3月21日晚,Solana链上的元宇宙项目 NeoNexus 宣布因资金不足无法继续运行,项目创始人Jack Shi 将「资金不足」归结为SOL的下降和整个Solana NFT生态的低迷,并表示愿意将项目交给社区。

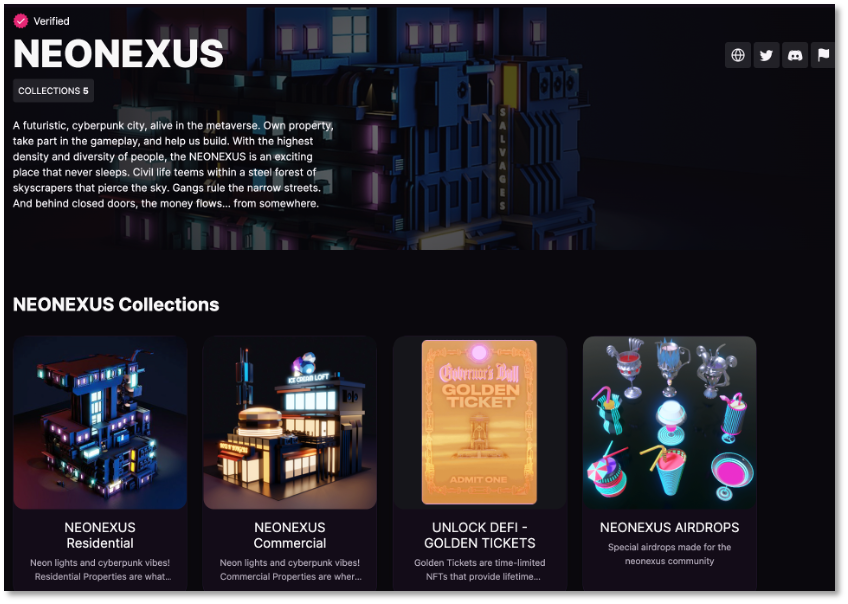

NeoNexus 属于以 NFT 驱动的链上虚拟空间项目,供用户铸造虚拟建筑。据粗略估算,该项目自去年9月起以 NFT 的方式筹集了25000 SOL,收入在300多万美元到600多万美元之间。

如今,NeoNexus 因「资金不足」停运的说法被社区成员质疑为「慢性地毯拉动」,有用户从去年年底就在 Discord 上吐槽该项目发展缓慢。质疑声四起之时,有人贴出了Jack Shi 在领英上的履历信息,甚至表示将发起诉讼。

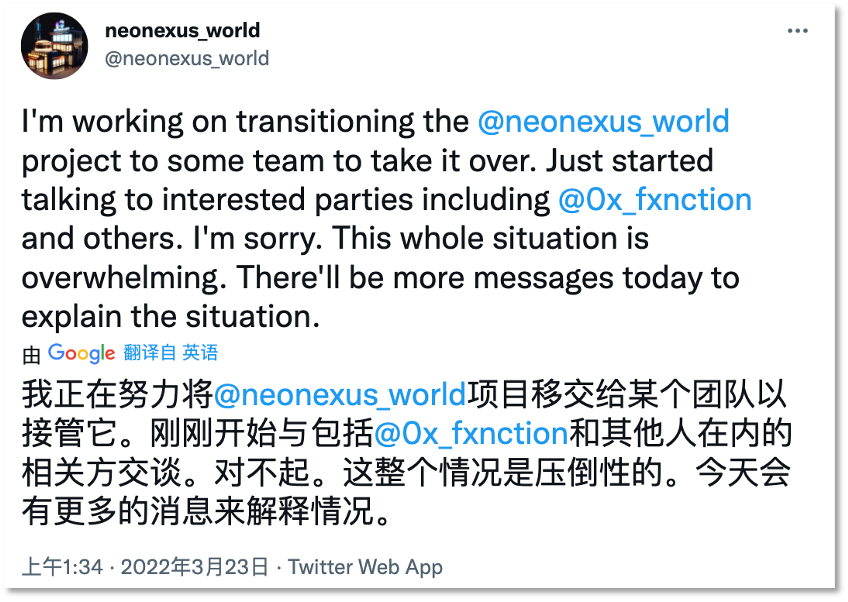

3月23日凌晨,Jack Shi更新推特称,正在努力过渡、将NeoNexus交给某个团队来接管,已开始与感兴趣的各方交谈。截至目前,NeoNexus官网仍处于无法访问的状态。

项目资金不足?创始人被曝与超跑合影

「我们不能再继续健康发展 NEONEXUS 项目了。」3月21日,NeoNexus项目的创始人Jack Shi在社区Discord上致信用户称,将在本月底解雇所有员工,愿意将项目移交给社区或社区选择一方接管。

Jack Shi 将 NeoNexus 难以为继的原因归结于SOL生态低迷造成了团队入不敷出。

他称,由于SOL价格下降很多,整个Solana NFT空间的活跃度、交易量和兴趣都在下降,想要在这样环境下发展和继续项目非常困难,他们的资金用于支付20多名员工的工资、开发和技术成本、法律费用、会计费用、债务和所有应缴的商业税,「我们不再有足够的资金来继续这个项目的发展。」

