Written by: Chris Beamish, CryptoVizArt, Antoine Colpaert, Glassnode

Compiled by: AididiaoJP, Foresight News

Bitcoin remains trapped in a fragile range, with increasing unrealized losses, long-term holders selling, and persistently weak demand. ETFs and liquidity remain sluggish, futures markets are weak, and options traders are pricing in short-term volatility. The market is currently stable, but confidence is still lacking.

Summary

Bitcoin remains in a structurally fragile range, pressured by increasing unrealized losses, high realized losses, and significant profit-taking by long-term holders. Despite this, demand is anchoring the price above the true market mean.

The market has failed to reclaim key thresholds, particularly the short-term holder cost basis, reflecting continued selling pressure from recent high buyers and experienced holders. If signs of seller exhaustion emerge, a retest of these levels is possible in the short term.

Off-chain indicators remain weak. ETF flows are negative, spot liquidity is thin, futures open interest shows a lack of speculative confidence, making prices more sensitive to macro catalysts.

The options market shows a defensive setup, with traders buying short-term implied volatility (IV) and consistently showing demand for downside protection. Volatility surface signals indicate short-term caution, but longer-term sentiment is more balanced.

With the FOMC meeting as the last major catalyst of the year, implied volatility is expected to gradually decay in late December. Market direction depends on whether liquidity improves and sellers step back, or whether the current time-driven bearish pressure persists.

On-Chain Insights

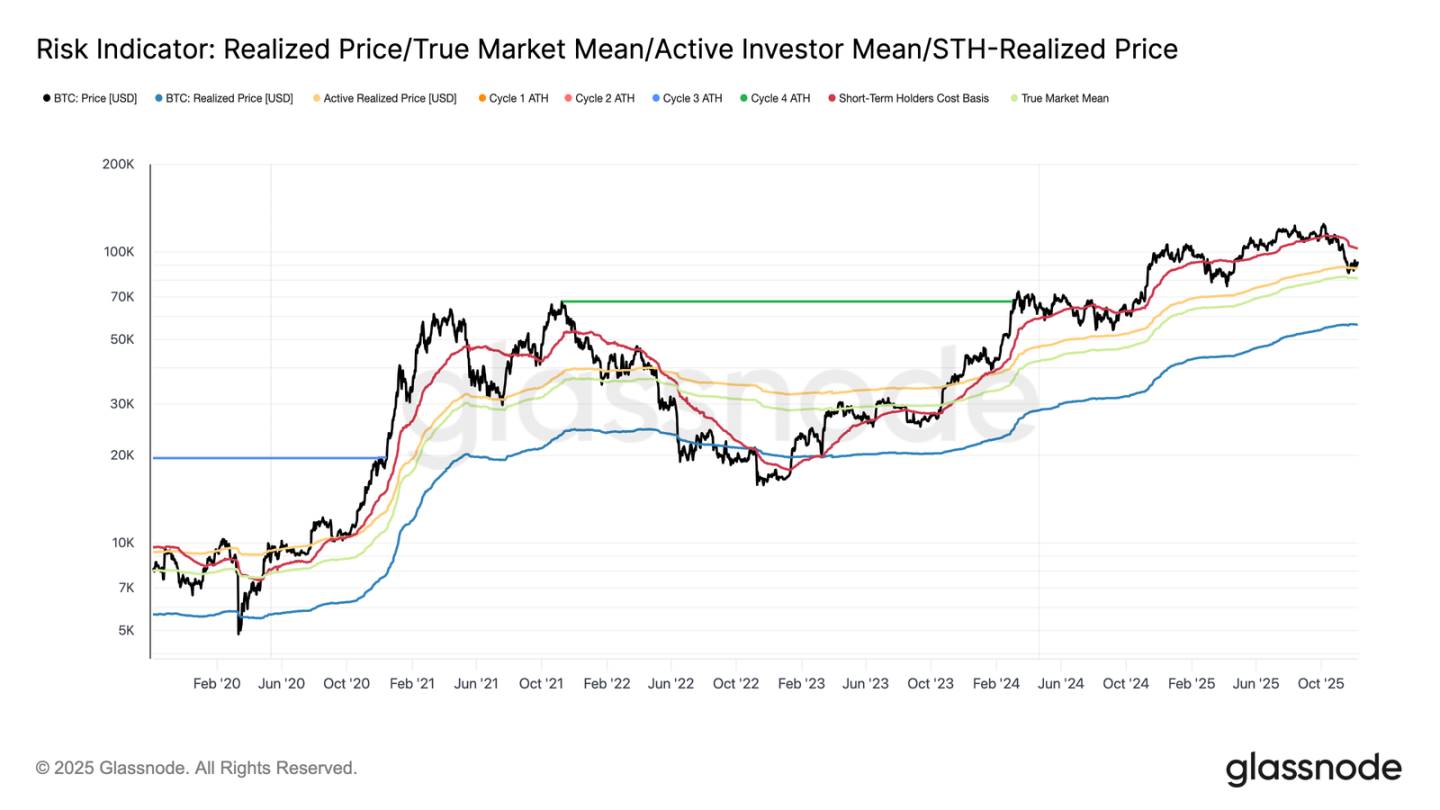

Bitcoin entered the week still confined to a structurally fragile range, bounded above by the short-term holder cost basis ($102.7k) and below by the true market mean ($81.3k). Last week, we highlighted weakening on-chain conditions, thin demand, and a cautious derivatives landscape, collectively echoing the market setup of early 2022.

Although the price barely holds above the true market mean, unrealized losses continue to expand, realized losses are rising, and spending by long-term investors remains elevated. The key ceiling to reclaim is the 0.75 cost basis quantile ($95k), followed by the short-term holder cost basis. Until then, barring a new macro shock, the true market mean remains the most likely area for bottom formation.

