Author: Fintax

1Introduction

In scenarios such as cross-border payments, asset preservation, and capital flows, the applicability of different financial instruments and institutional arrangements becomes more pronounced in highly uncertain environments. Compared to traditional settlement systems reliant on centralized intermediaries, on-chain assets inherently possess technical features such as cross-border transferability, self-custody, and not being entirely dependent on a single institution. Therefore, in situations subject to sanctions, high inflation, or capital flow restrictions, they are more readily used for value transfer, risk buffering, and asset allocation.

Taking Iran as an example, under extreme external pressure, the Iranian Rial plummeted by 30 times 1 against the US dollar on the open market. Under extreme macroeconomic shocks, on-chain assets with features like cross-border transferability, self-custody, and resistance to single-point freezing were quickly adopted by multinational trade participants and local residents as a risk buffer and capital substitution channel. Chainalysis research shows that by 2025, Iran's crypto ecosystem had reached approximately $77.8 billion, with on-chain activity showing high correlation with major macro events. However, this cross-border flow of assets also comes with it significant compliance risks. Their censorship-resistant characteristics, while providing users with autonomy, can also provide opportunities for illicit fund flows. How to balance innovation and regulation has become a common challenge for global policymakers.

The short-term "channel value" in a volatile macro environment cannot mask the deep-seated value differentiation within the crypto asset market. The long-term blind expansion of token supply stands in stark contrast to the rapid demise of a massive number of projects: CoinGeckoResearch data indicates that over 13.4 million listed crypto projects ultimately ceased trading and were deemed failures2. This vast "graveyard" profoundly demonstrates that assets driven solely by "issuance-financing-narrative" without foundation struggle to maintain consensus long-term; market capital and liquidity inevitably converge towards the few assets with sustainable value mechanisms.

Based on this background, this article takes the "value mechanism" as its core focus. First, it explores which tokens possess sustainable, cycle-resistant value when tested by economic policy uncertainty and multinational economic activity. Second, it provides an in-depth analysis of why, in the evolution of global digital finance, regulatory systems inevitably evolve along a path from governing financing chaos, to governing market infrastructure, and finally to classification details and digitalized reporting.

2Theoretical Foundation

2.1Theoretical Definition of Tokenization and the Three Foundational Proofs

The World Economic Forum (WEF) in its 2025 report defined "Tokenization" as: the process of representing asset ownership in a transferable digital format using a programmable ledger1. Unlike traditional financial systems that rely on fragmented external message passing (like the SWIFT system), tokenization theoretically constructs a Shared System of Record. Combined with smart contracts, it enables a single record system, flexible custody models, and on-chain governance.

The Bank for International Settlements (BIS) further stated in its "Unified Ledger" architecture blueprint that tokenization integrates information transfer, reconciliation, and settlement into a single seamless operation. This underlying architectural leap significantly reduces trust friction and compliance costs in multinational business collaboration. Its theoretical framework is built upon three foundational proofs: First, Proof of Value. This means asset issuance must have a verifiable value foundation—either cash flow support from the real economy or broad network consensus. This ensures on-chain assets are not fabricated "narrative bubbles"; Second, Proof of Ownership. This means property rights must be clear, and the right to dispose of the asset is directly granted to the legal holder. Distributed ledgers use cryptographic means for exclusive rights confirmation, cutting dependence on centralized intermediaries and technically avoiding tail risks like single-point freezing or misappropriation of assets; Third, Proof of Transaction. This requires the generation of an immutable, verifiable transaction history and clearing/settlement evidence. This means every cross-border capital flow is fully traceable, providing the underlying data foundation for post-facto compliance audits and穿透式监管 (penetrative supervision).

These three proofs together form the logical starting point for tokenization's reconstruction of financial infrastructure: Proof of Value establishes the issuance basis of assets, Proof of Ownership reconstructs the form of property rights realization, and Proof of Transaction reshapes the trust mechanism of clearing and settlement.

2.2Two Core Token Models: Native and Backed

Current tokenization models can be divided into two basic categories based on their value capture mechanisms: Native Tokens and Backed Tokens. Their ability to weather macro cycles shows significant differences, rooted in their different value anchors.

