Tom Lee进入第三季度时对以太坊的坚定信念,现在看来像是一次时机精准的操作。

就背景而言,BitMine Immersion最近又增持了42,197枚ETH,使其持有量超过574万枚ETH。

另一方面,Michael Saylor的MicroStrategy出售了3,588枚BTC,随着第三季度的展开,这为关于ETH与BTC作为国库储备资产的争论增添了一抹有趣的色彩。

值得注意的是,这场争论不仅仅在社交媒体上上演。

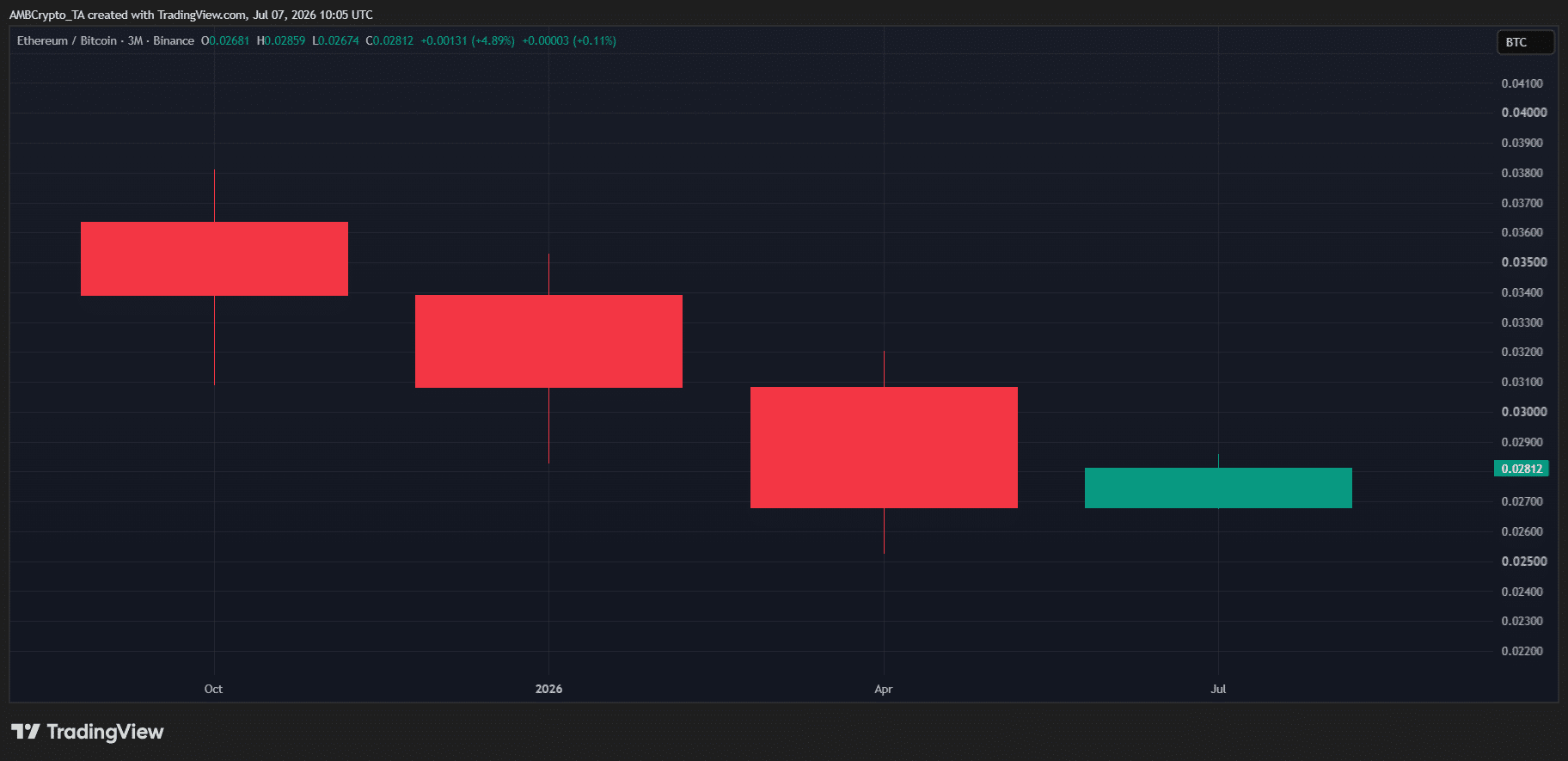

如下图所示,ETH/BTC比率在经历了连续三个季度的下跌后,于第三季度开局上涨近5%。这表明ETH相对于BTC正开始重新获得强势,支持了Tom Lee继续积累以太坊的决定。