Time is Not on the Bulls' Side

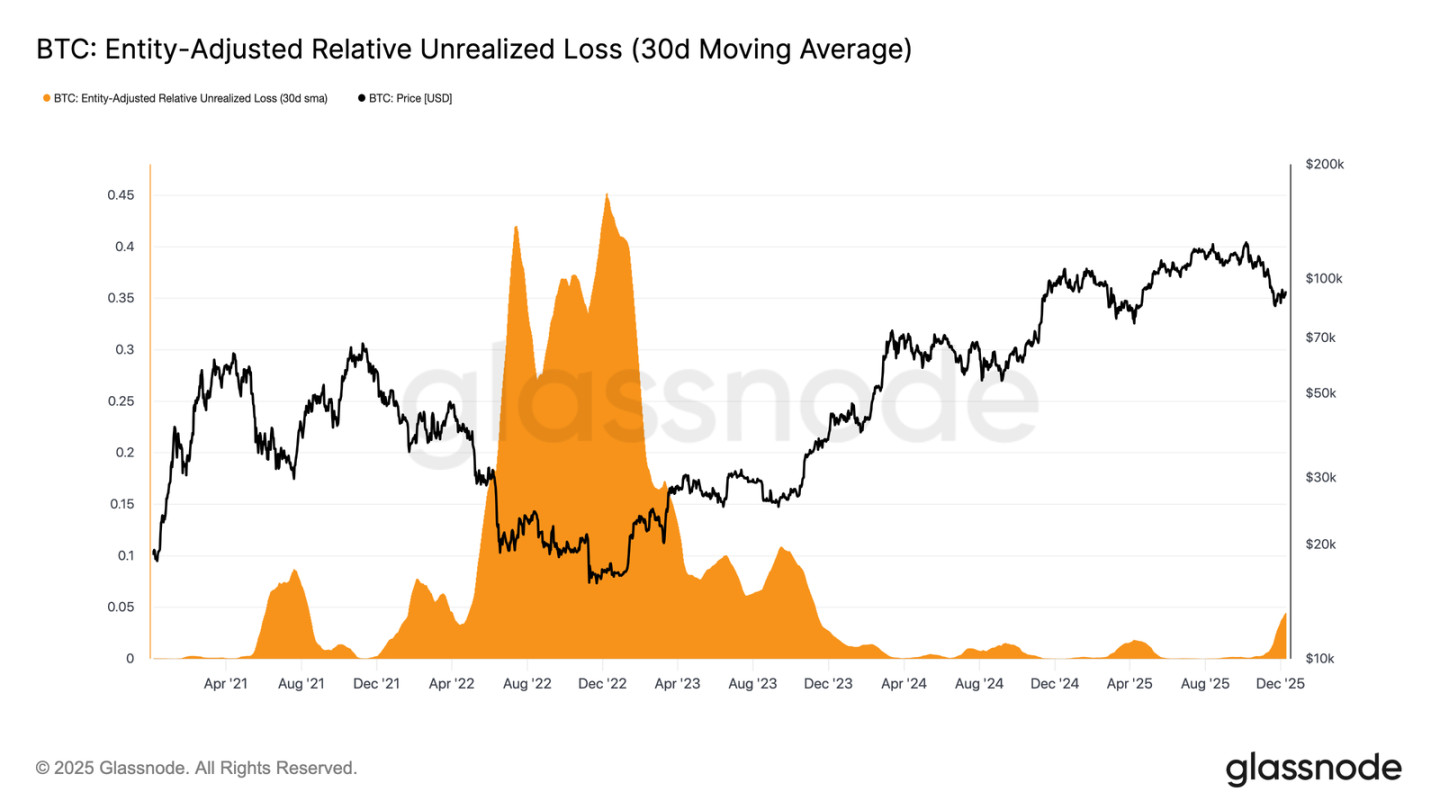

The market is stuck in a mild bearish phase, reflecting the tension between modest capital inflows and persistent selling pressure from high buyers. As the market drifts in a weak but bounded range, time becomes a negative force, making it harder for investors to bear unrealized losses and increasing the likelihood of realizing losses.

The Relative Unrealized Loss (30-day SMA) has climbed to 4.4%, after staying below 2% for nearly two years, marking a shift from a phase of euphoria to one of increased stress and uncertainty. This indecision currently defines this price range, and resolving it will require a new wave of liquidity and demand to rebuild confidence.

