Original Author: Long Yue

Original Source: Wall Street News

At 20:30 Beijing time tonight, the US Bureau of Labor Statistics will release the May CPI data. This is also the most watched heavyweight inflation data by the market before the Federal Reserve's new Chairman Wash's policy rate meeting next week.

According to reports from the Chase the Trade desk, Wall Street's four major institutions—Goldman Sachs, UBS, Deutsche Bank, and Morgan Stanley—have released a flurry of preview reports on the eve of the data release. The forecasts from the four institutions vary, but the direction is similar: Overall inflation may be high, but core inflation may not be that hot. Energy prices are pushing up overall CPI, while factors such as rent and auto insurance are suppressing core CPI.

Overall CPI May Rise Above 4% to Hit a Three-Year High, Core CPI Possibly Below Consensus

Looking at the forecasts, the four institutions' predictions for the May year-on-year overall CPI are concentrated in the range of 4.17% to 4.3%, all higher than April's 3.81%. However, the forecasts for the month-on-month core CPI are generally lower than the market consensus.

The trends of overall and core inflation show a clear divergence.

The "worrying" part is overall inflation. The year-on-year predictions from Goldman Sachs, UBS, Deutsche Bank, and Morgan Stanley are all above 4%. Deutsche Bank's estimate of 4.27% and Morgan Stanley's estimate of 4.3% are 46-49 basis points higher than April's figure and would be the highest since April 2023.

The "positive" part is core inflation. Excluding food and energy, the month-on-month core CPI may only be 0.17%-0.22%, significantly lower than the market's mainstream expectation of 0.27%-0.30%.

Overall Inflation May Break 4%: Energy Is the "Culprit"

Energy will be the core driver of the potential jump in this inflation reading.

Following the outbreak of the Iran war, US retail gasoline prices have risen sharply, driving a projected month-on-month increase in energy commodity prices of about 6%~7% for May, with the entire energy category seeing a month-on-month increase of nearly 4%. This effect directly pushes the year-on-year overall CPI from 3.81% in April to 4.17%~4.3% in May.

Deutsche Bank's calculations show that energy inflation year-on-year may approach 24%; back in February, this number was only 0.5%.

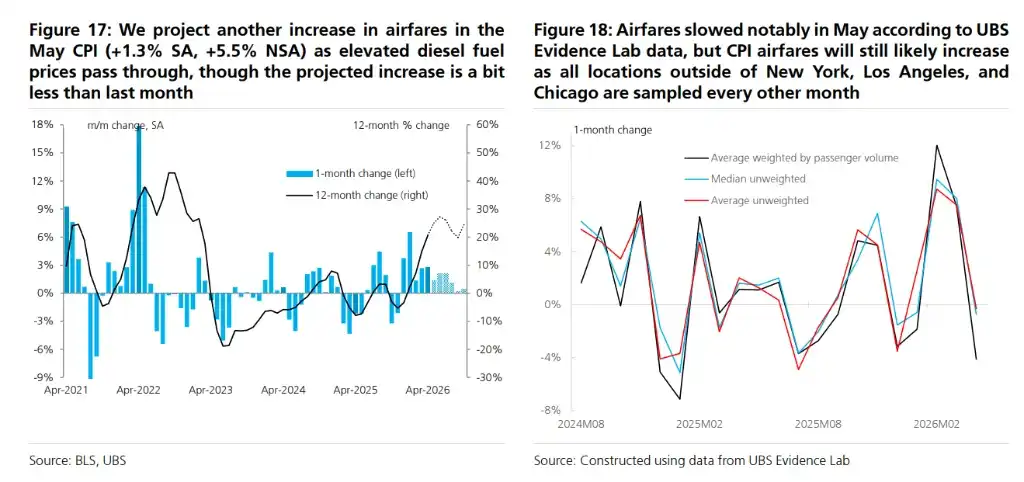

Airfare increases are one of the most direct transmission channels. Rising fuel costs directly increase airline operating costs. Airfare prices in May are expected to rise month-on-month by 1.3%~2%.

