The full report is freely available in PDF format.

Welcome to Strategy Watch #4

Strategy Watch was built to address a clear demand for high-signal, impartial analysis of fund-level performance and allocation trends in digital assets.

Our objective is straightforward — to make Strategy Watch a must-read monthly publication for the digital asset investment community.

This publication is strengthened by direct input from market participants. Funds and allocators that contribute data and insights help shape a more complete and valuable view of the landscape. If you have insights, data, or allocation updates worth sharing, we welcome your contribution.

Present your latest initiatives and updates to a curated audience of institutional allocators.

Inside the Latest Strategy Watch

The report is structured across six core sections, each focused on a distinct dimension of institutional activity in digital assets:

01 Institutional Flow Monitor | Institutional demand split by vehicle in May. ETF allocators reduced exposure while digital asset treasuries kept accumulating. What does this divergence signal for allocator positioning?

02 Fund and SMA Performance | Market-neutral strategies kept compounding gains, while the strongest directional returns came from stock selection rather than market beta.

03 Strategy Deep Dive: DeFi/Yield | A CIO's perspective on why fundamentals matter more than ever, and where the next wave of crypto value creation will accrue.

04 On-chain Vault Performance | On-chain credit continues to stabilize, but can vault yields compete with Treasury rates and native ETH staking?

05 Manager Monitor | Find out how managers are positioning as cash balances rise and fundraising conditions remain subdued.

06 Allocation Updates | Institutional expansion continued through new investment firms, dedicated crypto divisions, and quant fund launches.

The Premier Digital Assets Allocator Platform. Learn more

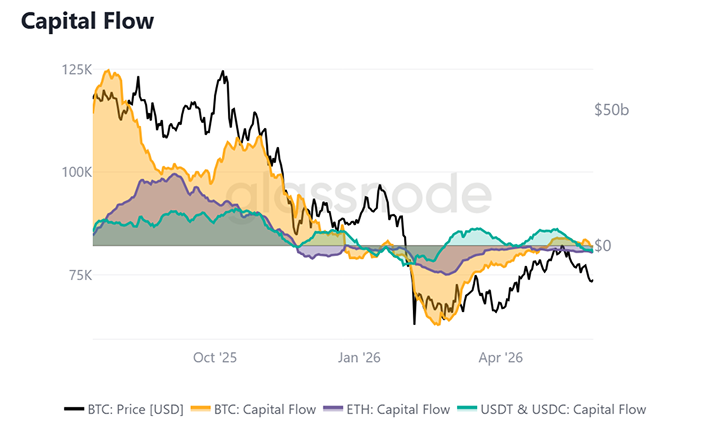

Institutional Flow Monitor

- Bitcoin flows hovered near neutral while Ethereum outflows deepened and stablecoin inflows reversed sharply into month-end.

April's tentative stabilization carried into May for Bitcoin alone. BTC flows held close to neutral, spiking to +$2.9B on May 07 before drifting back to -$0.3B at the close. Ethereum again diverged, deepening from -$1.7B to a -$2.4B trough late in the month before ending at -$2.1B. The sharper signal came from stablecoins, which reversed from a +$6.1B peak early in May to -$2.5B by month-end, a decisive swing into net outflow. That rotation out of dollar liquidity points to allocators trimming risk into June rather than redeploying into spot.

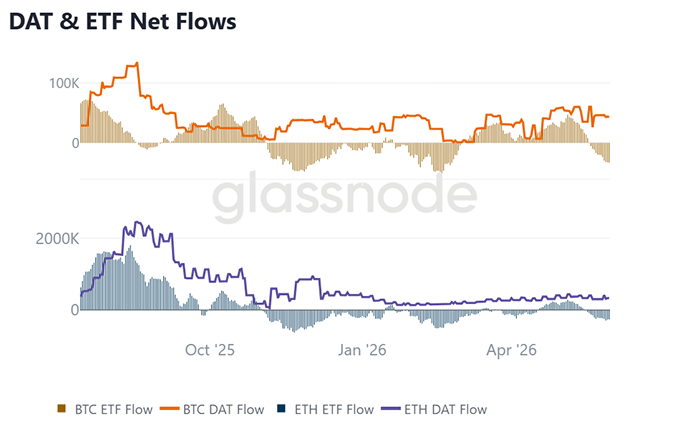

ETF & DAT Net Flows

- Spot ETF flows for both Bitcoin and Ethereum swung from early-month highs into outflows while treasury vehicles kept accumulating.