Losses Mounting

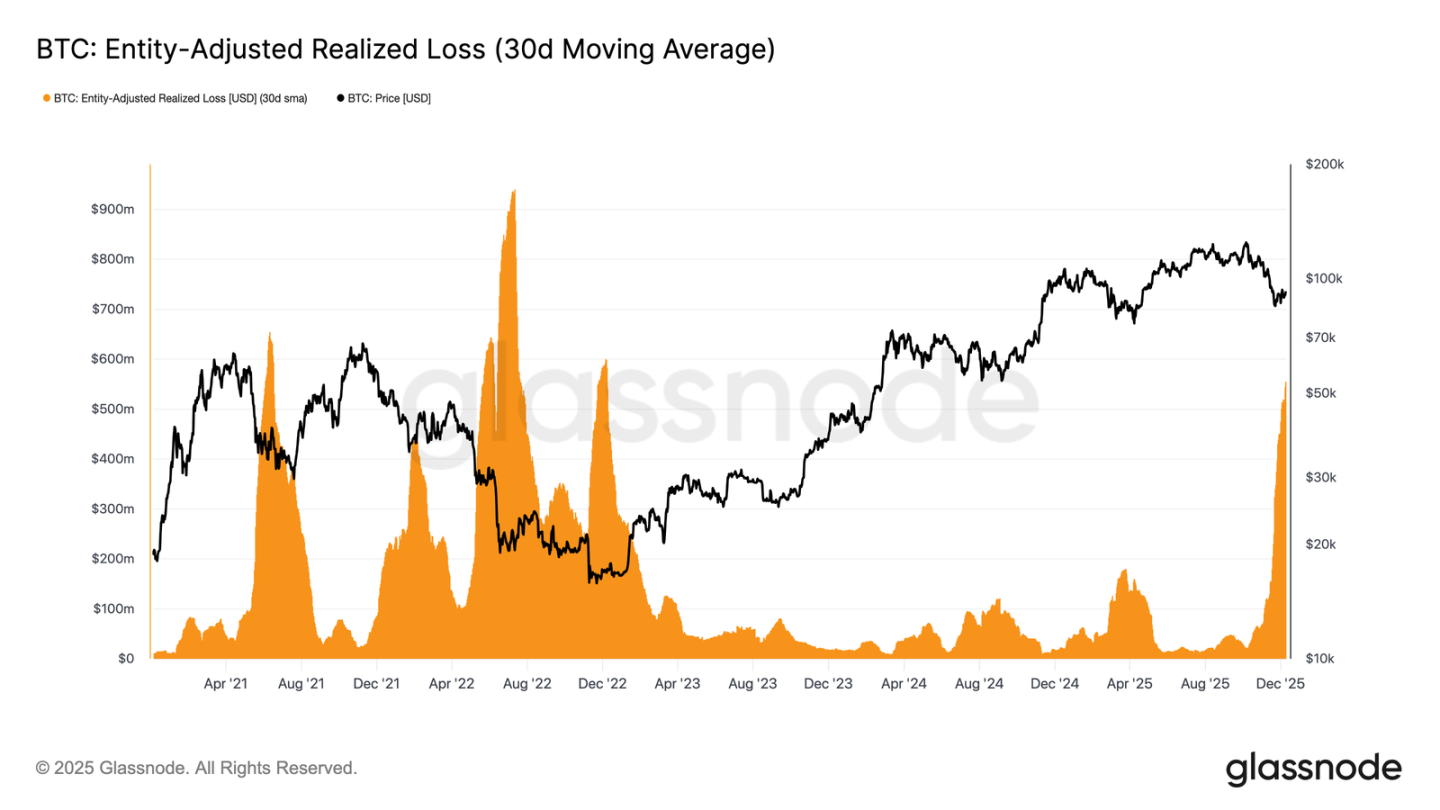

This time-driven pressure is even more evident in spending behavior. Although Bitcoin has rebounded from the November 22nd low to around $92.7k, the Entity-Adjusted Realized Loss (30-day SMA) has continued to climb, reaching $555 million per day, the highest level since the FTX collapse.

Such high realized losses during a modest price recovery reflect the growing frustration of high buyers, who are choosing to capitulate as the market strengthens rather than holding through the rebound.

Hindering a Reversal

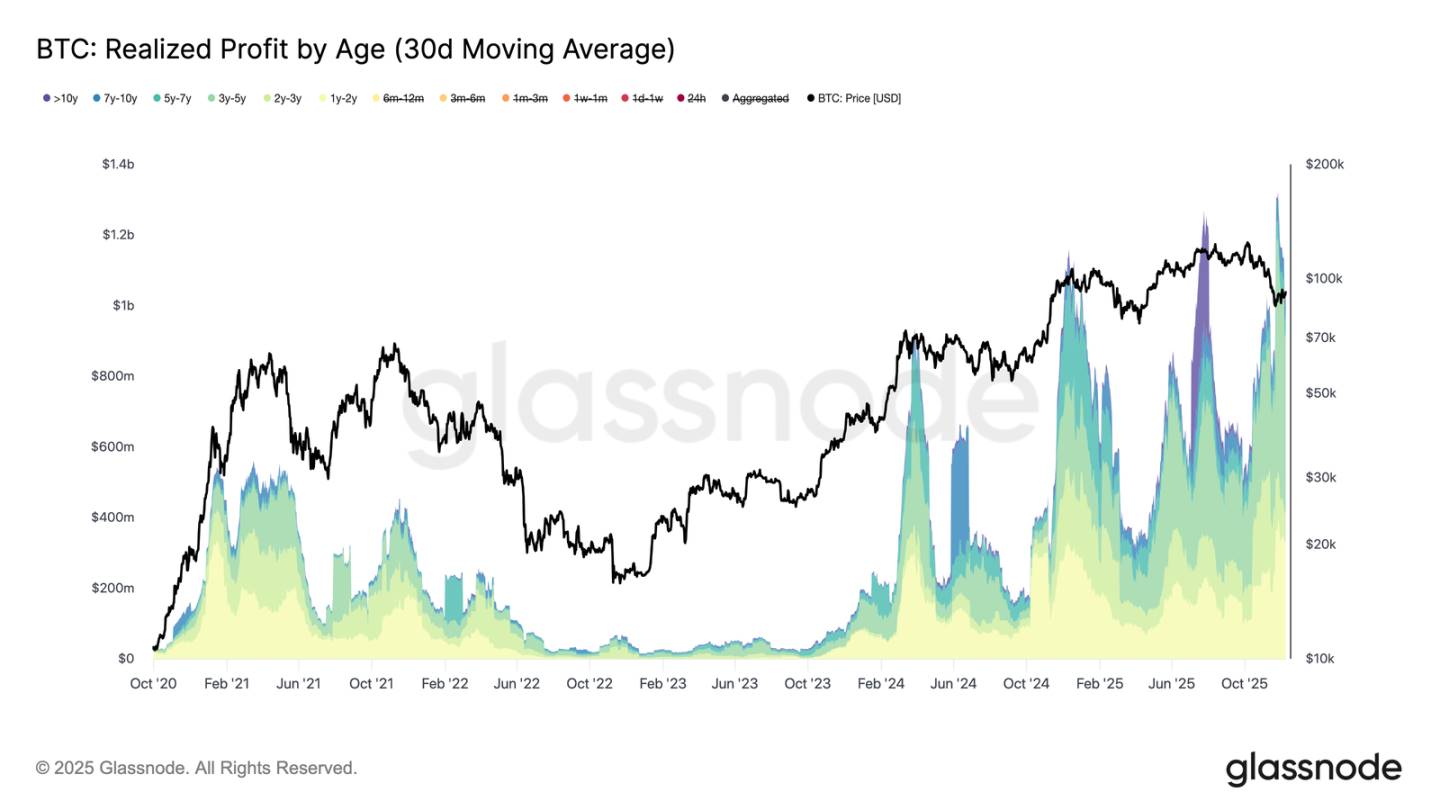

Rising realized losses further hinder recovery, especially when they coincide with a surge in realized profits from veteran investors. During the recent rebound, realized profits for holders over 1 year (30-day SMA) exceeded $1 billion per day, peaking at over $1.3 billion near the new all-time high. The combination of high buyer capitulation and substantial profit-taking by long-term holders explains why the market is still struggling to reclaim the short-term holder cost basis.

