Author:angelilu,Foresight News

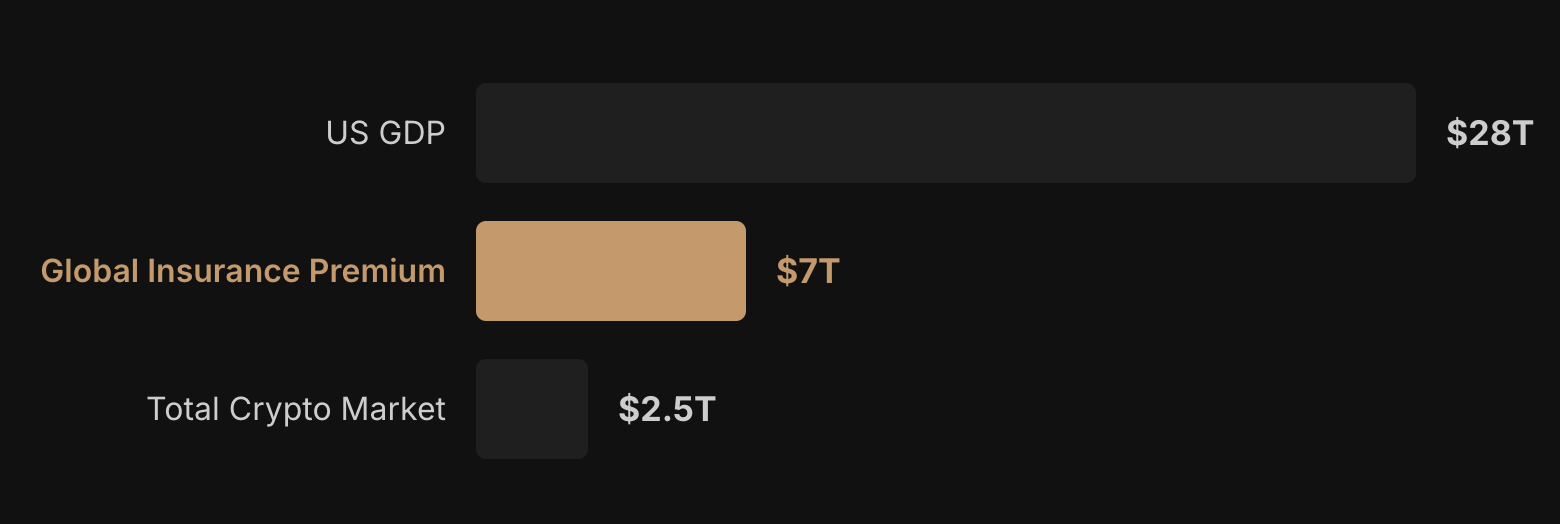

Reinsurance might be the last major financial market that has not yet been digitized. Last year, the global scale of RWA tokenization grew by more than 10 times, and the market value of stablecoins exceeded $320 billion, but the reinsurance sector has seen almost no substantial deployment of on-chain infrastructure.

One reason is the extremely high regulatory barriers. Reinsurance entities need to obtain licenses in jurisdictions, meet solvency requirements, and achieve segregated custody standards—which are difficult for ordinary DeFi teams to bypass.

A team composed of insurance technology veterans and on-chain developers is prying open this door to the 'global reinsurance market'.

Moving Reinsurance Companies' Capital Pools On-Chain

The global reinsurance market is dominated by a few giants like Munich Re and Swiss Re, where external capital cannot enter, underwriting conditions are opaque, and solvency cannot be verified. What the Re protocol does is to move reinsurance companies' capital pools on-chain, allowing anyone to deposit money into them and earn premium income.

