After fluctuating for over two months, Bitcoin is finally showing signs of a breakout.

Leading the charge for Bitcoin is once again the familiar face Michael Saylor, but this time he has a new weapon: STRC.

If you scroll through Saylor's recent tweets, you'll find him promoting STRC almost daily. AI-generated, low-quality promotional videos featuring tropical resort pools and women holding cocktails send a clear signal: the man who propelled MSTR to the pinnacle of Nasdaq is applying the same marketing firepower to STRC.

Why is he doing this? Because STRC is currently almost the only tool Strategy has to convert market money into BTC buying pressure. For the past three months, the funding source for every large-scale BTC acquisition announced by Strategy has pointed to STRC.

What is STRC

STRC stands for Variable Rate Series A Perpetual Stretch Preferred Stock, a type of perpetual preferred stock issued by Strategy that listed on Nasdaq last November.

Its operating mechanism is roughly as follows:

You spend about $100 to buy one share of STRC. Strategy pays a monthly cash dividend with an annualized yield of 11.5%, which is about 96 cents per share per month. It never matures, and Strategy does not need to repay the principal.

The share price is anchored near the $100 par value by adjusting the dividend rate monthly: if it falls below $100, the dividend rate is increased to attract buying interest; if it rises above $100, the dividend rate is decreased, allowing the price to fall back towards par. The maximum adjustment to the monthly dividend rate is 25 basis points.

Strategy can only issue new shares at par value to raise funds when the STRC share price is above $100—this is the premise of the entire flywheel. The proceeds from the issuance, after deducting the dividend reserve, are mostly used to purchase BTC.

Saylor calls this product "short-duration high-yield credit" or a "Bitcoin-backed money market fund." With current US Treasury yields around 3.5%, STRC offers a yield roughly three times that of Treasuries.

The Flywheel

A common misconception about Saylor is: he is printing unlimited money to buy BTC.

He can't. Saylor cannot create money out of thin air; he must wait for the market to hand it to him. Every additional share of STRC issued requires a real marginal buyer willing to pay $100 for it.

Buyers of STRC are essentially making a credit "trade." The extra 8% yield STRC provides compared to Treasuries is compensation for "Strategy's credit risk."

However, what many STRC buyers don't know is that the funds they use to purchase STRC will be indirectly magnified threefold before flowing into BTC.

Strategy has a public financial goal: a 33% leverage ratio.

Among the company's total funding sources, perpetual preferred shares like STRC, STRF, and STRK should make up about one-third, with the remaining two-thirds coming from MSTR common stock. Saylor calls this principle "intelligent leverage." This means that for every dollar Strategy raises through STRC, to maintain the 33% leverage line, they must issue approximately $2 worth of MSTR to be invested in BTC alongside it. $1 STRC + $2 MSTR = $3 BTC buying pressure.

