Author: 21Shares Research Team

Translation: TechFlow News

TechFlow Insights: The 21Shares research team has released an in-depth report on Hyperliquid, with the core argument being: Hyperliquid has evolved from a crypto derivatives DEX into a 7×24 operational exchange for all types of assets. During the February Iran airstrike, when CME was closed, Hyperliquid's WTI crude oil contract completed price discovery nearly 48 hours early. Traditional assets now account for 35% of trading volume, with revenue approaching CME's, yet its valuation multiple is only half. The report provides bull and bear scenario valuations, worth a serious read.

On February 28th, US-Israeli coalition airstrikes on Iran plunged traditional markets into darkness. The Chicago Mercantile Exchange (CME) was closed, its infrastructure unable to react. Hyperliquid didn't stop. This blockchain-based derivatives exchange operates 7×24, with its WTI crude oil perpetual contract pricing in real-time, surging to $111.53, while traditional market traders could only watch.

This event highlighted Hyperliquid's role as a crucial trading venue and price index during intensified geopolitical conflicts—it provided real-time price discovery during the weekend gap. By March 2nd, when traditional markets reopened, WTI had pushed above $110, and the spread between Hyperliquid and CME had closed. Hyperliquid wasn't just faster; it essentially priced in the shock nearly 48 hours ahead of the traditional system.

That narrative alone is compelling. But what turned it into an investment story is what happened next. Fast-forward two months, 24-hour trading volume for crude oil on Hyperliquid remains around $5 billion, with crude oil contracts still among the platform's top five traded assets.

