Author: Nancy, PANews

As crypto assets continue to experience weakness and decline, crypto mining companies are facing increasingly severe survival pressures. In search of new growth avenues, more and more mining companies are accelerating their shift into the AI arena. This transformation narrative has quickly gained favor in the capital markets, leading to significant stock price increases for many mining firms, with some even reaching new all-time highs.

However, while the AI business injects new growth potential into mining companies, the massive capital expenditures, ongoing funding requirements, and lengthy return cycles behind it are pushing these firms into another battle of capital consumption. At a time when the profitability of mining operations remains under pressure, this high-stakes gamble of transitioning to AI is testing the financial strength and execution capabilities of mining enterprises.

Stock Prices Outperform Bitcoin Significantly, Mining Companies' Valuations Enter a Divergence Phase

Mining companies are transforming into landlords of computing power in the AI era.

With the profit margins for Bitcoin mining continuously narrowing and some mining companies even falling into losses, the AI boom has fueled a sharp surge in global demand for data centers, power resources, and GPU computing power. An increasing number of mining companies are accelerating their pivot towards AI infrastructure, seeking new growth curves.

For mining companies, this transition offers inherent advantages. Over the years, to meet the demands of large-scale mining, they have amassed critical assets such as abundant power resources, land reserves, substation access capabilities, and mature cooling and heat dissipation systems. Compared to data center operators starting from scratch, mining companies only need to upgrade and retrofit their existing facilities to quickly enter the AI infrastructure market, catering to AI computing power demands at a lower cost and with a shorter cycle.

Since last year, the pace of mining companies transitioning to AI has noticeably accelerated. Some miners have decisively scaled back or even exited traditional mining operations, fully shifting to AI computing and data center operations; others have retained part of their mining business but are gradually reallocating resources and capital expenditure focus towards the AI sector. Today, several mining companies have grown into significant players in AI infrastructure construction.

Looking at the timing of transition, CoreWeave, Applied Digital, and Bitdeer began laying out AI computing and data center businesses as early as 2022-2023, among the earlier movers in the industry; while mining firms like Iris Energy, Terawulf, Hut 8, Riot Platforms, and Bitfarms began to fully ramp up AI infrastructure construction in 2025, coinciding with the AI industry's rapid expansion cycle.

In terms of stock performance, the market has shown considerable recognition for the AI transition narrative of mining companies. The 11 mining companies have seen an average year-to-date gain of 75.97%, significantly outperforming Bitcoin over the same period, with most hitting new highs after their transition. Among them, Bitfarms (129.62%), Hut 8 (131.87%), Terawulf (118.68%), and Riot Platforms (93.71%) have been particularly standout performers, benefiting from this wave of AI infrastructure revaluation.

In terms of market capitalization, mining companies have shown clear divergence. As a representative of successful transition, CoreWeave's market cap has reached $62.855 billion, far exceeding other miners and setting a new valuation benchmark for the industry; Iris Energy, Terawulf, Hut 8, Applied Digital, and Riot Platforms form a tier with market caps between $10 billion and $20 billion; companies like MARA Holdings, Core Scientific, Bitdeer, CleanSpark, and Bitfarms remain in the sub-$5 billion range. This divergence stems not only from first-mover advantages but also reflects the market's differentiated pricing based on each mining company's AI strategy execution capabilities, client resources, and data center deployment progress.

However, from a fundamental perspective, most mining companies are still in the heavy investment phase of their AI transition. Although the latest quarterly earnings reports of many miners show revenue growth, overall profitability remains under pressure. On one hand, volatility in the value of crypto asset portfolios weighs on profit performance; on the other hand, the construction of AI data centers requires massive capital expenditures, with costs for power expansion, infrastructure development, and procurement of equipment like GPUs continuously increasing, driving up operating costs and leaving most mining companies yet to escape a loss-making state.

It is noteworthy that despite generally pressured earnings performance, the stock prices of related mining companies have still risen significantly, indicating that the current market focus is not on short-term profitability but rather on the growth potential of mining companies as operators of next-generation computing power infrastructure.