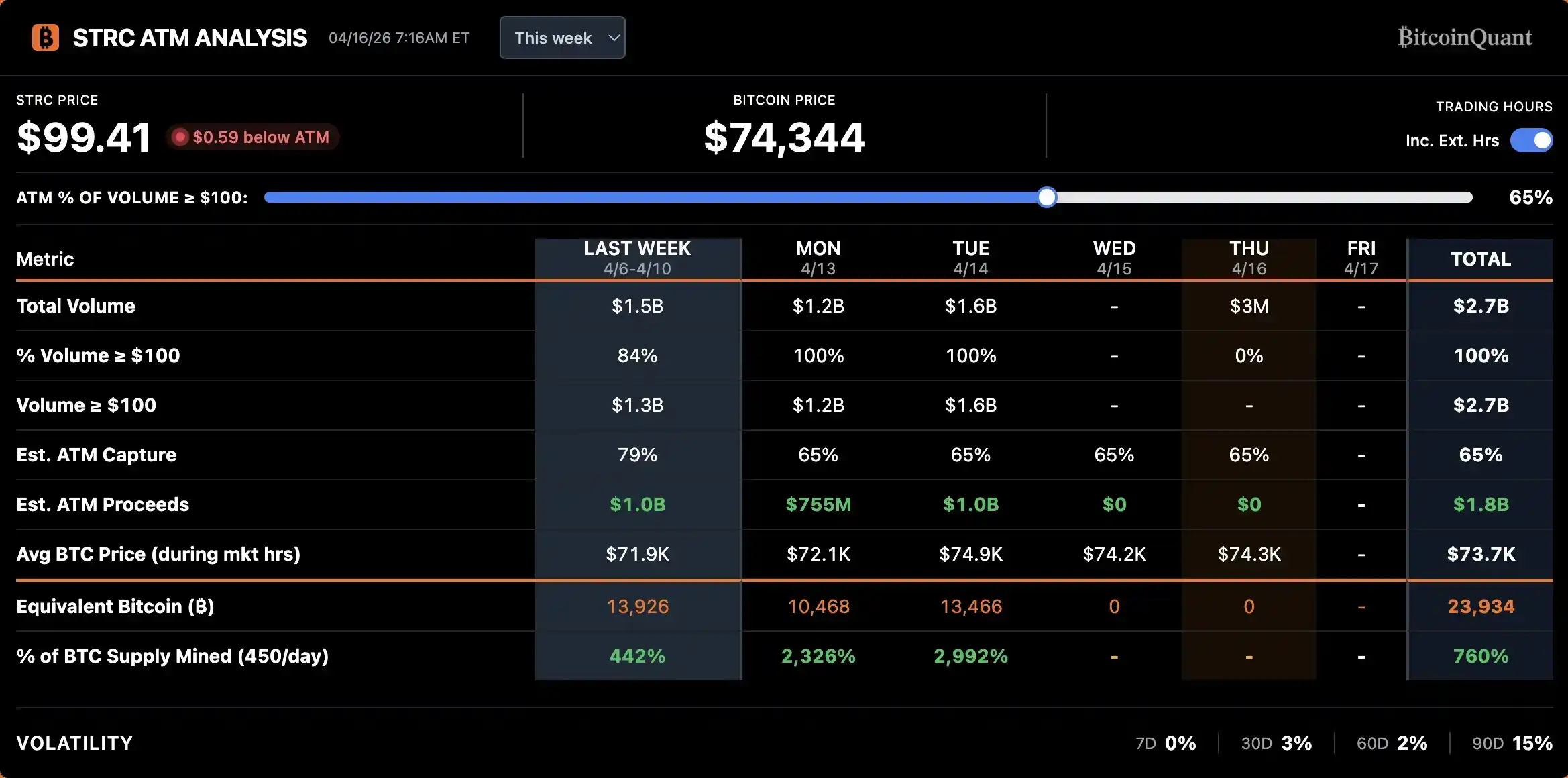

On April 14th, Strategy raised approximately $1 billion through STRC in a single day. With a 3x magnification, this corresponds to about $3 billion in BTC buying pressure, neatly matching the scale of BTC acquisitions in the first two weeks of April before the ex-dividend date.

When BTC falls, the collateral shrinks, STRC's credit risk increases, and Strategy must raise the dividend rate to compensate for the new risk level. But the higher the dividend rate, the greater the cash flow pressure and the higher the probability of default. This is an unstable feedback loop. During the period last October when BTC halved from $120,000 to $60,000, the STRC dividend rate was raised from 7% all the way to 11.5% to barely pull buying interest back.

Conversely, when BTC stabilizes and rises, the collateral thickens, credit quality improves, and STRC becomes more attractive at the same dividend rate, further amplifying demand. BlackRock's Preferred and Income Securities ETF listed Strategy's preferred stock as its second-largest holding in April, with its market value increasing from about $200 million in March to $344 million, a direct endorsement of Strategy's current credit status by fixed-income institutions.

Strategy's flywheel has turned positive: More funds buy STRC → Strategy buys BTC with 3x magnification → BTC price gets support → STRC collateral base becomes more solid, credit spread compresses → STRC becomes more attractive at the same dividend rate → More funds buy STRC.

