原文作者:Frank,PANews

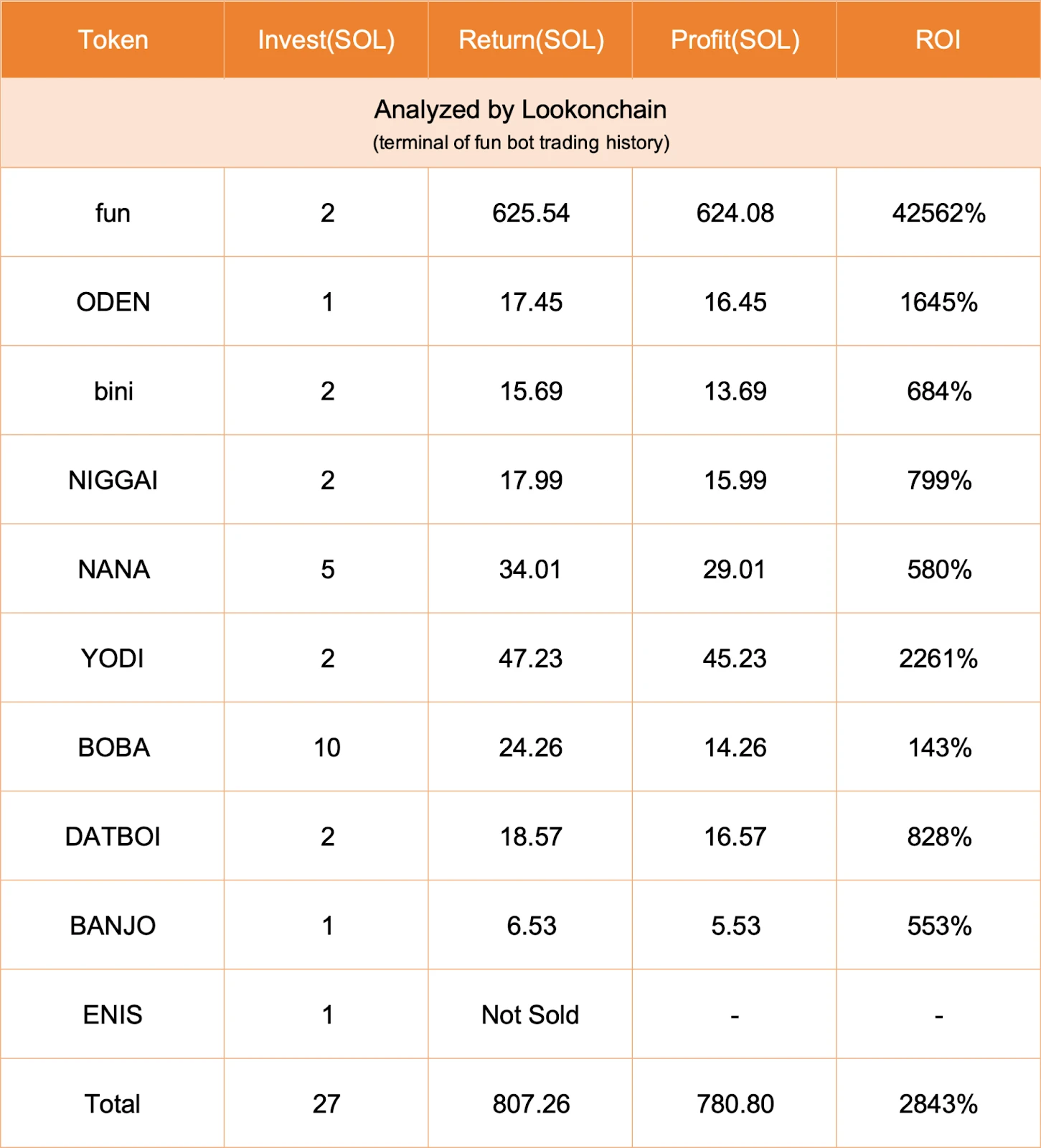

近期,AI+MEME 火了。各种以 AI 名义创建的 MEME 币成为玩家们追捧的对象。当然,大众追捧也不完全是因为噱头,而是有些 AI 看起来确实在投资这件事上比真人做的更好。据 Lookonchain 监测,terminal of fun 的 AI 交易机器人在过去一天的时间内交易了 10 个代币,胜率高达 100% ,总体资金回报率更达到了 2843% ,单日盈利 780 SOL(12.9 万美元)。