Institutional demand split by vehicle in May. Spot ETF flows peaked early, with Bitcoin at +46.8k BTC and Ethereum at +283.4k ETH on May 05, before both rolled over into net redemptions, closing at -33.1k BTC and -261.5k ETH as ETF outflows reached a monthly record. Digital asset treasuries told the opposite story and stayed positive throughout. BTC DAT flows held between +26.1k and +60.4k BTC, ending at +42.9k, while ETH DAT flows ran from +302.4k to +439.2k ETH before settling at +330.8k. The divergence suggests balance-sheet buyers kept accumulating into weakness even as ETF allocators de-risked.

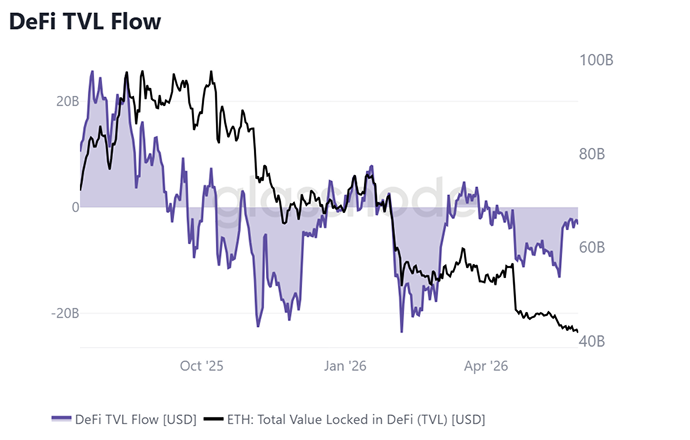

DeFi TVL & Stablecoin Cap

- Ethereum DeFi TVL ground to new monthly lows even as the pace of net outflows eased through the second half of May.

The contraction that followed April's lending exploit persisted through May, though its intensity faded. Ethereum TVL slipped from $45.1B to $41.7B, closing at the monthly low after peaking at $46.1B on May 11. The flow picture was more constructive than the level implied. Thirty-day net flows stayed negative throughout but recovered from a -$13.3B trough on May 18 to -$3.2B by month-end, the shallowest outflow pace since the exploit. The combination of a falling TVL base alongside decelerating outflows suggests the forced deleveraging phase is largely complete, though fresh inflows remain absent.

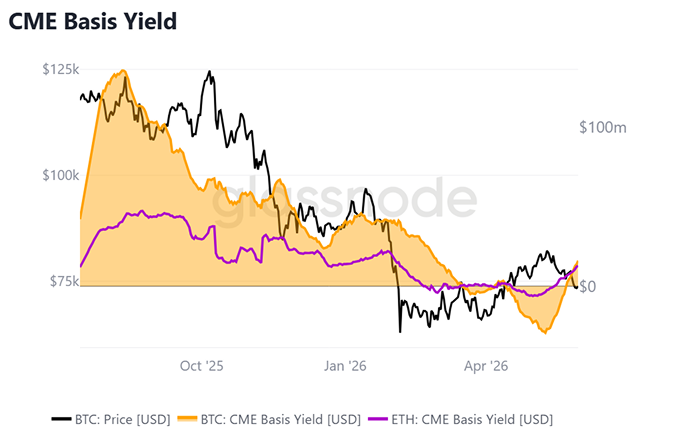

CME Basis Yield

- CME basis yields for both Bitcoin and Ethereum climbed back into positive territory through May, reviving the cash-and-carry trade.

Here we measure the return available to institutions running cash-and-carry trades. After April left both curves in backwardation, May delivered a clean reversal. BTC basis yield bottomed at -$29.3M on May 09 before rising steadily to +$16.0M, the monthly high reached at the close. ETH followed the same path, recovering from -$6.2M at the open to +$12.8M by month-end. Both series finished May at their peaks, with futures reclaiming a premium to spot for the first time since March. The rebuild restores a positive carry to market-neutral strategies, and a continuation into June would mark the firmest premium environment in several months.

Disclaimer: This report does not provide any investment advice. All data is provided for information and educational purposes only. No investment decision shall be based on the information provided here and you are solely responsible for your own investment decisions. Exchange balances presented are derived from Glassnode’s comprehensive database of address labels, which are amassed through both officially published exchange information and proprietary clustering algorithms. While we strive to ensure the utmost accuracy in representing exchange balances, it is important to note that these figures might not always encapsulate the entirety of an exchange’s reserves, particularly when exchanges refrain from disclosing their official addresses. We urge users to exercise caution and discretion when utilizing these metrics. Glassnode shall not be held responsible for any discrepancies or potential inaccuracies. Please read our Transparency Notice when using exchange data.