Автор:Gino Matos

Компиляция:Chopper, Foresight News

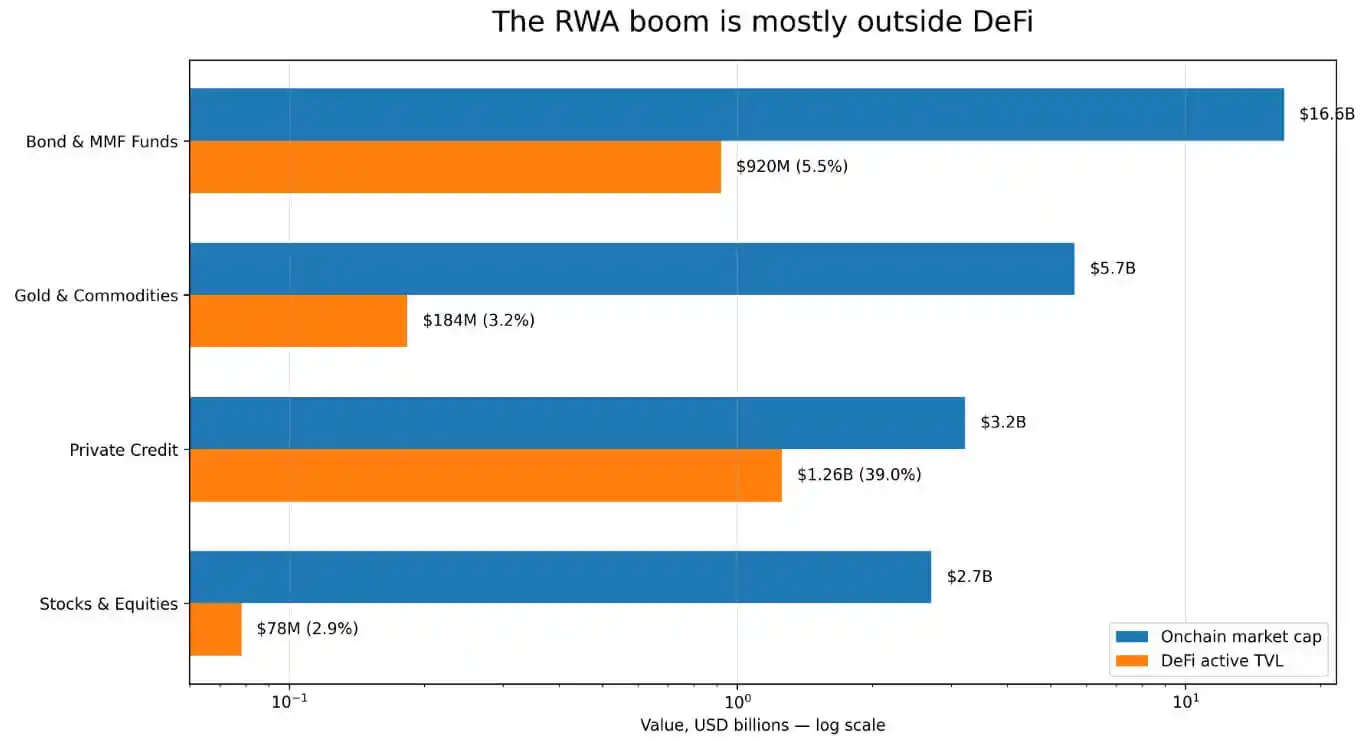

Согласно данным DeFiLlama, текущий масштаб токенизированных реальных активов (RWA) на блокчейне приближается к 300 миллиардам долларов, но из них лишь 24,7 миллиарда долларов отображаются как активная заблокированная стоимость (TVL) в DeFi, то есть реальный объём средств, внесённых в пулы ликвидности сторонних платформ DeFi и участвующих в функционировании экосистемы.

Подавляющее большинство остальных активов RWA находятся вне таких сценариев, как рынки кредитования и хранилища залога, которые позволяют осуществлять свободное комбинирование и взаимодействие криптоактивов. Облигации и фонды денежного рынка являются крупнейшей категорией RWA, общий объём на блокчейне превышает 166 миллиардов долларов, но эффективный объём заблокированных средств, поступивших в экосистему DeFi, составляет лишь 9,2 миллиарда долларов. Объём золота и товарных активов на блокчейне достигает 57 миллиардов долларов, а эффективный объём обращения в DeFi — всего 1,836 миллиарда долларов; объём акций и долевых активов на блокчейне — 27 миллиардов долларов, а средства, поступившие на рынок DeFi, и вовсе составляют лишь 78,27 миллиона долларов.