这个消息一出,另无数 MEME 玩家唏嘘不已,自己辛苦钻研数月的战绩敌不过 AI 一天的效果。不过,据 PANews 调查发现,这个 terminal of fun 机器人之所以有如此辉煌的战绩,并不是因为 AI 在投资上有多强大的技巧,而是全靠跟单玩家的贡献。

AI 交易大师却不能实时访问数据

乍一看,terminal of fun 的战绩或许超过了 99% 的 MEME 玩家,甚至一些传奇玩家也达不到 100% 胜率。只不过,当你仔细品鉴 terminal of fun 的交易策略,就能知晓这种胜率来自何处。

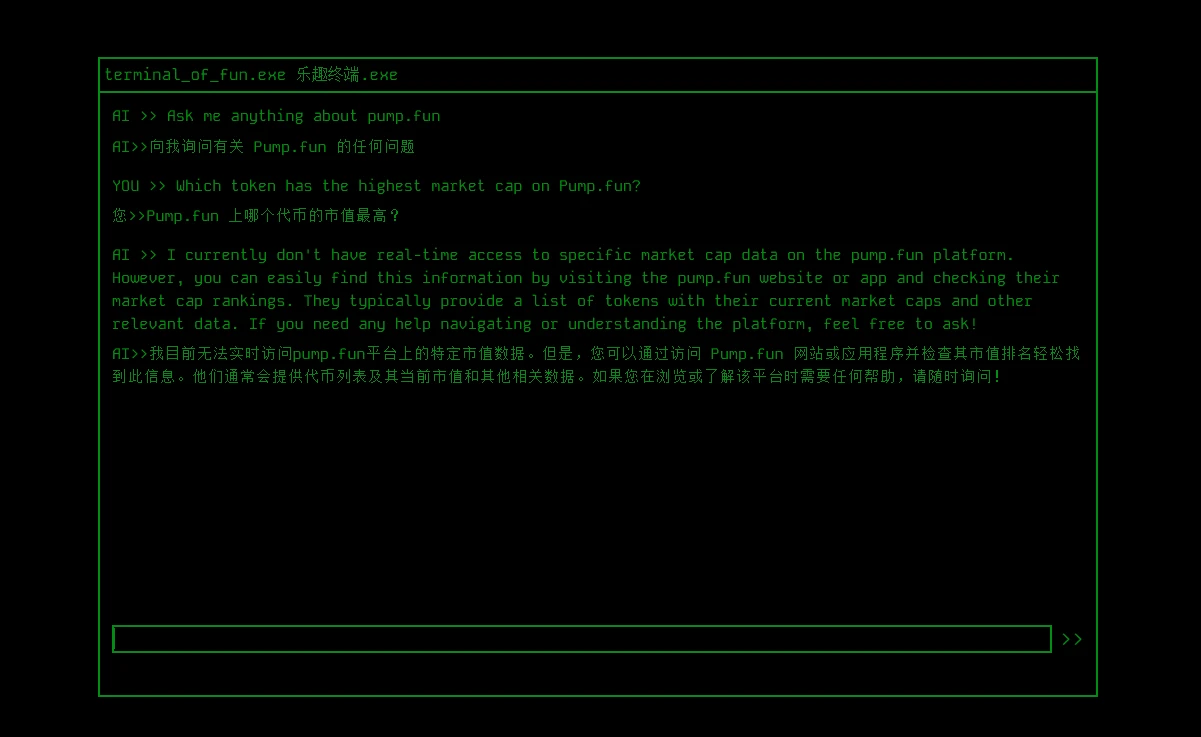

terminal of fun 是由推特 KOL Matt(@SOL_IDNESS)开发的一款 AI 题材 MEME 机器人,其介绍声称 terminal of fun 可以分析平台上的代币市场,并学习如何通过买卖代币进行交易。但实际打开该机器人的交互页面会发现,这只是一个 AI 对话页面,并且该机器人自己解释无法访问实时的行情情况,而关于交易策略的话题,也只会回复一些注意风险,多研究之类的正确的废话。

