Author: Thejaswini M A

Compiler: Chopper, Foresight News

Devoting oneself to meticulously refining high-quality, long-term products often sees capital arriving belatedly; while projects that are all hype and hollow inside attract a frenzy of investment. This is an immutable law of the market, cycling endlessly from the Tulip Mania and the Dot-com Bubble to canal stocks and the NFT wave.

Currently, artificial intelligence is seen as the next mega-bubble. A typical feature of a bubble is market participants heavily leveraging up, with entire business models built on precarious castles in the air, ignoring foundational flaws in the system until it collapses, after which everyone blames the 'bubble market'.

This article focuses on the Bittensor network, which cleverly aims to incentivize the masses to develop AI through token rewards. The entire network is divided into over a hundred independent ecosystem units called subnets. Developers build AI-related services, the system scores the results, and developers can instantly receive the crypto token TAO as compensation.

Wall Street is already racing to launch Bittensor ETF products, with Bitwise and Grayscale having filed applications with the SEC. The hidden vulnerabilities of this system are now clearly visible to all.

Bittensor builds a decentralized AI network by borrowing the competitive incentive logic of Bitcoin: using tokens to incentivize participants to compete with each other, relying on market competition to filter out quality results from inferior projects. The network is divided into approximately 128 subnets, each corresponding to a specific AI business segment, such as model inference, large model training, data scraping, etc.

Miners are responsible for mining, validators for scoring. TAO rewards miners based on the quality assessed by validators. Validators' rewards are determined by how closely their scores match those of other validators, weighted by their stake. Therefore, a validator's earnings depend on whether their score aligns with the consensus, not on whether it is objectively correct.

