撰文:Tanay Ved

编译:AididiaoJP,Foresight News

关键要点:

-

Tether 仍然是全球稳定币的领导者,在新兴市场锚定美元获取渠道,并通过其储备推动市场对美国国债的需求。

-

随着新法规和竞争动态重塑稳定币市场,并在合规性和收益分配方面出现差异化,USDT 的主导地位正在下降。

-

以太坊和波场在 USDT 活动中的角色正在演变,波场在高频、低成本的支付领域保持领先地位,而以太坊费用的下降和流动性的增强推动了更广泛的零售和结算应用。

-

新兴通道带来了新的增长机遇,USDT0 和专注于稳定币的网络(如 Plasma)正在将 Tether 的分布扩展到更多网络和用例(如支付)。

引言

Tether 的 USDT 无疑是当今全球稳定币的领导者,占据着约 3000 亿美元市场中约 60% 的份额。USDT 曾经主要是一种交易工具,如今其意义已超越加密货币市场,成为新兴经济体获取美元的关键渠道,并对美国本土市场具有日益增长的地缘政治重要性。与此同时 Tether 已成为该行业盈利能力最强的公司之一,季度利润达数十亿美元,并正在进行一场 200 亿美元的融资,这可能使其成为全球最有价值的私营公司之一。

然而监管和日益激烈的竞争重塑稳定币格局,Tether 的下一篇章取决于它能否维持其网络效应并延伸其长期的主导地位。基于我们最近对 GENIUS 法案后稳定币领域动态的观察,我们审视了 Tether 的市场地位,因为它平衡着主导性的现在与竞争日益激烈的未来。我们探讨了 USDT 的市场份额如何演变,其活动在不同区块链上有何不同,以及新兴通道将如何塑造其在稳定币下一阶段增长中的作用。