Native Tokens are assets issued directly on-chain, with embedded issuance, transaction, and ownership records. These assets (such as native assets of public chains like Ethereum) are typically not pegged to external physical assets. Their core function is to serve as a settlement medium within the network and as a "security budget" to maintain the operation of the decentralized system. Specifically, native tokens attract nodes to maintain network consensus through economic incentive models (like Proof-of-Stake PoS) and act as network fuel fees (Gas Fee) when users call smart contracts and execute complex business logic. The sustainable value of native tokens is deeply tied to whether the public chain network can continuously reduce friction costs for real economic activity—its value沉淀 (precipitation/sedimentation) stems from the prosperity of the network ecosystem and the frequency of actual use. In short, the value anchor of native tokens is network utility.

Backed Tokens are also issued and circulated on-chain, but their value is strictly pegged to off-chain assets. The core mission of Backed Tokens is to bring the real yields of traditional financial markets on-chain. In the current context of heightened economic policy uncertainty, Backed Tokens demonstrate extremely strong practical value. For example, tokenizing high-quality liquid assets like US Treasury bonds not only赋予 (endows) traditional assets with 7×24-hour, divisible global liquidity but also provides on-chain capital with a risk-free rate benchmark detached from the high volatility of the crypto market. For enterprises operating internationally, this constitutes a tool for efficient liquidity management, hedging against local currency depreciation, and reducing cross-border friction costs in complex macro environments. The value anchor of Backed Tokens is off-chain asset value.

The essential difference between the two types of tokens is: the value of Native Tokens comes from within the network, and its sustainability depends on whether the ecosystem can continuously create value by reducing costs and increasing efficiency; the value of Backed Tokens comes from off-chain mapping, and its sustainability depends on the credit quality and redemption ability of the anchored assets.

3Economic Analysis of Sustainable Token Value

After several bull and bear cycles, the crypto asset market is undergoing a profound value return. CoinGeckoResearch data shows that over 13.4 million crypto projects driven solely by "issuance-financing-narrative" ultimately ceased trading and were eliminated by the market. This vast "graveyard" reveals a fundamental rule: speculative products lacking underlying asset support and real application scenarios are destined to fail in maintaining market consensus when macro liquidity recedes.

From an institutional economics perspective, for a token to possess sustainable value that can weather cycles and withstand external macro shocks, its essence must be its ability to substantially reduce friction costs in the real economy and establish a stable rights structure. This sustainable value can be analyzed from the following three dimensions.

3.1Macro Hedging

Enterprises engaged in international expansion and cross-border trade heavily rely on stable, low-friction cross-border payment networks. However, the traditional correspondent banking model, with its lengthy clearing chains and complex compliance nodes, creates significant institutional friction. As of Q1 2025, World Bank data shows the global average cost of cross-border remittances remains high at 6.49%, with average explicit fees through traditional bank channels reaching 12% to 13%3. Cross-border remittance costs by global region are shown in Table 1. Furthermore, due to macroeconomic instability, cross-border remittance costs in some regions are also showing an increasing trend. The Bank for International Settlements also pointed out in its "Agorá Project" research that the existing cross-border payment system is fraught with challenges, and tokenization technology can integrate information transfer, reconciliation, and settlement into a single seamless operation.

Table1Cross-Border Remittance Costs in Selected Global Regions

| Region |

Average Cost (%) |

Cost Trend |

| South Asia |

4.80 |

Lowest Globally |

| East Asia & Pacific |

5.76 |

Stable |

| Latin America & Caribbean |

5.72 |

Stable |

| Middle East & North Africa |

6.25 |

Rising |

| Europe & Central Asia |

7.94 |

Rising Sharply |

| Sub-Saharan Africa |

8.78 |

Continuing to Rise |

Data Source:RemitBee4

When economic policy uncertainty rises sharply—for example, extreme capital controls due to geopolitical games, sanctions, or the severing of SWIFT network connections during a macro crisis—traditional cross-border capital flows not only face high implicit and explicit costs but also encounter availability crises where funds can be frozen at any time. At this point, the value of tokens first manifests as their macro hedging ability as an independent, censorship-resistant channel.

Chainalysis's global macro data validates this logic: in regions under extreme stress from hyperinflation or intensified geopolitical conflicts, retail and corporate users tend to convert funds en masse into supported stablecoins like USDT and USDC to maintain multinational supply chain operations and hedge against rapid local currency depreciation. These on-chain assets, issued based on programmable ledgers, return asset control to the end-user through Self-custody mechanisms, cutting dependence on a single centralized financial intermediary. For multinational economic entities, this on-chain value network with global liquidity has become a capital buffer against the tail risks of macro policies.

3.2AnchoringReal Yield

The demise of a massive number of "shitcoins" proves that token economics relying purely on community sentiment and Ponzi-like liquidity cannot last. The World Economic Forum points out that tokens with sustainable viability must have clear "Embedded Rights"—unalterably赋予 (granting) holders legitimate economic and governance rights at the underlying code level.