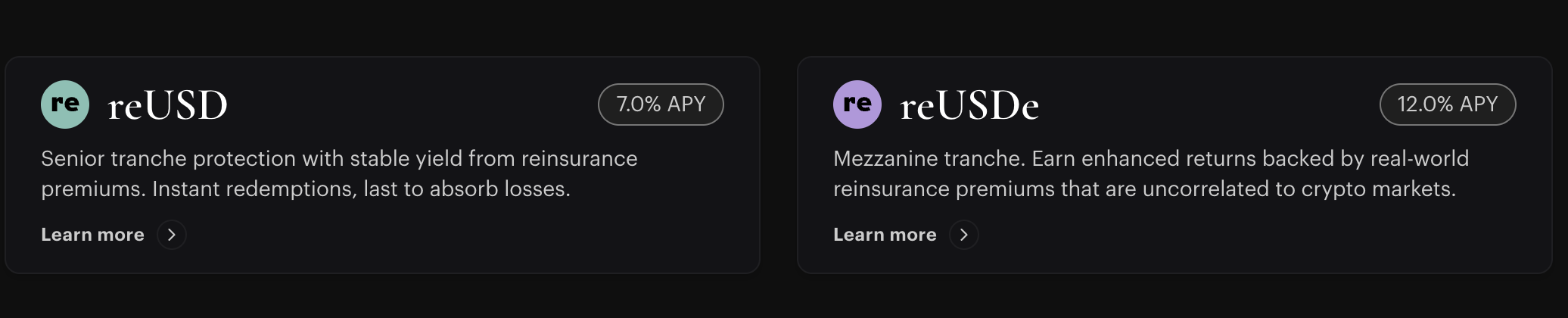

Its core model is not complicated: Insurance companies bundle part of their risks into reinsurance contracts, which are compliantly underwritten by their licensed reinsurance entity Cover Re. Decentralized liquidity providers can then deposit stablecoins into two types of tokenized tranches to earn insurance underwriting income, with the two product forms corresponding to different risk appetites:

reUSD is the senior (stable) tranche, offering principal-protected fixed income (benchmark rate + 250 basis points), with risks absorbed first by the junior tranche; reUSDe is the high-yield tranche, bearing first-loss risk, with a current highest annualized yield of about 23%. The loss absorption order is: first by reUSDe holders and Re Capital, then by reUSD.

To address the regulatory barriers, Re's solution is to separate the operation of the on-chain protocol from the licensed entity: Cover Re SPC (Cayman Islands) acts as an independent reinsurance entity to undertake compliant contracts, while the Resilience Foundation is responsible for issuing the governance token. This achieves legal separation of compliance risk from the technical risk at the protocol layer through an independent licensed entity.

Points and TGE

Re is about to launch its governance token RE. The core role of the token is to enable market participants to formulate protocol rules, but specific revenue, profits, or insurance fund flows are still operated by the licensed entity.

Re's points program aims to reward wallets that provide and store funds within the ecosystem. Its Season 1 points event recently concluded, with 7% of the total RE supply allocated to Season 1 participants. Specific claim windows and vesting mechanisms have not yet been announced. Season 2 started on June 1, 2026, currently with 2,904 active users and a total of 41.2 billion points.