Tether 的市场地位与重要性

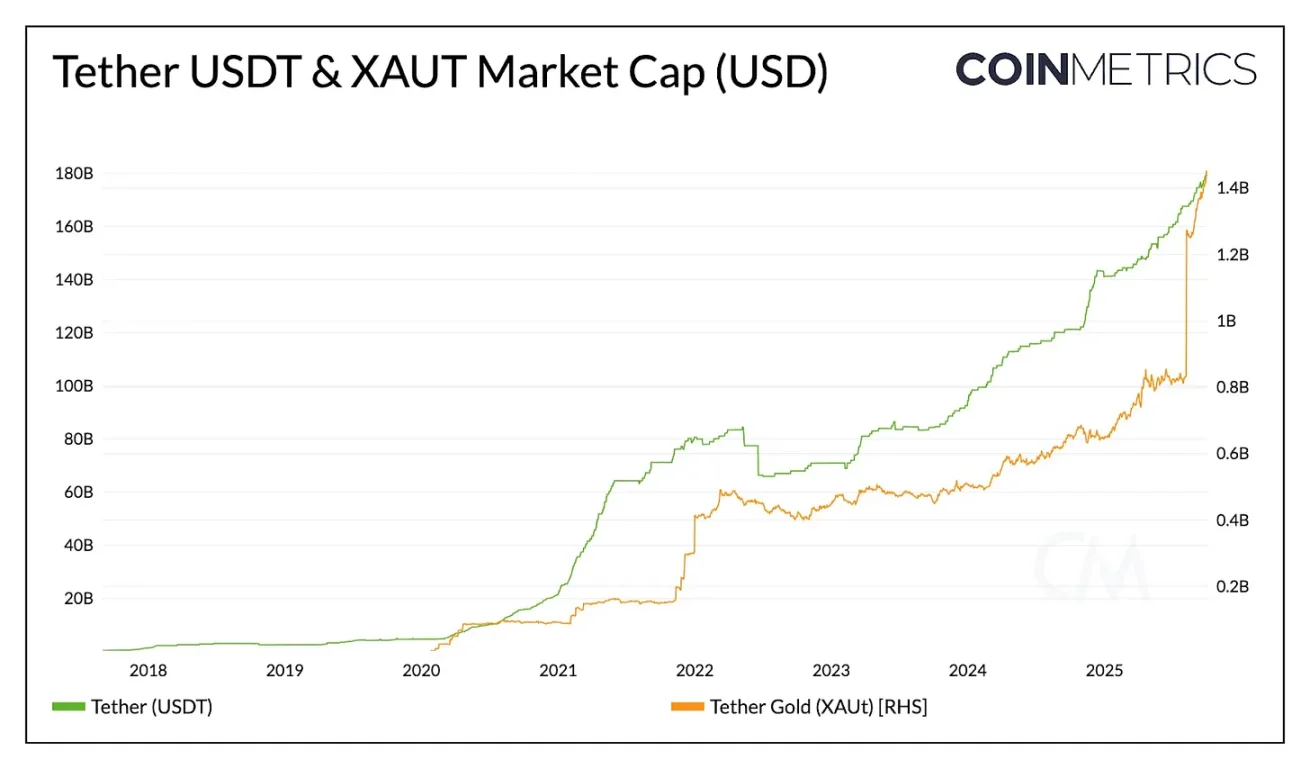

Tether 的 USDT 流通量为 1780 亿美元,是规模最大的稳定币,优势明显(约比 Circle 的 USDC 大 2.4 倍,比所有其他稳定币的总和大约 3.6 倍)。其规模和流动性使其成为保护储蓄、提供经济稳定性和促进交易的重要工具,特别是在银行基础设施有限的地区或本地货币通胀率超过 5% 的国家。

资料来源:Coin Metrics Network Data Pro

除了美元,Tether 还通过 XAUt 提供代币化黄金敞口,随着对替代性价值存储需求上升,其市值已增长至超过 14 亿美元。Tether 似乎正在扩展这一双重战略,与 Antalpha Platform 寻求一场 2 亿美元的融资,用于设立一个将收购 Tether 的 XAUt 代币的数字资产国库。随着进一步投资于比特币和黄金开采,Tether 正朝着融合不同形式的价值保存方式迈进。