Mining Companies' Survival Battle Escalates, AI Transition Requires Overcoming Multiple Hurdles

The downturn in the Bitcoin market is making the survival environment for mining companies increasingly severe.

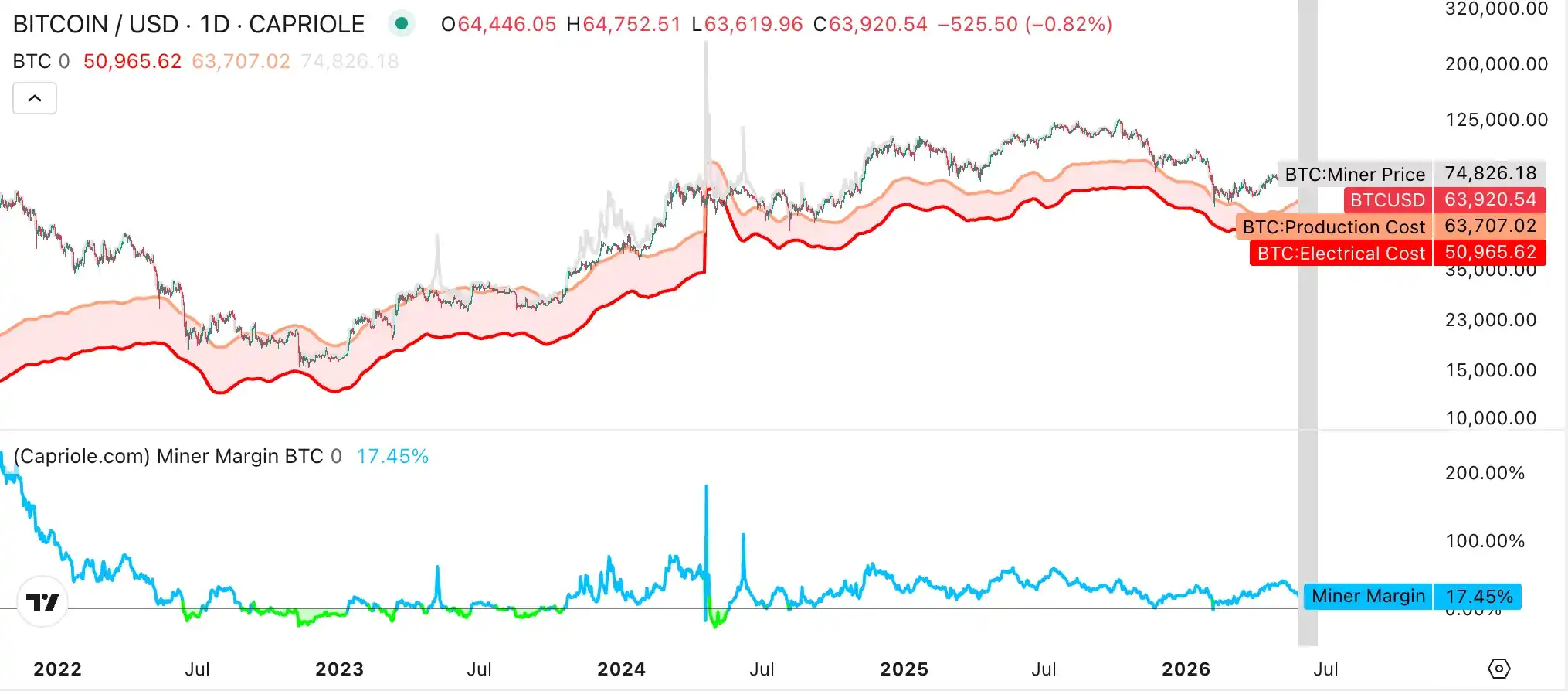

Data from Capriole Investments shows that as of June 18, the average production cost for Bitcoin is approximately $63,707, with power costs around $50,965, resulting in a miner profit margin of only 17.45%. Over the past 30 days, miner profit margins have contracted by 47.8%. Meanwhile, data from the Luxor Hashrate Index also shows that as of June 18, the daily revenue per 1 TH/s of hashrate has dropped to $0.032, a significant decline from $0.053 during the same period last year.