Ex-Dividend Day Arbitrage

The dividend mechanism of preferred stock is different from bonds. Bonds accrue interest daily; you earn interest for each day you hold. Preferred stocks pay out in a lump sum on a fixed date. For STRC, as long as you hold the share at the close of the day before the ex-dividend date, you receive the full 96-cent monthly dividend.

This creates an obvious arbitrage window: buy in a few days before the ex-dividend date, collect the dividend, and sell the next day. Data from the past few months shows that STRC's average decline after the ex-dividend date is about 20 cents, far less than the 96-cent dividend itself. The net profit per share from a single ex-dividend arbitrage can reach about 40 to 50 cents.

Arbitrageurs won't miss this opportunity.

As shown in the chart, trading volume begins to climb about a week before the ex-dividend date, peaks on or the day before the ex-dividend date, and quickly subsides afterward. The surge in volume in April was significantly steeper than in March, indicating that more and more capital is participating in STRC's ex-dividend arbitrage.

However, such arbitrage behavior might not be a good thing.

For the STRC product itself, the two or three weeks after the ex-dividend date enter a "dead zone"—liquidity shrinks, bid-ask spreads widen, and the share price remains below the $100 par value for extended periods. This repeated de-anchoring erodes STRC's positioning as a "money market product," pushing it towards a form more akin to a monthly volatile bond.

For Saylor, his BTC purchases can easily be front-run by arbitrage capital. STRC issuances are concentrated in the two weeks before the ex-dividend date, meaning his BTC buying actions are also concentrated in those two weeks.

Now, traders engaging in arbitrage swarm in to buy STRC at the same time each month. They know Saylor is about to take this money to sweep the spot market for BTC, so they can buy BTC in advance and sell after Saylor pushes the price higher, thereby increasing Saylor's acquisition cost.

Significant increase in Coinbase spot premium around STRC's recent ex-dividend dates

There are two potential solutions: change the dividend frequency, for example from monthly to weekly, to spread out the arbitrage profits; or launch a more junior, more frequently paying derivative product to disperse the concentrated arbitrage trading.

Sure enough, Saylor acted quickly, announcing on Saturday that Strategy had filed a proxy statement proposing to change STRC's dividend payment frequency from monthly to semi-monthly. The annual dividend obligation and dividend rate would remain unchanged.

If the proposal is approved, the first semi-monthly dividend will be paid on July 15th.

Bitwise advisor Jeff Park pointed out that no corporate bonds currently use a semi-monthly dividend payment mechanism in the market, and retail investors' preference for higher frequency payments has been confirmed by the success of products like weekly dividend ETFs.

On a deeper level, Jeff Park sees this as a landmark step in the infiltration of the cryptocurrency industry's "streaming payments" vision into traditional capital markets: the frequency of interest payments essentially reflects the efficiency of converting monetary potential energy into kinetic energy. The digital currency era should naturally break the artificially set time cycle restrictions.

He believes STRC sets a new benchmark for traditional enterprises and is optimistic about the future evolution from semi-monthly, to daily, and even instant payments.

A New Narrative for DeFi

The emergence of STRC has brought a breath of fresh air to the bleak DeFi market.

Stablecoin yields in DeFi have been on a downward trend over the past year. Stablecoin deposit APY on Aave is around 2%, Ethena's USDe and Sky's USDS are both below 4%, and even PTs for mainstream stablecoins on Pendle struggle to break 6%. This level of return,对应 the risk exposure of smart contracts in the AI era, has deterred many DeFi veterans due to the risk-reward ratio.

DeFi needs a credible, sufficiently large source of yield to pull money from TradFi back on-chain, and STRC刚好 provides this opportunity.

Two projects are currently attempting to package STRC's yield onto the chain:

Apyx Protocol uses a dual-token model. apxUSD is the base stablecoin, over-collateralized by preferred stocks like STRC, SATA, and US Treasuries; apyUSD is the staked version, receiving the underlying dividend and interest income, currently with an APY of about 12.78%. The supply规模 has reached $130 million, and corresponding yield and leverage products are already available on Pendle and Morpho.