市场份额与增长压力

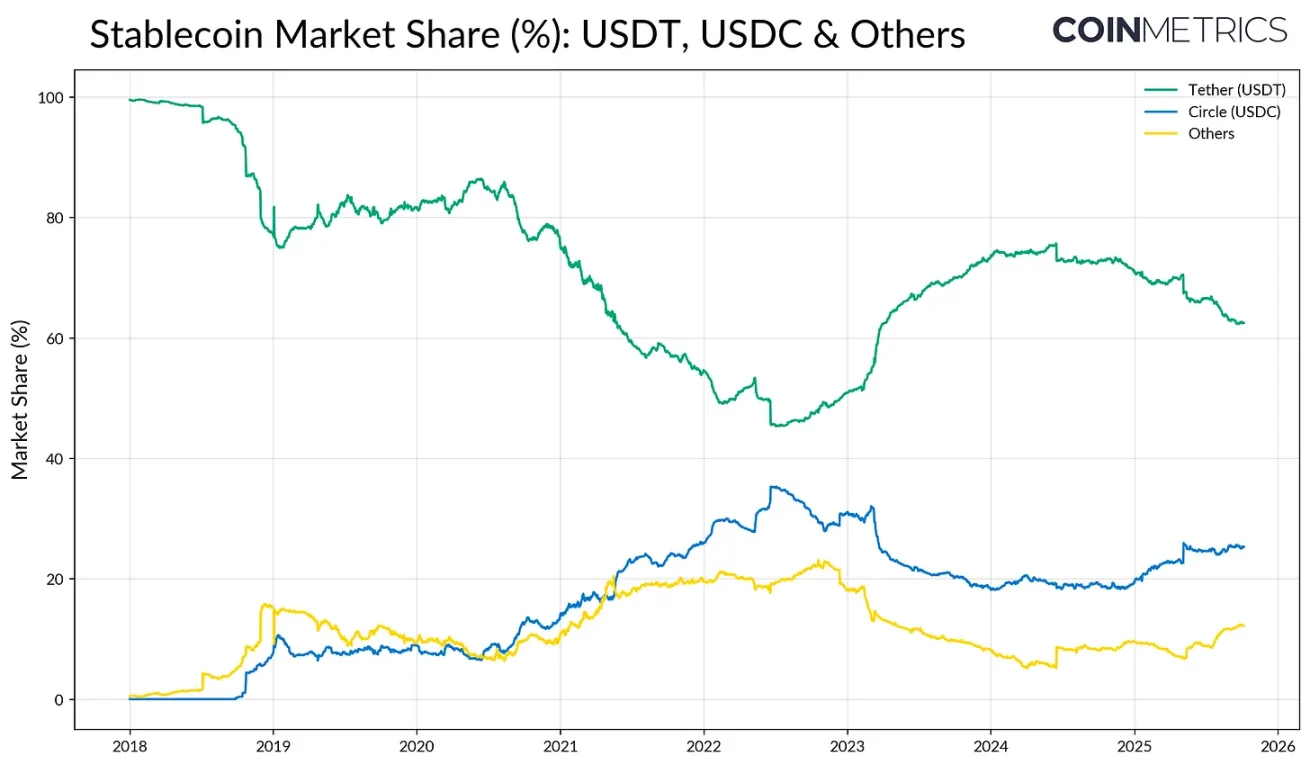

USDT 的先发优势和在交易所的深度流动性赋予了其强大的"网络效应"。在该行业早期阶段,USDT 的市场份额曾超过 80%,此后 USDC 和 BUSD 的崛起使其主导地位降至接近 50%。2023 年硅谷银行(SVB)的崩溃迅速逆转了这一趋势,资本逃离了竞争发行方。然而自 2024 年以来,并且随着 2025 年 GENIUS 法案的临近通过,USDT 的份额再次显示出受压的迹象。

资料来源:Coin Metrics Network Data Pro

Circle 的 USDC 在境内监管势头的推动下逐渐重拾根基,而"其他"稳定币,主要是生息替代品,如 Ethena 的 USDe、Sky 的 USDS 和代币化货币市场基金,正在赢得市场份额。市场目前似乎处于转型期,USDT 在流动性和采用率方面继续领先,但面临着来自进入市场的现有支付网络和分配收益的替代品的日益激烈的竞争。

盈利能力与合规之路

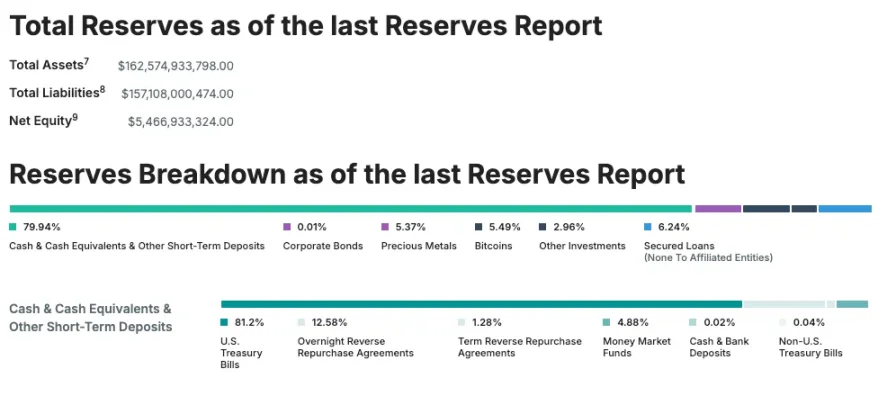

尽管竞争日益激烈,Tether 仍是最赚钱的稳定币发行方,在 2025 年第二季度实现净利润 49 亿美元。这得益于其 1270 亿美元的美国国债储备,使其成为全球最大的美国政府债务持有者之一。然而 Tether 一直是一家总部设在萨尔瓦多的离岸发行方,其部分储备包括不合规资产,如贵金属、比特币和担保贷款。为解决这个问题,Tether 计划推出 USAT,一种在美国设立、完全合规的稳定币,以加强其境内增长战略及其在美国债务需求中的作用。