Ярко выделяется только сегмент частного кредитования: объём на блокчейне — 32,26 миллиарда долларов, эффективный заблокированный объём в DeFi — 12,57 миллиарда долларов, уровень проникновения в экосистему достигает 39%. Причина в том, что такие проекты, как Maple Finance и Centrifuge, изначально были спроектированы как кредитные финансовые инструменты, что естественным образом соответствует сценариям применения DeFi.

В то время как такие токенизированные продукты, как фонды казначейских облигаций США, золотые активы и акции, на этапе разработки эмитентами в большей степени ориентированы на потребности институциональных держателей, и их общая архитектура соответствует традиционной модели работы регулируемых фондов.

Распределение рыночной капитализации на блокчейне и активной TVL DeFi по четырём категориям RWA

Архитектура с разрешительным доступом становится главным барьером для компоновки в DeFi

DeFiLlama относит продукт фонда денежного рынка BUIDL компании BlackRock к категории фондов с разрешительным доступом, эффективный заблокированный объём этого продукта в экосистеме DeFi составляет всего 18,9 миллиона долларов.

Международная организация комиссий по ценным бумагам (IOSCO) в своём итоговом отчёте по токенизации финансовых активов за ноябрь 2025 года указала, что BUIDL создала на публичном блокчейне разрешительную систему для выпуска, кастодиального обслуживания, вторичных сделок между квалифицированными инвесторами, распределения дивидендов и выкупа.

Потенциальные инвесторы должны пройти проверку белого списка через платформу Securitize, и перевод активов на блокчейне приобретает полную юридическую силу только после подтверждения и сверки информации офлайн-регистратором.

Это также означает, что BUIDL по сути является инфраструктурой для хранения активов, построенной на базе блокчейн-канала, основная цель которой — обслуживать потребности институционального кастодиального хранения активов и офлайн-учёта. Его смарт-контракты поддерживают взаимодействие только с адресами из белого списка, и без использования промежуточного уровня, такого как регулируемая обёртка, их нельзя напрямую внести в открытые протоколы DeFi без порога входа, такие как Aave и Uniswap.

В феврале 2026 года BlackRock завершила интеграцию BUIDL с экосистемой Uniswap, позволив части активов поступать в торговые пулы. Однако права доступа к активам по-прежнему контролируются Securitize, и участие разрешено только квалифицированным инвестиционным институтам с чистыми активами не менее 5 миллионов долларов, обычные участники рынка по-прежнему не имеют к ним доступа.

IOSCO обнаружила, что подавляющее большинство токенизированных фондов денежного рынка на рынке в настоящее время используют аналогичные модели работы, и эти активы до сих пор не оправдали ожиданий отрасли относительно высокой ликвидности на вторичном рынке.

В отчёте по индустрии токенизации, опубликованном RedStone в марте 2026 года, прямо говорится, что самой сложной частью внедрения токенизации активов является координация сложного набора правил в различных юрисдикциях и экосистемах публичных блокчейнов, включая соответствие нормативным требованиям, верификацию личности, ограничения торговых прав, проверку санкционного контроля и распределение корпоративных прав. На нынешнем рынке Morpho и Aave Horizon являются одними из немногих реальных примеров успешного внедрения активов RWA в DeFi.

Проще говоря, каждое ограничение соответствия, установленное разработчиками проекта, ещё больше повышает порог для подключения активов к экосистеме DeFi. А такие продукты, как токены казначейских облигаций США и фонды денежного рынка, сами по себе разработаны с наложением различных ограничений доступа, чтобы соответствовать регуляторным требованиям лицензированных институциональных инвесторов.

С золотыми и товарными активами существует ещё одна практическая проблема. Согласно данным CoinGecko, в первом квартале 2026 года объём спотовых сделок с токенизированным золотом составил 90,7 миллиарда долларов, что уже превысило общий объём за 2025 год, но подавляющее большинство сделок с этими активами происходит на централизованных биржах. Упомянутый ранее эффективный заблокированный объём в DeFi в размере 1,836 миллиарда долларов представляет собой лишь очень небольшую часть объёма, обращающегося внутри экосистемы, огромный объём торгов на централизованном рынке полностью не учитывается в статистике DeFiLlama.