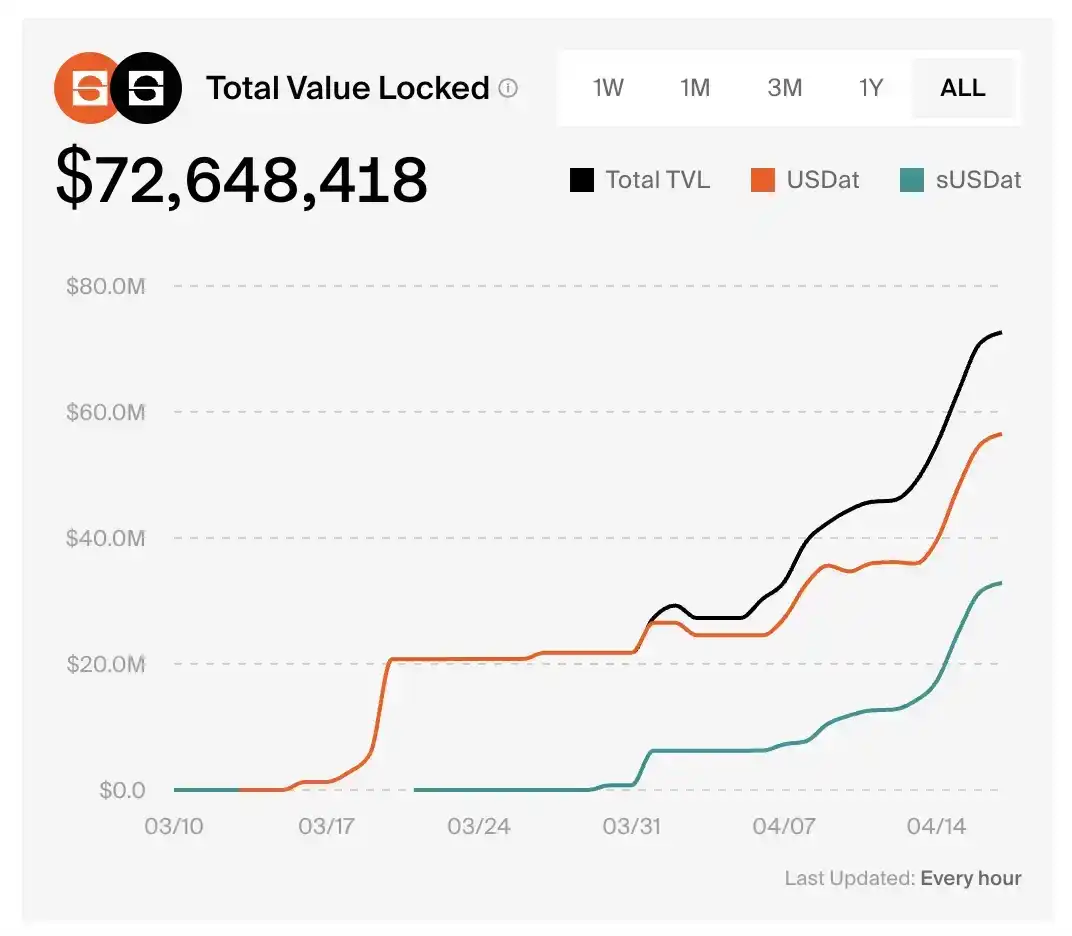

Saturn Credit's sUSDat is a staked, yield-bearing stablecoin that承接 STRC's yield. The protocol's TVL surged from zero to $72.6 million in just over a month.

According to Pendle market data, the current APY for PT-sUSDat is 9.2%.

Hoist with His Own Petard

The more successful Saylor's精心designed financial machine runs, the harder it becomes to avoid one question.

Strategy currently holds nearly 3.5% of the total BTC supply and continues to advance at a rate of billions of dollars per month.

What was BTC's original value proposition? A decentralized monetary asset that does not rely on any single entity and cannot be unilaterally manipulated by anyone.

When the perpetual preferred stock of a listed company becomes the primary marginal buyer for BTC—a decentralized, non-reliant-on-any-single-entity, cannot-be-unilaterally-manipulated monetary asset—is Bitcoin drifting away from its original form?