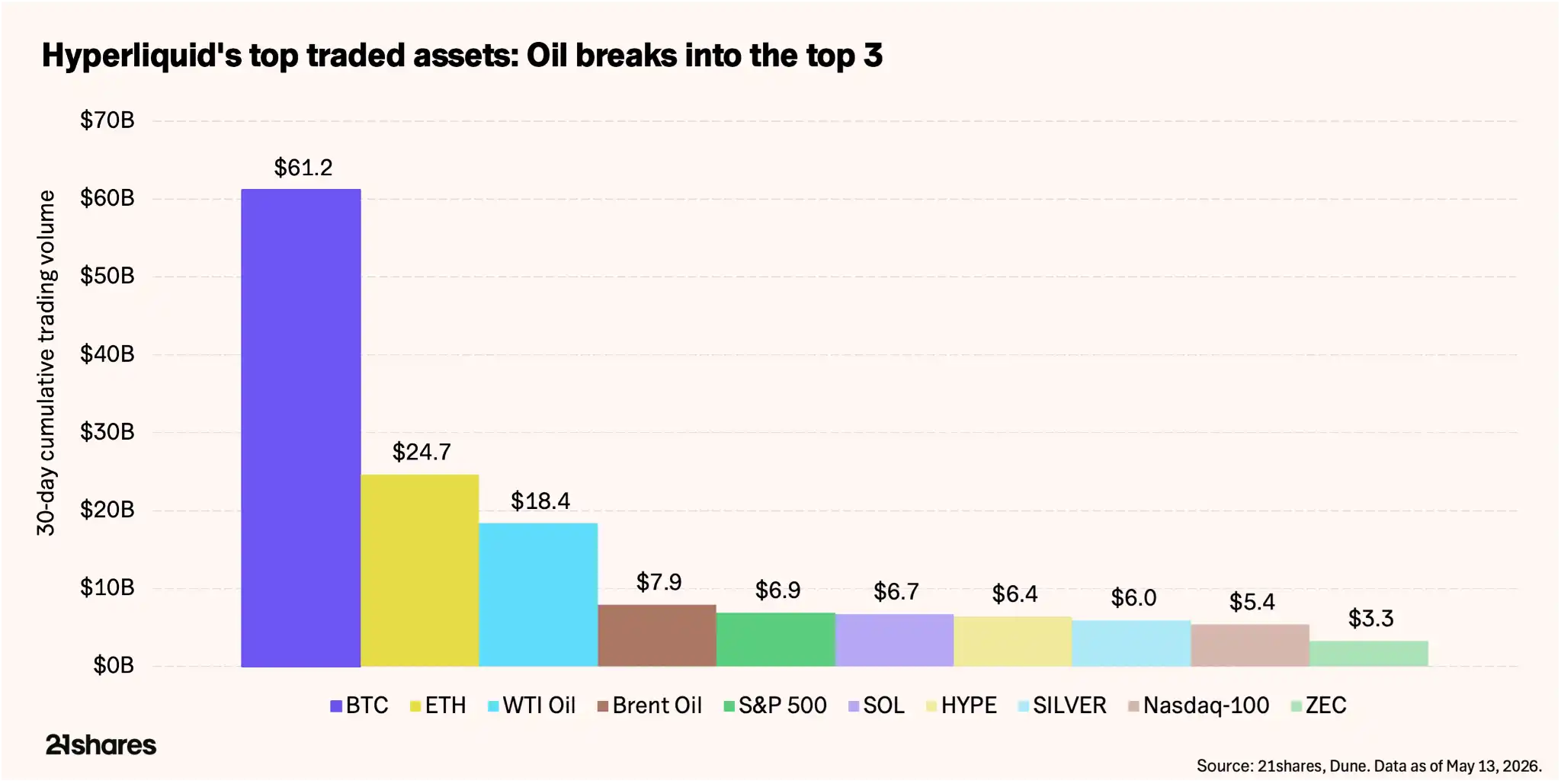

Bitcoin remains the largest traded asset on Hyperliquid, but traditional assets—S&P 500, Silver, Nasdaq 100, WTI, and Brent Crude—now occupy half of the top ten spots. Individual stocks like Micron Technology (MU) even crack the top ten on certain days. We believe this demonstrates Hyperliquid's ultimate trajectory. Hyperliquid is not just an exchange for trading crypto perpetuals; it has fully evolved into an "exchange for everything," where users can trade perpetual contracts on almost any type of asset.

Caption: Distribution of Top Ten Traded Assets on Hyperliquid Platform

Hyperliquid's Business Model is Evolving

This report will help you understand how to reasonably value Hyperliquid and which key metrics and risks investors should monitor.

In the past, most of Hyperliquid's revenue came from digital asset trading, its business model highly correlated with overall crypto market trends. But the growth in non-digital asset trading volume fundamentally broadens the platform's core business model.