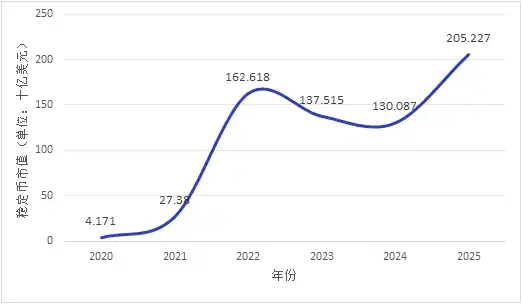

Market capital is undergoing a clear structural shift: accelerating convergence towards assets with "real yield." World Economic Forum reports show that the total transfer volume of stablecoins and other supported tokens reached $27.6 trillion in 2024, exceeding the combined transaction volume of Visa and Mastercard. The market capitalization of stablecoins has shown an overall持续上升的趋势 (trend of continuous rise) since 2020 (see Figure 1. Yearly data is for January of that year). From a macro capital efficiency perspective, there is a potential collateral pool of approximately $230 trillion globally, but constrained by the inefficiency and time friction of physical circulation in traditional financial systems, only about $25 trillion of securities are actually activated as collateral.

Tokenizing high-quality liquid assets (HQLA, such as US Treasury bonds) not only赋予 (endows) traditional assets with 7×24-hour, infinitely divisible global transfer capability but also directly introduces the real economy's risk-free rate on-chain. This mechanism constructs a valuation anchor detached from pure crypto speculation, aligning the value logic of supported tokens with modern finance's classic valuation models, providing a new liquidity tool for corporate treasury management. Market performance confirms this: during periods of increased macro volatility, the circulation scale and trading activity of compliant stablecoins both show significant increases, reflecting the market's substantial demand for "verifiable value anchoring." International Monetary Fund research (2025) indicates that tokenizing central bank reserves is a key path to maintaining the core settlement function of central bank money in the digital asset ecosystem. Its essence is the technical carrier migration of the existing reserve system, not the creation of new central bank liabilities.

Figure1Evolution of Stablecoin Total Market Capitalization (2020-2025), Data Source: CoinLedger5

3.3ReducingFriction andCost

In the micro lifecycle of corporate operations and financial clearing/settlement, the core value of sustainable tokens stems from their重构 (restructuring) of contract execution efficiency. In traditional capital markets, corporate actions like dividend distribution, stock splits, and voting are not only time-consuming and laborious but also prone to information asymmetry and reconciliation errors due to non-structured data characteristics.

The Programmable nature of smart contracts provides a new paradigm to solve this problem: the immutable code mechanism effectively prevents unilateral rule changes and重塑 (reshapes) commercial trust through standardized operations. Multinational compliance checks (KYC/AML), complex asset service流转 (circulation/flow), automated收益分配 (revenue distribution), and other commercial contracts can be transformed into automatically executed program code. Furthermore, smart contracts enable "Atomic Settlement" (i.e., Delivery versus Payment, DvP), fundamentally eliminating reconciliation friction and counterparty risk in multinational collaboration.

Thus, the sustainable value of native tokens is established: they act as the "system security budget" and network fuel (Gas Fee) that maintains the efficient and secure operation of the decentralized underlying ledger. This value logic has been validated by the market—on public chains like Ethereum, network activity and native token consumption show a high positive correlation; the prosperity of the application ecosystem is directly translated into value capture by the token. As long as the underlying public chain can continuously bring substantial cost reduction and efficiency gains to the real world's cross-border payments, supply chain finance, and clearing/settlement systems, the value cycle of its native token can establish a self-consistent flywheel效应 (effect).

4Chaos Governance and Infrastructure Construction

If the underlying programmable mechanism of tokens determines their intrinsic value to weather cycles, then the evolving regulatory framework defines their survival boundaries and compliance costs within the modern macroeconomic system. PwC's annual regulatory report also believes that regulation is no longer a constraint but is actively reshaping the market, enabling digital assets to become an architecture for responsible expansion6. Globally, crypto asset regulation shows a clear evolutionary path over time from "governing financing chaos" to "governing market infrastructure," and then to "classification details and digitalized reporting." The core driving factor is: as the crypto market scale expands and asset complexity leaps, the contagion path of financial risk has fundamentally shifted from within the isolated crypto ecosystem to traditional cross-border capital flows and the macro financial stability system.

