4月28日,曦智科技-P(01879.HK)正式在香港交易所主板挂牌上市,成为全球AI硅光芯片第一股,亦成为全球光电混合算力赛道首家登陆资本市场的公司。

曦智科技此番成功上市,不仅让上海企业在资本市场再下一城,也为本地AI芯片阵营注入了新的强大动能。

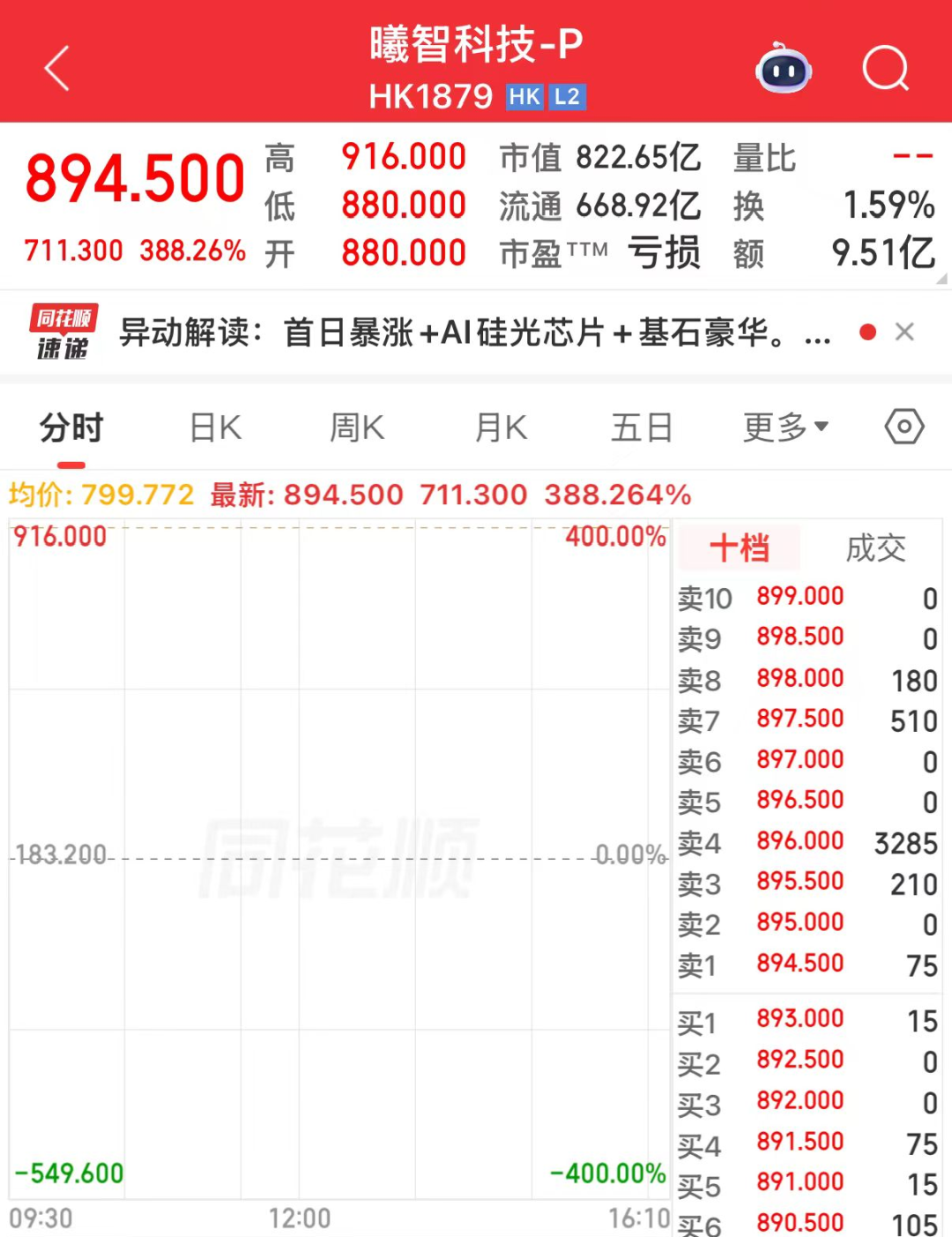

上市首日,曦智科技开盘价为每股880港元,较183.2港元发行价上涨380%。截至发稿,公司股价达到894.5港元/股,对应市值超822亿港元,延续了公司招股阶段近5800倍认购的市场热度。

