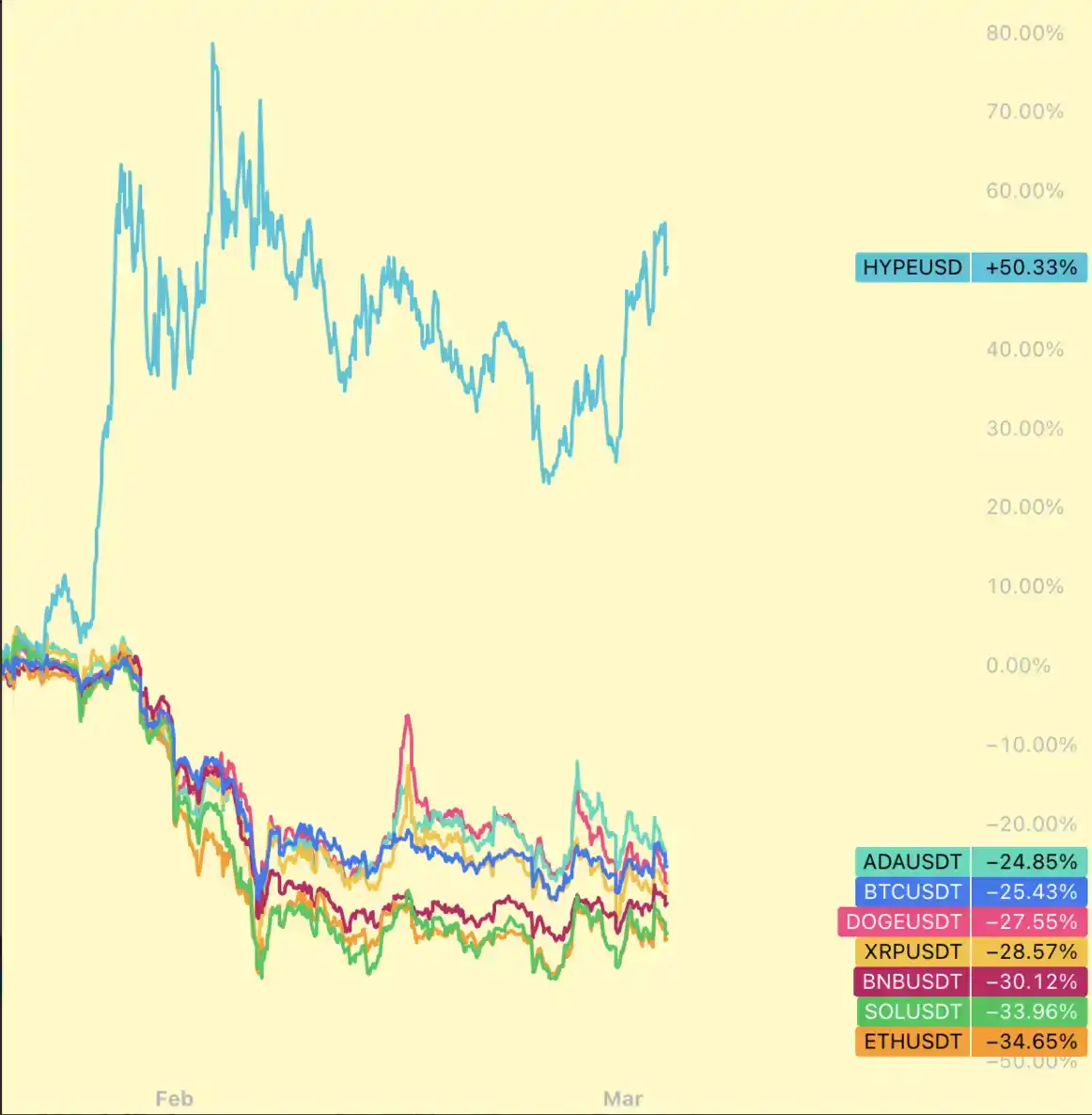

As the HIP-3, which supports traditional market trading, grows stronger, HYPE's price performance has long begun to decouple from Bitcoin, the default benchmark of the crypto market. When the news of the attack broke, Bitcoin's price initially fell and then fluctuated. In contrast, HYPE, which caters to trading demands for precious metals and stocks, demonstrated independent momentum.

In late January, when silver broke through $100 and gold surpassed $5500, the trading volume for silver alone on the HIP-3 exchange tradexyz reached $1.2 billion, driving HYPE up by 55% over three days, while Bitcoin only rose by 3% during the same period.

Tokenomics explains the reason for HYPE's strong performance. Hyperliquid's HIP-3 protocol stipulates that 50% of all fee revenue generated by HIP-3 exchanges flows into the Hyperliquid Official Aid Fund and is used to repurchase HYPE. Macro volatility drives trading volume, increased trading volume boosts repurchase scale, bringing strong buying pressure to the HYPE token.

HYPE holders are not only betting on the growth of Hyperliquid as an offshore Perp DEX but are also going long on geopolitical uncertainty.

Hyperliquid is merely the clearest expression of this narrative so far, and the market is finally starting to reflect this.

Gap

Despite this, on-chain derivatives still have a distance to go to meet traditional institutional standards.

Hyperliquid's current advantage lies in small to medium-sized retail orders. According to research by Blockworks Research, during regular trading hours, the spread of its silver contracts is comparable to that of COMEX micro contracts. However, there is a significant gap in depth. COMEX's order book depth within a ±5 basis point range reaches $13 million, while Hyperliquid's is only around $230,000.

In extreme crash scenarios, the tail risk of on-chain liquidity degradation is greater. A 1% trade in Hyperliquid silver can experience slippage of over 50 basis points, whereas COMEX maintains better execution costs under such conditions.

Currently, Hyperliquid's liquidity and funding rate models do not yet meet the needs of large funds. To compete at the institutional level, on-chain platforms need to address KYC issues and even establish technical and cooperative frameworks that match traditional clearing institutions. Many industry participants still believe that if the Chicago Mercantile Exchange (CME) were to launch 24/7 trading, it would have inherent hedging advantages and a foundation of trust.

Nevertheless, the traditional financial market's model of controlling risk by physically shutting down during off-hours indeed shows limitations. The ability to continuously price risk without waiting for the Monday market open is the core value of offshore exchanges like Hyperliquid.

The shift of market pricing power to on-chain will be a long-term process. But one must have dreams, what if they come true?