4.1Temporal Evolution of the Regulatory Path

Examining the lifecycle of cross-border capital flows, the evolution of the regulatory path is a passive response and active prevention of prominent risks at different stages, which can be specifically divided into three phases:

4.1.1Phase One: Governing Financing Chaos

In the early stages of crypto market development, the market was filled with projects driven solely by narratives. Due to模糊的资产定义 (vague asset definitions) and lack of cash flow support from the real economy, financial risks were集中表现为 (manifested集中ly as) regulatory arbitrage, illegal fundraising, and the resulting damage to investor rights. A large number of projects failed shortly after trading began. Faced with such chaos, the defensive focus of regulation was to切断 (cut off) the无序兑换通道 (disorderly exchange channels) between traditional fiat and根基不稳的代币 (rootless tokens), aiming to prevent the illegal outflow of跨国资本 (cross-border capital) and its systemic disruption to the macro financial order. The core characteristic of this stage is "containment-style regulation"—with curbing risk spillover as the primary goal.

4.1.2Phase Two: Governing Market Infrastructure

As the crypto ecosystem evolved, centralized exchanges (CEX) and custodians rapidly expanded in scale, leading to extreme institutional concentration risk. However, these institutions普遍存在 (generally suffered from) commingling of funds and lack of internal controls in the absence of regulation. When faced with macro liquidity tightening or economic policy uncertainty shocks, these centralized nodes lacking risk缓冲能力 (buffering capacity)极易引发 (easily trigger) "bank run"-like scenarios, similar to traditional banks, with strong pro-cyclical effects. Therefore, the regulatory focus shifted to the韧性建设 (resilience building) of the underlying infrastructure. Policymakers began mandating the implementation of asset isolation (Bankruptcy Remoteness) and independent third-party custody to ensure the integrity of client assets in the event of institutional bankruptcy, thereby cutting the systemic risk contagion chain triggered by single points of failure. The hallmark of this stage is "institution-building regulation"—introducing traditional financial infrastructure safety standards into the crypto ecosystem.

4.1.3Phase Three: Classification Details and Digitalized Reporting

As blockchain technology is gradually absorbed by the mainstream financial system to reduce cross-border transaction friction, regulation entered deep waters. Regulators realized that a "one-size-fits-all" approach could no longer adapt to complex asset forms. Cutting-edge regulations represented by the EU's Markets in Crypto-Assets Regulation (MiCA) and Liechtenstein's Token and VT Service Provider Act (TVTG) define tokens as "Containers of Rights" and implement classification-based regulation strictly according to their underlying economic characteristics. Simultaneously, regulatory tools accelerated towards digitization and API-fication, requiring全天候穿透式监控 (all-weather penetrative monitoring) of on-chain liquidity and cross-border capital movements through unified data reporting interfaces. The core characteristic of this stage is "embedded regulation"—integrating compliance requirements into the technological foundation.

4.2Differentiated Regulation Based on Token Type

Regulators have adopted differentiated compliance requirements and policy tools for tokens with different value anchors.

The regulatory logic for Native Tokens is to strengthen network resilience and anti-money laundering (AML)穿透 (penetration). Non-anonymous crypto assets have a significantly higher average market capitalization than their anonymous counterparts due to their potential regulatory compliance advantages (Cremers et. al, 2025). Native tokens possess characteristics of decentralization and类似无记名资产 (bearer-like assets), with their issuance and settlement completed in an on-chain closed loop. In complex macro environments, this anonymity provides users with autonomy but can also be abused to evade compliance requirements. International AML regulators (e.g., FATF) have listed the AML穿透 (penetration) of Virtual Asset Service Providers (VASPs) as a key regulatory area in their多次更新的指引 (multiple updated guidances). For native tokens and their service providers, regulatory tools heavily rely on On-chain Analytics and the强制实施 (mandatory implementation) of the FATF "Travel Rule," requiring the identification and recording of the真实身份信息 (real identity information) of both transaction parties7. That is, achieving compliance penetration through the service provider环节 (link) without破坏 (destroying) the decentralized network architecture.

