Author: David Christopher

Compiler: Saoirse, Foresight News

Recently, MicroStrategy disclosed that between June 29 and July 5, the company sold 3,588 bitcoins for a total value of approximately $216 million. The proceeds from this sale were used to distribute STRC dividends and to replenish the U.S. dollar reserves that had been depleted by previous dividend payments. Even after completing this sale, MicroStrategy publicly stated that its $1.25 billion reserve construction capacity remains fully available.

In other words, this $216 million bitcoin sale, intended to replenish reserves, does not consume the $1.25 billion quota allocated for building reserves. Financially, there is a distinction between "replenishing reserves" and "building reserves." However, both operations essentially serve the same purpose: injecting funds into the same pool of dollar reserves, differing only in their accounting classification.

Put differently, this bitcoin monetization plan never locks the total potential bitcoin sale volume at $1.25 billion. That cap only limits one type of operation: raising new funds through bitcoin sales to build up the dollar reserve. Beyond that, the plan allows MicroStrategy to sell bitcoin for other purposes, with the recent sale being a prime example.

Three Major Funding Pools

On June 29, after several weeks of sustained pressure on MSTR and STRC stock prices, MicroStrategy launched a bitcoin monetization plan as part of its overall Digital Credit Capital framework. This plan permits the company to sell bitcoin for three core purposes:

- Build Reserve: Sell bitcoin to raise up to $1.25 billion to bolster the dollar reserve;

- Cover Preferred Stock-Related Expenses: Sell bitcoin to pay fixed dividends on preferred stock and debt interest; or, after using reserve funds to make payments, sell bitcoin to refill the reserve — a method management may choose when selling bitcoin is deemed more advantageous than issuing common stock;