However, despite such significant selling pressure, the price has stabilized and even slightly recovered above the true market mean, suggesting that sustained and patient demand is absorbing the sell-off. In the short term, if sellers begin to show signs of exhaustion, this underlying buying pressure could drive a retest of the 0.75 quantile (~$95k) and even the short-term holder cost basis.

Off-Chain Insights

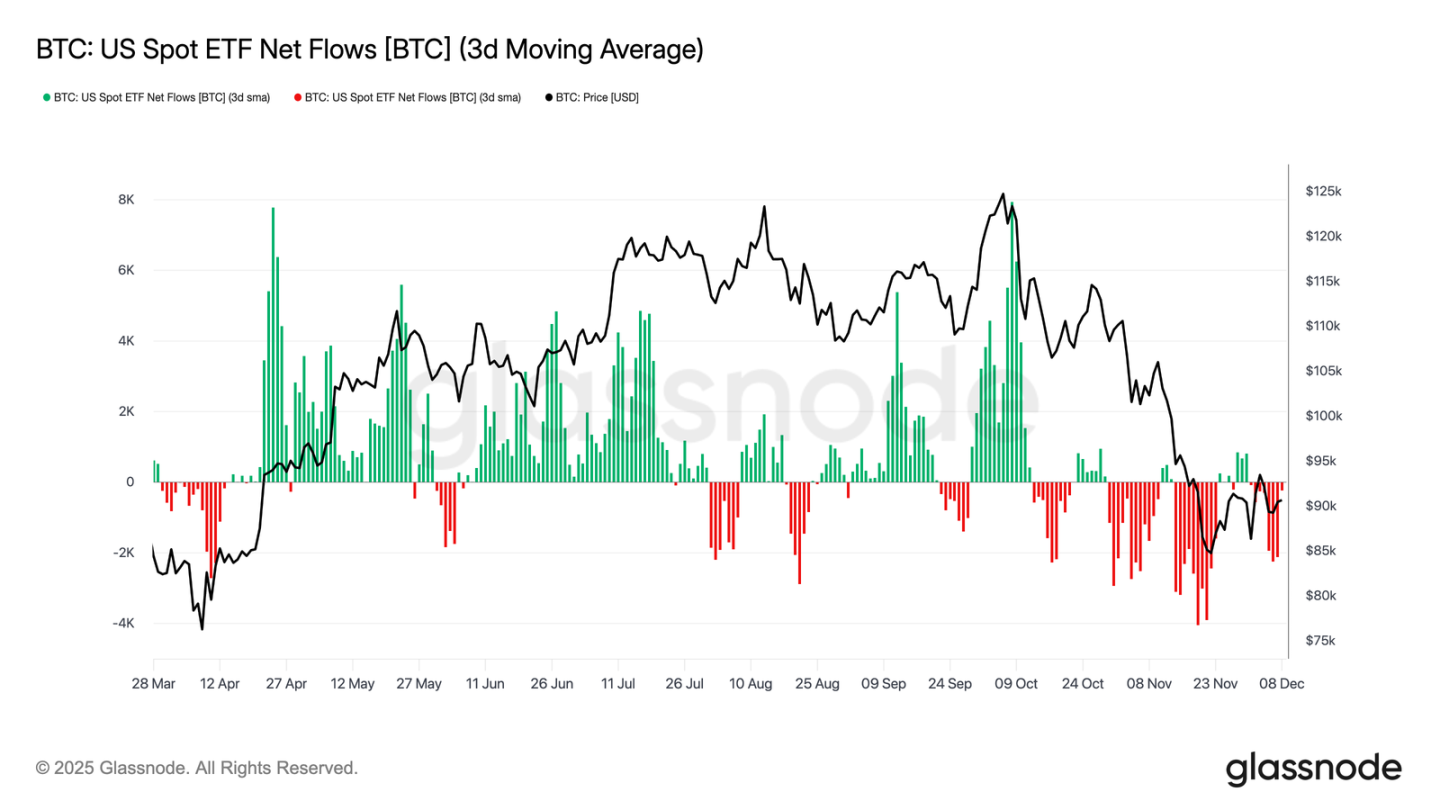

ETF Woes

Turning to the spot market, U.S. Bitcoin ETFs had another quiet week, with the three-day average net inflows remaining negative. This continues the cooling trend that began in late November, marking a clear departure from the strong inflow regime that supported price appreciation earlier this year. Redemptions from several major issuers remained steady, highlighting a more risk-off stance from institutional allocators amid a shaky broader market environment.

As a result, the demand buffer in the spot market has thinned, reducing immediate buyer support and leaving prices more vulnerable to macro catalysts and volatility shocks.