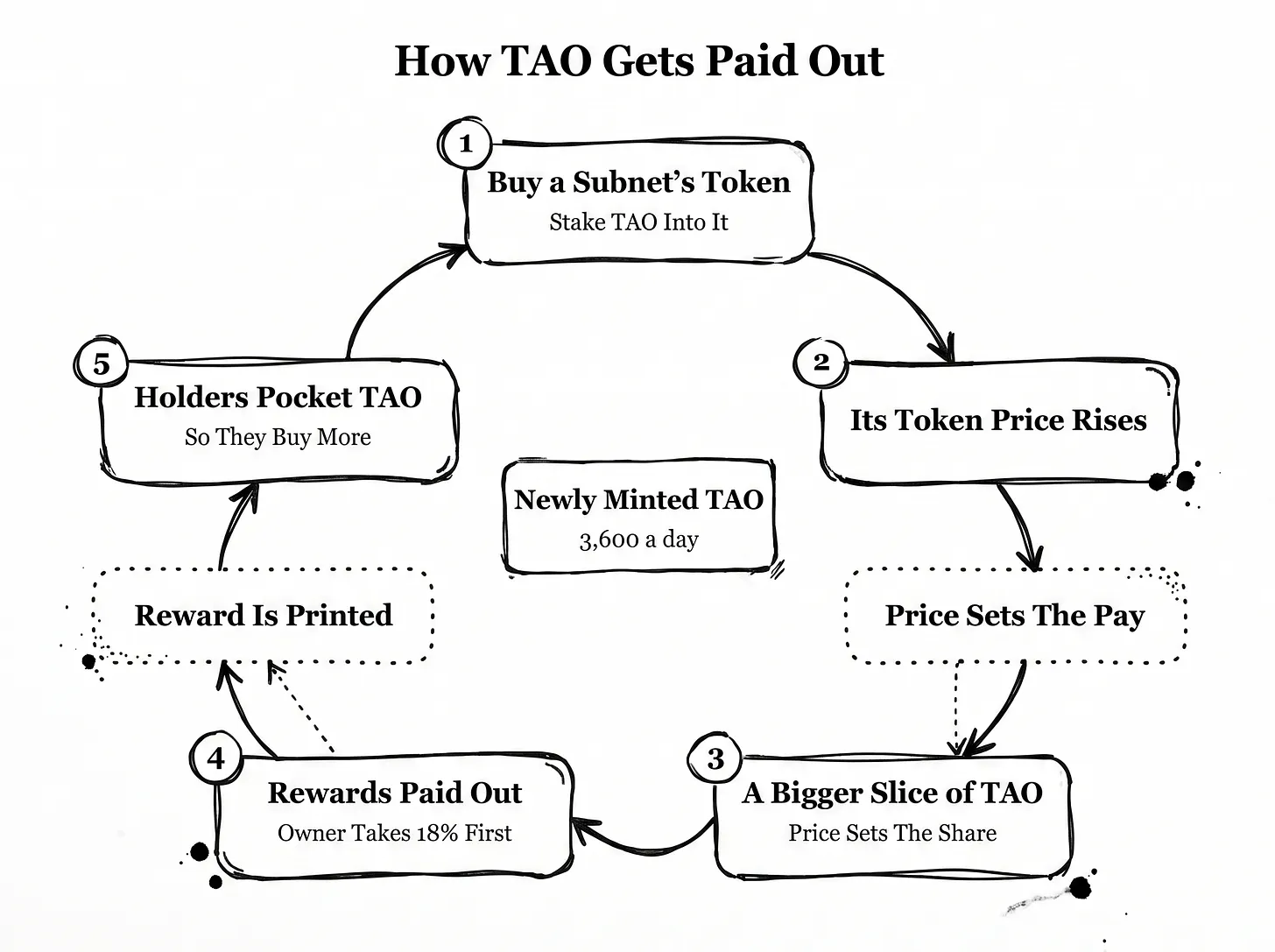

The share of newly minted TAO allocated to each subnet is determined solely by the price of that subnet's native Alpha token and has no relation to the quality of the AI output. Additionally, subnet operators take an 18% cut of the rewards first, with the remainder distributed to other participants.

TAO is a token with a market cap of about $2 billion, of which approximately $690 million is staked into subnets. These subnets determine which AI projects receive funding.

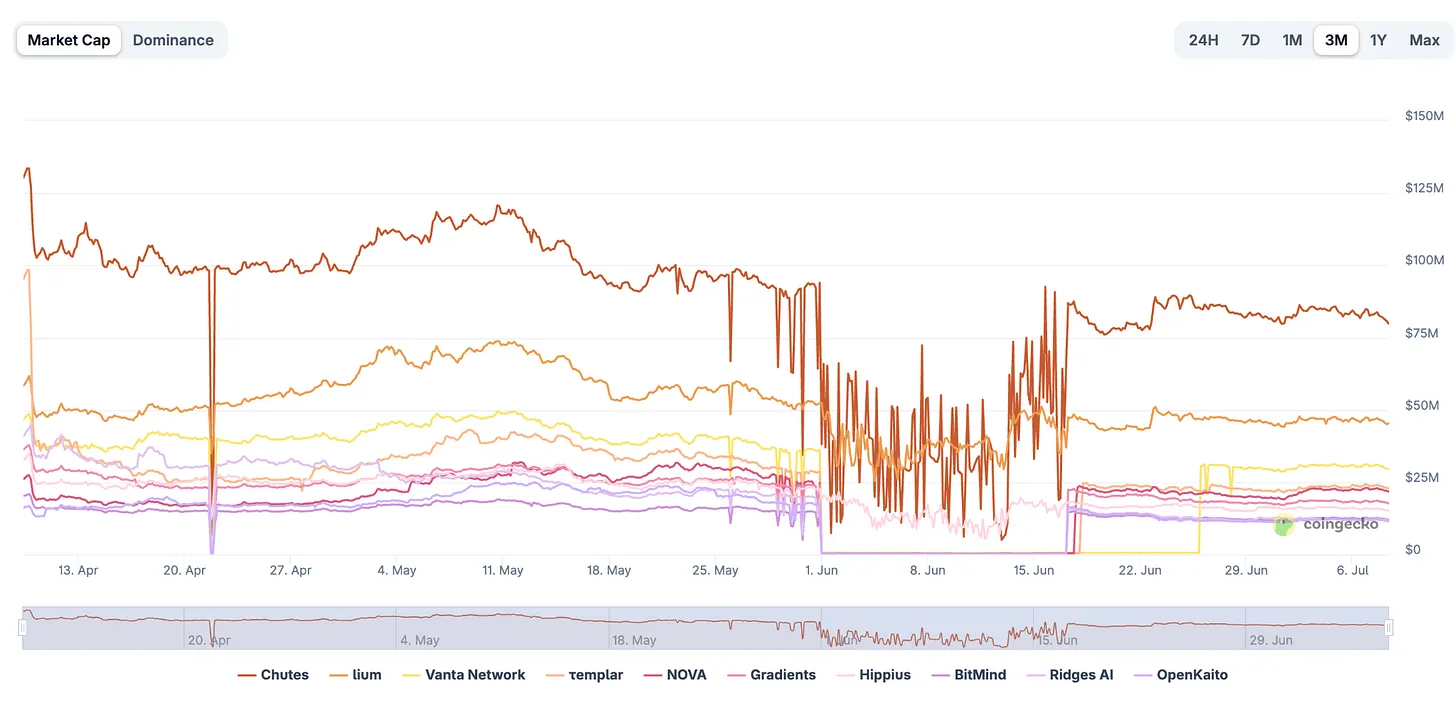

Bittensor Subnet Token Market Cap Rankings, Data Source: coingecko.com

Each subnet issues its own independent native token called Alpha. Users staking TAO into a subnet are essentially buying that subnet's Alpha token, driving up its market price. The proportion of newly minted TAO a subnet receives is determined by the average price of its Alpha token over a period.

