Author: Connor Dempsey

Compiled by: Deep Tide TechFlow

Deep Tide Guide: Connor Dempsey is a seasoned professional in the crypto industry, having worked at Circle, Messari, and Coinbase Ventures. He currently leads marketing at Crossmint. In this short commentary, he presents a viewpoint: under the logic of "common prosperity," China is pushing AI companies to go public quickly at reasonable valuations, while their American counterparts won't IPO until late 2026, by which time their valuations could be 100 times higher than those of Chinese companies. The wave of AI IPOs will continue to drain market funds, putting short-term pressure on crypto, but 2026 could be a good year for early-stage investments.

Main Text:

A wave of IPOs from Chinese AI companies is coming and will last for 1-2 years.

Moreover, their valuations are more attractive than those of their American counterparts.

Disclaimer: The following content is based on a conversation I had with an old friend familiar with the Chinese market (the Chinese market is largely a black box to me).

China's Logic

China is building AI as fast as the U.S. But China has stronger control over the private sector, and they are concerned about the wealth gap.

The logic is this: AI is a winner-takes-all game. The longer companies stay private, the more wealth is concentrated in the hands of a few founders and investors.

Chinese policy pressures high-growth AI companies to go public earlier, allowing ordinary investors to share in the prosperity.

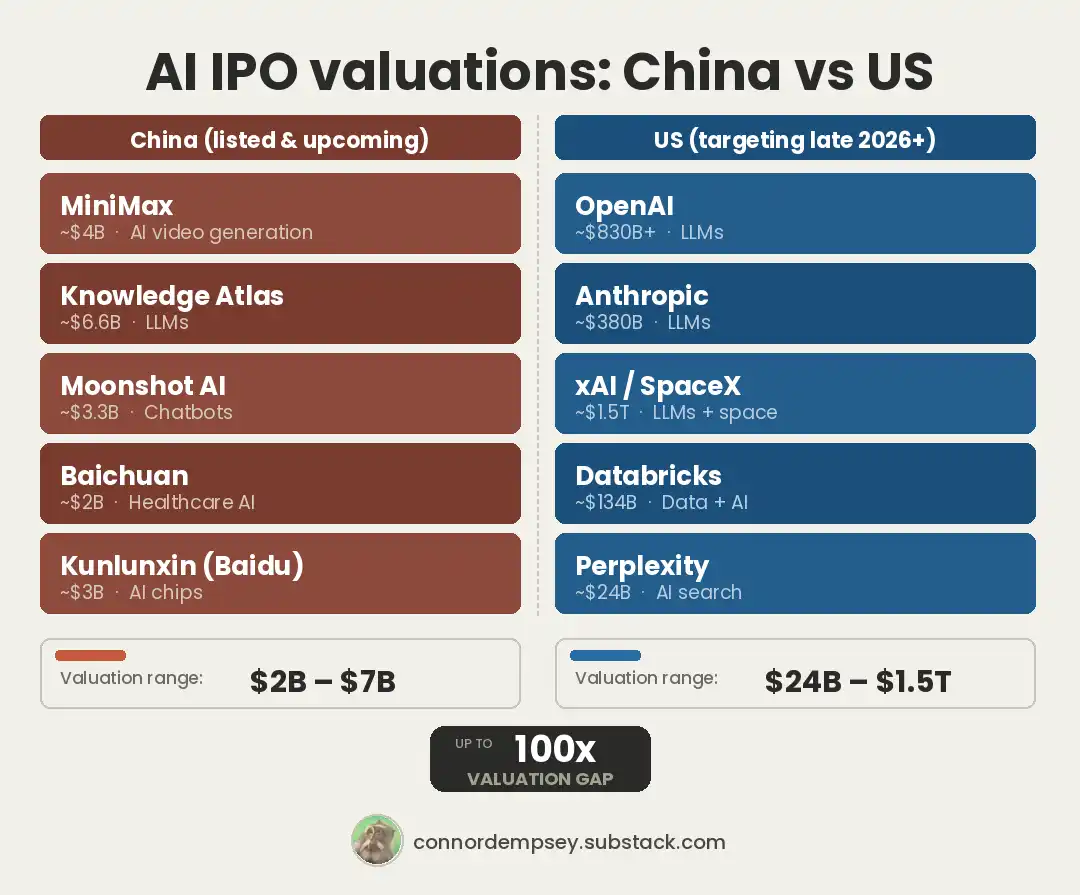

MiniMax (AI video generation) and Zhipu (China's OpenAI) have already gone public. Moon's Dark Side (chatbots), Baichuan Intelligence (medical AI), and Baidu's Kunlun Chip are in the queue, with IPO valuations ranging from $2 billion to $7 billion, which is reasonable. DeepSeek is the only exception, claiming it will continue to raise private funding.

As a Westerner, I'm not taking China's side, but this logic makes sense. U.S. AI giants won't distribute equivalent levels of wealth to the public.

America's Pace

The U.S. also has a wave of AI IPOs coming, expected to start in late 2026 to early 2027. OpenAI, Anthropic, Databricks, Perplexity, and Elon Musk's xAI (merged with SpaceX) should go public within this window.

But by the time ordinary investors can buy in, the valuations of these companies could be 100 times higher than their Chinese counterparts.

OpenAI and Anthropic will likely be trillion-dollar companies at IPO. Databricks and xAI are already valued at over $100 billion.

AI is the Only Game in Town

No matter how it ultimately unfolds, the U.S.-China AI race will proceed at full speed and will likely suck the air out of every other tech sector, including crypto.