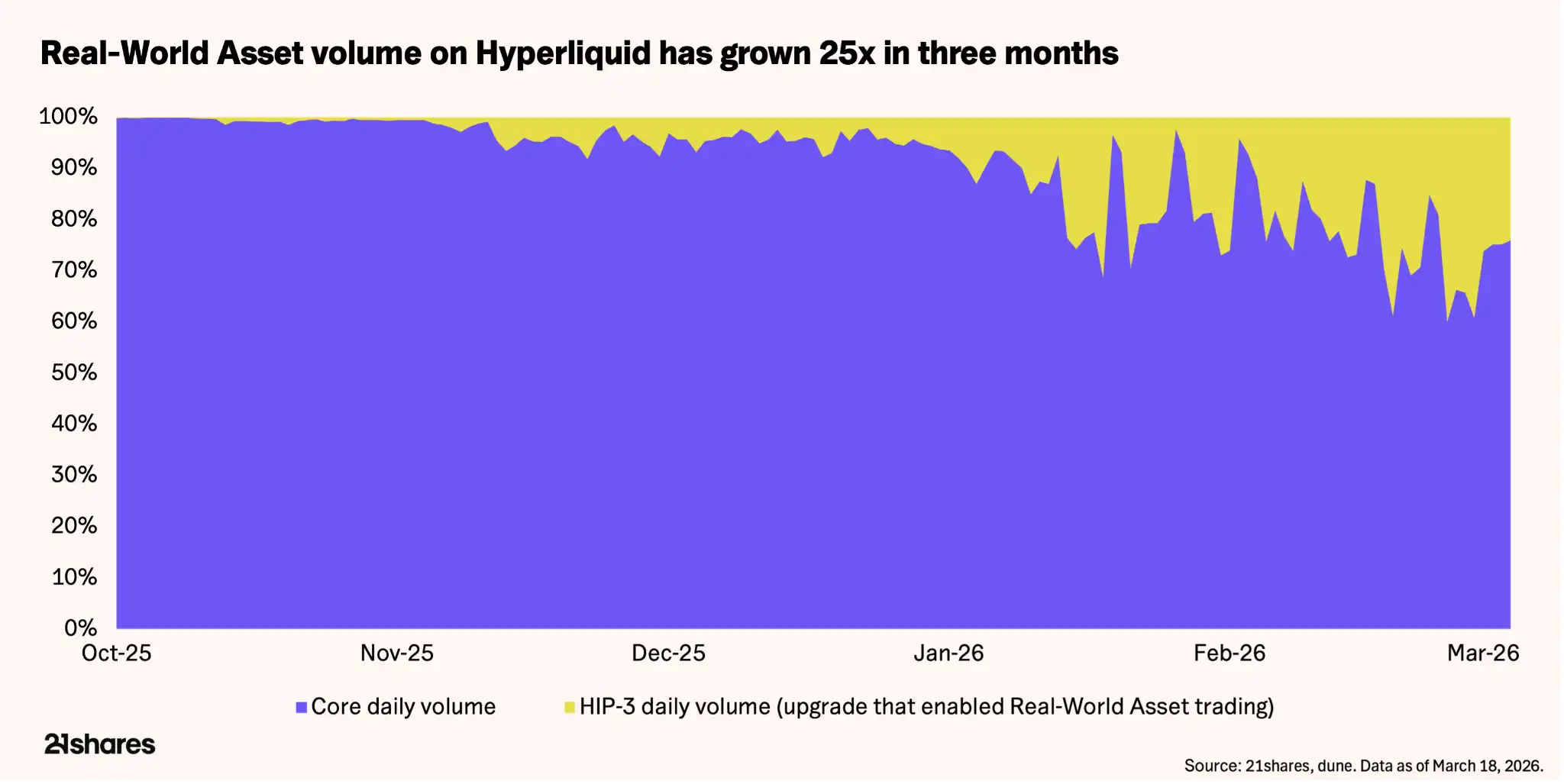

HIP-3 is the protocol's permissionless framework allowing anyone to list new perpetual futures markets. Currently, HIP-3 accounts for about 35%-37% of total trading volume, up 600%-800% from the end of 2025. Open Interest (OI) for these markets reached $1.7 billion in mid-May, growing over 150% since February. Commodities account for about $730 million of that, with crude oil alone making up roughly 20%.

The pace of change is rapid. Crypto trading pairs—the platform's original business—have seen their share drop from around 90% to about 65%. Five of the current top ten traded assets by volume are traditional market instruments, like commodities. A platform that once only offered crypto derivatives is increasingly resembling a macro exchange.

Hyperliquid's bull case is built on this asset class diversification. With the launch of HIP-4 in early May, focusing on prediction markets and options, Hyperliquid is accelerating its journey to becoming an "exchange for everything."

Follow the Money

Hyperliquid's metrics place it among the most profitable protocols in the digital asset space, even allowing comparison with leading traditional derivatives exchanges:

- Cumulative Historical Total Trading Volume: $4.22 trillion. Of this, $2.9 trillion occurred in 2025, comparable to CME Group's $3 trillion in crypto derivatives contract volume.

- Cumulative Protocol Total Revenue: $1.15 billion. Single-year revenue in 2025 was $873 million, compared to CME Group's $6.5 billion for the same period.

Furthermore, the HYPE token benefits from a consistent buy-side force and value return mechanism—the Assistance Fund. This fund channels 97%-99% of the platform's generated fees into automated token buybacks, having repurchased over $1.5 billion worth of HYPE to date. This "share buyback program" scales linearly with trading volume, requires no board approval, and directly impacts the token's supply dynamics with every trade.

At current operational pace, the implied buyback yield is approximately 13% of the circulating market cap. For comparison: CME Group approved a $3 billion stock buyback plan at the end of 2024 but only utilized $532 million. Annualizing this gives about $1.06 billion against a market cap of ~$105 billion, a yield of about 1%. Hyperliquid's capital return rate is roughly 13 times that of CME's, albeit with higher risk.

HYPE serves as both the medium for paying trading fees and the required collateral for deploying new HIP-3 markets. Currently, listing a new perpetual contract market requires locking 500,000 HYPE, valued at approximately $19.5 million. As the platform expands to more asset classes, HYPE is simultaneously drawn from circulation in multiple ways. At current trading volumes, the protocol is in a state of net deflation: monthly buybacks of approximately 1.95 million HYPE exceed unlocks and staking releases of about 1.75 million.

