作者:氪rypto

引言

本文深入探讨 OLM (@OLM_Research) 的发展历程,从IMO(初始模型发行)的成功到现在成为去中心化社区,开始融入 ORA 生态系统。我们欣然见证一路以来ORA的OLM和IMO为人工智能模型开发带来的诸多影响。

1.初生:IMO历史首秀,创新开辟商业模式

1.1 IMO

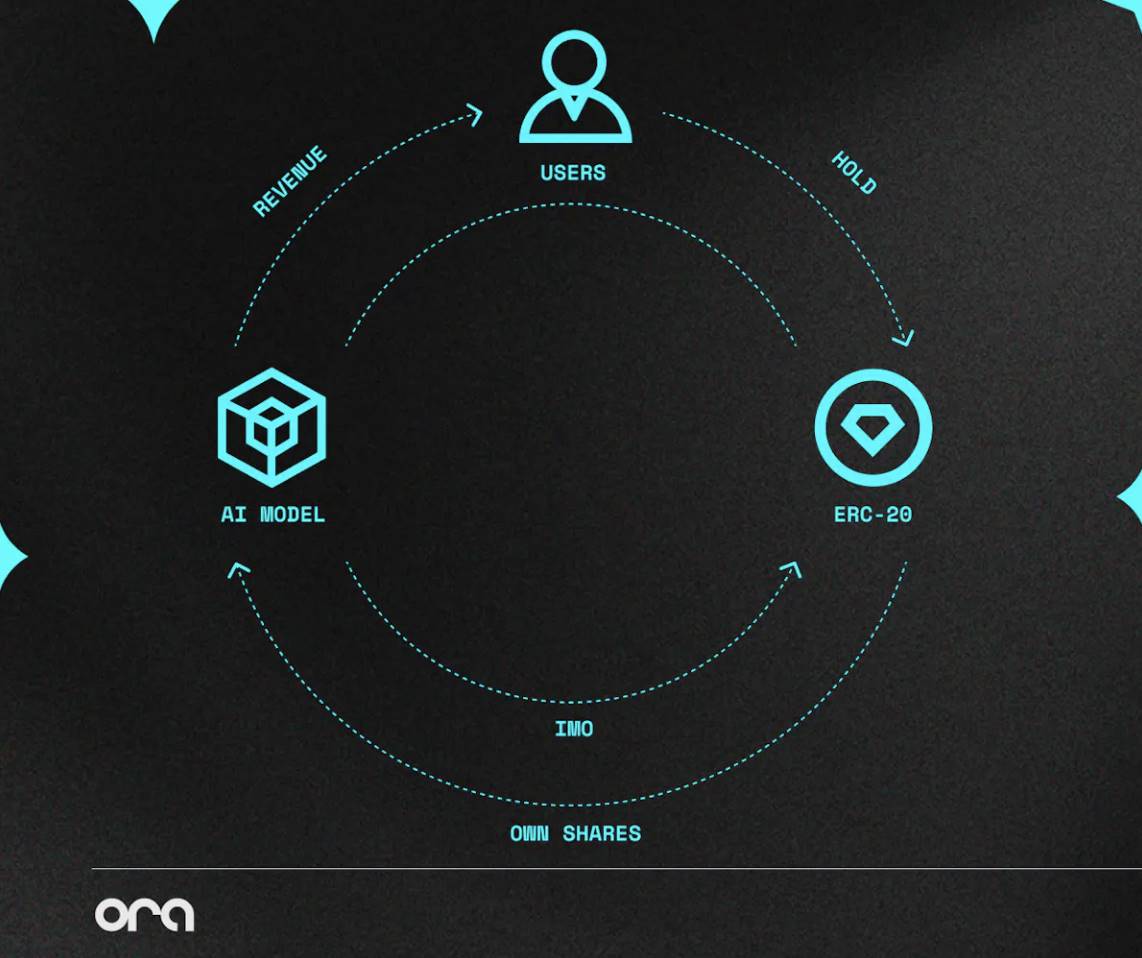

IMO,即初始模型发行,将开源AI模型的所有权代币化。IMO的引入,不仅将AI模型作为链上资产,还为持有者提供了类似股票股息的收益,带动了其商业价值。对于人工智能模型来说,IMO为开源项目提供可持续的资金来源,促进模型的传播和持续贡献。而且它还允许代币持有者通过收入和推理资产(如 ERC-7007)获取人工智能模型的价值。

可以说,是IMO凭借一己之力将整个AI行业的价值带入区块链,因此广泛被业内看好为本周期内最大的商业创新模式。

1.2 OpenLM

OpenLM由去中心化团队所创建,是一个执行语言建模(LM)存储库,旨在促进中型LM的研究,持有MIT许可。

1.3 OLM IMO

OLM的IMO 是全球首个 IMO,标志着人工智能与加密领域的结合,在以太坊上实现了模型的代币化,创造出与OpenLM模型愿景一致的生态系统,推动“开放式人工智能”的发展。OLM代币在市场中也表现出色,最高涨幅超过 60 倍,市值达到 6000 万,印证出IMO在AI行业中的巨大潜力和财富效应。