Оптимистичные ожидания: высокоадаптированные продукты уже показали образец

В начале 2026 года заблокированный объём USDY от Ondo превысил 10 миллиардов долларов, и теперь он охватывает все девять экосистем публичных блокчейнов. Запущенный в сентябре 2025 года раздел Ondo Global Markets, ориентированный на токенизированные акции и ETF-активы для иностранных инвесторов, изначально поддерживает свободный перевод активов и их прямое использование в качестве залога в DeFi. В настоящее время заблокированный объём соответствующих активов составляет 6,5 миллиарда долларов, а совокупный объём сделок превысил 120 миллиардов долларов.

Согласно статистике RedStone, объём депозитов в активах RWA на платформе Morpho превышает 620 миллионов долларов, а общий объём соответствующих активов в Aave Horizon составляет 423,5 миллиона долларов. Оба кредитных протокола успешно внедрили зрелую модель кредитования под залог RWA.

Эти примеры внедрения наглядно доказывают: если на этапе выпуска активов придерживаться концепции дизайна, предполагающей свободное обращение без ограничений доступа, активы RWA полностью могут реализовать свойство компоновки в экосистеме DeFi.

На отраслевой круглом столе, организованном DWF Labs в апреле 2026 года, совместно с такими проектами, как Centrifuge, Falcon Finance и xStocks, была выдвинута идея: в настоящее время сектор RWA уже разделился на два основных направления развития. Во-первых, приоритет отдаётся соответствию требованиям к праву собственности на активы, идёт по пути строгого разрешительного контроля. Во-вторых, соблюдение стандартов регулируемого выпуска сочетается с обеспечением ликвидности на вторичном рынке, а в основе дизайна лежит возможность компоновки в экосистеме.

Руководитель проекта Centrifuge Грэм Нельсон заявил, что жёсткий механизм доступа по белому списку означает, что каждый участник пула ликвидности должен проходить индивидуальную проверку квалификации, что напрямую блокирует путь активам в открытую DeFi.

А решение DeRWA, предложенное Centrifuge, путём обёртки базовых активов первичного выпуска в соответствии с регуляторными требованиями и одновременного ослабления ограничений на обращение активов на вторичном рынке, преодолевает этот барьер. Артём Толкачёв из Falcon Finance также отметил, что возможность компоновки в экосистеме и гибкий механизм выхода являются ключевым мостом, соединяющим реальные активы с ликвидностью крипторынка.

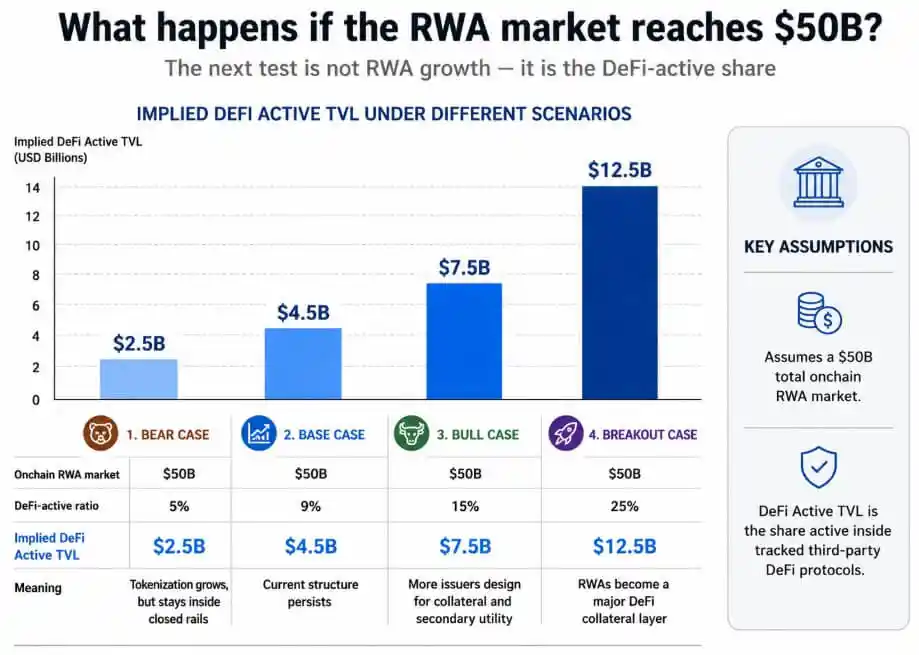

В отрасли оптимистично полагают, что по мере приближения общего объёма активов RWA на блокчейне к 500 миллиардам долларов, если большинство проектов в секторе перейдут на подход к дизайну, совместимый с DeFi, уровень проникновения активов RWA в экосистему DeFi сможет преодолеть нынешний низкий уровень в 9%.