Doing the Math

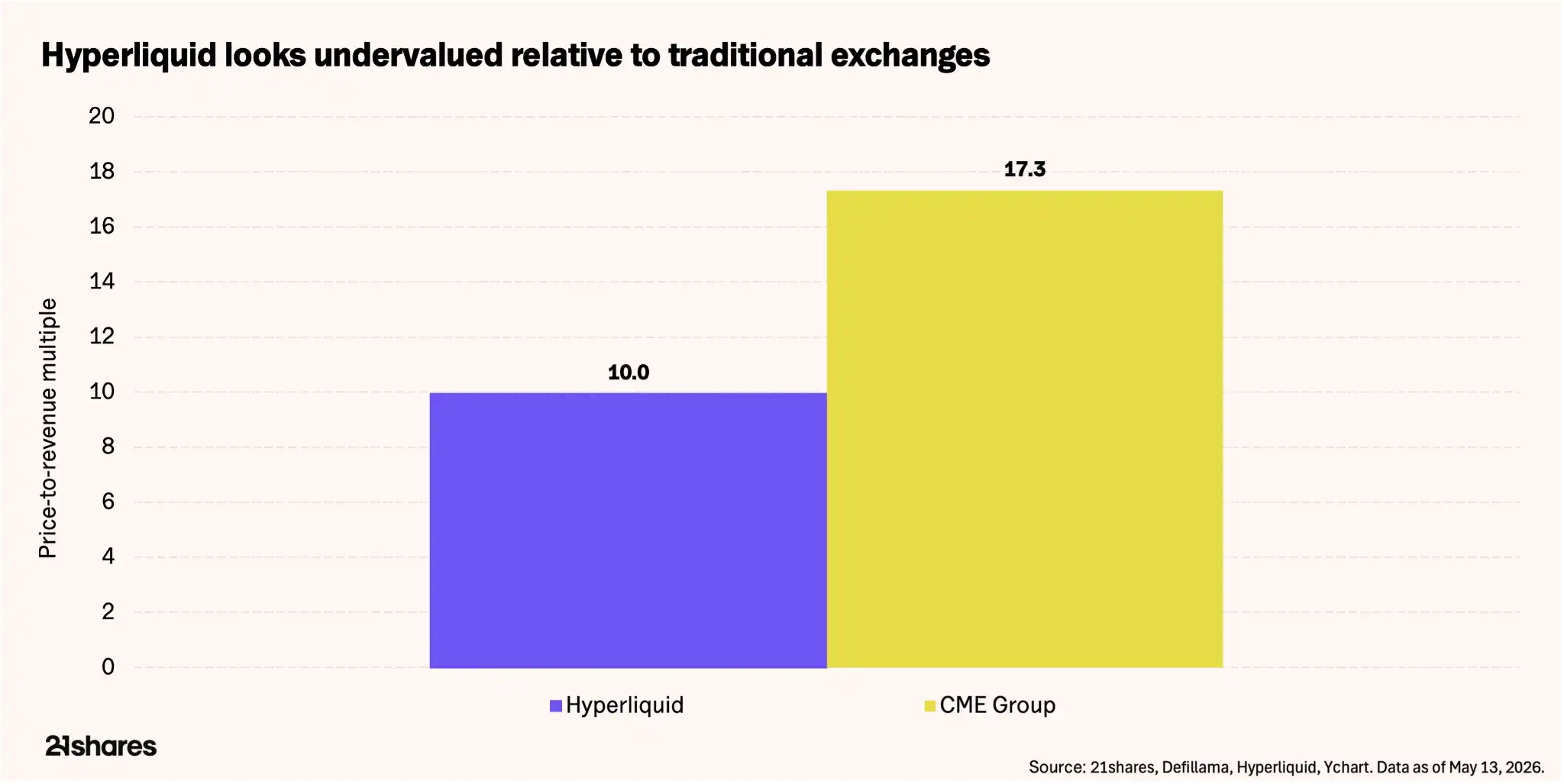

HYPE's current circulating market cap is approximately $9.4 billion. Measured against the past 12 months' revenue of $944 million, Hyperliquid's Price-to-Revenue (P/R) ratio is about 10x—in contrast, the world's largest derivatives exchange, CME Group, trades at a P/R of 17.32x, with a market cap of ~$110 billion and 2025 revenue of $6.5 billion.