Jack Shi 没有披露项目到目前为止的收入。但根据NeoNexus官方信息显示,这个构建在Solana链上的NFT应用,从去年9月通过空投引流后,开始销售Golden Tickets(金票)、虚拟的住宅、商业楼等形态的NFT和财产代币,并筹集了以SOL结算的资金。

根据公开信息,NeoNexus已经铸造了4000个建筑类NFT,分别为2000个住宅属性的NFT 和2000个商区属性的NFT,还有6000个包括娱乐、工业、公共地产属性的NFT待开发。

Magic Eden上仍在列的Neo Nexus NFT系列

据估算,NeoNexus 通过铸造系列NFT筹集了大约 25000 SOL,在密集铸造的10月、11月,SOL 最高上涨至259美元,最低为137美元,以此计算,NeoNexus募资价值约在342.5万美元到647.5万美元之间。进入12月,SOL开始随加密资产市场的下行而下跌,目前徘徊在92美元附近。

尽管Jack Shi 说明了资金的用途,但并没有列出各项用途的具体支出,这导致用户无法相信 NeoNexus「资金不足」一说。而该项目进展缓慢的状况则被用户在Discord提及,有人在去年12月时就发现社区活跃度下降,担心自己铸造的房子NFT 凉凉;另有人在今年1月时询问项目是否还在继续运营,社区管理员提示他跟进「住宅画廊」的公告。

3月15日,NeoNexus 还在预告娱乐建筑NFT的铸造,6天后,该项目创始人突然宣布因「资金不足」停运,项目的官网也已经无法打开。

Jack Shi「资金不足」的说法被一些用户指责为「慢性的地毯拉动」、「软跑路」。而3月22日,以抨击NFT欺诈而闻名的推特网友zachxbt 贴出Jack Shi于去年11月与兰博基尼跑车的合影,以此追问项目到底是以什么方式耗尽了资金。

针对 NeoNexus 的质疑声就这样在加密社区KOL的晒图推动下达到了高潮。

创始人信息遭曝光 项目更新接管动态

NeoNexus 创始人用一封信就将项目甩给了社区,但他并未详细规划项目该如何由社区接管,他也未与用户在Discord社群中探讨相关细节。

NeoNexus 官网停止访问后,其已经上线二级市场的住宅NFT和商区建筑NFT均有所下跌。Solana NFT数据网站SolsWatch显示,3月22日, NeoNexus住宅NFT 的地板价最低为0.6 SOL,而前一日为2.75 SOL;NeoNexus 商区 NFT的地板价跌到了0.64 SOL,前一日为2.45 SOL。

在Jack Shi被晒出与超级跑车的合影后,他在领英上的职业履历也被网友扒出。他于2012年毕业于哥伦比亚大学计算机和数学专业,曾在加拿大皇家银行资本市场实习,并在这家公司担任过商品技术分析师和场外清算技术分析师;2016年4月起,他在道明证券美国公司担任高级开发人员;2021年8月,他创建了Unlock DeFi公司,并开始了第一个 NFT 项目 NeoNexus。

大多数情况下,区块链上创建的项目往往由匿名团队运营,人们大概也比较意外,Jack Shi 居然是 NeoNexus 的实名创始人。也因如此,项目因资金原因难以为继的消息出现后,有用户表示将搜集团队信息和相关证据,对该项目发起诉讼。

3月23日凌晨,Jack Shi 和 NeoNexus 的推特均发布了新动态称,正在努力将项目移交给某个团队接管,已经开始与相关方交谈,今日将继续更新消息来解释情况。

NeoNexus更新接管动态

这一信息更新后,NeoNexus 的住宅和商区建筑NFT的价格有所回升,均达到了1 SOL以上。尽管该项目的官网仍处于无法访问中,但从Jack Shi的表达看,NeoNexus 可能会迎来新的转机。

截至目前,上线了NeoNexus NFT的二级市场平台均未下架该NFT,鉴于Magic Eden存在专门针对NFT欺诈制定的防范程序,NeoNexus 至少在这个程序下还未被判定为违规。

尽管 NeoNexus 情况未明,但发生在NFT市场的「地毯式拉动」并不少见,它常指一种退出骗局,即匿名的开发商突然离开项目并带着投资者的钱跑路。

此前,在Magic Eden上线的NFT项目King of Chess就从投资者那里卷跑了645 SOL,当时价值58000美元;而另一个项目Balloonsville 造成的损失更大,骗取了投资者 5000 SOL,当时价值近60 万美元。

在Magic Eden上出现的跑路项目不仅让该平台付出了向买家退款的代价,也损害了该平台的声誉。

今年2月,Magic Eden制定了新的安全程序,要求在平台发布NFT产品并募资的创作者进行KYC证明,每个项目在上架前都要签署合作协议,团队负责人私下向平台递交协议后才再公开上架作品。此外,项目需将其资金在平台上托管至少24小时,或选择将托管期延长14天,以证明项目的真实性。该平台试图以此防范「地毯式拉动」骗局。

「匿名」或许是加密社区的原教旨主义体现,但对于用户来说,匿名项目往往存在跑路风险,如何「去信任化」也是区块链的要义,将此理念通过技术落实于应用本身或许还需要很长的路要走。