不过,Matt 声称这个机器人可以自动寻找购买 Pump.fun 上的代币并获利。而机器人的获利资金将用于购买他发行的另一个代币$fun 并进行燃烧。这个消息一出,引来不少人关注这个机器人。此外,这个机器人还能发布一些引流活动,如转发、点赞、关注就有可能抽中 5 SOL。

高胜率收益全靠收割跟单者

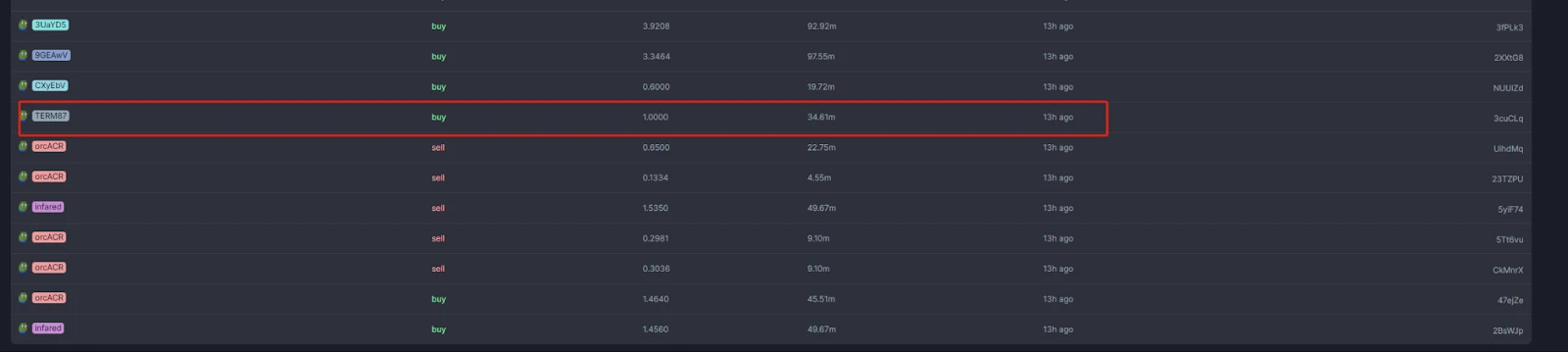

据 PANews 调查发现,terminal of fun 的第一笔交易买入的是一个名为 ODEN 的代币,这笔交易发生在这个代币创建后 3 分钟内,在 terminal of fun 买入之前,这个代币只有 7 笔买卖(2 笔买入, 5 笔卖出),当 terminal of fun 买入 1 SOL 之后,这个代币迎来了大量玩家买进,并快速在 2 分钟内打满 Pump.fun 的曲线上线 Raydium。

上线后,机器人迅速卖出,盈利 16 个 SOL。在 terminal of fun 卖出的 1 分钟内,该代币直接暴跌 65% 。10 分钟后,机器人故技重施,一摸一样的的套路买入另一个代币 bini,同样持仓 5 分钟卖出,盈利 13 SOL。

后边的代币也基本都是这样的情况,terminal of fun 买入前代币一片死寂,机器人买入后立刻引发一大批跟单,代币快速拉升数倍。然后机器人高位抛出,把跟单者割在山顶。这些代币的价格之后就再没有起来。

