Source: Bankless

Author: David Christopher

Compiled and Edited by: BitpushNews

The debate between Coinbase and Robinhood has been discussed many times by many observers—including us.

But the system update released by Coinbase on December 17th gives us a reason to revisit this topic in depth. The company announced the launch of 24/5 commission-free stock and ETF trading, native prediction market integration via Kalshi, and a decentralized exchange (DEX) aggregator providing instant access to millions of tokens—a clear step towards becoming an "everything app" that can rival the breadth of Robinhood.

These announcements clarify the future Coinbase is building and allow us to compare it more comprehensively with Robinhood. Their competitive goal is now unmistakable: to become the single platform for users to manage their entire financial lives. By mastering users' fund balances, they aim to master user behavior. But the way they are building this "super app" theory reveals two very different philosophies–and 2026 will test which foundation is more solid.

HOOD (Robinhood)

Robinhood is building the financial super app the old-fashioned way—by continuously stacking products until users can manage their entire financial lives on one platform.

In addition to stock, options, and cryptocurrency trading, Robinhood offers its 3.9 million Robinhood Gold subscription users a suite of products that give it functionality comparable to a digital neobank. This subscription service, which grew 77% year-over-year, bundles a 3% cash-back credit card, 3.25% cash interest, and a 3% IRA (Individual Retirement Account) match. Users' salaries, savings, investments, and daily spending are all concentrated in the same interface—a data advantage that traditional brokerages cannot match.

This positioning seems particularly relevant when you consider demographics—75% of Robinhood's 26.9 million funded customers are under the age of 44, a highly mobile-first and "financially conscious" user base. As argued by Omar Kanji of Dragonfly and others, this foundation helps position the company to be a major beneficiary of the expected over $10 trillion wealth transfer over the next decade, as older generations pass assets down to younger ones. These inheritors are likely to consolidate assets into the platforms they use every day—and Robinhood is making itself very suitable for daily use.

Beyond digital banking features, Robinhood's revenue sources are already quite diversified. Options trading remains its "cash cow." Cryptocurrency contributes 21% of total revenue. Net interest income accounts for 35% of revenue. And the prediction market business conducted through Kalshi has reached an annualized revenue of $100 million.

The data supports this:

-

Transaction-based revenue increased 129% year-over-year, primarily driven by cryptocurrency.

-

Q3 net profit reached a record $556 million—a 271% increase year-over-year.

-

Operating expenses have remained flat since September 2022.

COIN (Coinbase)

Coinbase is also building a super app—but with a distinct "crypto-native" flavor and an underlying Layer 2 ambition.

On the front end, Coinbase wants to be the single place for users to manage their on-chain and off-chain financial lives, although it is still primarily focused on the former for now. The December system update made this clear: 24/5 commission-free stock and ETF trading, prediction markets via Kalshi, and ongoing on-chain integrations for instant access to millions of tokens. Add in direct deposit, high-yield savings via USDC lending rates, borrowing up to $5 million against BTC (up to $1 million against ETH), and earning crypto rewards for spending with a debit card—the pieces of the super app are falling into place.

While cryptocurrency prices have fallen, the builders and deliverers are still in action.

However, Coinbase is not just building products for its own users. Its grander vision seems to be turning every product it offers into plug-and-play infrastructure that powers all other institutions coming on-chain.

The theory here is that TradFi giants like JPMorgan, Fidelity, and Morgan Stanley will not build their own crypto infrastructure. They will outsource to Coinbase because it's cheaper, they lack the technical expertise, and Coinbase has 13 years of proven security. Over 200 institutions are already using Coinbase's "Crypto as a Service" platform—meaning users might be trading crypto on the front end of a traditional bank, but Coinbase is handling everything behind the scenes.

This focus on infrastructure extends across the business. Coinbase holds Bitcoin and Ethereum for most major spot ETFs—a near-monopoly position in crypto custody. They are allowing institutions to leverage Coinbase's infrastructure to issue their own stablecoins. The acquisition of Echo brought financing and token issuance in-house. And the acquisition of Deribit captured about 90% of Bitcoin options open interest.

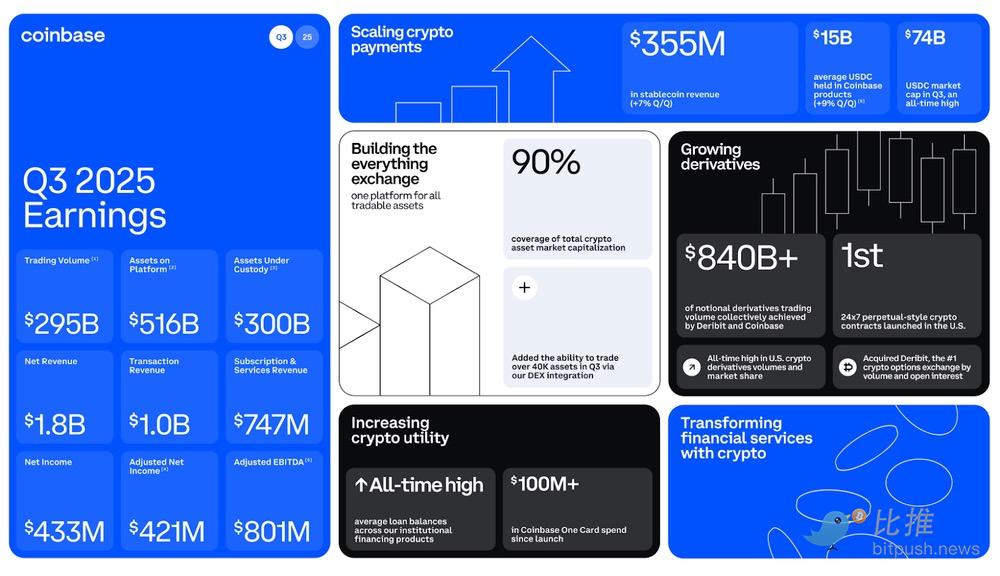

The revenue structure reflects this dual focus. Q3 2025 revenue was $1.8 billion, with subscription and service revenue hitting a quarterly record of $747 million (41% of total revenue). Stablecoin revenue from the USDC partnership contributed $354.7 million, up 44% year-over-year. Staking brought in $185 million. Custodial assets, driven by ETF inflows, exceeded $300 billion, with custody fees reaching approximately $143 million.