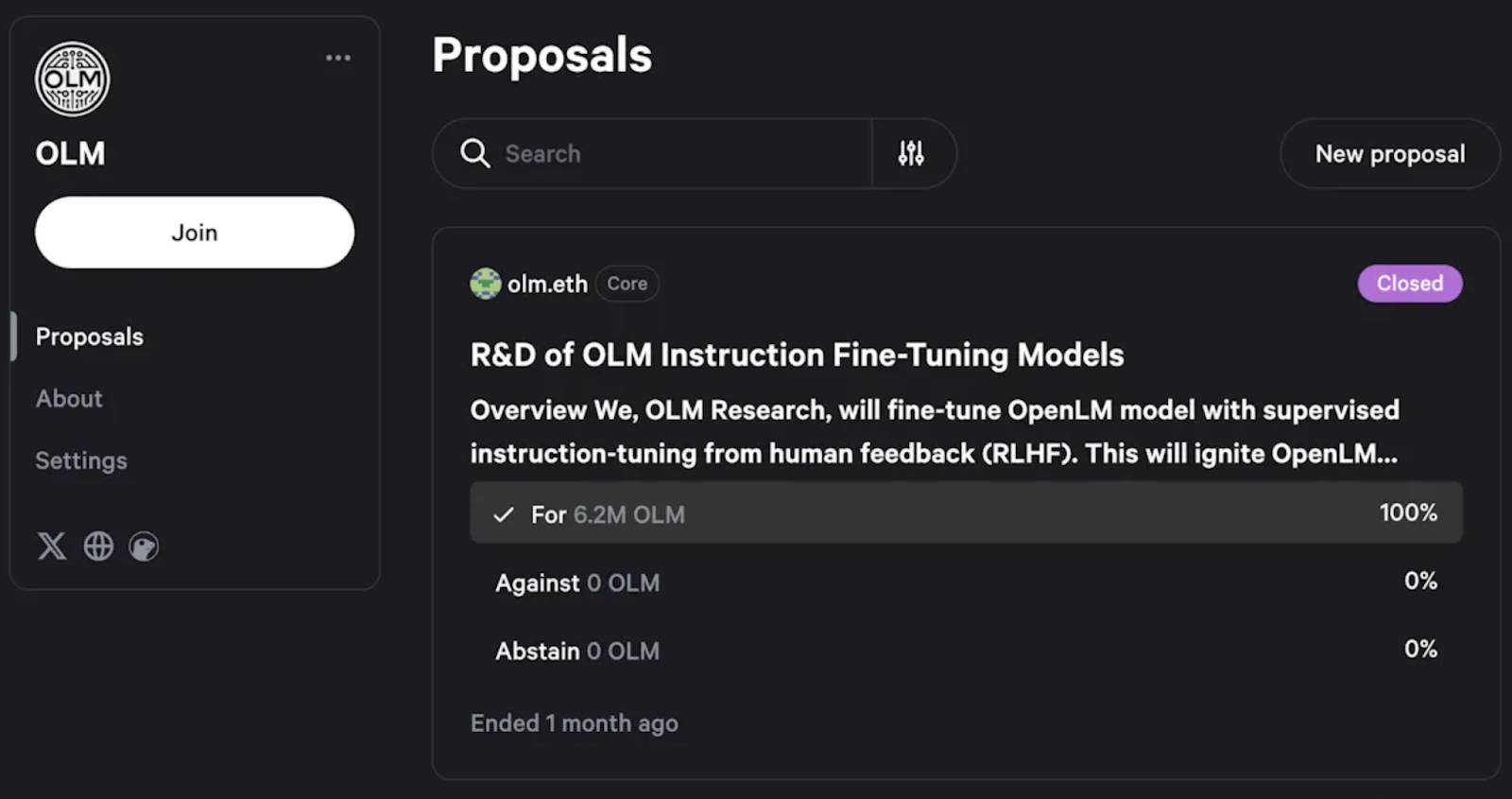

2. 驱动:社区自赋能,去中心化是关键

OLM Research和OLM DAO是“IMO后”的两个社区自组织,体现了IMO概念中的“去中心化”和“开源开发精神”。

OLM的全开源属性,让所有人都能在其人工智能模型和其他基础上进行研发,从而激励社区为持续发展做出贡献。

OLM由社区和贡献者驱动,真正实现去中心化运营。这个显著特征突显出去中心化和协作精神,引领OLM之路迈向成功。

3. 研究:AI模型也在不断进步

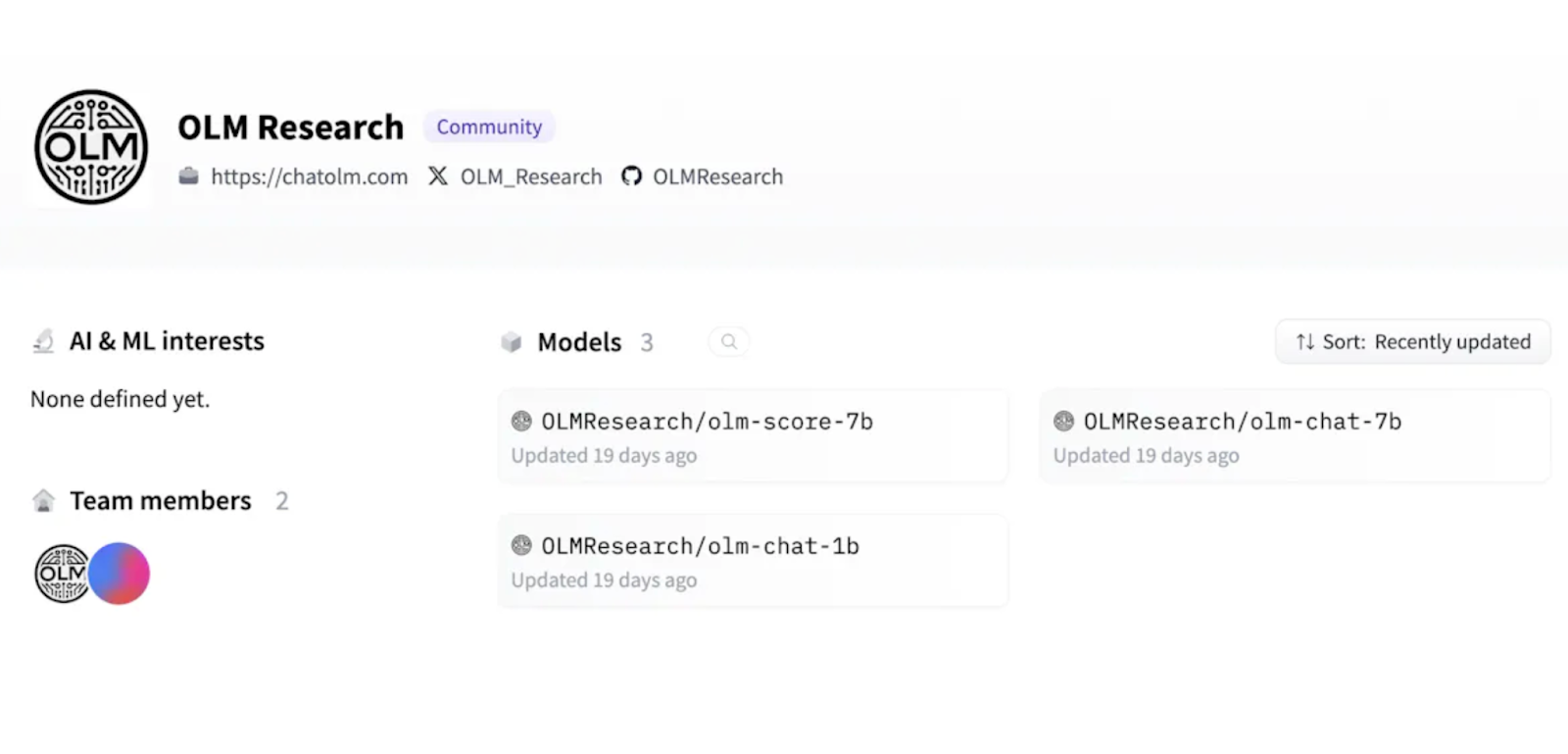

近期,OLM Research在人工智能模型开发方面取得了重大进展。在OpenLM初始模型基础上,取得的两项进展如下:

-

优化Open_LM模型:通过注意力机制(Attention Mechanism)和数据处理(Data Handling)升级了 OpenLM 模型。

- 引入微调模型(Fine-Tuned Models):基于OpenLM,引入微调模型(1B和7B open_lm Chat Models以及 (A.I.)location AI Model)。

4. 产品力Max的ChatOLM——去中心化AI聊天机器人