然而,Tom Lee的信念并非仅仅基于期望。

BitMine最近在X上发帖称,《清晰度法案》通过几率上升是其不断增加ETH头寸的主要原因。

据该公司称,预测市场目前认为《清晰度法案》通过的概率约为50%,为两周来最高水平。BitMine认为,随着智能合约平台更深入地融入日常金融,监管的明确性将成为以太坊的一个重要催化剂。

因此,从BitMine的角度来看,近期ETH/BTC比率的上升只是反映了市场对《清晰度法案》成为法律的更高预期。

自然,现在更大的问题是,这种重新定价是否还有进一步的空间。ETH能否在整个第三季度继续跑赢BTC,还是BitMine看涨以太坊 [ETH] 的观点已经领先于基本面?

随着比特币重拾势头,以太坊能否保持领先?

BitMine对ETH的增持是基于以太坊长期的去中心化金融故事。

但链上数据显示,这一叙事尚未完全兑现。

根据DeFiLlama的数据,以太坊的DeFi活动仍远低于之前的高点。总锁仓价值(TVL)仍低于400亿美元,而去年十月回调前大约在890-900亿美元。

与此同时,以太坊在第三季度开始时,其稳定币供应量较6月底的约1,600亿美元减少了超过50亿美元。

换句话说,市场在以太坊链上基本面尚未跟上的情况下,就已经在对《清晰度法案》进行定价。