The good news is that gasoline prices peaked on May 20th and have since fallen by about 40 cents per gallon. UBS expects this to lead to a month-on-month decline of about 0.13% in the overall CPI for June, with the year-on-year rate falling back to around 3.81%. In other words, May is likely the peak of this round of overall inflation.

Why Core Inflation May Be Lower Than Expected: The Key Lies in Housing Cooling Down Again

Core CPI excludes food and energy. Precisely because these two hottest components are excluded, the May core data will look much more moderate.

Housing carries a very high weight in the US CPI, about 35%.

Both Goldman Sachs and UBS predict that Owner's Equivalent Rent (OER) and primary residence rent in May will increase month-on-month by about 0.22%~0.23%, continuing a slowing trend. In April, these two components rose by 0.53% and 0.55% month-on-month, respectively. Deutsche Bank also lists "housing inflation trends remaining moderate" as one of the reasons for the softness in core inflation.

Because OER itself has a large weight, even a decrease from around 0.5% to just over 0.2% will significantly lower the core CPI reading.

Auto insurance is another cooling point.

Goldman Sachs expects auto insurance prices to fall 0.1% month-on-month in May. Its online data model shows that changes in premiums are giving a downward signal for auto insurance CPI. Deutsche Bank also mentions that auto insurance is expected to be weak again.

There is also no significant upward pressure in used cars. Goldman Sachs expects used car prices to remain flat and new car prices to rise 0.1%; UBS expects used car prices to fall 0.26% and new car prices to fall 0.10%.

This means that several items that have frequently disturbed US core inflation in recent years—housing, auto insurance, used cars—are not giving strong inflation signals this time. In other words, the low May core CPI is not due to a single component "suddenly cooling down."

Core Inflation Is Not Cooling Across the Board: Airfare, IT Goods, and Some Services Still Have Pressure

A core CPI reading below consensus does not mean all core items are cooling.

Airfare is an upward item.

Goldman Sachs expects airfares to rise 2% in May. UBS expects a 1.34% increase. The reason is that jet fuel prices remained high for most of May, which may be passed through to ticket prices.

There is significant divergence in judgments on hotel prices. Goldman Sachs expects hotel prices to rise 0.2%; UBS lowered its lodging forecast based on Smith Travel Research data, expecting the price of lodging away from home to fall 0.77%. However, UBS also notes that CPI measures prices at the time of booking, while STR data is closer to check-in time. This timing difference may bring upside risks, especially potentially reflecting early demand related to the World Cup.

There is also stickiness in goods.

UBS expects core goods prices to rise 0.08% month-on-month, between the 0.11% in March and 0.03% in April. Its assessment is that the impact of tariffs on the 12-month core goods inflation may have slightly passed its peak, but residual pass-through will still keep monthly core goods prices growing slightly positively for the rest of this year.

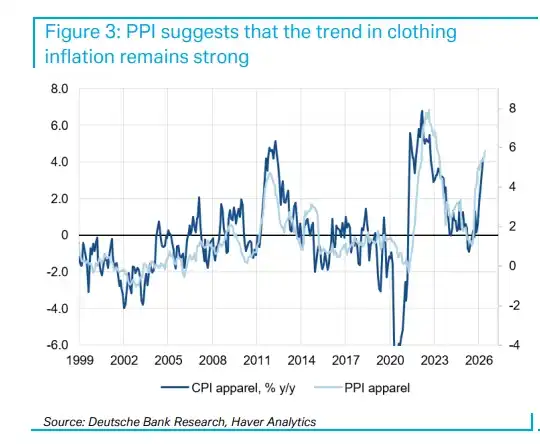

Deutsche Bank also mentions that import prices indicate that IT goods prices still have strong momentum, partly due to global memory chip prices remaining high. Meanwhile, apparel PPI shows that apparel inflation trends remain strong, although import prices are weak, and the momentum in CPI may have slowed compared to previous months.

Services are more complex.