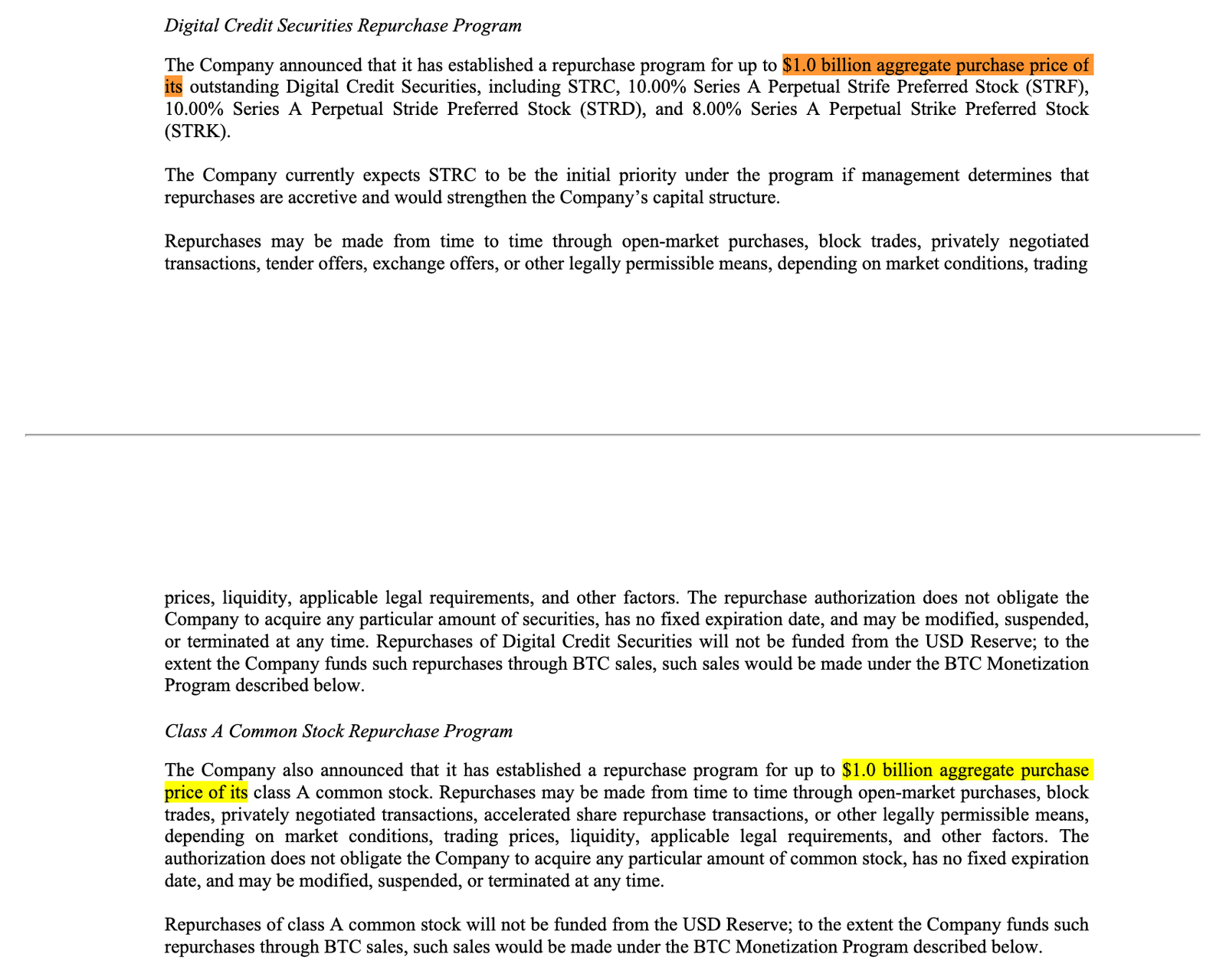

- Fund Share Repurchases: Sell bitcoin to repurchase preferred stock or MSTR common stock, with each repurchase channel capped at $1 billion, totaling $2 billion. Sale proceeds can also cover taxes, fees, and related expenses from the repurchases.

Only the first funding pool has the widely reported $1.25 billion limit; the third repurchase channel alone could monetize up to $2 billion worth of bitcoin. Just these two channels with explicit caps could lead to the sale of over $3 billion in bitcoin, not even counting the unlimited funding pool for dividend payments and reserve replenishment.

Distinguishing 'Building' from 'Replenishing': Blurry-Lined Accounting Operations

The sole purpose of the dollar reserve is to fund preferred stock dividends and debt interest payments. Under current rules, this money cannot be used for stock buybacks. As of June 28, the dollar reserve balance was $2.55 billion, sufficient to cover the company's annual $1.76 billion in mandatory payments for approximately 17 months. The board has set a floor: the reserve must cover at least 12 months of payments, unless the board approves a lower threshold.

This is why the distinction between "building reserve" and "replenishing reserve" deserves close scrutiny:

- Selling bitcoin *before* a dividend payment and depositing the new cash into the reserve: defined as building reserve;

- First using the reserve to pay a dividend, then later selling bitcoin to make up the shortfall: defined as replenishing reserve.

The plan categorizes them as two distinct operations, but their ultimate purpose is identical: selling bitcoin for cash to fund preferred stock dividends and interest payments. The relevant details were publicly disclosed, but this recent sale event vividly demonstrates how convenient this classification system is for the company. MicroStrategy sold $216 million worth of bitcoin, used the funds for dividends and to refill the reserve, yet publicly maintains that the $1.25 billion reserve-building quota remains untouched.

The market must now learn to read this "MicroStrategy-specific vernacular." "Building" and "replenishing" are merely nuanced accounting terms, yet they directly determine whether a bitcoin sale counts against the publicly stated cap.

From Simple Accumulation to Active Capital Management

In the June 29 announcement, Michael Saylor stated that this capital framework was designed to meet the company's needs for liquidity, standardized operations, and active capital management. CEO Phong Le was more direct: MicroStrategy is transitioning from a one-way street of issuing stock to buy bitcoin to a comprehensive, active capital operation.

As Matt Walsh and Jeff Dorman of Castle Island Ventures analyzed on a podcast last week, MicroStrategy has effectively become an actively managed hedge fund.

The market's narrative for MicroStrategy used to be simple: issue MSTR common stock, buy bitcoin, providing investors with leveraged bitcoin exposure. The new framework fundamentally alters this logic: the company will now actively buy and sell its own various capital instruments to balance the multiple pressures between common stock, preferred stock, dollar reserves, and bitcoin assets.

Walsh and Dorman pointed out that this operating model is internally contradictory: issuing common stock can secure preferred stock dividends but suppresses MSTR's valuation premium relative to its bitcoin holdings; selling bitcoin can extend the cash runway but fundamentally undermines the core "never sell" narrative; fully funding preferred dividends can stabilize market confidence but continuously depletes cash reserves; cutting preferred dividends preserves liquidity but could trigger a sharp drop in preferred stock prices.

The accounting loophole in the reserve quota is a microcosm of this strategic shift. Bitcoin is no longer the core asset held for the long term but a financial lever to adjust the balance sheet and maintain the functioning of the preferred stock payment system.

Conclusion

Investors must now anticipate the risks in Michael Saylor's capital management model: every action benefits one part of the capital structure while harming another.

This is also the key signal from the July 6 announcement: MicroStrategy is not short on room to sell bitcoin; its potential sale volume far exceeds the number the market superficially sees. The $1.25 billion figure only represents the company prioritizing the preservation of its bitcoin holdings if investors mistakenly believe it's the total sales cap; don't fall into this cognitive trap.

Today's MicroStrategy is a financial institution whose rules the market must parse word by word. Every professional term is critical: build, replenish, issue, repurchase, stabilize. Investors must dissect every term, like Fed watchers parsing policy statements, to gauge the potential scale of its future bitcoin sales.

This monetization plan gives MicroStrategy operational flexibility, but the underlying internal contradictions remain. It is no longer a simple, clear leveraged bitcoin investment vehicle; betting on this company is essentially a wager on its active capital management capabilities — betting it can continuously sell, refill, issue, repurchase, and stabilize its various capital tools without one link breaking and causing a systemic collapse.

Personally, I wouldn't take that bet.