Author: Claude, Shenchao TechFlow

Shenchao Intro: As the Nasdaq continues to hit record highs and Nvidia's market cap approaches $5.3 trillion, Michael Burry, the hedge fund manager who famously shorted the subprime mortgage market during the 2008 financial crisis and became the real-life subject of the movie "The Big Short," is doubling down on his contrarian bets.

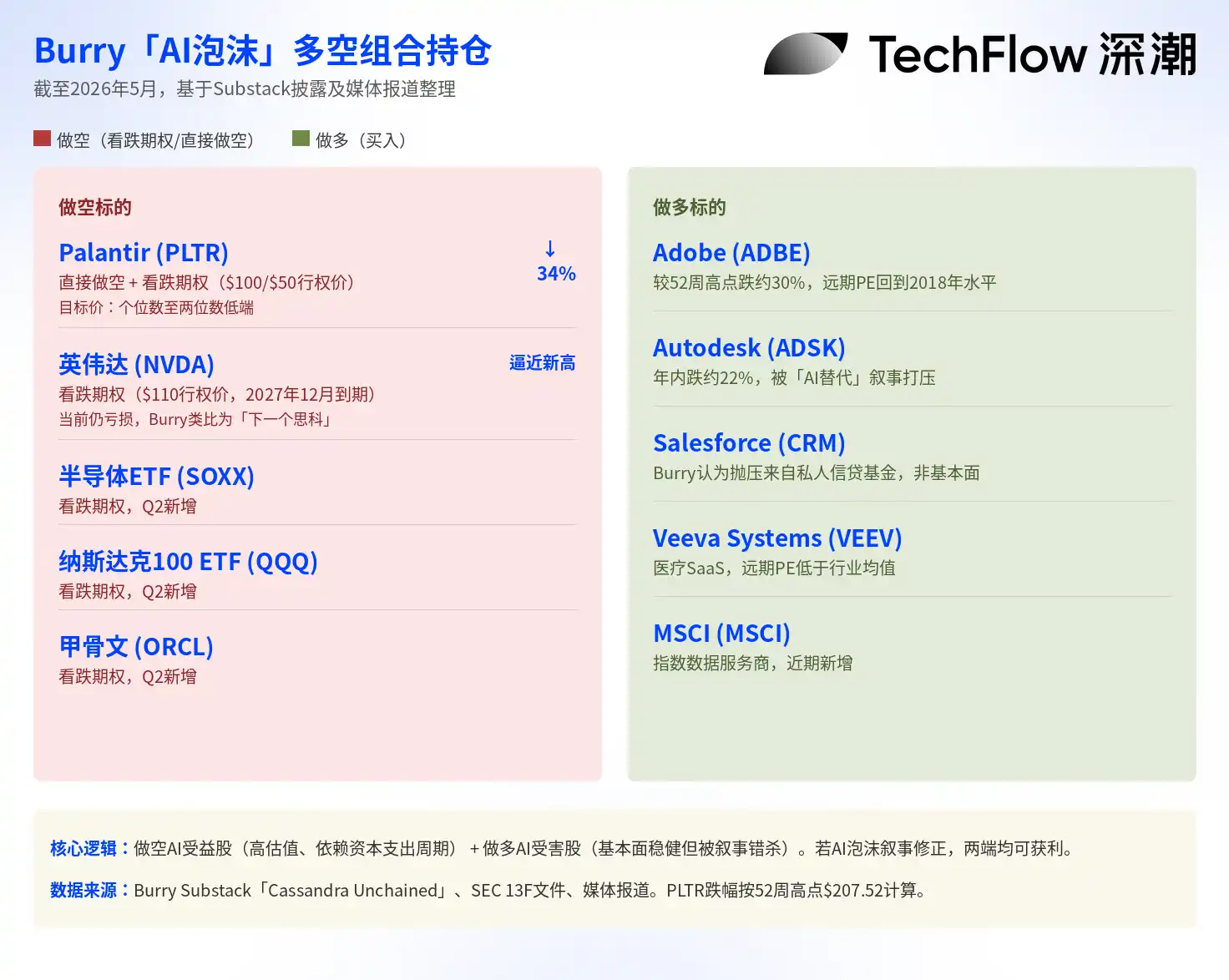

He is not only maintaining his bearish bets on Nvidia and Palantir but also expanding his short positions to include a semiconductor ETF and Nasdaq ETF. Simultaneously, he is buying traditional software stocks that have been battered by the AI narrative, constructing a complete portfolio betting on the "AI bubble repricing."

