Author: Claude, TechFlow

TechFlow Summary: On June 22, SK Hynix's intraday market capitalization reached 208 trillion won, surpassing Samsung Electronics for the first time in 26 years. Hanwha Investment & Securities directly raised its target price from 1.63 million won to 4.3 million won, the highest among Korean brokerages. The core logic is that long-term supply agreements (LTA) and HBM demand have fundamentally changed the profitability volatility of memory chips. The stock has risen over 340% year-to-date, briefly surpassing 3 million won in pre-market trading but retreated over 5% in regular trading.

On June 22, SK Hynix's stock price hit a historic high of 2.95 million won, pushing its market cap to 208.1 trillion won, exceeding Samsung Electronics' 207.3 trillion won. This is the first time since November 2000 that Samsung has lost its top spot in the Korean stock market.

According to the Korea Herald, by 3:15 p.m., SK Hynix closed at 2.91 million won, up 5.32%, while Samsung Electronics fell slightly by 0.28% to 353,000 won. SK Hynix has surged 341.9% year-to-date, compared to Samsung's 197.7% gain. Both companies are in the semiconductor sector, but the market is voting with its feet: in the AI era, companies directly benefiting from infrastructure buildout are commanding a higher valuation premium than diversified giants.

Hanwha Investment & Securities Sets 4.3 Million Won Target Price, More Than Doubling Previous Estimate

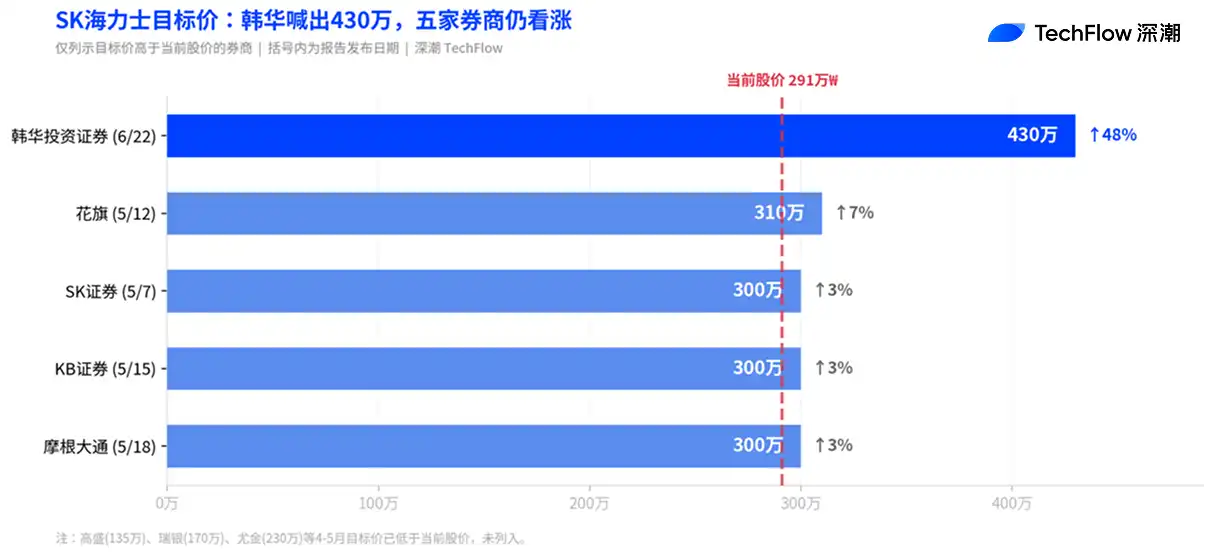

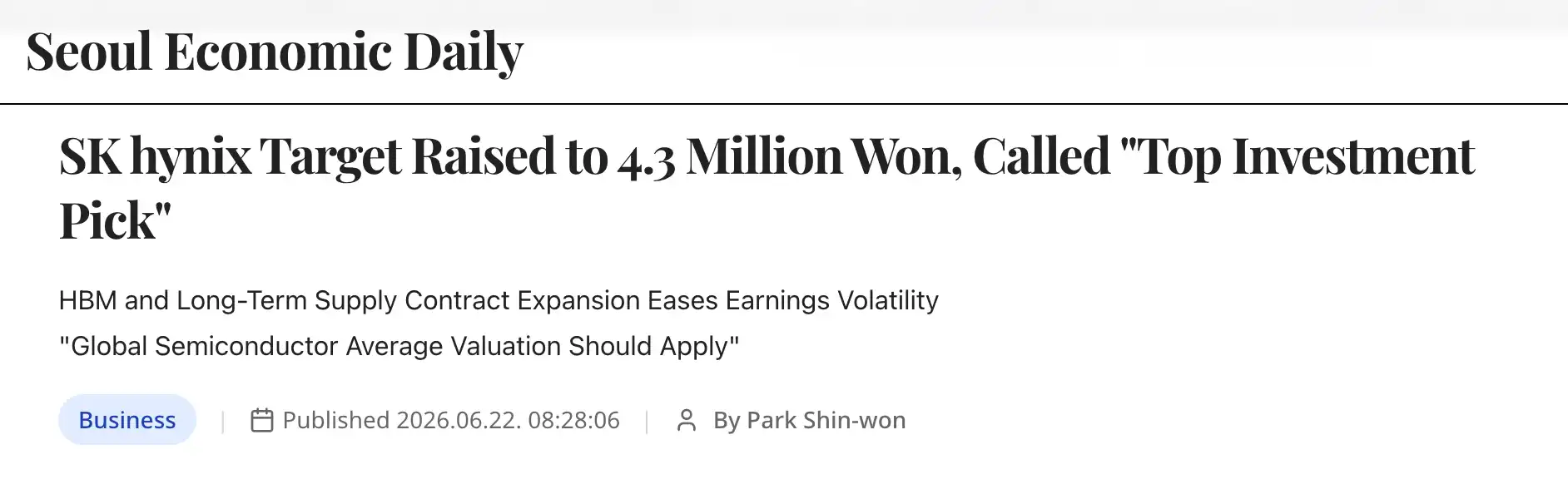

On June 22, Hanwha Investment & Securities analyst Park Jun-young raised SK Hynix's target price from 1.63 million won to 4.3 million won, an increase of nearly 1.6 times, currently the highest target price among Korean brokerages.