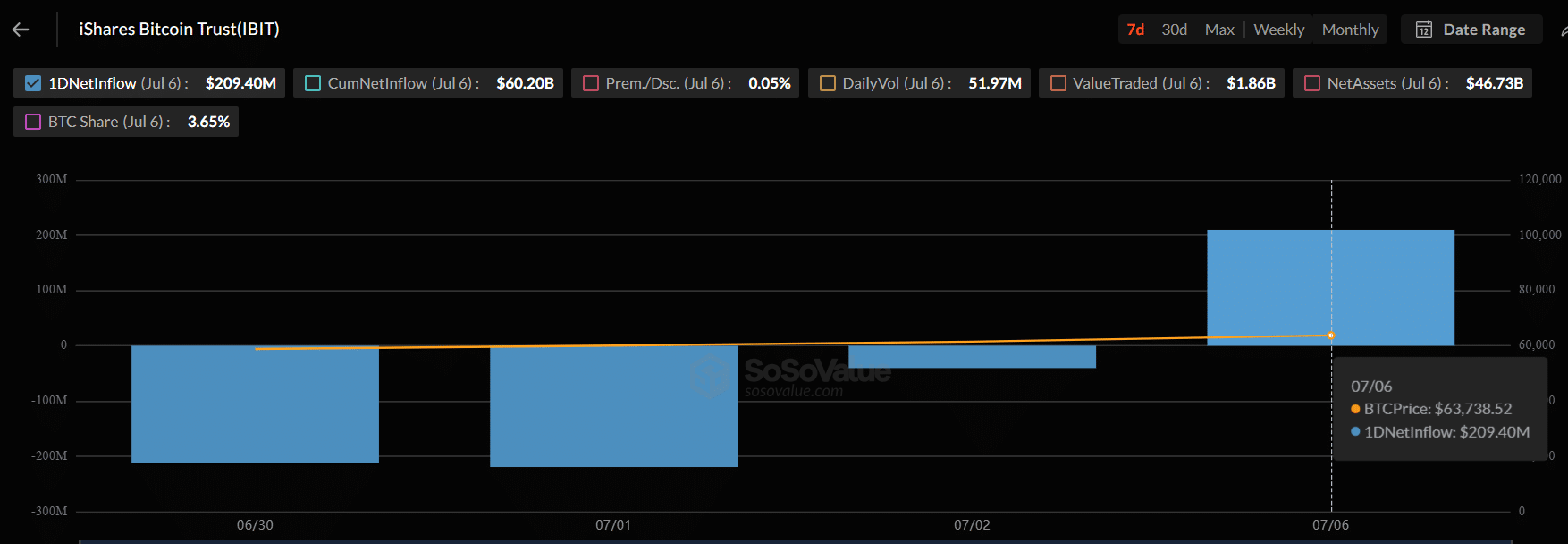

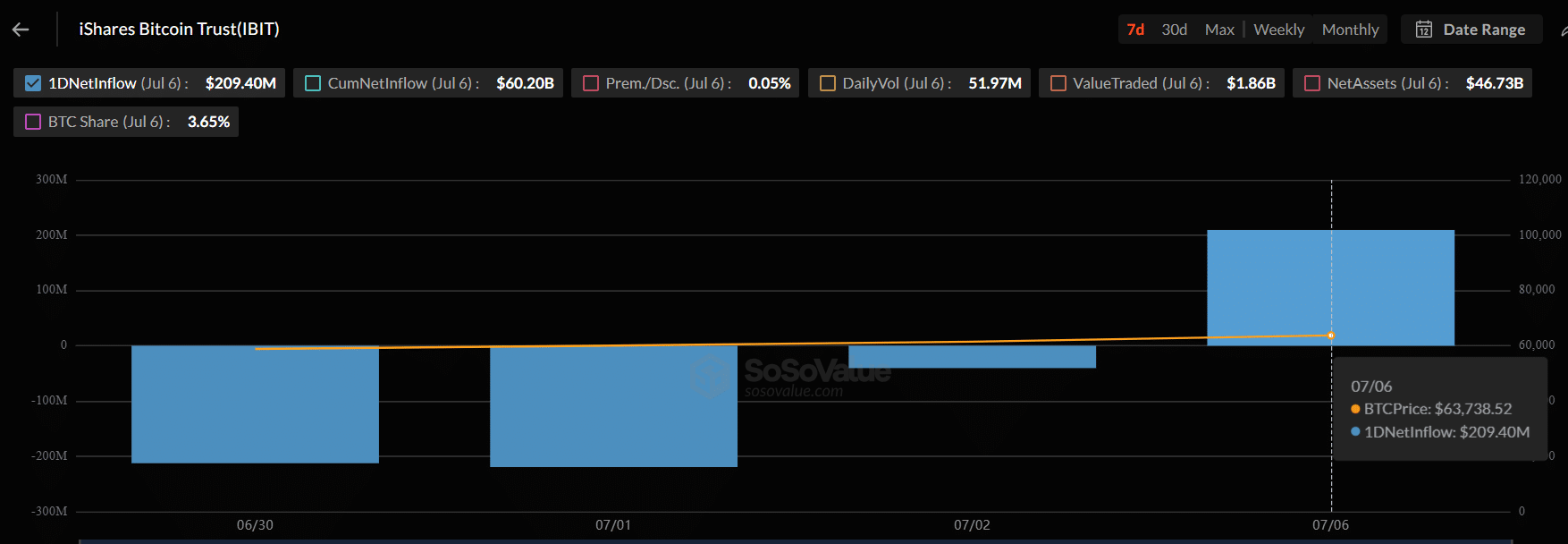

更添挑战的是,贝莱德已恢复购买比特币,在连续11天净流出后,录得超过2.09亿美元的净流入。此举表明在ETH链上基本面仍然滞后的情况下,市场对比特币的信心有所恢复。

在此背景下,Tom Lee的ETH观点显得越来越雄心勃勃。

尽管MicroStrategy出售了BTC,比特币仍维持在约64,000美元附近,这表明贝莱德的买入足以吸收这些抛售供应。这使得ETH与BTC作为国库储备的争论势均力敌——以太坊有政策乐观情绪支撑,而比特币则继续受益于强劲的机构需求。

因此,天平仍然倾向于比特币一方。

ETH/BTC因《清晰度法案》的"预期"而上涨,但以太坊的链上活动并未跟上。与此同时,比特币正迎来新的机构资金流入。除非以太坊的DeFi指标开始复苏,否则维持ETH/BTC在第三季度初的势头可能会很困难。

最终总结

- ETH/BTC因《清晰度法案》的乐观预期而上涨,但以太坊的DeFi活动尚未跟上。

- 贝莱德正在重新购买BTC,这为比特币提供了更强的支撑,使得ETH/BTC在第三季度继续保持超额表现更加困难。