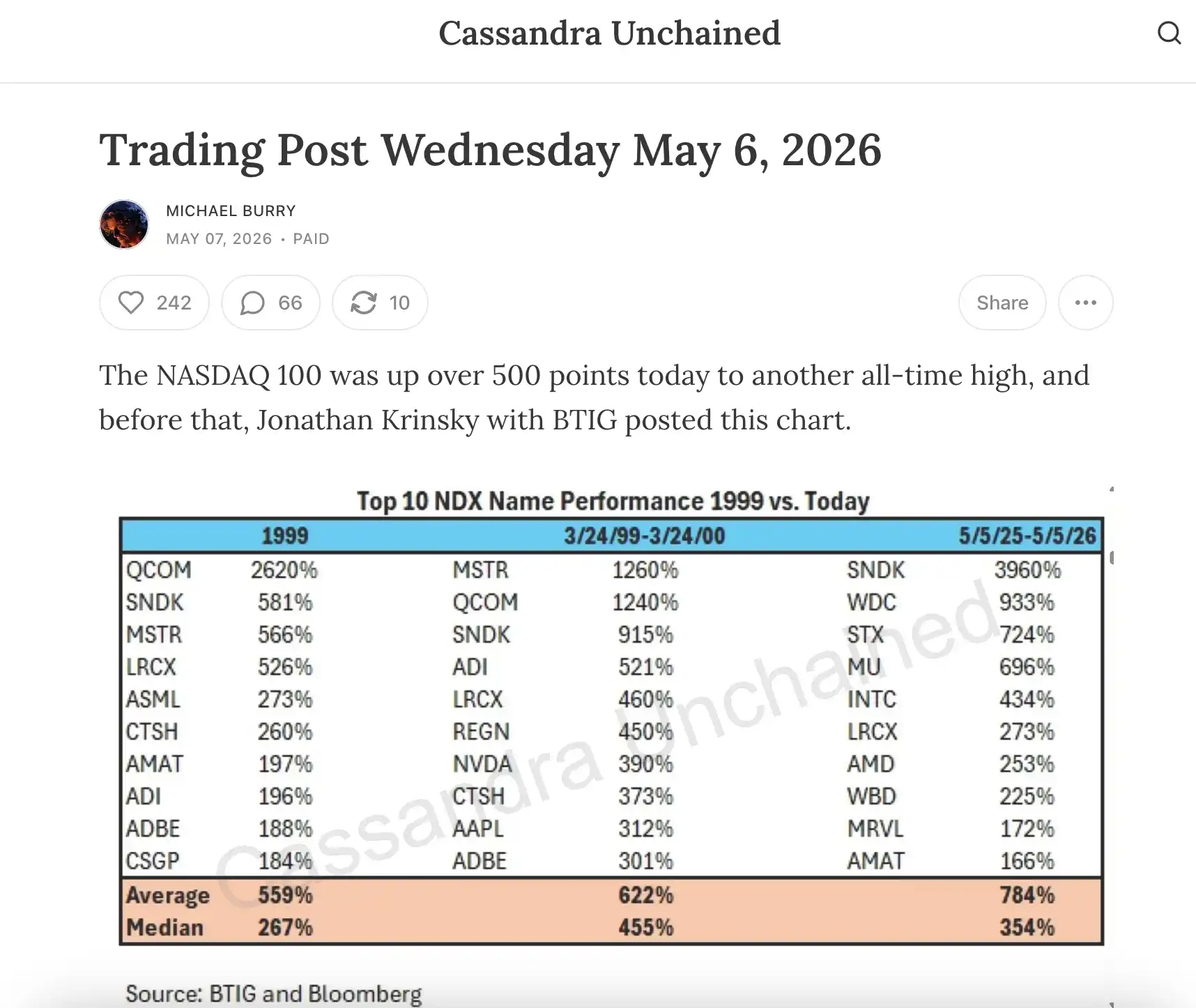

The Nasdaq Index hit consecutive all-time highs this week, closing at approximately 26,247 points on May 8th, with the S&P 500 also reaching a record the same day. The Philadelphia Semiconductor Index has risen about 55% since the second quarter began, and Nvidia's stock price neared its record high of $217.80, with its market cap exceeding $5.2 trillion. The AI-driven tech stock frenzy is at its most feverish stage.

Yet, at the moment of peak market euphoria, an investor known for his contrarian bets is heavily wagering in the opposite direction.

According to a Foreign Policy Journal report on May 7th, Michael Burry, the hedge fund manager whose prediction of the 2008 subprime crisis was adapted into the film "The Big Short," disclosed his latest portfolio adjustments this week in his Substack column "Cassandra Unchained":

He not only maintains his put options on Nvidia and Palantir but also added a direct short position on Palantir and expanded his bearish bets on the semiconductor ETF (SOXX), Nasdaq 100 ETF (QQQ), and Oracle.

At the same time, he began buying a batch of traditional software companies marginalized by the AI boom, such as Adobe, Autodesk, Salesforce, and Veeva Systems, on the grounds that their stock price declines stem from panic selling rather than fundamental deterioration.