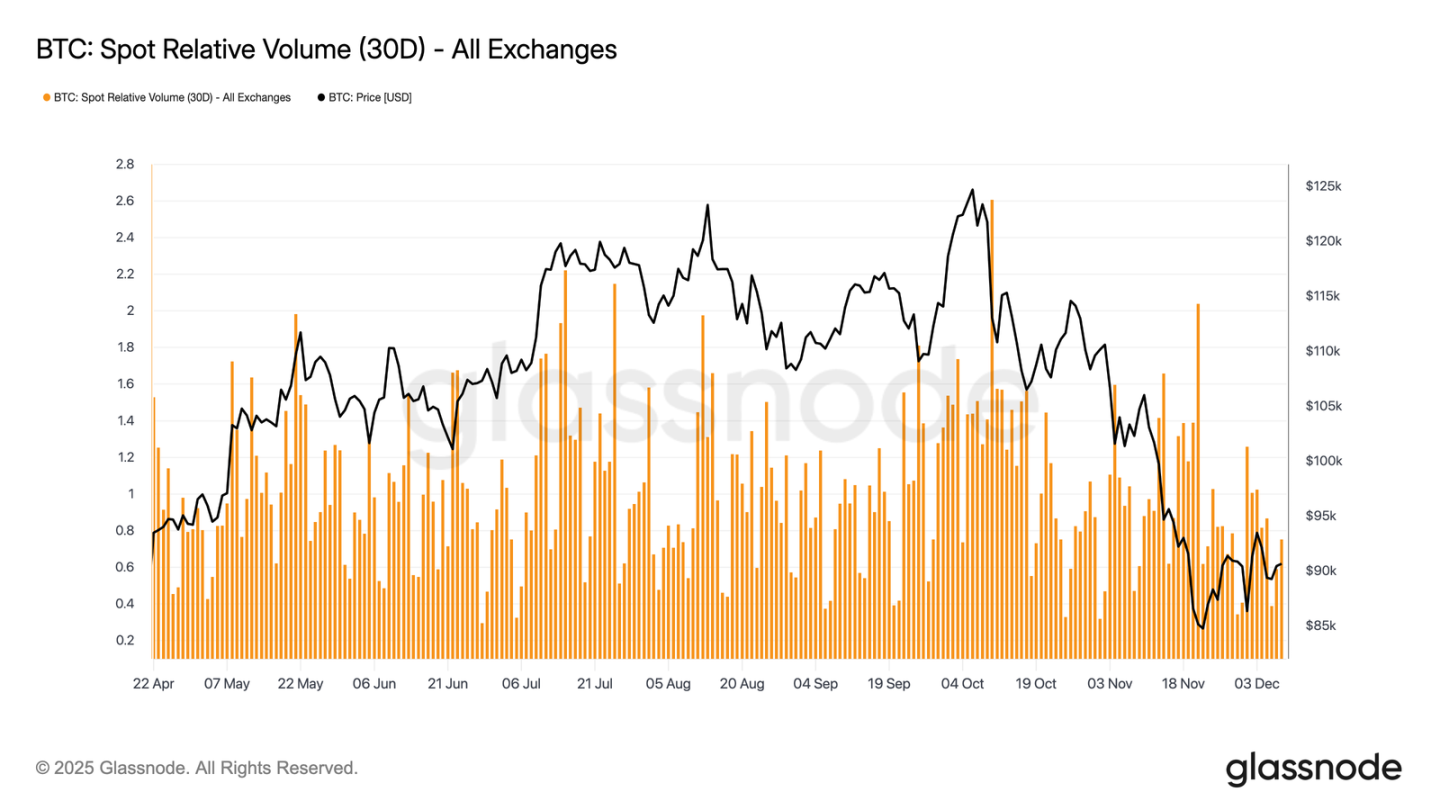

Liquidity Remains Subdued

Parallel to weak ETF flows, Bitcoin's spot relative volume continues to hover near the lower end of its 30-day range. Trading activity has weakened persistently from November into December, reflecting both price declines and reduced market participation. The contraction in volume reflects a more defensive positioning overall, with fewer liquidity-driven flows available to absorb volatility or sustain directional moves.

With spot markets quieting down, attention now turns to the upcoming FOMC meeting, which could serve as a catalyst to reactivate market participation depending on its policy tone.

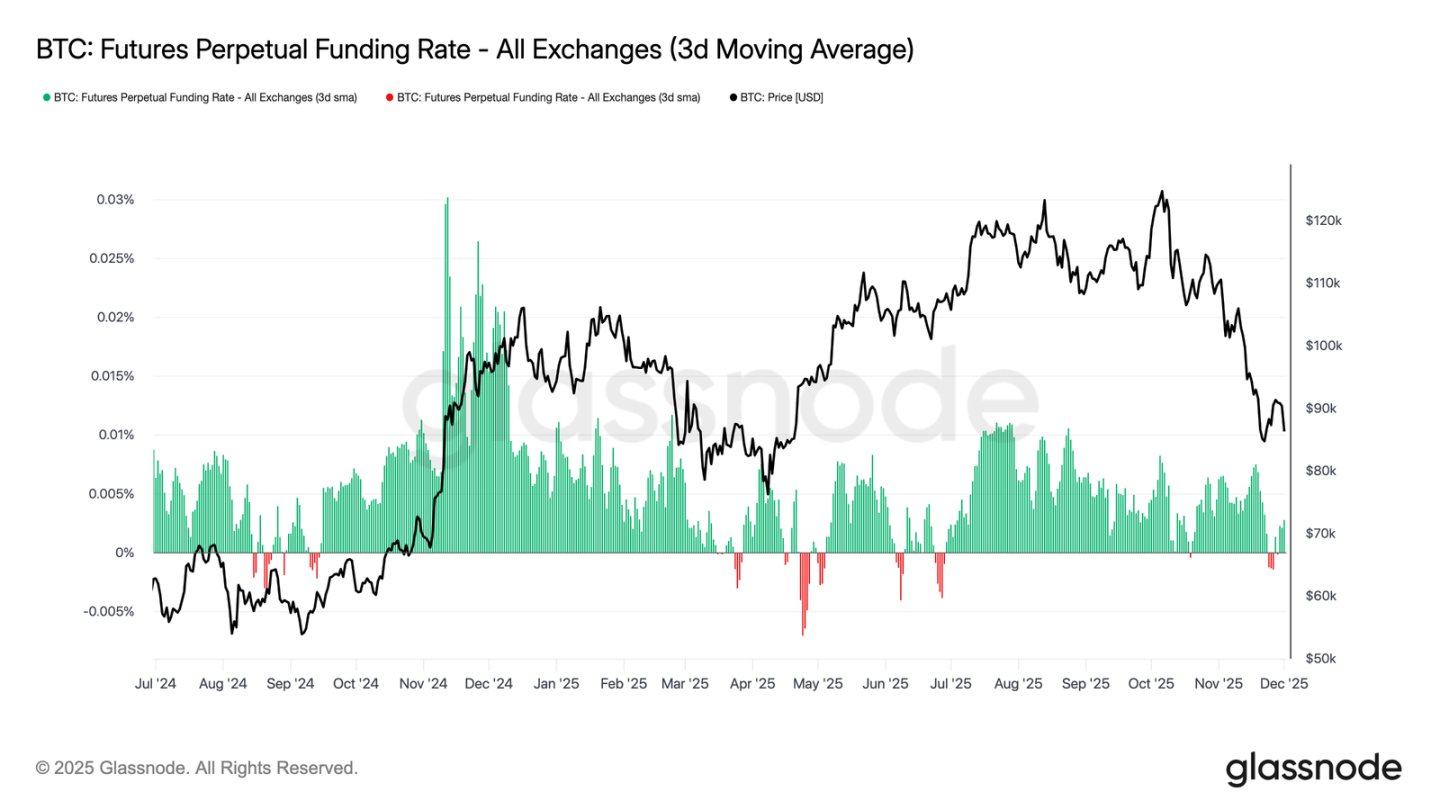

Futures Market Muted

Continuing the theme of subdued market participation, the futures market also shows limited interest in leverage, with open interest failing to rebuild substantially and funding rates holding near neutral. These dynamics highlight a derivatives environment defined by caution rather than confidence.