Park's core argument is: SK Hynix is no longer a company with severe profit volatility; it is transforming into an enterprise capable of consistently generating high-level profits. He noted that Korean memory chip makers have long suffered from valuation discounts, but with the expansion of long-term supply agreements (LTA) and soaring HBM demand, earnings visibility has fundamentally improved.

According to the Seoul Economic Daily, Hanwha used a price-to-earnings ratio (P/E) of 10x to calculate the target price, the lowest level among global semiconductor companies. SK Hynix's current 12-month forward P/E is about 6.6x, lower than that of fellow memory maker Micron. Hanwha predicts that even if the memory market weakens, SK Hynix's operating margin will remain above at least 30%, compared to figures that have fallen below 10% or even turned negative in past downturns.

Hanwha also listed ADR listing as a catalyst. Park Jun-young stated that an ADR listing within the year would give SK Hynix the opportunity to be valued directly against peers like Micron in the US market, saying "SK Hynix is currently the optimal investment target in terms of both fundamentals and momentum."

Multiple Brokerages Collectively Raise Target Prices, Memory Industry Valuation Framework Being Rewritten

Hanwha is not alone. In the past two months, Korean and international brokerages have seen a round of intensive upward revisions to SK Hynix's target price.

SK Securities raised its target price to 3 million won on May 7, using a 10x P/E framework, which was the highest among Korean brokerages at the time. KB Securities raised it to 3 million won on May 15, predicting a 2026 operating margin of 78.1%, stating that memory semiconductors are becoming "scarce strategic assets that determine the overall performance of AI systems." Citi raised its target price from 1.7 million won to 3.1 million won on May 12, citing stronger-than-expected HBM price growth in the second half. JPMorgan raised its target to 3 million won on May 18, simultaneously raising its EPS estimates for 2026-2028 by 9% to 20%.

Nomura Securities released a report on May 15, stating bluntly, "This time is really different," believing the valuation logic of the memory industry is undergoing a paradigm-level shift, and risk premiums should converge towards those of TSMC, rather than continuing to apply the traditional cyclical stock framework.

Behind these revisions is a common logical support: LTA has changed the pricing mechanism of the memory industry. According to Hanwha's analysis, current long-term supply agreements include price decline protection clauses and legal safeguards for contract performance, allowing manufacturers to maintain certain profit margins even during market downturns. This is fundamentally different from the past model where DRAM spot prices fluctuated wildly and manufacturers passively endured cycles.

Q1 Performance: Revenue First Surpasses 50 Trillion Won, Operating Margin at 72%

The target price hikes are supported by hard data. SK Hynix reported Q1 FY2026 revenue of 52.58 trillion won, a 198% year-on-year increase, breaking the 50 trillion won mark for the first time. Operating profit was 37.61 trillion won, a 405% increase. Operating margin reached 72%, surpassing Nvidia's 65% and setting a new record in the semiconductor manufacturing industry.

HBM is the core driver. SK Hynix currently holds about 70% to 80% of the global HBM market share and is a key supplier for Nvidia's AI accelerators. According to a Goldman Sachs report in April, the 2026 global DRAM supply-demand gap forecast has widened from 3.3% to 4.9%, the most severe in 15 years. The top three memory manufacturers have basically sold out their capacity for this year, and fab construction cycles of four to five years mean there will be virtually no new capacity added within the year.

UBS, when raising SK Hynix's earnings forecast in April, noted that AI-driven HBM demand continues to cannibalize DDR capacity, coupled with the server replacement cycle and simultaneous explosion in storage SSD demand, meaning the global DRAM supply-demand gap will persist until Q4 2027, calling it a "storage super cycle not seen in nearly three decades."

Pre-Market Surpasses 3 Million Won, But Falls Over 5% in Regular Trading

In pre-market trading on June 23, SK Hynix briefly touched 3.002 million won on Nextrade's NXT platform, breaking the 3 million won barrier. However, the stock price retreated after the regular session opened, trading at 2.75 million won as of 11 a.m., down 5.79% from the previous close.

The immediate cause of the decline was the overall weakness in global large-cap tech stocks, despite the solid performance of the US memory sector overnight (Micron up 6.9%, SanDisk up 4.1%). The KOSPI has risen 7.53% this month, but the gains have been highly concentrated in Samsung and Hynix stocks. The KOSPI 200 index excluding these two actually fell 2.48% over the same period, indicating extreme market divergence.

According to the Korea Herald, some brokerages have issued warnings: with Samsung Electronics' projected profit scale and growth rate both higher than SK Hynix's, the market cap reversal could be a signal of short-term overheating.

However, data from Mirae Asset Securities tracking high-return investors (top 1% in returns over the past month) shows that SK Hynix was still the most net-bought stock as of the morning of the 23rd. These investors see the pullback as a buying opportunity.