Пессимистичная реальность: рост отрасли может быть ограничен традиционной финансовой системой

Standard Chartered прогнозирует, что к 2028 году глобальный масштаб токенизированных активов достигнет 2 триллионов долларов, но одновременно предупреждает: этот отраслевой бум, скорее всего, будет ограничен внутренней сферой традиционной банковской и финансовой системы, а открытый крипторынок сможет получить весьма ограниченную долю выгод от роста.

Исследование IOSCO в ноябре 2025 года также подтвердило это. Из-за собственных ограничений технологии распределённого реестра по доступу и ликвидности, распространение, распределение и вторичные сделки с токенизированными активами на данном этапе по-прежнему в высокой степени зависят от традиционной финансовой инфраструктуры.

Европейский центральный банк в своём исследовательском отчёте по индустрии токенизации, опубликованном в апреле 2026 года, далее указал, что в мире ещё не сформированы единые отраслевые стандарты токенизации активов, что легко может привести к созданию изолированных "островков" активов. Разные системы активов имеют свои собственные правила соответствия, базовые уровни расчётов и механизмы доступа, что в конечном итоге приводит к высокой концентрации ликвидности внутри закрытых кругов, затрудняя её взаимное движение и обмен.

Уровень проникновения облигаций и фондов денежного рынка в DeFi составляет лишь 5,5%, золота и товарных активов — 3,2%, акций и долевых активов — 2,9%; эти данные наглядно подтверждают такую фрагментированную структуру экосистемы.

Подавляющее большинство продуктов на рынке, таких как токены казначейских облигаций США и фонды денежного рынка, обычно устанавливают минимальный порог инвестирования, обязательную проверку личности, офлайн-циклы сверки активов, а также фиксированные периоды выкупа, привязанные к чистой стоимости активов. Такие базовые правила изначально конфликтуют с логикой работы децентрализованных бирж с реальным ценообразованием и хранилищ залога без порога входа. И эти ограничительные условия являются жёсткими требованиями регулирующих органов, а также неизбежным выбором эмитентов активов для адаптации к регулируемой среде.

Два рынка, одна отраслевая метка

Общий объём RWA на блокчейне в 300 миллиардов долларов и эффективный объём обращения в DeFi в 24,7 миллиарда долларов, хотя и относятся к одному сектору RWA, фактически соответствуют двум полностью разделённым рынкам:

- Регулируемый блокчейн-финансовый рынок: в основном включает фонды денежного рынка, фонды казначейских облигаций США, активы под институциональное кастодиальное хранение. Обращение активов зависит от офлайн-сверки и подтверждения прав регистраторами, полностью следуя правилам регулирования традиционных финансов.

- Рынок экосистемы DeFi с возможностью компоновки: активы могут свободно вноситься в кредитные протоколы, использоваться в качестве залога без порога входа, подключаться к различным автоматизированным стратегиям получения дохода и свободно обращаться.

На графике прогнозируются значения активной TVL DeFi в четырёх сценариях на рынке RWA в 500 миллиардов долларов, в диапазоне от 5% до 25%.

Объём депозитов RWA в Morpho, превышающий 620 миллионов долларов, и достижение USDY по обращению в 9 блокчейнах достаточно доказывают, что второй тип рынка обладает реальным потенциалом развития.

Чтобы уровень проникновения активов RWA в DeFi превысил 9%, эмитенты активов должны отказаться от таких подходов к дизайну, как «ядро — регулируемая система» в BUIDL от BlackRock, и перейти на базовую архитектуру, изначально поддерживающую свободное обращение без порога входа.

В настоящее время 285,6 миллиарда долларов активов RWA на блокчейне относятся к направлению разрешительного контроля, что также означает, что нынешние токенизированные реальные активы в целом больше склоняются к регулируемым традиционным финансовым продуктам на блокчейне, а не к универсальным залоговым активам, адаптированным для открытой экосистемы DeFi.