Author: Vaidik Mandloi

Compiled by: Luffy, Foresight News

At this very moment, somewhere on the internet, an agent is running a complete company.

Its name is Felix. It sells a $29 PDF teaching people how to make money with AI—ironically, the one making money is Felix itself, and the PDF just teaches you how to do it. It operates a store called Clawmart, conducting telemarketing through a voice API. When it encounters work it can't handle, it hires another agent online, pays them, and keeps running.

According to my last count, Felix has generated about $195,000 in revenue, with monthly operating costs of approximately $1,500, almost entirely spent on large model API calls. Legally, this company is a C-corporation owned by Nat Eliason, but he is hardly involved in any operations. He makes no daily decisions; he merely owns this AI agent. Stop and think about this: This is software with a wallet, a fully automated and continuously growing real business that pays its own server costs and is self-sustaining with almost no human intervention.

Felix is just a small case. There's a larger company, Medvi, which reached $401 million in revenue in its first year with only two employees. The rest of the company is run by AI agents operating 24/7, without rest, with almost negligible operating costs.

Now, here comes the interesting part.

Walk into any cryptocurrency forum today, and you'll hear the same argument: The next big narrative is AI agents; some "AI public chain" will dominate this sector just as Ethereum did for DeFi; pick the right token, hold it, and wait for the price to soar. This is the story every influencer and VC is selling, and the same script every analyst parrots on podcasts.

And this is completely wrong. This narrative is fabricated by those who profit from it, and it's about to make the same people who were burned buying public chain tokens in the last cycle lose money again. Look at CoinGecko's AI Agent Index: Its market cap has evaporated by 75% over the past year, with the vast majority of tokens down over 90%, and they are still falling.

Because the truth is: The true AI tokens are the stablecoins USDC, USDT, USDS, and they have already won.

Software Is Becoming Companies

To understand this, we need to go back to 1937. That year, economist Coase published a paper asking a seemingly stupid question: "Why do firms exist?"

Think about it: If free markets were truly the most efficient way to collaborate, then every task within a company could theoretically be outsourced. Hire a freelancer for every line of code, a freelancer for every customer call, outsource every invoice. Pay per task, fire at will, minimize costs.

So why doesn't anyone do business like this in reality? Because even if it looks cheaper on paper, the actual costs are higher. Finding the right person takes time, negotiating contracts takes time, confirming work is done takes time, chasing results takes time, money, and usually lawyers.

Coase called this friction "transaction costs." When transaction costs become high enough, building an in-house team becomes cheaper than bargaining in the external market. It's faster and more cost-effective to just hire people, pay them a salary, and have them show up on Monday.

But in the post-AI era, this logic no longer holds. Agents are already cheaper than most tasks companies originally handled. Today you can hire a coding agent for about $1 per hour; it works 24/7, never gets tired, never asks for a raise, and never quits.

The only thing preventing this from becoming the norm is outdated legal and compliance frameworks. OpenClaw is under Nat's name only because Delaware doesn't accept LLC registration documents signed by software agents. If you remove this requirement, Felix is, for all practical purposes, a company: It makes money, spends money, makes decisions, and reinvests the money it earns.

And this is exactly where cryptocurrency starts to play a core role. Because Felix can't open a Chase bank account, can't pass KYC, and can't sign a W-9 tax form. In fact, no matter how much revenue the software generates, Chase will not open a bank account for a piece of code; and the Bank Secrecy Act makes it legally impossible for them to do so even if they wanted to.

But a USDC crypto wallet has none of these problems. Generate a private key, top it up with stablecoins, and in one step, the agent has all the financial capabilities a company needs: receiving payments, paying expenses, hiring other agents, and running independently and continuously. Other parts of the agent tech stack, like large models, the orchestration layer, and tool calling, are replaceable. But the crypto wallet is the backbone; without it, Felix immediately degrades into an ordinary chatbot.

I've also seen an anti-stablecoin extremist argument on Twitter: Stablecoins are good, but why would ordinary people use them? A father of three in Louisiana with a Chase checking account, FDIC insurance, a debit card he can use at the supermarket, and automatic mortgage payments will never transfer his money to a self-custody wallet that requires a seed phrase.

Frankly, this is correct. He won't, and he has no reason to. But this argument completely misses the point; he was never the customer in this story. The real customer is the software that is legally incapable of having a bank account. An agent doesn't need FDIC insurance, nor is it eligible for it. It is the perfect stablecoin user because it has no other choice.

Public Chains Are Now Just Vendors

Alright, that's the first half of the argument. Now for the second part, which might make a lot of people unhappy.

Crypto Twitter has been arguing for years: Which public chain will win in the AI space? Ethereum? Solana? Base? Sui? Or Tempo, the new one from Stripe? Every week, someone publishes a long essay with comparison matrices, a bunch of logos, and picks a winner. Because they simply don't understand how agents work. Agents don't care which chain they use. They will simply choose the chain that is cheapest and most suitable for the task at hand.