曦智科技表示,借助公开市场融资,公司将加速技术迭代与产品落地,夯实人工智能算力底座,推动前沿硬科技成果商业化普及。

用“光”为AI时代注入新动能

公开信息显示,曦智科技成立于2017年,由麻省理工学院物理学博士沈亦晨创立,是全球光电混合算力领域的技术及商业化先行者。

谈及股票代码“01879.HK”,曦智科技创始人兼CEO沈亦晨对记者表示,1879年是极具里程碑意义的年份:爱迪生发明白炽灯,光开始引领第二次工业革命的前进方向。同年,经典电动力学创始人麦克斯韦逝世,伟大的物理学家爱因斯坦诞生。以“1879”致敬先驱,公司致力于用光的技术为人工智能时代注入新的力量。

当前,全球人工智能产业对算力的需求呈指数级增长,与此同时,传统数据中心在带宽、功耗与延迟方面都面临瓶颈,算力供给与市场需求间的缺口持续拉大。在此背景下,光电混合算力通过引入光学能力进行数据处理与传输,被视为算力基础设施演进的重要技术方向之一。

根据弗若斯特沙利文数据,曦智科技凭借光互连与光计算两大产品线,已成为全球首家实现光电混合算力大规模部署的公司。2025年,在中国独立Scale-up光互连解决方案市场中,曦智科技按收入计算排名第一,市场份额约为88.3%,为多个千卡级GPU集群提供支持。公司光计算芯片全球累计出货量连续两年位居第一。

曦智科技表示,本次上市募集资金将精准聚焦核心主业研发与技术升级,长效推动公司近封装光学(NPO)、共封装光学(CPO)、PACE 3光电混合计算加速卡等核心项目落地。

根据公司规划,公司70%的募集资金将用于未来五年研发投入:其中35%聚焦光互连业务,重点攻坚高端硅光芯片设计、高速光电传输等核心技术;另外35%投入光计算领域,集中资源迭代并研发下一代光电混合计算卡,加速落地商业化。凭借光电融合创新,曦智科技将持续为全球AI产业输送高效、低耗、可规模化的底层算力支撑。

认购倍数近5800倍

光互连与光计算分别对应算力体系中的“连接”与“计算”两大核心环节。前者通过以光信号替代传统电信号,实现GPU、CPU及各类加速芯片、交换机与存储设备之间的高速互连;后者则以光子替代电子,尝试在底层计算范式上实现突破。

根据弗若斯特沙利文的资料,到2030年,中国Scale-up光互连与光计算市场规模预计将分别达到1805亿元与14.62亿元。在光计算市场,截至2025年,光计算芯片在中国AI推理芯片中的市场渗透率少于0.5%,预计到2040年将达到20%。

广阔的市场前景及标的稀缺性,让曦智科技获得了全球资本市场的高度认可,公司国际发售与公开发售整体认购倍数亮眼。基石名单集阿里巴巴、GIC、贝莱德(BlackRock)、富达国际(Fidelity International)等20家全球机构,阵容亮眼,合计认购2.099亿美元(约16.44亿港元),占发售股份比例高达68.14%。认购倍数与基石认购比例在近年港股IPO市场中均居于前列。

富达国际表示,曦智科技是全球少有的真正实现光电混合算力规模化商业落地的企业。作为长期基本面投资者,富达国际始终寻找具备非线性增长潜力的颠覆性技术企业。曦智科技“光互连+光计算”双轮驱动的模式,不仅解决了当下AI集群的互连痛点,更通过光计算为下一代算力打开想象空间。这与富达国际看好AI基础设施长期机会、精选具备核心科技护城河企业的投资策略高度吻合。富达国际将持续以长期视角关注公司发展,并期待曦智科技借助资本市场力量不断推进技术创新、产品迭代与全球化布局,持续引领全球算力革命,成为下一轮全球算力架构升级的重要参与者。

中国移动链长基金表示,作为曦智科技IPO前的战略投资人及本次发行的基石投资人,中国移动链长基金热烈祝贺公司成功登陆港股。算力是数字经济的核心引擎。面对AI时代日益突出的功耗与带宽挑战,探索光电融合等新型计算路径,已成为产业界的共同课题。中国移动作为全球规模最大的通信运营商和信息技术产业链链主,不仅看重曦智的长期成长潜力,更愿意开放场景与资源,推动光电计算技术从实验室走向规模化产业应用。公司期待与曦智携手,共同为数字经济的可持续发展筑牢更有竞争力的算力底座。