Merely pumping the price short-term cannot sustainably increase the reward share; continuous buying is needed to support the price, forming a self-reinforcing cycle: Buy Alpha → token price rises → subnet receives a larger share of new TAO tokens → new tokens are directly distributed to Alpha token holders → holders receive incremental funds and continue buying more. External capital inflow pushes the price up, attracting even more capital.

The only constraint in this cycle is the network's continuous issuance of Alpha tokens. To realize their earnings, miners and validators must constantly sell, creating continuous selling pressure on the token price. For a subnet to keep receiving funding, there must be a constant stream of new buyers to absorb this selling pressure. This is precisely the deliberately designed operating logic of this mechanism.

The advantage of this mechanism is that, through independent subnet tokens, investors can specifically bet on individual AI sub-sectors. For example, investing only in inference subnets while avoiding model training, or vice versa. Capital can precisely target a single segment of the AI industry chain, which is impossible in traditional stock markets.

However, on-chain systems can only recognize token transfer activities and cannot track the real usage volume of AI products. There is no clear, traceable ledger of commercial revenue. Token prices are entirely driven by capital flow, unconstrained by actual income. Traditional stock prices are supported by verifiable product sales revenue; for instance, Nvidia's stock price is backed by trackable product sales. In contrast, the sole support for a subnet token's price is secondary market buying activity. When capital inflow becomes the only metric, token price is entirely defined by capital enthusiasm.

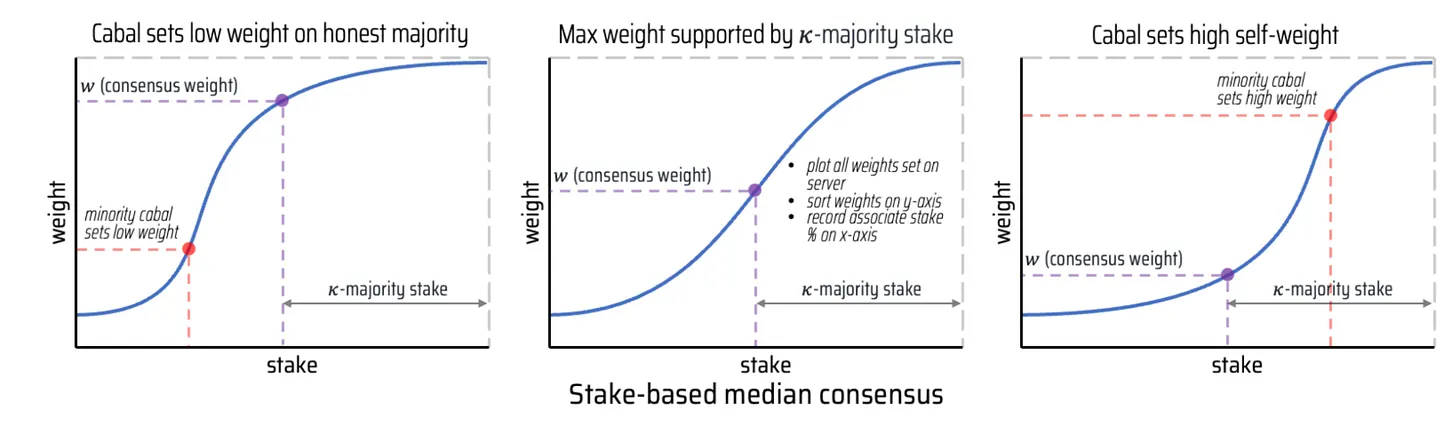

The design intent of this mechanism is to require validators to score miners objectively and fairly. The underlying consensus protocol, Yuma, also has anti-collusion rules: if a score deviates too much from the group average, it is invalidated, preventing validators from profiting by artificially inflating scores for familiar projects. This design is quite ingenious.