As mining revenues continue to shrink, many mining companies have had to sell Bitcoin to maintain cash flow, further increasing survival pressure on small and medium-sized miners, and mining resources are accelerating their concentration towards top players. Currently, the three major mining pools—Foundry USA, AntPool, and F2Pool—collectively account for 59% of the global network's hashrate share. In comparison, in 2022, the top three Bitcoin mining pools collectively accounted for only 44% of the hashrate share.

Although traditional mining operations are struggling, the explosive growth in demand for AI data centers is also driving a market re-evaluation of mining companies' value. VanEck points out in its latest research report that the most valuable assets of mining companies are not their mining rigs, but rather their power resources, substation access capabilities, land reserves, and data center infrastructure—precisely the scarce core resources most needed by the current AI industry. Because AI clients are willing to pay electricity and rental rates far higher than those of traditional mining operations, AI infrastructure is expected to become the primary growth engine for mining companies over the next decade.

According to a report from research firm Bernstein, hyperscale cloud providers, AI cloud service providers, and chip companies have announced over $90 billion in AI infrastructure partnerships, involving approximately 3.7 GW of power capacity. Currently, the pursuit of power resources has become the core of AI infrastructure competition, with Bitcoin mining companies collectively controlling over 27 GW of planned power capacity. In some parts of the United States, the cycle for securing new 1 GW power connections can be as long as 50 months, making existing mining sites important landing spots for AI data center expansion.

However, the transition to AI is far from an easy path. VanEck states that the market is still in the early stages of the AI transition, with enterprise valuations primarily measured based on Gross Energized Power. Mining companies that have signed AI leases generally receive higher valuation premiums, while projects still in the planning stage struggle to gain market recognition. Future industry valuation logic will gradually shift from "power capacity" to "project delivery capability," eventually returning to core metrics such as cash flow, return on capital, and tenant quality. Currently, the industry has only delivered about 25% of its signed capacity. The ability to complete AI data center construction on time and within budget will become a key factor determining enterprise valuation.

VanEck also emphasizes that AI tenant quality will directly impact the valuation levels of mining companies. Clients like Microsoft, Amazon, and Google—hyperscale cloud providers—can bring more stable cash flows and lower financing costs, while smaller GPU cloud service providers correspond to higher operational risks and capital costs.

Meanwhile, the enormous funding required for the transition is testing the financial strength of mining companies. VanEck estimates that mining companies transitioning to AI infrastructure still face massive capital expenditure needs, with a short-term funding gap of approximately $50 billion and long-term capital requirements potentially reaching $221 billion.

Under immense financial pressure, many mining companies have begun raising funds through various methods. For instance, miners like Iris Energy, TeraWulf, Bitfarms, and CleanSpark have raised capital through issuing convertible bonds, attracting investors with low coupon rates and future conversion potential; while companies like Core Scientific, Terawulf, MARA, Bitdeer, and Riot Platforms have chosen to sell off or even liquidate part of their Bitcoin reserves to continually fuel their AI transitions.

Additionally, many mining companies are beginning to secure future revenue by signing long-term AI or high-performance computing (HPC) contracts, thereby obtaining project financing support and reducing overall operational risks. For example, CoreWeave reached a $6 billion AI cloud services cooperation agreement with Jane Street; IREN secured a $9.7 billion AI cloud computing contract with Microsoft; Hut 8 signed data center leasing agreements totaling $9.8 billion; and Bitdeer is collaborating with Norway's DCI to build the country's largest AI data center project.

For mining companies, AI currently offers a development path with far greater imagination space than traditional mining operations. However, this transition is not a simple switch from mining to selling computing power; it is essentially a long-term competition centered on capital, resources, and execution capabilities.