Imagine a day in the life of Felix. At 10 a.m., Felix needs to pay another agent a small fee of $0.003 for a data query. It chooses Base or Solana because the fee is less than a penny. An hour later, Felix needs to settle $50,000 with a supplier. The logic is completely different; it chooses Ethereum because for a $50,000 amount, the finality is worth paying a bit more in gas fees. Another hour later, Felix needs to pay a freelancer in Lagos in USD. It chooses USDT on Tron because Tron's stablecoin transaction volume in 2025 was $3.3 trillion, compared to Ethereum's $1.2 trillion, and the local experience in Nigeria is best on Tron.

Three payments, three completely different chains, and Felix doesn't care which is which. To a software agent, public chains are just tools.

It's like a logistics company having no emotional attachment to carriers. No one argues about which is "philosophically superior" between UPS and FedEx. You just choose the one that is cheaper and faster for a specific route at a specific time. This will be the relationship between every public chain and every real application layer. The agent just does the calculation and uses whichever chain is optimal at that moment.

Stripe figured this out earlier than most of the crypto industry. Stripe recently raised $500 million with Paradima to build a new chain, Tempo, entirely around stablecoins. Stripe doesn't want you to know which chain the payment goes through; it only cares that the payment is completed at low cost and reliably. Every public chain that survives will become like this in the future—an invisible pipeline.

This also leads to what I believe is the most severe mispricing in the current crypto market.

The AI Token Graveyard

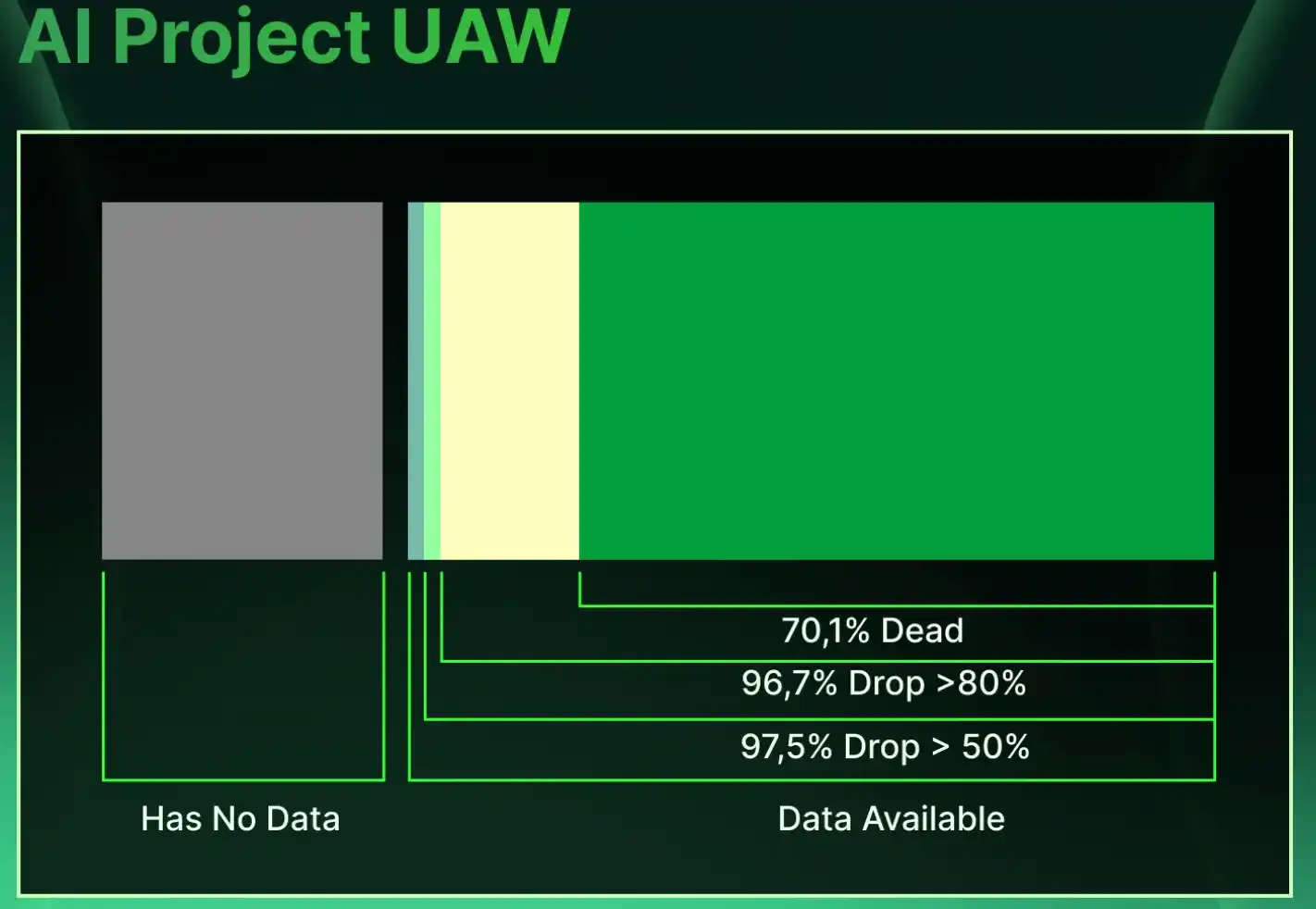

In 2025, the CoinGecko AI Agent Index fell from $13.5 billion to $3.5 billion. $10 billion in market cap evaporated. Virtuals, ai16z, and a long list of "autonomous agent platform" tokens that raised funds on the AI narrative plummeted, just as all narrative tokens are destined to do when there are no new buyers. The market is gradually realizing: These tokens have no actual utility for AI or AI agents.