However, this anti-collusion mathematical model has a critical threshold; it is only effective when the colluding party's staked amount is less than half of the total validator stake in the subnet. Once colluding nodes control a majority of the staked compute power, miners and validators can privately collude, mutually inflating scores to瓜分 (split) TAO rewards, and the network will still automatically distribute the earnings.

Another major vulnerability is 'score copying': some validators do not verify AI outputs at all but simply copy scores from the public ledger of other validators, claiming rewards without any effort. The project team introduced a 'commit-reveal' mechanism to patch this flaw: sealing scores for a period to prevent immediate copying. However, this solution only works for scenarios where AI output quality fluctuates continuously. If a subnet's business is stable and its output homogeneous, copying scores can still be profitable.

Data Source: RaoFoundation Subnet

Now, let's look at the threshold for cheating and who holds the power. The Rayon Labs team operates three leading subnets, collectively瓜分 (taking) a quarter of the network's daily new TAO issuance. Approximately two-thirds of all TAO is in staking, with a large portion concentrated in the hands of a few entities.

The market holds two completely opposing interpretations of this: Perspective One: Bittensor is an efficient market mechanism. There's no need for a closed-door committee to decide AI project funding qualifications. A vast number of market participants publicly bet on various AI sectors, and capital naturally flows to the directions favored by the market. Capital inflow is often a leading signal of a sector's potential. Perspective Two: Token prices must be tied to real commercial demand to have practical meaning, such as paying customers and verifiable sales revenue. Bittensor's value anchor is extremely weak.

The highest-earning subnets on the network generate far more revenue from token issuance than from actual customer payments. The number of core operators who can adjust reward distribution rules is extremely small. In the spring of this year, the project adjusted token release rules and sold a large amount of held tokens, triggering internal conflicts. The network's largest operator, Covenant AI, directly exited the network.

While early mechanism flaws can be quickly fixed, and the network has already corrected major issues through hard forks, consider the Optimism ecosystem. Native crypto venture capitalists, tired of unrestrained pre-funding models, introduced a retrospective funding mechanism: funds are only distributed to projects that have proven their practical value, not merely for betting on future potential. Rewards are granted after verifying results, not as pre-subsidies before token issuance. Gitcoin and Filecoin have also implemented different variants of this concept.

The core flaw of the Bittensor system lies in using token circulation收益 (profits) as the incentive metric, rather than more reliable, validation-based standards tied to actual business落地 (implementation).