Caption: HYPE vs. CME P/R Ratio and Revenue per Employee Comparison

The market is already valuing HYPE using traditional exchange valuation frameworks. The real question is whether Hyperliquid's revenue quality justifies the comparison. To illustrate the efficiency advantage of blockchain infrastructure versus traditional systems: Hyperliquid's 2025 revenue of $873 million was generated by a team of just 11 people—$79.36 million per employee. CME Group's $6.5 billion revenue was supported by 3,875 employees, averaging $1.7 million per person. The difference is stark.

On a fully diluted basis—accounting for the full 1 billion HYPE token supply, most of which is not yet unlocked—the valuation stretches to approximately $37 billion, implying a 38-39x revenue multiple. This figure would only be justified if revenue grows significantly before all tokens enter circulation. But given Hyperliquid's annualized user growth exceeding 100%, coupled with expansion into new asset classes like commodities and prediction markets, this growth premium may be reasonable.

Rather than assigning a specific target price, consider the following scenarios:

Bull Scenario: If geopolitical tensions persist, commodity trading remains elevated, traditional asset traders continue to flock to Hyperliquid post-close, and HIP-3 Open Interest grows to $3-5 billion, annualized revenue could reach the $1.2-$1.5 billion range. Applying CME's 16-17x P/R multiple implies a market cap of $15-$17 billion, corresponding to a HYPE price of ~$62-$70. If options and prediction markets gain traction in the coming months, revenue acceleration could be even stronger.

Base Scenario: Under similar assumptions, with HIP-3 OI growing to $3.2-$5.3 billion, annualized revenue enters the $1.0-$1.1 billion range. At a 17x multiple, the implied market cap is ~$17-$18 billion, corresponding to a HYPE price of ~$75.

Caption: Three Valuation Scenarios Compared (Bull/Base/Bear)

Bear Scenario: If non-digital asset trading cools, buybacks may fail to offset token unlocks, and annualized revenue slides toward the $350-$450 million range. Applying a more conservative 10x multiple—reflecting slower growth and higher dilution—points to a market cap of ~$3.5-$4.5 billion, corresponding to a HYPE price of ~$15-$19, representing a 51%-62% drawdown from current levels. This still does not account for the revenue diversification from the upcoming launch of prediction markets and options trading.

The market is validating our bullish thesis: Bitcoin is down 9% year-to-date, while HYPE is up over 50%. This decoupling stems from HYPE's ongoing transition to diversified revenue streams. HYPE is not risk-free; it simply exchanges crypto beta risk for geopolitical volatility risk. Whether this trend can persist depends on the geopolitical landscape and team execution.

Risks That Must Be Acknowledged

HYPE carries several core risks that investors need to weigh against the protocol's growth:

Centralization & Attack Vectors: The 2025 JELLYJELLY and POPCAT token attack incidents nearly drained the $230 million liquidity vault, forcing validators to manually intervene and delist the assets. While effective, this exposed that the platform can act in a centralized manner when funds are threatened.

Regulation: Hyperliquid still geo-blocks US users, and on-chain commodities operate in a regulatory gray area. To resolve this, HYPE may need to acquire licenses, similar to how Polymarket acquired a CFTC-regulated entity to legally operate in the US market.

Geopolitical Shift: HIP-3 revenue benefits from global tensions. A cooling of macro volatility could quickly erode the "Geopolitical VIX" premium currently driving platform usage, impacting token value.

Issuance vs. Buybacks: Although the protocol is currently in net deflation, its ability to absorb ongoing token unlocks is entirely dependent on trading volumes remaining high.

Conclusion

The crude oil market trades on a blockchain not because of decentralization ideals, but because every other market was closed. This distinction—utility over ideology—is the core difference between Hyperliquid's current moment and previous DeFi narratives.

Valued at 13-15x annualized revenue, the market is pricing HYPE as a legitimate exchange business, not a speculative altcoin. The margin of safety depends on whether non-crypto trading volume is sustainable, whether buybacks continue to outpace dilution, and the execution of new features.

The data itself, at the very least, warrants a serious look at HYPE. As for whether it deserves a place in your portfolio, that depends on your judgment of the world beyond the charts.