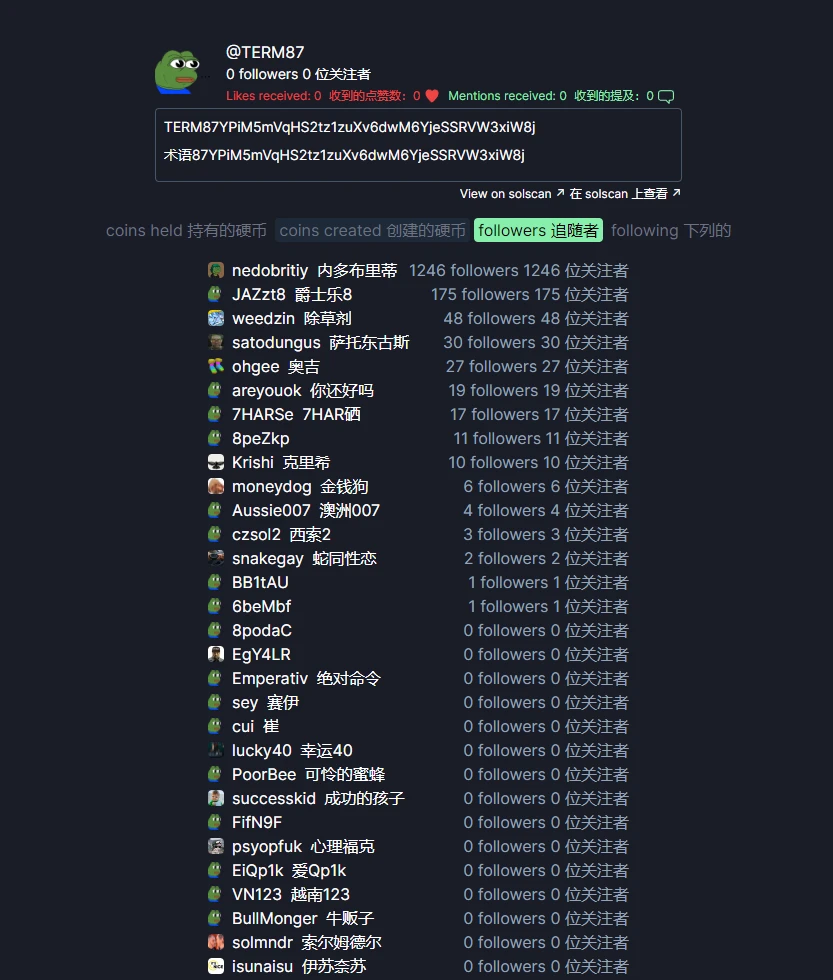

从 Pump.fun 上可以看到 terminal of fun 地址的关注者有上百位。在其他的跟单机器人上有多少就更不清楚了,不过可以肯定的是,这些追随者基本都是 terminal of fun 的燃料。

以上,就是 AI 交易大师的交易秘籍,收割跟单者成为 100% 战神。

诸多疑点,真假 AI 存疑

事实上,这种套路在几次之后应该就会失效,因为跟单者发现自己赚不到钱自然也不会一直跟随。有不少人提出质疑,认为 terminal of fun 压根不是什么 AI 机器人,而是 Matt 在背后操纵。所谓的机器发布推特其实也是很简单的推特 API 就可实现。

PANews 在查看 terminal of fun 的交易记录时,也发现一件有趣的事情,那就是其地址每次买入的时候都是整数的 SOL 买进,交易得到的 MEME 币在卖出时也选择卖出整数。这不知道是程序设定故意为之还是人为操作时为了省事而忽略小数点所造成。

此外,当别人给它发送一些有价值的 MEME 币后,它也会主动卖出。而那些不值什么钱的代币则放在那里不管了。综合前述关于该机器人无法访问实时数据的情况来看,这种智能程度的确令人存疑。