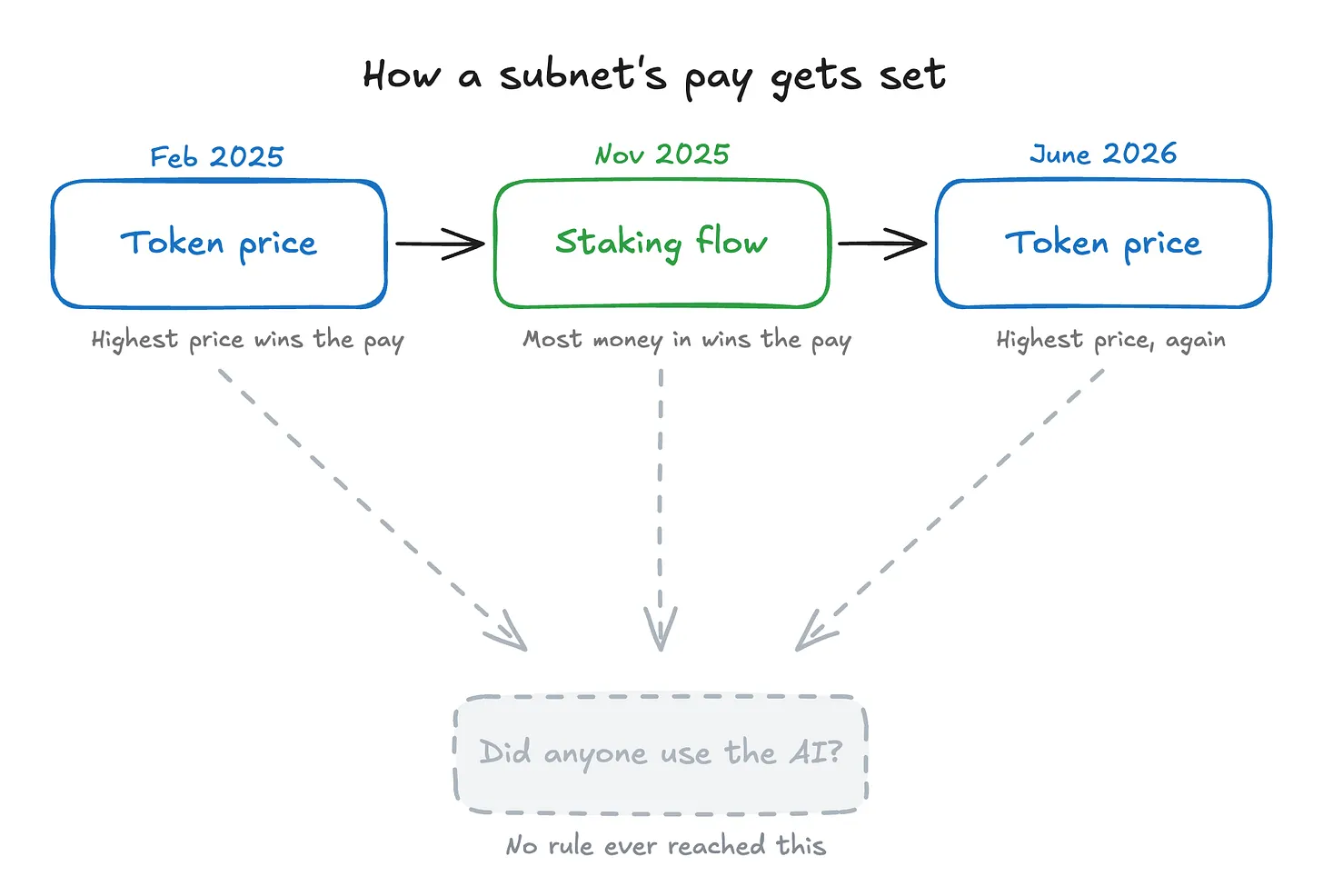

The network has revised subnet reward distribution rules twice a year. Initially based on subnet token price, it switched to net staking capital flow (inflow minus outflow) last November. In June of this year, due to various flaws exposed by the capital flow rule, it switched back to the token price mechanism. Both rules are merely proxy metrics, unable to measure the most crucial data—whether real users are paying to use the corresponding AI services.

A network willing to overturn its own fundamental rules twice in a short period, thereby动摇 (shaking) its survival foundation, perhaps possesses greater transformative power than most networks. But upon冷静审视 (calmly examining) the two hard forks and rule adjustments, all three sets of评判标准 (evaluation criteria) ignored the key metric: the willingness of real external users to pay for subnet services. All the rules引导 (guide) 'money chasing money,' not 'value following market demand.'

Even if this system involves大量资金空转浪费 (significant capital idling and waste), it is objectively building foundational infrastructure. Just as the Dot-com Bubble gave birth to the global fiber-optic backbone network, the Bittensor frenzy催生 (spawns) computing hardware and AI training resources that will retain long-term value even after the hype subsides.

The distributed AI sector itself holds immense industry红利 (dividends). Open-source solutions are the only path to breaking the monopoly of chip giants, much like Linux颠覆 (disrupted) the OS landscape and Wikipedia重构 (reconstructed) the encyclopedia content ecosystem. This network is上演 (staging) similar disruptive innovation: The Covexus team, leveraging 70 distributed devices to train a large model, achieved performance surpassing Meta's Llama 2 and even received public recognition from NVIDIA CEO Jensen Huang. Yet, it gets buried in the noise of massive token speculation.

This is also why this ETF is more than just an omen. Both Grayscale and Bitwise expect the U.S. Securities and Exchange Commission (SEC) to respond later this year, around August. Once approved, this inherently flawed system will be directly接入 (connected) to the investment portfolios, including retirement funds, of the American public. Blindly entering investors will face巨大风险 (significant risks). However, the ETF's落地 (launch) also represents two positive changes for the emerging ecosystem: massive传统资金 (traditional capital)入场 (entry) and the industry undergoing comprehensive public regulatory scrutiny. Regulatory endorsement and oversight by millions of new shareholders over收益分配 (profit distribution) is the most effective way to force the network to optimize its incentive mechanisms. The随之而来的严苛审查 (ensuing rigorous scrutiny) will ultimately push the entire ecosystem towards maturity.

With this optimism, I want to say you should pay close attention to what truly matters. Like all young, flawed systems, this one is new, and its bugs need fixing. What I want to emphasize is its potential: open, multi-party, non-proprietary AI, not the封闭生态系统 (closed ecosystems) built by large cloud service providers with the world's largest server clusters.

I look forward to a future where subnets can脱离 (break away from) foundation subsidies and become self-sustaining. It will indicate that the most powerful technology of our era does not have to be controlled by a few entities.