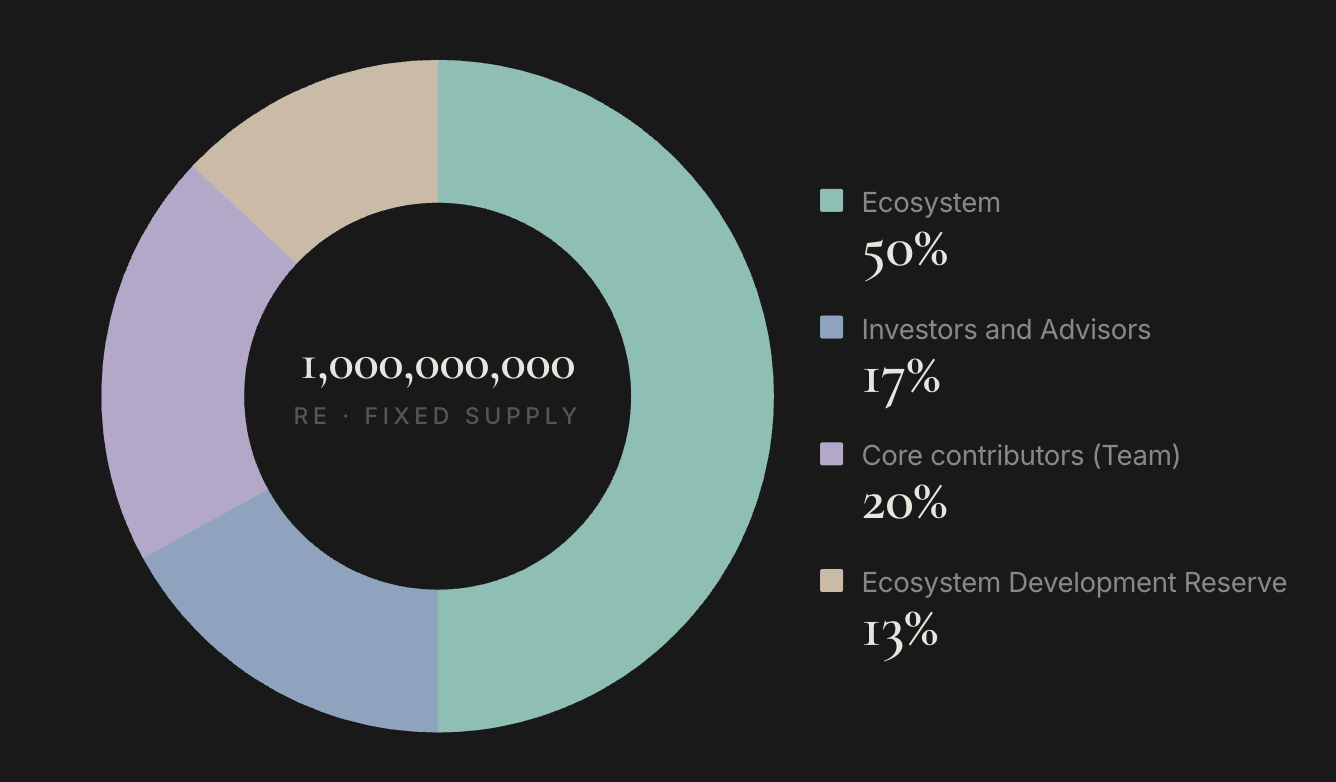

The total supply of RE is fixed at 1 billion tokens, divided into four parts:

- Ecosystem 50%: 500 million tokens, for community incentives, points program redemptions, and other ecosystem allocations. The 7% supply for Season 1 is allocated from here.

- Core Contributors / Team 20%: 200 million tokens, team allocation, typically with a vesting period; specific lock-up arrangements have not been announced.

- Investors and Advisors 17%: 170 million tokens, corresponding to seed round and strategic round investors, also expected to have lock-up periods.

- Ecosystem Development Reserve 13%: 130 million tokens, for future partnerships, protocol development, etc., managed by the foundation.

RE has been included in Coinbase's listing roadmap, but the specific TGE date has not been announced.

Re Reinsurance Data

Another major feature of Re is the low correlation of its assets. The income source of reinsurance comes from car accident rates, workplace injury occurrence rates, and property damage frequency—these numbers do not fluctuate with BTC price. When the crypto market oscillates repeatedly under geopolitical conflicts and macro policy pressures, the scarcity value of truly non-correlated assets is being repriced.