Thus, a complete Big Short-style hedge portfolio has emerged, with the core logic being shorting AI beneficiaries and going long on AI victims.

Starting from the $1.1 Billion Bet Last November

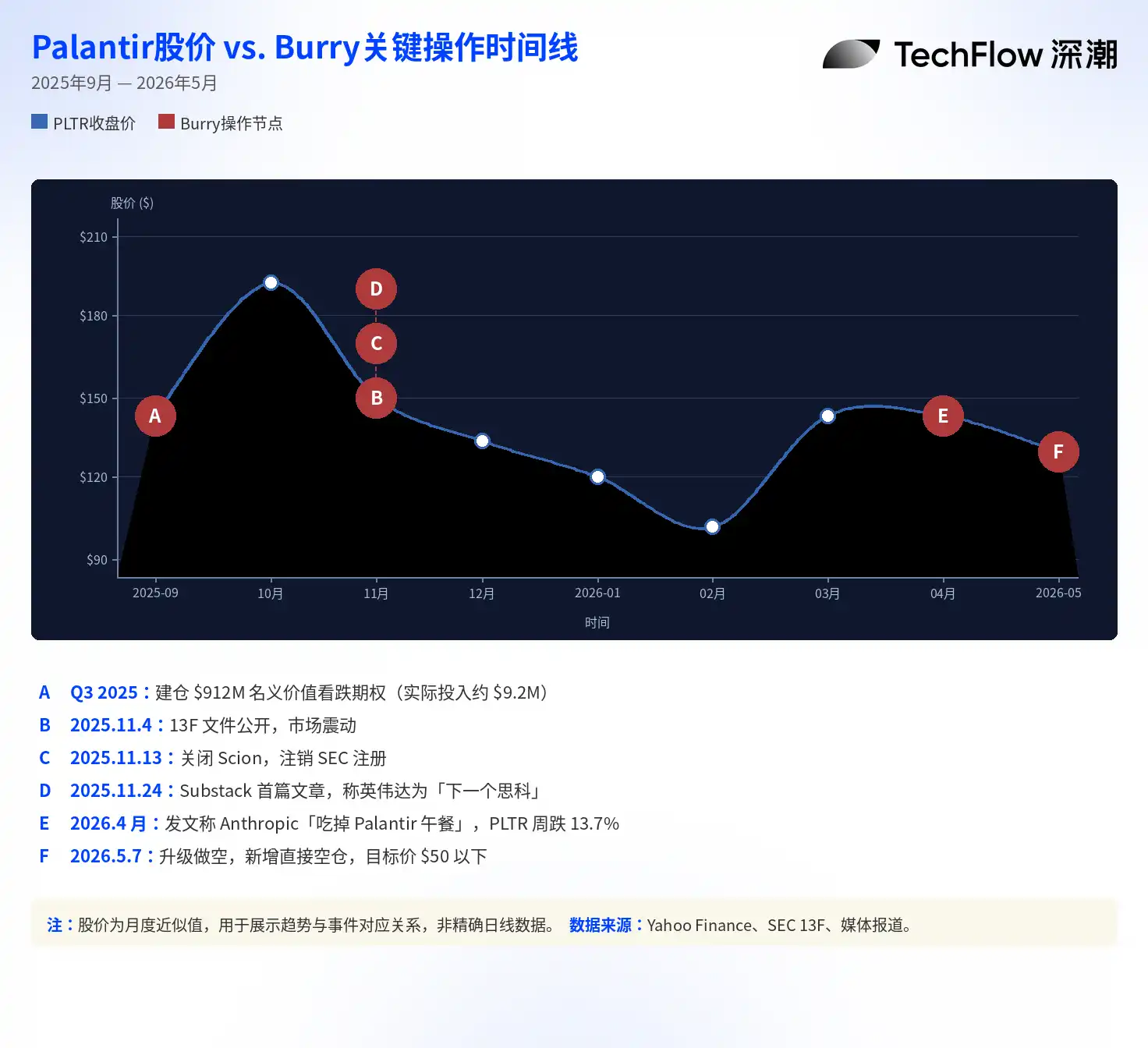

Burry's shorting of the AI sector began in the third quarter of 2025.

At that time, the 13F filing of his hedge fund Scion Asset Management showed he had purchased put options on Palantir with a notional value of approximately $912 million and put options on Nvidia with a notional value of about $187 million. The news, disclosed last November, sent shockwaves through the market, putting pressure on Palantir and Nvidia's stock prices.

However, Burry later clarified on platform X that his actual capital outlay was about $9.2 million, not the widely reported $912 million—the latter being the notional value of the option contracts, a difference of nearly a hundredfold. This detail is crucial: the notional value in 13F filings is often misinterpreted as the actual capital invested, thereby exaggerating the scale of the trade.

Soon after the disclosure, Burry announced the closure of Scion Asset Management and the deregistration from the SEC, ending his career of managing external capital.