Robinhood's grand vision is to be the go-to place for handling all matters of personal financial life, while Coinbase is playing two games at once: building the best crypto super app for its own users, while simultaneously becoming the backend that powers the crypto products for everyone else.

Diverging Crypto Strategies

Both companies see cryptocurrency as core to their super app ambitions, but their approaches reflect their origins.

Robinhood treats cryptocurrency as just another asset class alongside stocks and options. It is a revenue driver that fits perfectly into the existing product suite. The acquisition of Bitstamp ($200 million) provided it with global licenses and institutional infrastructure. Tokenized equities—currently around 800 listed in the EU, including private companies like OpenAI and SpaceX—expand the product offering. The real test will be the success of the Robinhood Chain, which should make many of these tokenized equities more fungible (e.g., for loans), although we currently have few details on the extent of "DeFi" or other on-chain activities the chain will support.

Beyond that, Robinhood faces more immediate limitations, such as token selection. In the US, users have access to fewer than 50 tokens on the platform, while Coinbase offers nearly unlimited tokens indirectly (via Jupiter and Base) and directly supports over 200.

Coinbase's cryptocurrency approach is clearly different, offering everything from its own Layer 2 network to the various products mentioned in the previous section. It has set the standard for "crypto-specific" products to the point that it now seems to be pivoting to focus on building the rails for others to use. We see x402, aimed at becoming the industry standard for agent-to-agent (A2A) payments, and Coinbase's announcement that it will offer a "Stablecoin-as-a-Service" platform for companies to create whitelabel stablecoins, with Coinbase managing all the complexity. From issuance to trading to custody, Coinbase occupies every stage of the asset lifecycle.

2026 Outlook

The roadmaps for both companies are very aggressive—and increasingly overlapping.

Coinbase's December 2025 system update, with stock and ETF trading beyond traditional market hours (thanks to tokenization) and the announcement of stock perps launching next year, strongly encroached on Robinhood's territory. Native Kalshi integration brought prediction markets. Then there's Coinbase Business and Coinbase Tokenize, the former an all-in-one crypto-powered business operations platform, and the latter an "end-to-end" platform for institutional tokenization.

Robinhood's 2026 plans delve deeper into crypto infrastructure. Tokenized stocks will achieve 24/7 trading via Bitstamp in early 2026 and become withdrawable and composable in DeFi by late 2026. In prediction markets, Robinhood is moving from a distribution partner to launching its own market. The platform hopes to offer crypto staking, pending regulatory approval. It also has ambitions to "socialize" trading with Robinhood Social, an upcoming feed where traders can post content and display their actual trades and P&L. And of course, there's the Robinhood Chain.

The challenge for the Robinhood Chain will be building a developer ecosystem—an area where Base has already built momentum. Crypto-native culture is hard to manufacture artificially.

Conclusion

Perhaps a better framework here is "COIN and HOOD," rather than "COIN vs. HOOD." These two companies occupy different lanes, touching but not fully overlapping.

Robinhood is both a "super app" bet and a demographic wealth transfer bet. With 75% of its users under 44 and a full-stack digital bank keeping assets on the platform, the company is poised to become a new hub for deposits, spending, investing, and speculation.

Coinbase is a bet on a technological transition. It bets that the global economy is moving on-chain, and Coinbase will be the infrastructure layer that powers everyone else—from ETF custody to stablecoin backends to crypto-as-a-service for traditional banks.

Both face risks. Robinhood's generous Gold incentives (3% match, 3% cash back, 3.25% cash interest) are costly and have already shown vulnerability to rate cuts—the rate was recently 4-5% and is directly tied to the Fed rate. Adoption of tokenization depends on issuer decisions, which are beyond Robinhood's control. For Coinbase, user growth remains a significant risk, with its monthly active user count stagnating since 2021.

Moreover, both stocks may already be at high levels. Over the past few years, these two stocks have been major market winners—as of this writing, Coinbase (COIN) is up about 7x from its 2022 lows, and Robinhood (HOOD) is up 15x. Although they have pulled back from recent all-time highs, their valuations remain elevated after such staggering gains. This is worth investors pondering.

Ultimately, while both companies are building financial super apps—and encroaching on each other's turf in the process—their visions actually serve different goals.

-

Robinhood is committed to building an all-in-one financial platform—allowing users to manage all aspects of their financial life, from banking and daily spending to trading and investing, all in one place without leaving the platform.

Coinbase focuses on building the infrastructure to get everyone on-chain—it does build a crypto super app for its own users, but more importantly, it is becoming the backend rails that financial institutions, fintech companies, and even traditional banks rely on when entering the crypto space.

One aims to be your financial home, the other aims to be the plumbing underneath everyone's financial home. Both could succeed.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush