Part I: AI Sector Races Forward in H1, Funding Skyrockets

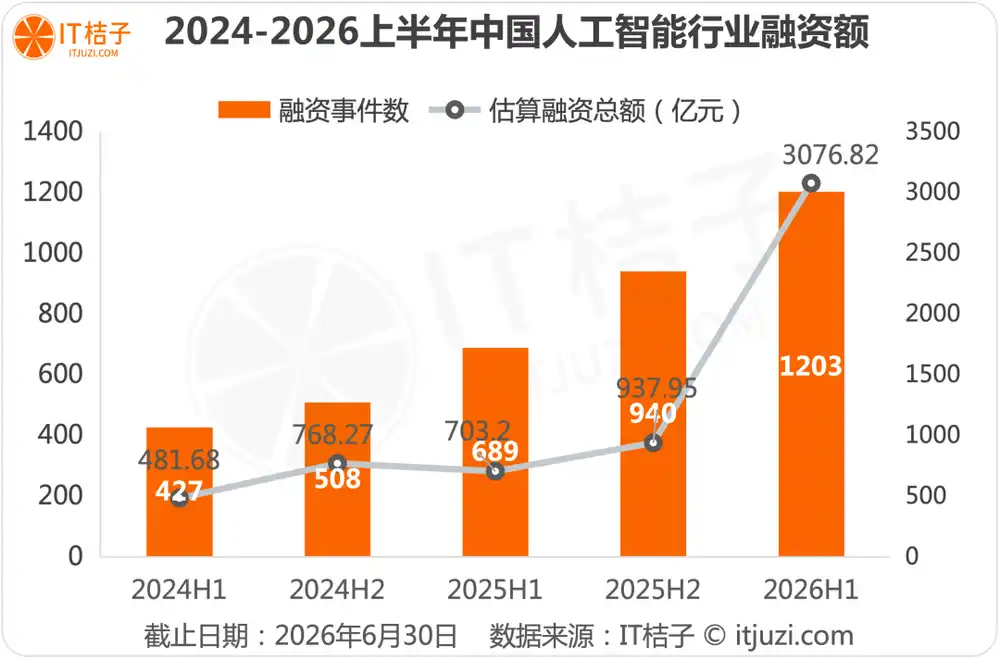

From January to June 2026, data from ITJuzi shows that equity financing in China's AI sector exhibited the core characteristics of "high total volume growth and a significant surge in funding amounts." Capital continues to increase its investment intensity in AI, with the funding scale for just six months already far exceeding the full-year level of 2025.

Data Statement:

1. Data filtering criteria: entries labeled "Artificial Intelligence" in the ITJuzi database's "Event Library," excluding non-AI industry entries.

2. Statistics scope limited to equity financing events in the primary market, excluding company listings (IPOs), post-IPO refinancing, M&A transactions, etc.

ITJuzi data shows that in the first half of 2026, there were 1,203 financing events in the AI sector, with total funding exceeding 300 billion yuan, far surpassing the full year of 2025. This reflects a sustained enhancement of capital's investment confidence in the AI sector. The AI industry has fully transitioned from the technology verification phase into the explosive period of large-scale implementation.

The funding pace in the AI sector during H1 2026 remained high from March onwards. Domestic AI funding scale consistently stayed above 40 billion yuan in March, April, and May. June saw explosive growth, with single-month total funding exceeding 100 billion yuan, primarily driven by the completion of DeepSeek's 51 billion yuan first-round financing, continuously pushing the overall funding scale of the sector higher.

The geographical pattern of AI sector financing in H1 2026 showed a landscape of "absolute leadership by Beijing, Hangzhou, Shanghai, and Shenzhen, significant agglomeration effects in the Yangtze River Delta region, and accelerated follow-up by new first-tier cities," highlighting prominent features of industrial cluster development.

In the AI financing landscape of the first half of the year, Beijing, Shanghai, Hangzhou, and Shenzhen absolutely led the way, contributing 73.89% of the total financing transaction count and monopolizing 86% of the funding scale, becoming the absolute core of China's AI financing.

Among them, Beijing, with 321 financing events and total financing of 95.517 billion yuan, ranked first nationally, serving as the absolute core of domestic AI sector financing. Hangzhou, benefiting from the rise of Deepseek and its first-round subscription exceeding 50 billion yuan, saw its funding amount surpass Shanghai and Shenzhen to rank second nationally, becoming the absolute leader among new first-tier cities.

Shanghai had 211 AI financing events with total financing of 59.570 billion yuan in H1, while Shenzhen had 215 events with total financing of 35.943 billion yuan. Although their financing volumes were similar, Shanghai's AI companies demonstrated stronger overall capital attraction ability, reflecting higher valuation midpoints for Shanghai AI companies and larger bets per deal by institutions.

Suzhou, with 19.022 billion yuan, ranked 5th nationally, becoming the third pillar in the Yangtze River Delta. Momenta's cornerstone round of 2.9 billion HKD and Pre-IPO round of 1 billion USD contributed approximately 9.7 billion yuan, accounting for over half of Suzhou's H1 AI financing amount.

In addition to Yangtze River Delta cities like Hangzhou, Shanghai, Suzhou, Wuxi, and Nanjing, new first-tier cities such as Hefei, Chengdu, Guangzhou, Xi'an, and Wuhan also saw AI projects securing financing. Some cities achieved zero breakthroughs in financing events, reflecting the continuous expansion of the AI industry's radiation scope and second-tier cities accelerating their AI sector layout through policy support and industrial spillover absorption.

Part II: Funding Scale Across AI Sub-sectors

Since the artificial intelligence industry covers a wide range, relying solely on a conceptual term cannot reveal its full picture. Therefore, we conducted a broader statistical analysis of sub-fields.

From the distribution characteristics of sub-sectors: In terms of total funding distribution, large models dominate overwhelmingly, taking over half of the total sector funds.

The large model sub-sector, with 159.853 billion yuan in total financing, became the absolute core technical foundation of the AI sector. Top projects frequently secured single rounds of tens of billions in financing, showing the strongest Matthew effect for capital. It is the first most heavily invested sub-sector in the primary market.

Additionally, in H1 2026, the AI infrastructure layer (including computing power, AI chips, training frameworks) raised a total of 72.568 billion yuan. These are capital-intensive sub-sectors with frequent large-scale financing. The AI technology layer, leaning towards simulation and spatial algorithms, had lower numbers of financing events and amounts compared to the infrastructure layer, often financing in sync with large model and embodied intelligence companies.

These two major sub-sectors together accounted for 258 events and combined financing of 106.783 billion yuan, constituting 18.00% of the total summarized funds. They represent the core investment direction for the AI industry's technical foundation, apart from large models.

The AI+Embodied Intelligence sub-sector is the second growth driver, with total financing reaching 90.644 billion yuan. It is the core hardware carrier sub-sector for AI technology implementation, with 312 financing events, making it the sub-sector with the highest number of financing events and the highest project activity level.

The AIGC application sub-sector raised a total of 59.605 billion yuan in six months, representing the most mature sub-sector for AI technology commercialization, with the highest capital recognition of its commercial value.

In terms of financing event distribution, the AI+Embodied Intelligence sub-sector had 312 financing events, accounting for 26.02% of all sector events. It is the most densely populated sub-sector with projects, covering all stages from early startups to growth-stage leaders, showing the strongest industry innovation vitality.

From the perspective of single-project financing capability, large models and AIGC are most prominent. The top three sub-sectors with the highest average financing amount per event are: AIGC (710 million yuan), Large Models (704 million yuan), both far exceeding the sector average. This reflects that capital is willing to offer extremely high valuation premiums and large-scale financial support for top projects in these three sub-sectors, which are the core targets of capital's heavy investment.

Part III: Capital's Core Betting Rhythm

&

In-depth Analysis Matching Different AI Companies' Financing Development Stages

Capital allocation in the AI sector in H1 2026 presented a clear rhythm: "heavy investment in growth stage, anchor in maturity stage, early-stage incubation." The financing scale, number of events, and capital preferences differed significantly across these three investment stages.

The core betting logic of capital can be clearly seen from the key data:

Companies in the ultra-early stage (Seed, Angel, Pre-A rounds) are the core source of technological innovation in the AI sector. They contributed 626 events, over half of the total, but the average financing amount per event was only 73 million yuan. The core logic of early-stage investment is "casting a wide net, early positioning, betting on the future"—locking in early-stage projects with innovative potential through small, high-frequency investments.

Growth-stage AI companies (Series A, A+, B, B+ rounds) were the core battlefield for capital deployment in the AI sector in H1 2026. Companies at this stage have completed technology validation and possess initial product implementation capabilities and commercialization potential. Together, they contributed 49.40% of the total financing amount, with an average financing amount per event of 380 million yuan.

Mature-stage AI companies are the anchor of the sector. Although they accounted for only 177 events, they contributed over 100 billion yuan in total financing, with the highest average financing amount per event reaching 624 million yuan. These mature-stage companies, which have formed industry leadership positions and possess stable profitability capabilities, often receive larger financial support.

To penetrate beyond the surface information of "funding amounts," we will break down the analysis into two stages—early stage and mid-to-late stage—and conduct an in-depth analysis of the companies with the highest financing amounts to answer a core question: What exactly is every penny of capital betting on?

1. Early Stage: The Source of Innovation and Incubation Pool for the Sector

According to ITJuzi statistics, the top 10 early-stage companies collectively secured 16.589 billion yuan, accounting for 36.7% of the total ultra-early stage financing. Who are the companies that can secure large-scale, even over 1 billion yuan, financing in the early stage?

Four Key Insights from the Early-Stage TOP10

Insight One: World Models become the "First Consensus" for early-stage investment.

Six companies in the world model direction collectively raised 9.7 billion yuan (58%). World models are seen as the "operating system" for embodied intelligence—whoever masters the world model masters the robot's ability to understand the physical world. The logic of early-stage VCs is to position themselves at the operating system level, which holds greater strategic value than competing at the application level.

Insight Two: Significant "Inflation" in Angel round financing amounts.

Four companies among the TOP10 completed financing exceeding 700 million yuan in their Seed or Angel rounds (Brag 2.1B, Wujie Power 1.9B, Inverse Matrix 900M, Daxiao 700M), which was unimaginable before 2024. This phenomenon indicates that the premium for founding teams' academic/industry backgrounds in the AI sector is extremely high. Top VCs are moving towards earlier stages to compete for scarce top-tier teams.

Insight Three: The spillover effect of the talent ecosystem from major companies is becoming evident.

Daxiao Robot, founded in 2025, is an embodied intelligence company incubated by SenseTime, launching the first domestically open-source and commercially applied "Kaiwu" World Model 3.0. Daxiao Robot's inclusion on the list represents a trend—AI talent and technology from major companies are diffusing outward through incubation/entrepreneurship, forming a "major company ecosystem" for startups.

Insight Four: None of the early-stage TOP10 are pure large model companies.

This is an extremely important signal—the early window for the large model sub-sector has essentially closed. Capital judges that the competitive landscape for foundational large models has preliminarily taken shape, and new early-stage large model projects are unlikely to receive support from top VCs. Capital is shifting towards the "downstream of large models"—world models, embodied brains, physical AGI.

2. Growth/Maturity Stage: Core Targets of Capital's Heavy Investment

Large-scale financing occurs frequently in both the growth and maturity stages, so they are considered together. According to ITJuzi statistics, the TOP20 companies collectively raised 156.5 billion yuan, accounting for over half of the total sector financing. So, who can attract concentrated capital bets?

Based on their focus areas, we categorize the TOP20 AI companies in mid-to-late stages into five major camps for analysis:

Camp One: The Big Three Large Models (Collectively 93.006 billion yuan, 59.4% of TOP20)

Deepseek, StepFun, and Kimi took the top three spots, each securing over 10 billion yuan in financing. Among them, DeepSeek obtained 51 billion yuan with just one Series A round, making it the largest financing event in the AI sector in H1 2026.

However, the financing logic of the big three differs significantly. DeepSeek's single 51 billion yuan round was completed at Series A, indicating extremely high valuation elasticity and capital trust. StepFun's intensive financing (four rounds in six months) reflects capital needs in the Pre-IPO冲刺冲刺 sprint stage, with a considerable portion of its 23 billion yuan likely allocated for final resource preparation before listing. Kimi's 18.9 billion yuan was completed in two relatively balanced rounds.

Camp Two: The "Seven Samurai" of Humanoid Robots (Collectively 28.226 billion yuan, 18.0% of TOP20)

Humanoid robots are the second major area, with the industry on the eve of large-scale implementation. Seven embodied intelligence companies—Independent Variable Robotics, ZhiPingFang, Qianxun Intelligence, Jijia Vision, Xinghai Tu, Galaxy General Robot, and Xingdong Jiyuan—each secured large-scale financing exceeding 2 billion yuan.

Moreover, their financing stages collectively entered Series B to strategic investment, indicating capital is no longer betting on technical routes but on who can achieve mass production first. Additionally, Independent Variable Robotics completed four rounds totaling 6.3 billion yuan in six months—an unusually intensive financing pace in the robotics sector—suggesting funds are rapidly concentrating towards it.

Camp Three: The "Three Musketeers" of AIGC Applications (Collectively 6.778 billion yuan, 4.3% of TOP20)

In the AIGC application sub-sector, ShengShu Technology, Sand.ai and LiblibAI, and Aishi Technology focus on the core scenario of multimodal video/image generation and have preliminarily achieved scaled commercialization of AIGC technology.

Compared to 2024 when most AIGC companies were in Angel/Series A stages, H1 2026 shows the AIGC sub-sector has clearly entered the commercialization verification phase. Notably, the financing amounts of the three companies are highly similar, without a clear "winner-takes-all" pattern—this reflects that the AIGC application layer is still in a "dividing the pie" rather than a "determining the winner" phase.

Camp Four: Autonomous Driving & Others (Collectively 25.893 billion yuan, 16.6% of TOP20)

Both Momenta and Kuwa Technology are in the Pre-IPO stage, reflecting that the autonomous driving sub-sector is entering an exit window. Huashen Zhiyao's 5.533 billion yuan represents the largest single financing in the AI drug discovery sub-sector, indicating that AI's commercial prospects in pharmaceutical R&D have been validated by capital's heavy investment. Sunrise's 4 billion yuan strategic investment represents the financing capability of AI chips under the logic of domestic substitution.

Part IV: Outlook for the Second Half of the Year

Looking at the AI industry from the midpoint of 2026, we predict the annual financing scale is highly likely to exceed 600 billion yuan, but the pace in the second half will be "high front, low back."

The H1 financing total of 307.682 billion yuan has already set a high base. According to seasonal patterns, financing is typically more active in H2, making it highly probable that the full year will exceed 600 billion yuan.

Additionally, the large model sub-sector will face its first round of "elimination matches."

In H1, the big three large models took 93 billion yuan. Furthermore, Zhipu and Minimax have entered the secondary market. The funding window for the remaining 200+ model companies is rapidly narrowing. We anticipate that the first cases of layoffs/transitions/M&A among large model startups will emerge in H2.

Companies that can survive will either have found clear differentiated scenarios (e.g., vertical models for AI drug discovery, AI programming, etc.) or secured strategic investments from industry giants. The window for pure "general-purpose large model" entrepreneurship has closed.

This article is from WeChat Official Account: ITJuzi , Author: Wu Meimei