Author: Yokiiiya Stablehunter

Five months ago, I wrote an article titled Stripe | The AWS of the Financial World: Why It Becomes the Biggest Winner in the AI + Stablecoin Era, where I wrote that 'Money will run on Stripe.' Stripe is not just building a better payment button; it's transforming financial capabilities like receiving payments, making payments, issuing cards, fund accounts, tax, and invoicing into infrastructure that developers can call, just like cloud services.

But after the emergence of Open USD, we see that Stripe might want to prove more than just 'money will run on Stripe.' Rather:

Money will not only run through Stripe.

Money may settle on a network Stripe helped define.

I. OUSD is a Key Step for Stripe to Become a Money Movement Network

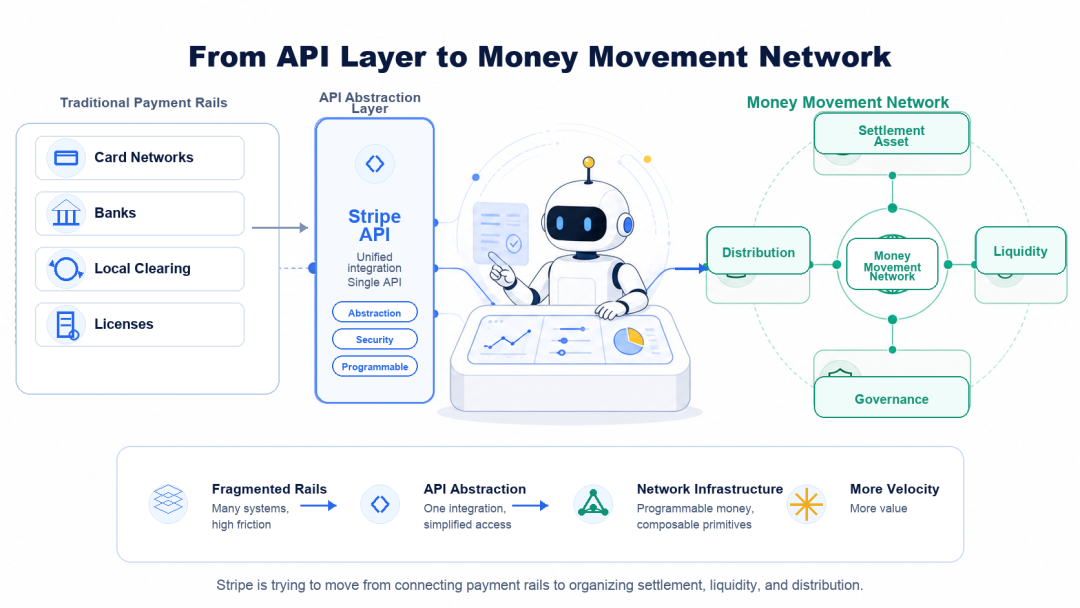

The significance of OUSD lies not in it being just another stablecoin, but in providing Stripe with a bigger story: from a payments API company to a money movement network.

It's unlikely to replace USDC in the short term, nor can it bypass all traditional financial systems. However, it gives Stripe the opportunity to not just connect payments, but to reorganize settlement, liquidity, and yield distribution. In the past, we often understood Stripe as a better payment gateway, but more accurately, Stripe is an aggregation layer built upon card networks, bank account systems, local clearing networks, acquiring/issuing licenses, and various traditional payment rails.

This is also its limitation.

What Stripe truly wants to break through is the strategic limitation of being merely 'the API layer on top of traditional payment networks.' If Stripe is just a better payments API, no matter how big it gets, it can easily be framed within comparison frameworks against Adyen, PayPal, Fiserv, Checkout.com, and acquirers. The market would look at its processed volume, take rate, gross margin resilience, potential increases in card network costs, and regulatory and local licensing constraints on expansion.