Why? Because AI is the most important technology of our lifetime. If you are a capital allocator, it's hard to look elsewhere right now. For example, if you have $1 million to deploy, you'll likely try to find a way to ride this AI wave.

As long as the AI IPO feast continues, crypto asset prices will likely remain under pressure.

Crypto venture capital has noticeably slowed down. I recently met an entrepreneur raising funds in the crypto space. His observation was: if you're not working on AI, most investors aren't interested.

The Silver Lining

Sentiment hitting the toilet and investors losing interest is nothing new for crypto. For example, after the ICO bubble burst in 2018, most of the investing public was indifferent to crypto for a full two years.

But if you were an early-stage investor during that time, you did very well. Seed rounds for Solana, Compound, and Uniswap were all done then. Circle's USDC (2018) was also built during that period.

I believe 2026 could be a similarly good year for those still deploying early-stage capital in crypto.

Meanwhile, U.S. crypto regulation is becoming clearer, and infrastructure for transforming financial markets through tokenization is being built.

Protocols like Hyperliquid are already spilling over into traditional markets, offering 24/7 crude oil futures trading when traditional markets are closed on weekends (see Syncracy's "The Great Perpification").

Although there are fewer crypto founders now, new and interesting companies are still launching. For example, Ryan Yi, with four years of venture capital and corporate development experience at Coinbase, founded Onchain Group, essentially an investment bank built for the token economy. Think traditional M&A, but with tokens as the assets and clients being the largest protocols in crypto.

AI is Crypto's Variable

While AI is sucking the air out of the room at the investment level, it will ultimately become the rocket fuel for crypto's utility.

Crypto has always had a user experience problem. Combining an AI front-end with a crypto back-end will suddenly make using crypto as easy as using Claude or ChatGPT. This will ultimately become a massive onboarding point for crypto assets and protocols.

AI Agents are also poised to become crypto's largest user base. Agent-to-agent commerce—millions of AI Agents transacting autonomously without human involvement—is one of the strongest use cases for stablecoins and blockchains. When you need millions of Agents creating wallets and transacting for fractions of a cent, traditional card networks would break. Crypto won't.

I bet the fusion of crypto and AI will be a big deal at maturity. It will also be one of the most remarkable phenomena in the history of this industry.

~CD