资料来源:Tether Transparency(截至 6 月 30 日鉴证报告)

USDT 如何在不同区块链间流动

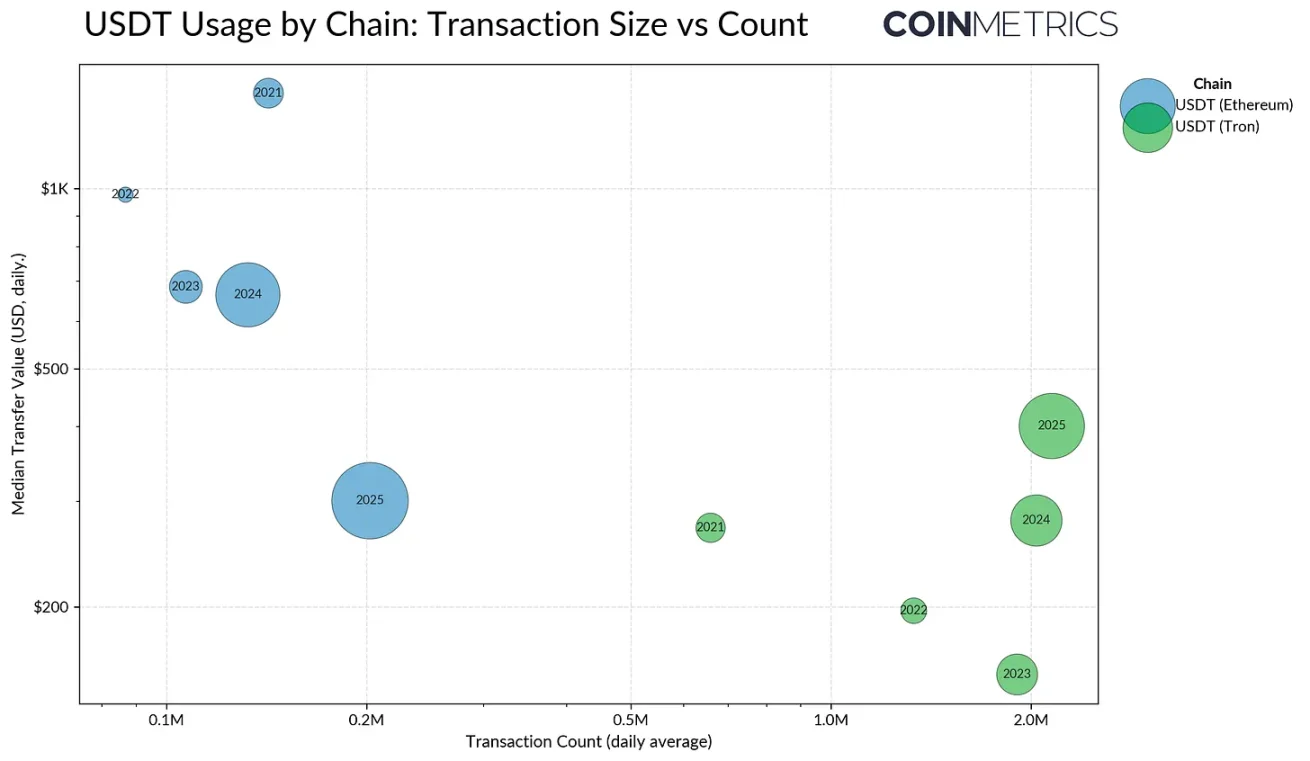

在确立了 Tether 作为发行方的市场地位后,了解 USDT 如何在不同区块链间流动、支撑其转移和结算的通道至关重要。USDT 的流通方式由每个网络的能力所塑造,并影响着在每个链上占主导地位的活动类型和用户群体。USDT 的使用反映了不同的活动类型,绝大部分发行集中在以太坊和波场上。