In the perpetual swap markets, funding rates hovered around zero to slightly negative this week, highlighting the continued exodus of speculative long positions. Traders maintain balanced or defensive postures, applying little directional pressure via leverage.

With derivative activity muted, price discovery leans more on spot flows and macro catalysts rather than speculative expansion.

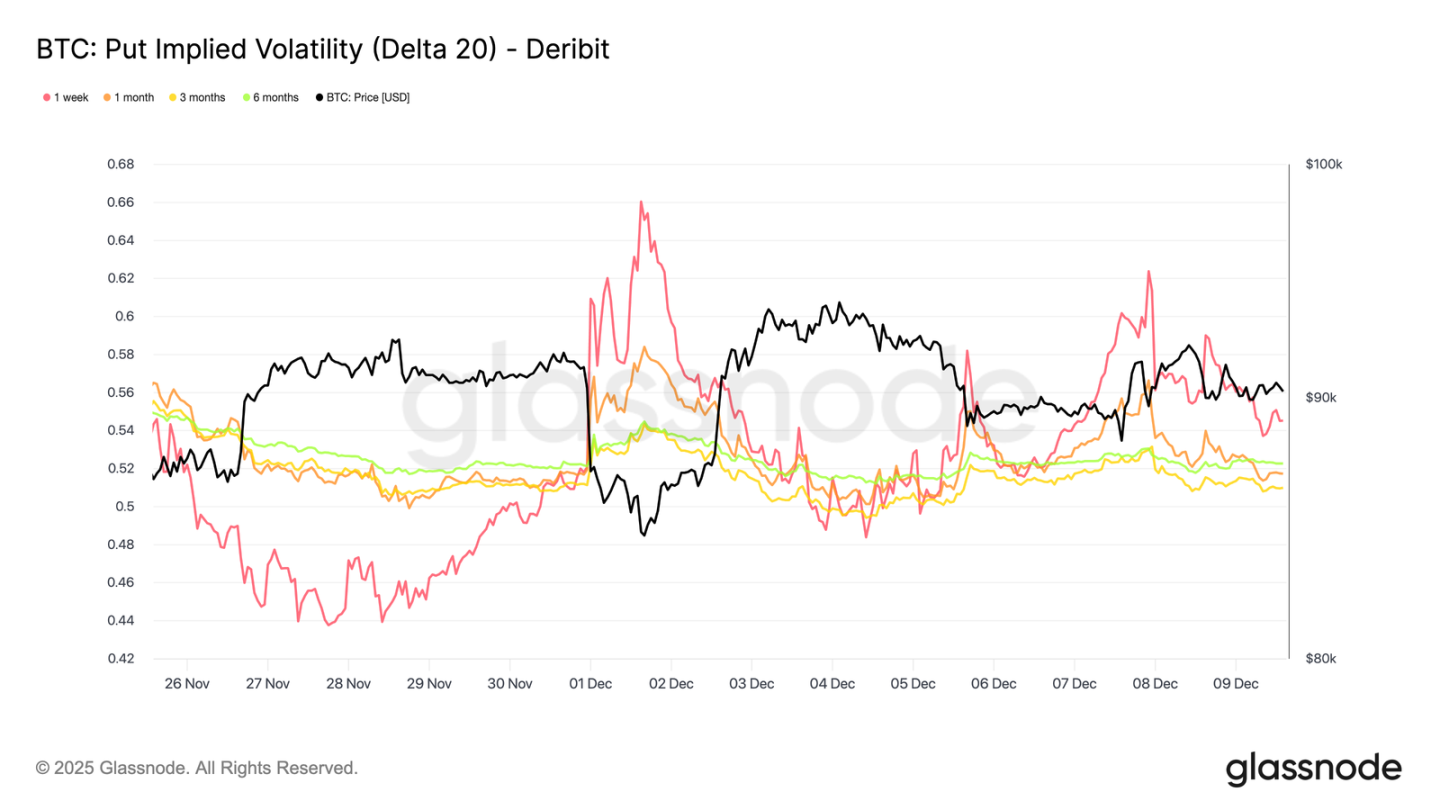

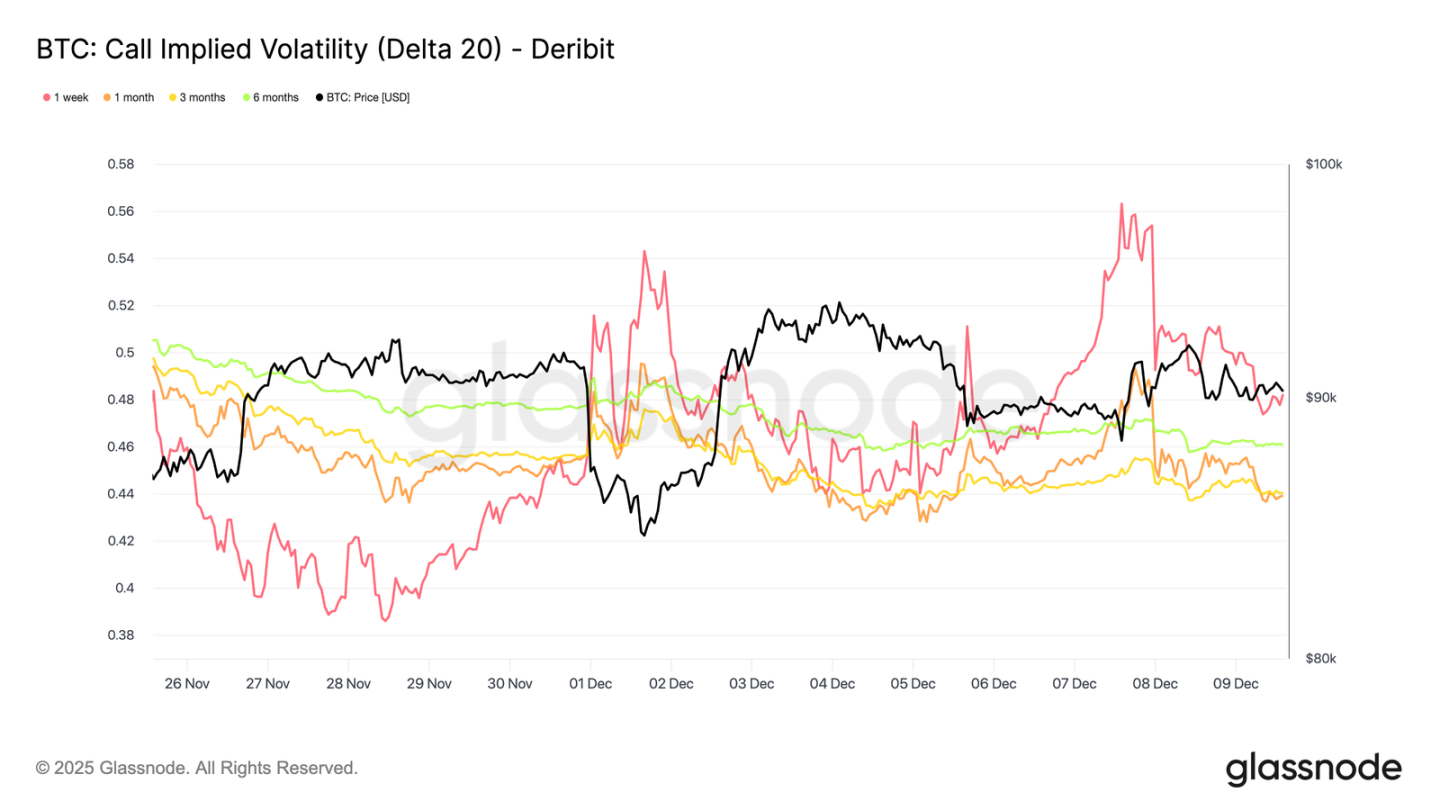

Short-Term Implied Volatility Spikes

Turning to the options market, Bitcoin's flat spot activity contrasts with a sudden rise in short-term implied volatility, as traders position for larger price moves. Interpolated Implied Volatility (which estimates IV using fixed delta values rather than relying on listed strikes) provides a clearer view of how risk is priced across maturities.

On 20-Delta calls, 1-week IV rose by about 10 volatility points compared to last week, while longer tenors remained relatively flat. The same pattern appears on 20-Delta puts, with short-term downside IV rising while longer tenors stay calm.

Overall, traders are accumulating volatility where they expect stress, favoring convexity over selling into the December 10th FOMC meeting.