This would still be a very good company, but not yet a truly financial network. The significance of OUSD is that it gives Stripe the chance to advance its story from 'we help merchants connect payment methods' to 'we participate in defining the next-generation commercial settlement network.'

The valuation logic for these two things is completely different. The former is software and payment aggregation; the latter is a network.

In the payment industry, the most valuable thing has never been just the API, but network effects. Visa and Mastercard are valuable not because they have prettier payment buttons, but because they organize a multi-sided network: issuing banks, acquiring banks, merchants, consumers, risk rules, dispute handling, and clearing paths all operate within the same rule-based system.

If Stripe wants to tell a bigger story than 'payments API,' it must answer one question: Is it possible for Stripe to not just connect others' networks, but to organize its own network? OUSD provides the narrative entry point for this. The appeal of OUSD to Stripe isn't whether it's just another dollar stablecoin, but that it simultaneously points to four things.

First, it gives Stripe the chance to own a default settlement asset.

In the past, Stripe helped merchants connect to Visa, Mastercard, ACH, local wallets, and bank transfers. In the future, if OUSD can become the default settlement asset for Stripe merchants, platforms, marketplaces, and AI agents, Stripe would no longer just be connecting others' networks; it would be organizing its own.

Second, it changes economic distribution.

In traditional payments, Stripe can collect processing fees, but underlying network fees, bank fees, card network fees, and some fund earnings go to others. If stablecoin reserve yields, mint/redeem, liquidity, wallets, cards, and on/off-ramps are all organized within the Stripe/Bridge system, Stripe has the opportunity to enter a deeper layer of economics.

Third, it provides a programmable money layer for agentic commerce.

If the underlying layer remains just credit cards and bank transfers, what agents can do will be constrained by authorization, risk management, settlement delays, cross-border costs, and reconciliation processes. Stablecoins can't solve all problems, but they are closer to a money rail that machines can call.

Fourth, it moves Stripe from a software company towards a network company.

If OUSD succeeds, the story Stripe can tell isn't just 'we make payments simpler,' but 'we are organizing the next-generation global commercial settlement network.' This is what truly matters. But we also need to look at it calmly.

For now, OUSD looks more like the narrative starting point for this ambition, not the already-completed infrastructure. A stablecoin network isn't announced into existence; it requires deep liquidity, stable and low-friction redemption, bank and regulatory acceptance, merchant willingness to hold or auto-settle, integration into enterprise ERP, treasury, and reconciliation systems, stable cross-chain and cross-region experiences, and governance that doesn't become a slow-moving consortium.

So, OUSD is not a USDC killer in the short term. It's more like Stripe asking the market a question: If future money flows no longer solely depend on traditional payment networks, then who will organize the new settlement assets, distribution networks, and economic distribution mechanisms?

II. What OUSD Actually Aims to Do: Not a USDC Killer, but Rewriting Stablecoin Profit Distribution

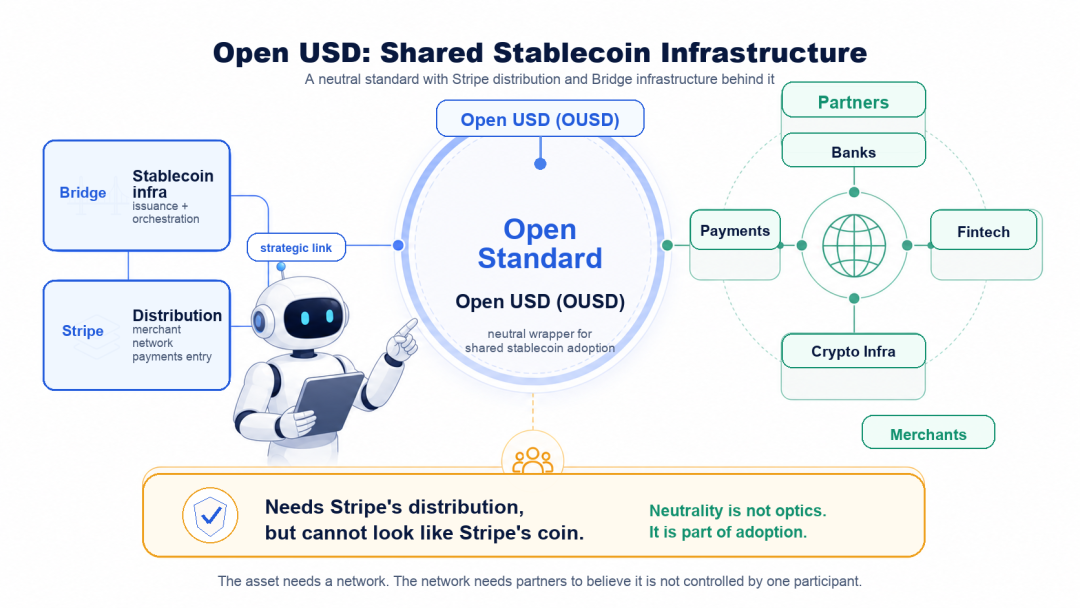

Open USD, abbreviated as OUSD, is a new dollar stablecoin announced by Open Standard on June 30, 2026. Its official definition is: a shared stablecoin for global financial activity.

It is not a 'private stablecoin' issued by Stripe alone. It is governed and operated by the independent company Open Standard, with participation from a group of payment companies, banks, fintechs, crypto infrastructure companies, and merchant platforms. The official participants listed include Stripe, Visa, Mastercard, BlackRock, BNY, Coinbase, Shopify, Bridge, Tempo, Privy, etc.

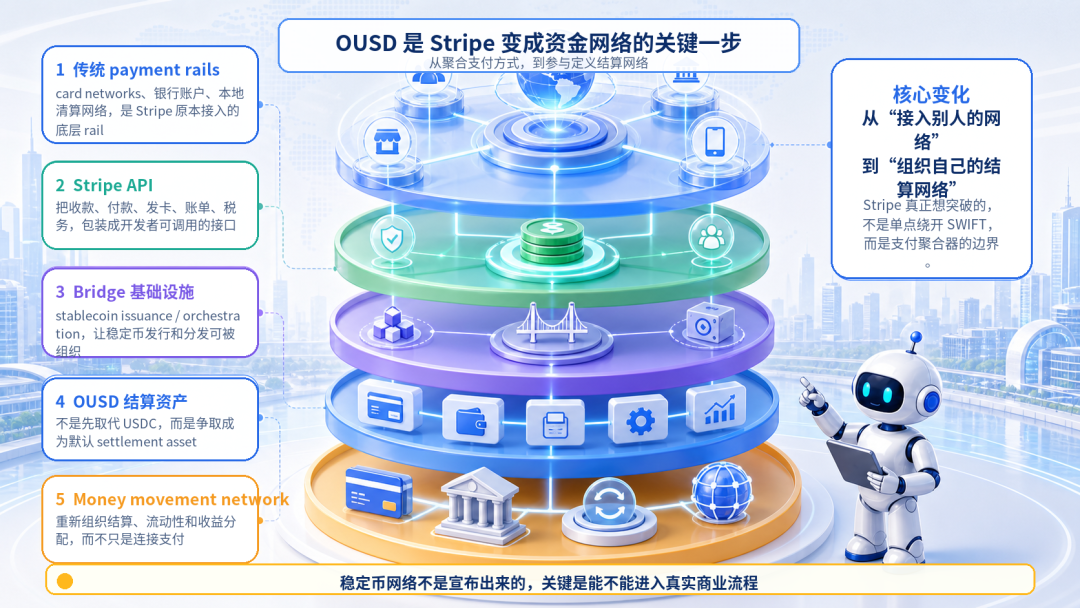

There's also a very interesting detail: OUSD was not officially launched directly by Stripe. It was announced by Open Standard, whose founding CEO is Zach Abrams. Zach Abrams is also the co-founder/CEO of Bridge, which has been acquired by Stripe.

So, from an organizational perspective, OUSD is not unrelated to Stripe. On the contrary, it clearly lies along the extended line of Stripe/Bridge's stablecoin strategy. But from a product and governance narrative perspective, it cannot be packaged as Stripe's own private stablecoin.

This is precisely what's subtle about OUSD: It needs the execution capability, payment network understanding, and future distribution power of Stripe and Bridge, but it must also present itself through the independent entity Open Standard as a stablecoin network with multi-party participation, co-governance, and shared economic benefits.

In other words, it needs Stripe's strength, but cannot appear to be just Stripe's coin. The design focus of OUSD has three points.

First, minting and redeeming incur no fees, and there are no artificially set caps on scale.

Second, the yield generated by OUSD's reserve assets, after deducting a small portion for management fees, will be distributed to partners who drive adoption and distribution.

Third, it adopts collaborative governance. The board of Open Standard consists of OUSD partners. The official vision is for it not to be a private network of a single company, but a stablecoin infrastructure co-shaped by participants. OUSD is not just another dollar stablecoin; it's attempting to answer a more commercial question:

If stablecoins are to become the infrastructure for global money flows, should the companies that use, distribute, and create transaction scenarios also participate in governance and profit distribution?

So, what is OUSD actually aiming to do? I don't think it's a USDC killer in the short term.

USDC's first-mover advantage is very real. It has liquidity, exchange and DeFi use cases, institutional trust, a compliance brand, and a vast number of completed integrations. Stablecoins are not something you can just migrate by changing the ticker; they involve redemption trust, liquidity depth, counterparty acceptance, and operational inertia.

Shortly after OUSD's announcement, Circle CEO Jeremy Allaire responded to the competitive concerns OUSD raised. His core message wasn't 'anyone can issue a stablecoin,' but rather the opposite: stablecoins are a long-term, accumulated platform and network effects business.

He emphasized that USDC's moat comes mainly from three things: developer and application integration, global liquidity, and regulatory and financial system integration.

In Circle's official Q1 2026 data, USDC's circulation was $77 billion, and quarterly on-chain transaction volume was $21.5 trillion. This number may not fully reflect real commercial payment penetration, but it's enough to illustrate one thing: USDC is not just a ticker that can be easily replaced; it's already an operational stablecoin network.

That's why framing OUSD as a 'USDC killer' would be an oversimplification. The truly interesting part about OUSD is not that it will immediately replace anyone, but that it has chosen another path: Instead of first competing for transaction liquidity in the crypto-native world, it is cutting in from enterprise payments, platform settlement, merchant distribution, and reserve yield distribution.

In the existing stablecoin model, many users are actually just distributors or channels. The more a stablecoin is used, the more the issuer benefits from the reserve yield. Yet, payment companies, platforms, merchants, wallets, banks, and fintechs that contribute distribution and use cases may not fully participate in the underlying economics.

This is what OUSD wants to change. It attempts to convince enterprises: you're not just using a stablecoin; you can also participate in the governance and economic distribution of this stablecoin network.

Therefore, what OUSD is challenging is not just USDC's market share. It's challenging a more fundamental issue in the stablecoin industry: Who contributes to the use cases of a stablecoin, and who should share how much of its economic benefits?

From this perspective, USDC's advantages remain strong, but what OUSD proposes is not a simple replacement relationship, but a new model for profit distribution. This also explains why it emphasizes open, neutral governance, and shared economics.

'Open' is to lower the psychological barrier for enterprise adoption and exit. 'Neutral governance' is to make participants believe this isn't a private stablecoin of a single company. 'Shared economics' is to let companies that truly bring distribution and transaction volume participate in the distribution of reserve yield and network value.

This is not a purely technical issue; it's a business organization issue. Of course, this path is also harder. The larger the alliance, the higher the coordination costs. The more participants, the more complex the governance. The more a stablecoin aims to become public infrastructure, the more it must address questions of responsibility, benefit distribution, liability, and final decision-making.

Allaire's rebuttal to 'everyone sharing profits' also touches on this exact contradiction: If all revenue is distributed out, who will continuously invest in infrastructure? This question isn't just defensive rhetoric from Circle. It's a question OUSD must answer in the future.

Circle's logic is: a strong issuer needs to retain sufficient profit to continuously build compliance, liquidity, redemption, and global financial infrastructure.

OUSD's logic is: If stablecoins are to become shared infrastructure, then participants contributing distribution, use cases, and transaction volume should also share more of the reserve economics and governance rights.

So, this isn't simple 'who is cheaper' competition. It's a competition between two ways of organizing stablecoins. OUSD is not a USDC killer in the short term.

It's more like a business counter-question to the USDC model: If stablecoins are truly to become the next-generation global payment infrastructure, should they be dominated by a strong issuer, or co-governed by a group of commercial networks that genuinely contribute traffic, use cases, and trust?

III. What Stripe Needs Isn't Just Growth, But a Bigger Corporate Narrative

Stripe is already a very large company, serving a vast number of internet companies, SaaS, platform businesses, marketplaces, and emerging AI companies globally. Its products have long gone beyond just a payment button, covering a whole suite of financial infrastructure including payments reception, disbursements, invoicing, tax, risk management, card issuance, fund accounts, and business registration.

But the problem is, capital markets don't just ask how big a company is. They also ask: What kind of company is this? This is a question Stripe has always needed to answer.

If Stripe is understood as a payment company, it gets valued within the framework of payment companies. The market will look at its transaction processing volume, take rate, gross margin, card network costs, competitive intensity, regulatory pressure, and whether it can sustain high growth in the long term.

If Stripe is understood as a software company, it faces another issue: its revenue structure includes a large portion driven by payment volume, unlike pure SaaS with very clear subscription revenue and software margin models.

Therefore, Stripe's most imaginative narrative has never been 'we are a payment company,' nor simply 'we are a SaaS company.'

Rather: We are the financial infrastructure for the internet economy. Five months ago, when I wrote it was 'the AWS of the financial world,' that's what I meant.

The core of AWS isn't that it has many APIs, but that businesses place their computing, storage, databases, networking, security, and deployment processes on it. It provides not a point solution, but the default runtime environment.

What Stripe wants to become is also not a point payment tool. It wants to become the default financial runtime environment for internet commerce. This is also why OUSD is important for Stripe.

Because if Stripe just continues to wrap more traditional financial capabilities into APIs, it's still abstracting over the existing financial system. It can become more user-friendly, more complete, and more like a financial OS, but the underlying settlement assets, clearing networks, and some of the economic benefits still reside with others.

What OUSD gives it is an opportunity to move down into the money layer. From this perspective, actions like Bridge, Open Issuance, OUSD, Privy, agentic commerce, and Tempo are not isolated. Bridge gave Stripe stablecoin issuance/orchestration capability. Open Issuance lets businesses issue and manage their own stablecoins. OUSD provides an entry point for a shared stablecoin and alliance network. Privy brings Stripe closer to wallets, identity, and user-side crypto-native onboarding. Tempo is a payments-focused blockchain incubated by Stripe and Paradigm, pointing to stablecoin payment and settlement rails. Agentic commerce provides the new use case for all this: In the future, if AI agents truly represent users, businesses, and software systems to initiate purchases, subscriptions, service calls, and settlements, then payment is no longer just an action of a person clicking a checkout button, but will become continuous fund flows between software.

Looking at these actions together, the story Stripe wants to tell is not just: we make payments simpler. It's: we enable the fund flows in the next-generation internet economy to be callable by software, manageable by businesses, and globally settled.

This is the money movement network narrative. It's bigger than payments API, and bigger than 'supporting stablecoin payments.'

Of course, this story is still just a story for now. OUSD hasn't become a real default settlement asset, and agentic commerce hasn't entered large-scale commercialization yet. Questions remain unanswered: Will businesses be willing to hold stablecoins? Can financial systems integrate? How will regulators view it? How will traditional payment networks react?

But corporate narratives don't emerge only after everything is complete; they often appear when a company is about to cross its existing boundaries.

The boundary Stripe is now trying to cross is from 'I help you connect payments' to 'I help you organize money flows.'

OUSD isn't just another competitor in the stablecoin market. It is a signal that Stripe is pushing itself from a payment company towards a money movement network.

IV. Agentic Payment Competes Not for Payment Gateways, But for the Settlement Layer of Machine Transactions

It's worth looking at OUSD alongside agentic payment, not because AI agents will definitely only use OUSD for payments in the future.

In fact, the most common and mature stablecoin asset in agentic payment today is still USDC. Many agent wallets, x402, and on-chain micropayment solutions more easily build around USDC by default. USDC's advantage isn't just its compliance brand; it's that it's already integrated into developer tools, wallets, exchanges, payment infrastructure, and on-chain liquidity networks.

Visa and Mastercard are not bystanders either. They won't sit back and let stablecoins replace them. A more realistic scenario is that card networks are also transforming themselves into payment networks usable by agents: finer-grained authorization, stronger tokenized credentials, risk controls, limits, and settlement rules more suitable for machine transactions.

In June 2026, Visa announced a set of AI, stablecoin, and token innovations to support smarter, programmable commercial transactions. Mastercard also launched Agent Pay for Machines, explicitly supporting multi-rail settlement with cards, accounts, and stablecoins.

So, the future of agentic payment won't be a simple 'stablecoins replace card networks' story.

What's more likely to happen is: card networks, bank accounts, stablecoins, wallets, on-chain settlement, and merchant systems will all compete for the same position: Who will become the settlement layer that agents can call, businesses can control, merchants can accept, and finance can reconcile?

That's why Stripe's moves are worth looking at together:

OUSD is the attempt at a settlement asset.

Tempo is the attempt at a payment chain and stablecoin settlement rail.

Bridge is the infrastructure for stablecoin issuance/orchestration.

Privy is the gateway for wallets, identity, and user onboarding.

If these are viewed separately, each is just a product move. But viewed together, they point to the same question: Stripe doesn't just want to participate in the front-end checkout of agentic payment. It wants to move from the payment gateway down to the settlement layer. This is also where the real dynamic lies between Stripe and traditional card networks.

Visa and Mastercard's advantage lies in their existing global merchant networks, issuing bank networks, risk rules, and dispute handling systems. Their most natural path is to transform their existing networks into payment networks that agents can also call.

Stripe's strength is not owning the card networks themselves, but standing on the side of merchants, developers, platforms, and emerging software companies, packaging complex financial capabilities into APIs. It's closer to the application layer and merchant side, and easier to enter the workflows of AI-native companies, agent tools, SaaS, and marketplaces.

So, if agentic payment truly develops, Stripe won't be content with just helping agents call Visa or Mastercard.

What it wants more is: to let agents safely use money within Stripe's rule system. The key here isn't 'can it pay,' but the whole set of issues after payment:

Who authorizes? Who sets the budget? Who bears the risk? Who handles KYC? Who processes refunds and disputes? Who syncs the transaction into the company's accounting system? Who decides how much an agent can spend, on which services, and with which asset for settlement?

This is the real complexity of machine transactions. An agent buying an API, calling data, subscribing to a tool, paying for compute power, completing a cross-border task—superficially, it's a payment; in reality, behind it lies a set of permission, identity, risk, budget, audit, and reconciliation issues.

Stablecoins can solve some settlement efficiency issues, but they can't solve all commercial payment problems alone. Card networks can continue to provide authorization, risk control, and merchant acceptance, but they also need to adapt to low-value, high-frequency, cross-platform, software-initiated transaction patterns.

What Stripe is competing for is precisely the middle layer between these two:

on one side, connecting merchants and developers; on the other side, organizing stablecoins, wallets, identity, risk, settlement, and reconciliation.

From this perspective, OUSD is not the whole answer to agentic payment; it's a piece of the puzzle for Stripe to move down to the settlement layer.

The real ambition is to turn agentic payment into a money movement network that Stripe can organize.

V. So, Can OUSD Support Stripe's Ambition?

Back to the initial question: Can Open USD support Stripe's ambition? My answer is: Not in the short term, but it makes this ambition more concrete for the first time.

It can't immediately free Stripe from traditional payment networks—Visa, Mastercard, ACH, local banks, card organizations, acquirers, issuers, regulatory licenses, KYC, AML, tax, reconciliation—these things won't disappear just because a stablecoin is announced. Commercial payments in the real world have never been as simple as 'money moves from A to B.'

Stablecoins can solve part of the transmission problem; they can make funds flow faster, cheaper, and more programmably. But they can't automatically solve the landing problem.

After the money arrives, who's responsible for booking it? Who does KYC? Who bears the fraud risk? Who handles refunds and disputes? Who ensures the merchant receives funds they can use? Who connects this transaction into the company's ERP, financial, and tax processes?

These questions still require a lot of traditional financial and commercial infrastructure. That's also why Stripe won't become a pure crypto company because of OUSD.

It's more likely to take another path: making stablecoins part of its existing financial infrastructure. That is, if OUSD succeeds, it won't be because it made Stripe leave the traditional financial system, but because it gave Stripe an additional settlement layer it can help define, outside the traditional financial system.

This layer might not replace everything, but it can change Stripe's position in money flows.

In the past, Stripe was more like an excellent translator, translating complex financial systems into APIs developers could call, turning capabilities like payments, invoicing, tax, card issuance, risk, and fund accounts into modules businesses could embed into their products.

But OUSD points to something else: Stripe is not just translating existing financial systems. It's starting to participate in defining new financial systems. That's why I think this is worth writing about. Not because OUSD will definitely win, but because it exposes the most important strategic question for Stripe's next phase:

Does Stripe want to become a better payment processor, or does it want to become the money movement network for the next-generation internet commerce?

These two things seem only slightly different, but in reality, they are worlds apart. The value of a payment processor comes from transaction processing, risk control, access efficiency, and merchant coverage. The value of a money movement network comes from network effects, default settlement assets, rule-making ability, liquidity organization capability, and economic distribution mechanisms.

The former is a service; the latter is infrastructure.

What Stripe has done best over the past fifteen years is turning financial services into software interfaces. But if it wants to support AI commerce, the global platform economy, cross-border payouts, stablecoin settlement, and agentic payment in the future, it can't just stay at the interface layer.

It needs to get closer to the money itself. OUSD gives it an entry point to get closer to the money itself. Of course, whether this entry point can become a real network depends on the coming years. It depends on whether OUSD finds real use cases, whether Stripe deeply embeds it into merchant, platform, and developer tools, whether participants truly bring distribution rather than just putting their logos on the announcement page, whether regulators accept this consortium stablecoin structure, and how Circle, Tether, banks, card networks, and other payment companies will react.

This won't be answered quickly, but it has already made one thing clear: Stablecoins are no longer just trading assets in the crypto world. They are becoming tools for payment companies, banks, platforms, merchants, and AI companies to compete for the gateway to the next-generation money network.

From this perspective, OUSD is not Stripe's endpoint; it's a signal that Stripe is trying to push itself from a payments API company towards a money movement network.

Five months ago, I wrote: Money will run on Stripe.

Looking at it today, this statement can be pushed one step further. What Stripe wants to prove is:

Money may settle on a network Stripe helped define.