波场历史上一直是新兴市场用户的主要接入点,因其低费用和快速结算而受到青睐。2025 年波场平均每日交易量超过 230 万笔,对于 USDT 转账来说似乎是一个用户粘性很高的网络,支持着一个持续、高速的小额、类支付流量的活动。这种模式与其在零售和汇款支付中的使用相一致,在这些领域,成本效益和可访问性最为重要。

资料来源:Coin Metrics Network Data Pro

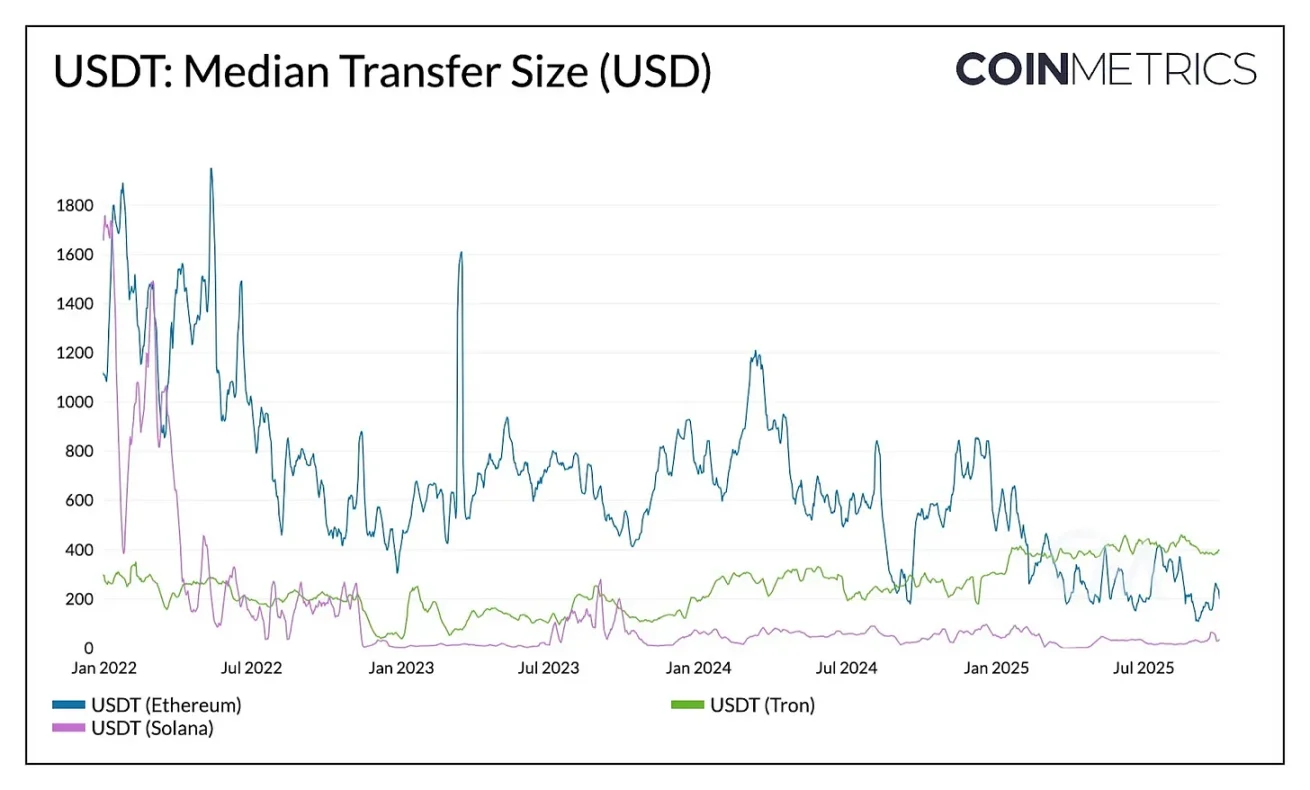

相比之下,以太坊传统上承载着更大价值、更低频率的转账,反映了其作为 DeFi 和机构活动的结算和流动性中心的作用。然而这种动态正在发生变化。

在 Dencun 和 Pectra 升级之后,以太坊的平均交易费用已降至 1 美元以下,使得小额转账的频率得以提高。以太坊上的中位转账金额从 2023 年的超过 1000 美元下降到 2025 年中的约 240 美元,而波场的中位金额则有所上升。这种动态使以太坊更接近于曾经波场独有的活动类型。