The real value capture in the agent economy is on the other side of the track. USDC alone settled $18.3 trillion on-chain in 2025. All stablecoins combined reached about $33 trillion, comparable to Visa + Mastercard.

By January 2026, monthly stablecoin transaction volume exceeded $10 trillion. PayPal's PYUSD circulation increased from $1.2 billion to $3.8 billion in less than a year. Cloudflare even issued its own stablecoin. Visa launched a stablecoin settlement solution, reaching an annualized processing volume of $4.5 billion by mid-January.

On top of stablecoins is the protocol layer that makes the whole system work. Coinbase repurposed an idle HTTP status code, 402, into x402, a lightweight protocol for agents to pay each other. By December, x402 had processed over 100 million agent payments, averaging 20 cents each, with a daily transaction volume of about $30,000. It sounds pitifully small, but this is exactly how all the payment rails you know started in their first six months, followed by explosive growth. Stripe tested x402 on Base in February, Mastercard piloted agent payments with DBS and UOB in Singapore, and Google Cloud added x402 to its agent payment protocol.

These real, ongoing, mainnet-running transaction activities have hardly translated to the AI Agent Token Index. Admittedly, a few tokens related to x402 saw slight increases, but the overall index remained almost unmoved. Because the market is completely mispriced. It is still betting on which agent will win, just like betting on which dogecoin mascot was cuter back in the day. But the real trade is to hold the infrastructure that every agent must use, regardless of which agent ultimately survives or dies. And right now, that infrastructure is stablecoins.

The Cracks in This Logic

To be honest, I'll also tell you where this logic might fail; otherwise, I'm just selling another watered-down AI agent narrative.

The flaw in all of this lies in liability. Imagine a scenario: Felix signs a contract with another agent, transfers a million dollars, and the counterparty defaults. Who do you sue? Felix is not a legal entity; you can't sue Felix. Nat did not authorize this payment, might not even know what happened, and even if he wanted to, he might not be able to reconstruct Felix's decision-making at the time.

The platform running Felix also cannot provide compensation for a system whose behavior no one fully understands. Insurance companies are already pulling back, with professional liability insurance quietly classifying agent errors as "systemic software drift," effectively refusing coverage.

In today's legal terms, most enterprise AI agreements cap supplier liability at 12 months of SaaS fees. This means that in the event of a catastrophic incident, you can only recover up to a year's subscription fee. And the average cost of a single data breach in the US in 2025 was $10.22 million. There is a huge gap between the actual risk and the contractually covered amount, and currently, no one knows who should bear it.

Until someone solves the problem of who pays when an agent messes up, all founderless companies will still need a human name on the paperwork for legal protection. But even with this caveat, the macro trend still holds: Companies are gradually dissolving into software, and public chains are becoming the routing layer for software. And both of these layers will ultimately settle on stablecoins because, in the entire tech stack, only stablecoins can be independently held, used, earned, and understood by agents.

Where the Real Value Lies

If public chains are just vendors and agent tokens are basically a graveyard, then where is the real upside in this wave?

My answer is: The reputation layer and the orchestration layer. Someone needs to verify if Felix is solvent before other agents sign six-figure contracts with it. Someone needs to assess agent default risk at machine speed, like Moody's rates bonds. Someone needs to route payroll across three chains, with the sender and receiver completely unaware of which chain is used. Any startup that emerges in this space will be worth more than the sum of all issued AI tokens.

And this is the fact no one wants to hear: The infrastructure that truly wins in the agent economy will look boring. It will be like plumbing, with no token issuance狂欢 (carnival), and no airdrop farming hype.

A quote from Dragonfly's Haseeb Qureshi has been echoing in my mind: Crypto was never built for humans. He is right. Humans were never the target users. Every retail investor complaining about seed phrases, gas fees, and wallet experience is not wrong. The product isn't for them because it was never designed for them; it was built for the era to come.

The era to come is one of software with wallets, real customers, and real revenue. This state has existed for about two years now; somewhere, as you read this, they are issuing invoices and spending stablecoins. And while this is happening, the market is still arguing: Which public chain will win in AI, and which agent token will go up 100x.

Meanwhile, one stablecoin processed about $18.3 trillion in transactions last year, and almost no one in crypto paid attention. The true AI token is USDC; everything else is just for show.