The regulatory logic for Backed Tokens is the auditing and liquidity management of the anchored off-chain assets. The value cornerstone of backed tokens lies in their刚性兑付承诺 (rigid redemption promise) for off-chain assets. Their core vulnerability is the potential maturity mismatch and value disconnect between on-chain ledger proof and off-chain real reserves. Facing macro shocks, regulation strictly focuses on preventing "De-pegging" risk. The US Office of the Comptroller of the Currency's regulatory proposal in February 2026 explicitly requires stablecoin issuers to maintain 100% high-quality liquid asset reserves and undergo monthly reporting and annual审查 (review), introducing traditional financial asset auditing standards onto the chain in a more refined manner8. Modern regulatory frameworks强制要求 (mandate) issuers to introduce high-frequency第三方独立审计 (third-party independent audits), strictly limit the investment ratio in high-risk assets, and establish dual liquidity pools, ensuring 100% or even超额 (excess) coverage of the circulating supply by high-quality liquid assets (HQLA). That is, using traditional financial asset auditing standards to provide credit support for on-chain value anchoring.

4.3"Codification" ofCompliance Rules

When handling high-frequency, complex multinational corporate transactions, traditional ex-post accountability-based regulation faces high cross-border enforcement costs and information lag. To balance promoting capital flow efficiency and maintaining financial security, regulators in multiple countries are actively promoting底层创新 (bottom-layer innovation) in "codifying compliance rules."

By introducing token standards specifically designed for compliance (such as ERC-3643, the T-REX protocol), digital identity verification (KYC/AML), AML Travel Rule thresholds, and capital transfer restrictions for specific jurisdictions are directly hardcoded into the smart contract底层 (foundation). This means that if a tokenized asset transfer initiated by a multinational enterprise fails to meet preset compliance whitelist conditions or triggers a dynamically updated sanctions blacklist, the transaction will be automatically blocked at the blockchain protocol level. This regulatory infrastructure innovation, which transforms legal logic into immutable code logic, not only significantly reduces the compliance verification costs for multinational business but also provides infrastructure guarantees for legal capital flows under extreme macro shocks. This marks a fundamental shift in the regulatory paradigm from "ex-post accountability" to "ex-ante embedding." DFCRC report estimates suggest that if the regulatory framework is clear, the tokenized financial market could create tens of billions of Australian dollars in economic benefits for Australia, indicating that the释放 (unleashing) of digital asset potential is dependent on the construction of regulatory infrastructure9.

5Summary and Outlook

Tokenization technology is driving the underlying reconstruction of global financial infrastructure, while macro geopolitical conflicts and persistently high economic policy uncertainty serve as stress tests for this emerging value carrier. Amid剧烈波动 (sharp fluctuations), pure "narrative bubbles" and rootless assets in the crypto market are being gradually stripped away, with market attention and liquidity accelerating their convergence towards tokens with real value support.

This study shows that truly sustainable tokens capable of weathering cycles typically possess several distinct traits:

First, the ability to provide a real yield, introducing off-chain asset credit on-chain;

Second, the ability to substantially reduce the cost of executing cross-border transaction contracts,重塑 (reshaping) commercial trust through programmability;

Third, acting as a security budget for decentralized networks, with their value沉淀 (precipitated/sedimented) in the actual usage frequency and cost-reduction/efficiency-gain capacity of the ecosystem. These tokens are not speculative symbols detached from现实基础 (real foundations) but are value carriers embedded in real economic activity, capable of承载 (bearing) specific functions,收益关系 (revenue relationships), or rights arrangements.

Currently, the global regulatory framework has shifted from early passive containment to active, embedded rule-building. Through classification details and compliance codification, regulators are prudently incorporating high-quality digital assets into the mainstream clearing and settlement system.

Facing this irreversible trend of financial evolution, this article proposes the following recommendations for various market participants:

For enterprises, on-chain assets should be viewed as infrastructure tools to enhance global capital turnover efficiency. In cross-border settlement scenarios, prioritize the use of compliant stablecoins to hedge against fiat exchange rate volatility risks and reduce institutional friction;同时需严格区分 (simultaneously, strictly distinguish between) highly volatile native tokens and strictly regulated supported tokens, implementing differentiated fund management strategies.

For issuers and financial institutions, the old-era logic of "issuing tokens equals financing" must be彻底摒弃 (thoroughly abandoned). The focus of digital asset design should fully shift to "rights embedding"—clearly and unalterably defining asset attributes in the underlying smart contracts, actively adopting compliance-oriented token standards like ERC-3643, and providing the market with transparent, real-time auditable proof of value and real reserve support.

For policymakers, it is recommended to adhere to a technology-neutral prudential principle and promote the innovation of a "compliance-as-code" regulatory paradigm. While坚守 (adhering to) the bottom line of preventing跨国洗钱 (cross-border money laundering) and systemic financial risks, guide the construction of a Unified Ledger based on multilateral consensus, deeply integrate national sovereign credit with programmable technology, and build the next generation of financial infrastructure适应 (adapted to) the digital economy era.