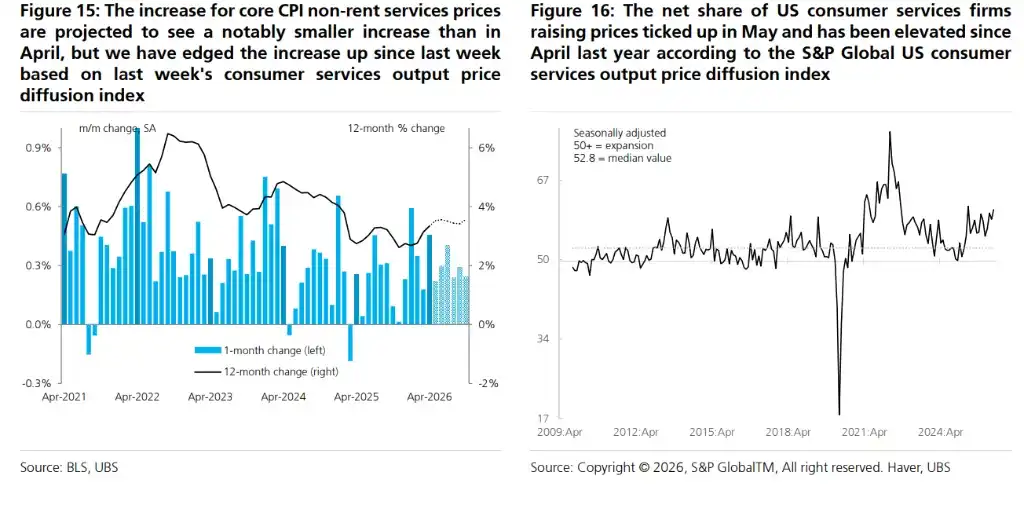

UBS has raised its forecast for non-rent core services prices from 0.17% to 0.21%, citing the S&P Global US Consumer Services Output Price Diffusion Index showing an increase in the proportion of consumer service firms raising prices in May, reaching the second-highest level since 2009, excluding the abnormal pandemic period.

What to Really Watch Tonight Is Not Just an Overall Inflation Above 4%

The surface numbers for May CPI may be high, but breaking them down is more crucial.

If overall CPI is high, primarily driven by gasoline and energy, the market will likely combine that with the decline in gasoline prices in June to judge its sustainability.

If core CPI is significantly lower than expected, the market will continue to examine where the low inflation is coming from: a trend slowdown in housing or a one-off seasonal drag.

If airfare, IT goods, and non-rent services continue to be strong, the significance of the core cooling will be discounted.

Therefore, this CPI might give the market two messages simultaneously:

On one hand, overall inflation has broken through 4% again, potentially even hitting a new high since April 2023.

On the other hand, core inflation might only be around 0.2%, clearly below market consensus.

This is what makes tonight's CPI so difficult to trade: overall inflation looks hot, but core inflation may not be that hot; oil prices push up the overall figure, while housing and auto insurance push down the core.

Inflation Swap Pricing: The Market Is Betting on a Dollar-Rising Surprise

The inflation swap market is currently pricing May overall CPI at 4.27%~4.28%, slightly above the Bloomberg survey median of 4.2%.

The analytical framework of Morgan Stanley strategist Molly Nickolin shows that in the past 12 CPI releases, inflation swap pricing correctly predicted the direction of the year-on-year inflation 9 times before the release. The current pricing implies an upside deviation of about 0.48 standard deviations relative to economists' expectations.

Based on historical backtesting, a 0.48 standard deviation upside surprise typically corresponds to a DXY US Dollar Index increase of about 0.14% within one hour of the release. Among all G10 currencies, the Swedish Krona (SEK) has historically performed the weakest in a "USD-bullish" CPI release day, with the largest average decline.

Looking Ahead: Oil Prices Are the Biggest Variable for the Inflation Path

The path of core CPI in the coming months depends on how long oil prices can be maintained.

The current baseline forecast is: Month-on-month core CPI remains around 0.2%. However, if the Middle East situation persists and the decline in oil prices falls short of expectations, upside risks will become more prominent—high oil prices not only directly push up energy prices but also continue to seep into core inflation through intermediate channels like airfare and transportation.

Deutsche Bank's long-term forecast is more pessimistic: Even if oil prices start to decline in June, overall energy inflation year-on-year will remain above 10% until early 2027 before turning negative. Core services inflation (excluding rent/OER) is also expected to remain above 3% for a long time.