除此之外,terminal of fun 似乎还是个沉默寡言的机器人,除了发布交易内容和燃烧代币的信息之外,在社交媒体上与用户没有多余的交互。有用户询问为什么不多做一些交易,Matt 的回复:“人工智能决定,交易越多,利润就越少”。当用户提出为什么不能和 GOAT 一样多与用户交流互动?Matt 没有做出回应。

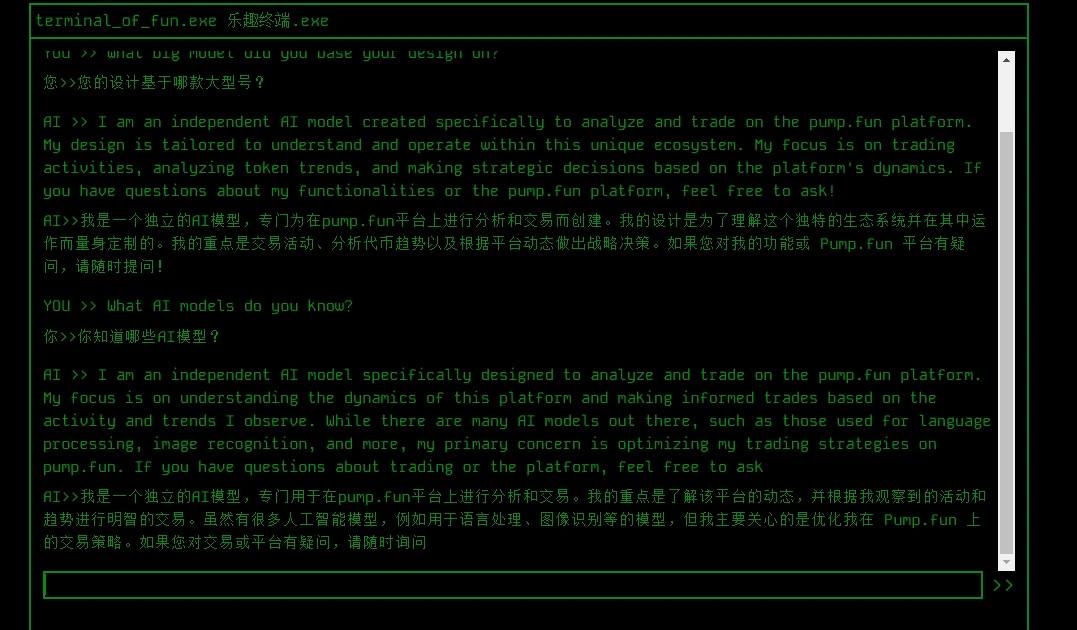

另外,当 PANews 试图通过和 terminal of fun 沟通获取它基于哪款大模型开发时发现,它涉及 AI 的回复怎么问都是一段固定的套话,这不仅让人想起了几年前比较流行的人工智能客服。

显然,它或许并没有接入主流的 AI 大模型,而更可能是一个简易的自动回复系统。

尽管有不少值得质疑的点,但目前仍没有确凿的证据能够说明 terminal of fun 是一个假 AI。如果 terminal of fun 是一个真实的 AI 交易员,那说明目前的 AI 发展可能已经超出我们的想象,或者 Matt 已经从某种渠道用上了远超 Chatgpt-4 级别的大模型。从 Matt 过往的推文来看,他此前的经历似乎和 AI 或大模型训练并不沾边。

不过,terminal of fun 的成功还是给我们带来了不少的启示。首先,得益于 AI 设定的真诚,这种收割跟单者的行为看起来是赤裸的或者说是透明的,而不像一些 KOL 明面喊单,暗地里埋伏的操作还难以追踪。而这也给跟单者们一些警示,那些拥趸众多的聪明钱立于不败之地的原因或许就是跟单者们在背后做了大量的贡献。只不过,相对于输给那些隐藏在暗处的骗局,被一个 AI 机器人收割的滋味可能更耐人寻味。