He then transitioned to being a personal investor and started a column named "Cassandra Unchained" on Substack (Cassandra being the Greek prophetess who foretold the truth but was never believed), where he continues to publish market analyses.

The Palantir Short Is Already Profitable, Burry Says "Not Done Falling"

Judging by the trade results, Burry's Palantir bet is currently profitable. Palantir's stock price has fallen from around $161 when he entered to the current approximately $137, down about 34% from its 52-week high of $207. Even though the company just released strong Q1 2026 earnings (revenue up 85% year-over-year), its stock price actually fell following the report.

Burry has not taken profits from this. According to his Substack disclosure, he currently holds put options expiring in December 2026 with a $100 strike price, and put options expiring in June 2027 with a $50 strike price, indicating he expects Palantir to fall more than 60% from current levels within the next year. He explicitly stated in a post that Palantir's fair valuation is merely in the "single digits to low double digits."

In April this year, Burry posted on Substack stating that Anthropic is "eating Palantir's lunch," pointing out that this AI safety company's revenue growth has exceeded a $300 billion annualized rate, and its more user-friendly, lower-cost AI integration tools are replacing Palantir's complex enterprise deployment solutions. Following the post, Palantir's stock price fell 13.7% within a week. Burry later deleted the post. Wedbush analyst Dan Ives dismissed the view as "fictional narrative," and Palantir CEO Alex Karp had previously publicly stated he "couldn't understand" Burry's short position.

The Nvidia Short Is Still Losing, But Burry Insists "AI Is a Bubble"

In contrast to the victory on Palantir, Burry's situation with Nvidia is completely different.

Nvidia's stock price closed at around $215 on May 8th, nearing its record high of $217.80, with a market cap of approximately $5.3 trillion. It is reported that Burry's held Nvidia put options have a strike price of $110 and expire in December 2027, currently in a deep loss position. However, he has not reduced the position; instead, he added to it in his recent portfolio adjustments.

The core logic behind Burry's short on Nvidia is "overbuilding of AI infrastructure." In his first Substack article last November, he compared the current AI investment frenzy to the late 1990s dot-com bubble, likening Nvidia to Cisco from that era. Cisco's stock rose 3,800% between 1995 and 2000, briefly becoming the world's most valuable company before plummeting over 80% after the dot-com bubble burst.

Burry's key arguments include: Hyperscale customers like Microsoft, Google, Meta, Amazon, and Oracle are extending the depreciation period of GPUs to flatter their financial statements. According to his estimates, these accounting practices will cumulatively understate approximately $176 billion in depreciation expenses between 2026 and 2028, artificially inflating profits across the industry. Furthermore, he believes the massive capital expenditure on current AI infrastructure is based on overly optimistic demand forecasts, mirroring the situation when telecom companies frantically laid fiber optic cables around 2000.

This view prompted a direct rebuttal from Nvidia. According to CNBC, Nvidia privately distributed a seven-page memo to Wall Street sell-side analysts, addressing Burry's allegations point by point, specifically citing Burry's posts on platform X as sources of information that needed refuting. Nvidia stated in the memo that its customers set GPU depreciation at four to six years based on actual useful life, and early products (like the A100 released in 2020) still maintain high utilization rates. Burry responded, "I am not saying Nvidia is Enron," but stood by his analysis.

Going Long on Software Stocks Pressured by AI: A Complete Bubble Hedge Portfolio

The most notable aspect of Burry's portfolio adjustments may not be the shorting itself, but rather his long positions.

He recently purchased shares of Adobe, Autodesk, Salesforce, Veeva Systems, and MSCI, among others. The common characteristic of these companies is: their business fundamentals remain solid, but their stock prices have plummeted due to the market narrative of "being disrupted by AI" and forced selling by private credit funds.

Adobe is currently down about 30% from its 52-week high, Autodesk has fallen about 22% year-to-date, and both stocks' forward P/E ratios have retreated to levels seen in 2018-2019.

Burry explained on Substack that he "does not believe the technical selling pressure from private credit and software debt is sufficient to impact these stocks in the long run." In other words, he believes the market has excessively punished companies labeled "AI losers" while excessively rewarding those labeled "AI winners"—and he is betting on the correction of this mispricing.

Looking at both the short and long sides together, Burry has constructed a classic long-short hedge portfolio: If the AI bubble narrative bursts, highly-valued beneficiaries like Nvidia and Palantir will be the first to suffer, while mispriced traditional software stocks may see valuation recovery. Even if the overall market declines, this structure could potentially achieve positive returns.

In the letter to investors when he closed Scion, Burry admitted, "My judgment on the value of securities has been out of sync with the market for quite some time." This statement was both self-reflection and his typical declaration.

At the peak of the AI frenzy, he has chosen to stand on the opposite side of the crowd.