资料来源:Coin Metrics Network Data Pro

这种行为转变也与供应量的重新分布同时发生。2025 年 8 月,以太坊上的 USDT 供应量(960 亿美元)超过了波场上的供应量(780 亿美元),显示出较低的费用和更深的流动性正在将活动吸引回以太坊。

资料来源:Coin Metrics Network Data Pro(以太坊上的 USDT,波场上的 USDT)

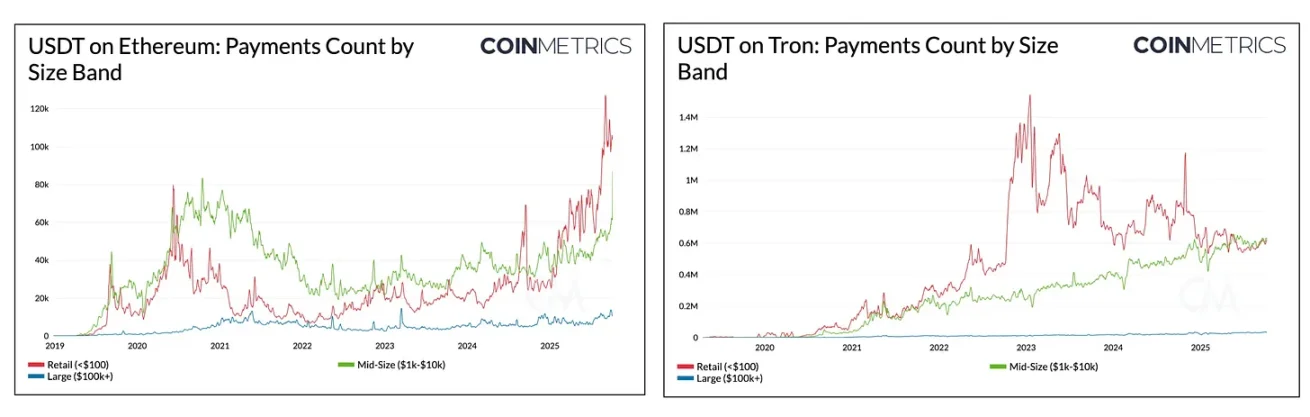

这一趋势在跨区块链的 USDT 支付构成中也显而易见。在波场上随着中等规模流量的势头增强,零售支付和中型转账之间的差距已经缩小。在以太坊上自 2024 年以来,零售(<100 美元)和中型(1 千 -1 万美元)支付的数量急剧增长,而大额(10 万 -100 万美元)转账保持稳定。这表明,随着网络变得更加易于访问,USDT 的使用正朝着小规模活动多样化。