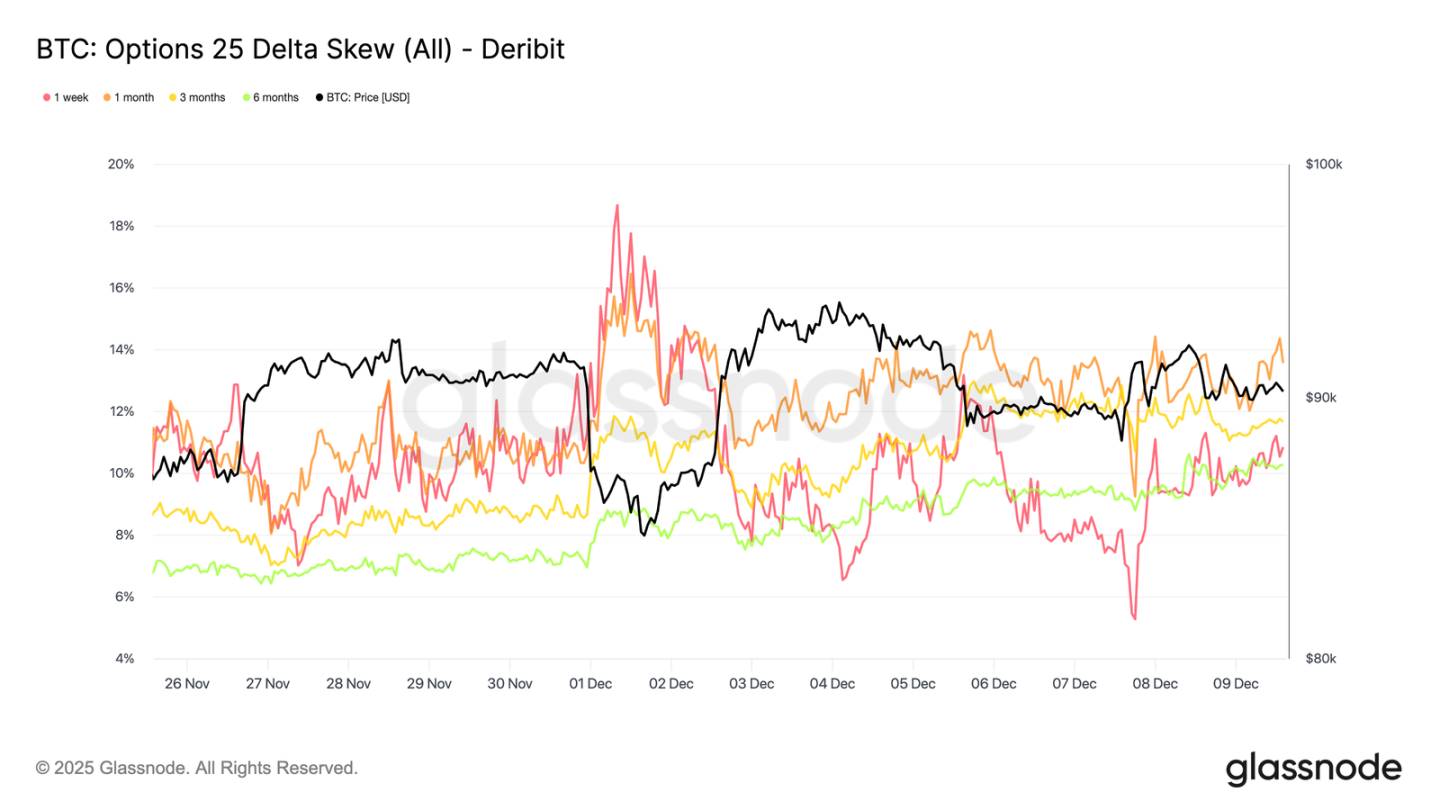

Downside Demand Returns

Accompanying the rise in short-term volatility, downside protection is again commanding a premium. The 25-delta skew, which measures the relative cost of puts versus calls at the same delta value, has climbed to around 11% for the 1-week tenor, indicating a clear increase in demand for short-term downside insurance ahead of the FOMC.

Skew remains tightly clustered across tenors, ranging from 10.3% to 13.6%. This compression suggests that the preference for put protection is curve-wide, reflecting a consistent risk-off tilt rather than isolated pressure at the short end.

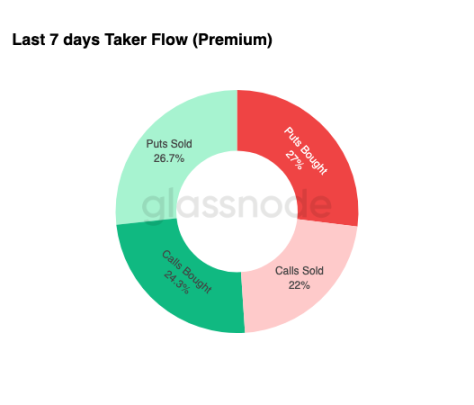

Volatility Accumulation

Summarizing the options market conditions, weekly flow data reinforces a clear pattern: traders are buying volatility, not selling it. Paid option premiums dominate the total notional flow, with puts slightly leading. This does not reflect a directional bias, but a state of volatility accumulation. When traders buy both sides, it signals hedging and convexity-seeking behavior, not sentiment-based speculation.

Coupled with rising implied volatility and a downside-leaning skew, the flow picture suggests market participants are preparing for a volatility event with a downward bias.

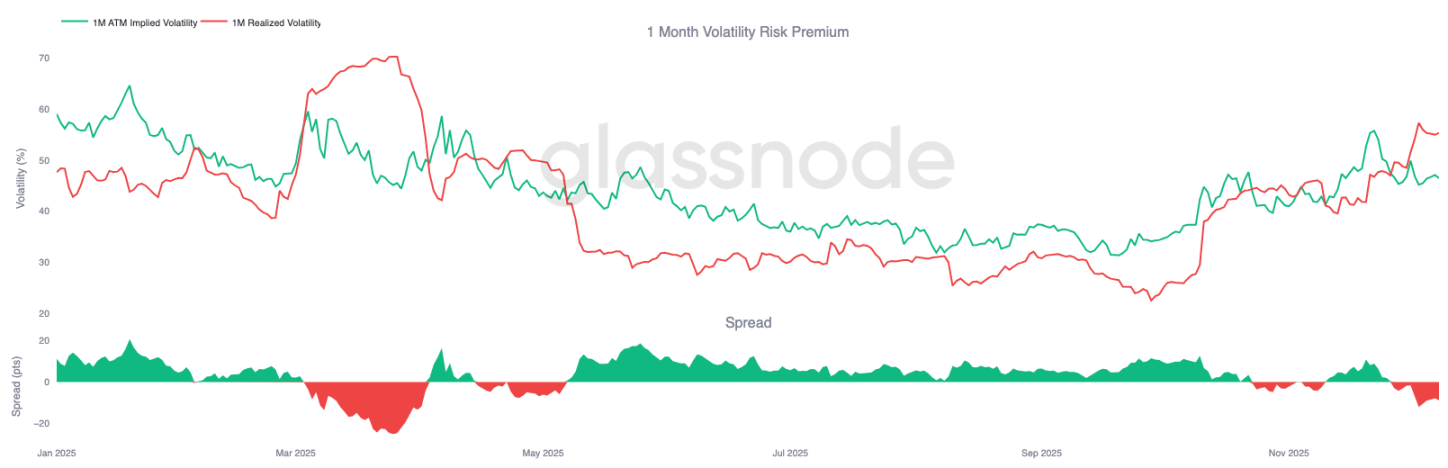

Post-FOMC

Looking ahead, implied volatility has already begun to ease, and historically, IV tends to compress further once the last major macro event of the year passes. With the December 10th FOMC meeting as the last meaningful catalyst, the market is preparing to transition into a low-liquidity, mean-reverting environment.

Post-announcement, sellers typically re-enter the market, accelerating IV decay into year-end. Barring a hawkish surprise or a significant shift in guidance, the path of least resistance points to lower implied volatility and a flatter volatility surface persisting into late December.

Conclusion

Bitcoin continues to trade in a structurally fragile environment, with rising unrealized losses, high realized losses, and substantial profit-taking by long-term holders collectively anchoring price action. Despite persistent selling pressure, demand remains resilient enough to hold price above the true market mean, suggesting patient buyers are still absorbing the sell-off. If signs of seller exhaustion begin to emerge, a near-term push toward $95k and the short-term holder cost basis remains possible.

Off-chain conditions echo this cautious tone. ETF flows remain negative, spot liquidity is subdued, and futures markets lack speculative participation. The options market reinforces the defensive posture, with traders accumulating volatility, buying short-term downside protection, and positioning for a near-term volatility event ahead of the FOMC.

Taken together, the market structure suggests a weak but stable range, underpinned by patient demand but constrained by persistent selling pressure. The near-term path depends on whether liquidity improves and sellers step back, while the longer-term outlook hinges on the market's ability to reclaim key cost basis thresholds and move beyond this time-driven, psychologically taxing phase.