有了之前的工作为基础,OLM Research进一步推出ChatOLM——一款由$OLM链上人工智能驱动的去中心化AI聊天机器人。

ChatOLM由微调模式OpenLM模型驱动,还具有抗审查性,它利用以太坊将人工智能推理分配给ORA的OAO驱动的去中心化ORA节点。

这个案例证明了OLM Research对衍生产品的开发能力以及交付能力。产品上线一个月后,就积累达8,000次以上的链上使用。

5. ORA 的贡献:不可或缺的中坚力量

ORA的支持,让OLM社区更加繁荣和去中心化,也给OLM的成功保驾护航:

-

维护开源opML和OAO框架,为OLM的IMO提供技术基础设施

-

将OLM开发的模型集成到Onchain AI Oracle(OAO)中,把OLM开放给区块链上的所有用户

-

在与OLM相关的模型活动中,奖励ORA积分,鼓励用户使用和参与其中,孵化去中心化的人工智能生态系统。

6. 展望未来,潜力无限

OLM 的旅程证明了IMO的革新潜力,随着OLM Research的持续创新,去中心化人工智能的未来将更加可持续和社区驱动。IMO让所有人能够以去中心化的形式投资AI,推动了整个AI行业的革新。我们也期待OLM社区与开源AI创新不断发展。