通过新兴通道扩展 USDT 的主导地位

USDT 在波场和以太坊等链上的演变突显了结算速度、成本和流动性如何塑造用户行为。展望未来,Tether 正通过新的分发渠道和结算层战略性地扩展其覆盖范围。

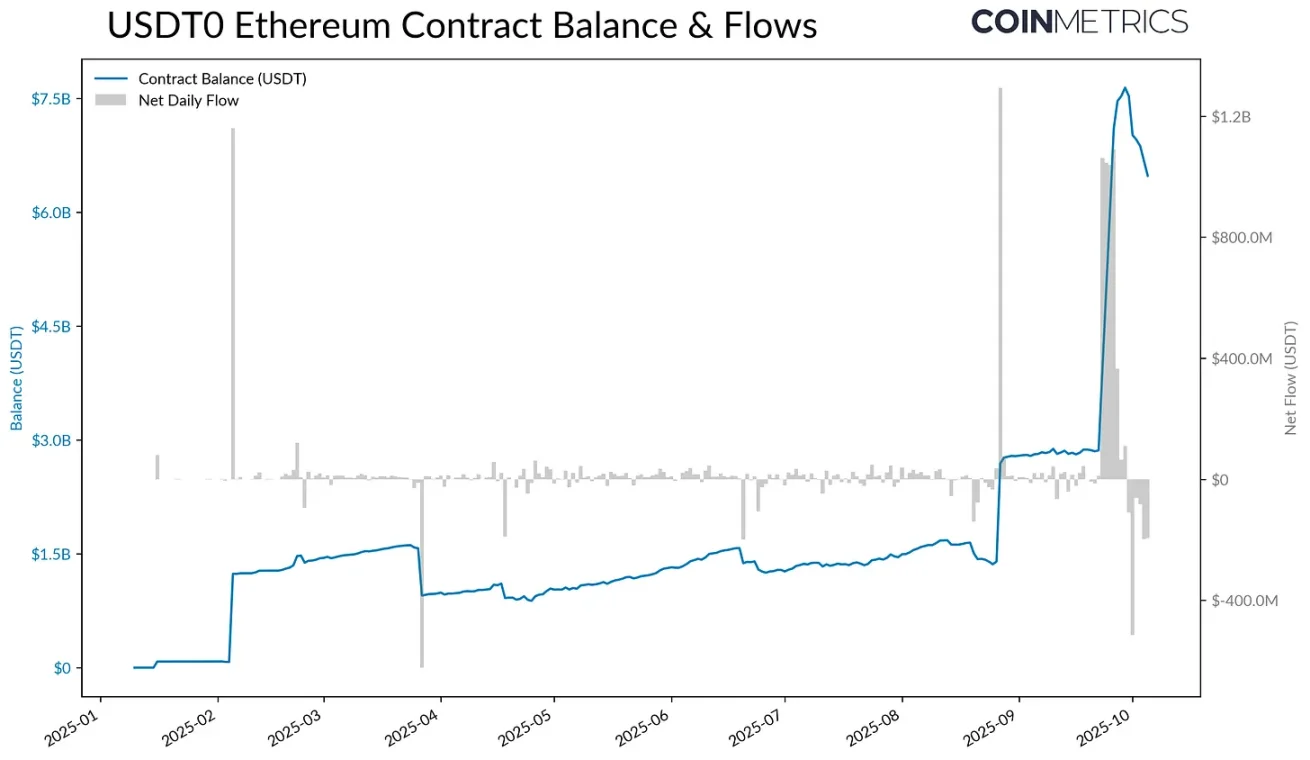

例如,基于 LayerZero 的全链同质化代币(OFT)标准推出的 USDT0,通过在以太坊上锁定 USDT 并在目标链上铸造等额代币,实现了无缝的跨链转移,并保持 1:1 的背书。

资料来源:Coin Metrics ATLAS

在 9 月 25 日推出 Plasma(一个为稳定币优化的 Layer-1 区块链)之后,锁定在 USDT0 以太坊合约中的 USDT 供应量从 28 亿美元激增至 77 亿美元。凭借零费用的 USDT 转账、稳定币作为燃料费以及高吞吐量设计,Plasma 迅速吸引了超过 60 亿美元的 USDT0 供应量,目前稳定在约 42 亿美元。

虽然其长期可持续性将取决于支付和储蓄用例的采用,但 Plasma 代表了一类新的 USDT 互补通道,类似于今天波场和以太坊服务于不同活动的方式。USDT0 和 Plasma 共同说明了 Tether 如何将其分发扩展到更广泛的网络集合,这些网络可以支持从高价值结算到支付、DeFi 和零售活动等各种需求。

结论

随着稳定币成为全球支付基础设施,Tether 的下一篇章将在竞争加剧和监管日益明晰的背景下展开。其维持主导地位的能力将取决于能否从一个离岸发行方演变为一个多链、合规的基础设施提供商,同时又不削弱其在流动性和分发方面的核心优势。全链 USDT 和专注于稳定币的网络(如 Plasma)的出现,预示着结算和支付更加多样化的未来。Tether 是扩展其网络效应,还是在竞争对手面前失去阵地,最终将定义该行业下一阶段的演变。