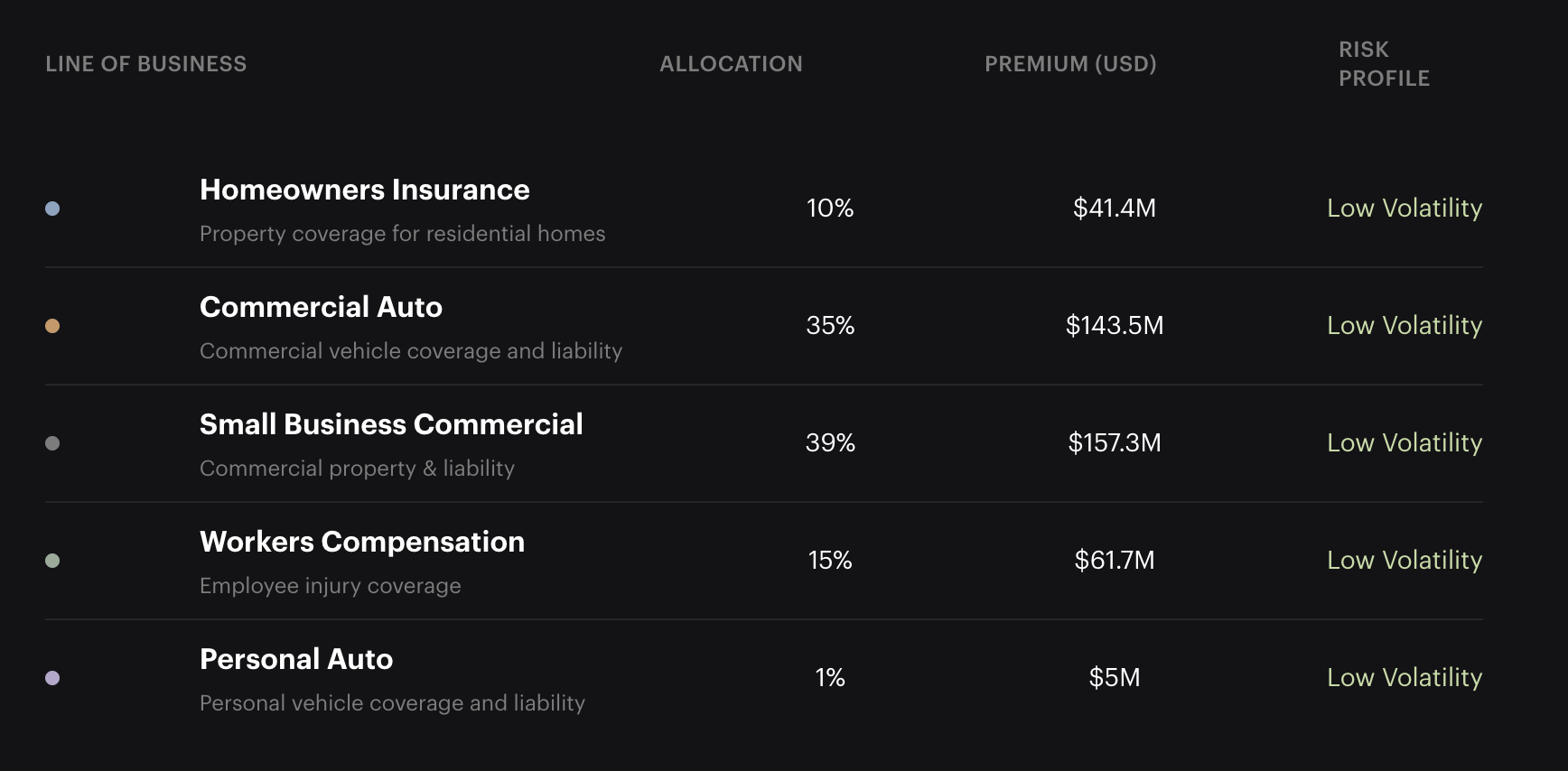

According to its official website data, as of early June 2026, its underlying underwriting portfolio totals $409 million, distributed across commercial auto insurance (35%), small business commercial insurance (39%), workers' compensation (15%), residential insurance (10%), and personal auto insurance (1%). All are in low-volatility daily insurance types, with no high-volatility catastrophic risk exposure. Each reinsurance contract is fully collateralized, with 100% cash or investment-grade assets deposited into segregated Regulation 114 trusts, and solvency can be verified on-chain.

Team and Funding

Re's CEO Karn Saroya has gone through a full round of entrepreneurial experience in the insurtech space. He previously co-founded the insurtech platform Cover, which launched in 2016, raised a total of $27 million from institutions like Exor and Tribe Capital, and later shut down due to business adjustments. Even earlier, he founded the fashion app Stylekick, which was acquired by Shopify.

Other co-founders include Anand Dhillon, Ben Aneesh, Cliff White, and Tribe Capital co-founder Arjun Sethi (the project started under the Tribe Capital crypto incubation system). The specific roles of team members have not been fully disclosed through official channels.

Re completed a $14 million seed round in September 2022, with investors including Tribe Capital, Framework Ventures, Morgan Creek Digital, global reinsurer SiriusPoint, Exor, and Stratos. Post-seed valuation was approximately $100 million. In May 2024, an additional $7 million strategic round was raised, led by Electric Capital, with participation from Nexus Mutual and Avalanche Labs, bringing total funding to about $21 million.

Competitors in the Sector

Comparable projects in the same sector have different directions.

Nexus Mutual is the longest-standing protocol in the on-chain insurance field, but it covers crypto-native risks like DeFi smart contract vulnerabilities and hacker attacks, not involving real-world insurance contracts.

Neptune Mutual focuses on parametric insurance (automatic payouts based on predefined trigger conditions), with a TVL of about $13 million. Its scale is significantly different from Re's, mainly targeting DeFi protocol security scenarios, and has not entered the real-world insurance market.

Ensuro's positioning is closest to Re's—obtaining a regulatory license in Bermuda, partnering with Nexus Mutual to connect on-chain capital with real insurance risks—but publicly disclosed scale data is limited, and it has not yet gained visibility in the mainstream market.

The core differences from the above three are: Re covers insurance types like commercial auto and workers' compensation, which have extremely low correlation with the crypto market; the compliant structure of the licensed reinsurance entity Cover Re allows institutional funds to enter legally; and the $400 million in already underwritten premium volume makes it the only on-chain protocol in this sector that has reached a real commercial scale.