Original | Odaily Planet Daily (@OdailyChina)

Author | Wenser(@wenser2010 )

Polymarket's deceptive marketing has finally caught the attention of regulatory authorities.

Recently, the U.S. Commodity Futures Trading Commission (CFTC) has initiated a broad investigation into the prediction market platform Polymarket, covering its business activities including social media campaigns. Previously, U.S. Republican Senator John Curtis and Democratic Senator Adam Schiff co-signed a letter to CFTC Chairman Mike Selig, urging an investigation into Polymarket's practices of paying KOLs for deceptive marketing and using fraudulent marketing tactics to promote gambling-like products to American audiences.

At a time when the World Cup is driving a surge in prediction market trading volumes, this move may pour cold water on the development of this sector. More importantly, the CFTC's investigation into Polymarket has brought to light conflicts of interest between U.S. federal and state authorities, as well as between officials and capital. (Recommended reading: "WSJ: Fake Websites, Fake Trades, Real Promotion, Polymarket's Traffic Scam").

End of the Wild West Era for Prediction Market Marketing, Regulatory Policies May Enter Deep Waters

If the earlier incidents involving Polymarket—such as university students posting fake profit videos and paid KOLs exaggerating prediction profits—were seen as the wild attempts of the early expansion phase of prediction markets, then the formal CFTC investigation is clear proof that this wild growth period is over.

Prediction Market Platform Data Sees Explosive Growth, Attracting Strong Attention from Traditional Internet Giants

As we entered June 2026, with the official start of the World Cup, prediction markets have received unprecedented attention, leading to a continuous rise in trading volumes.

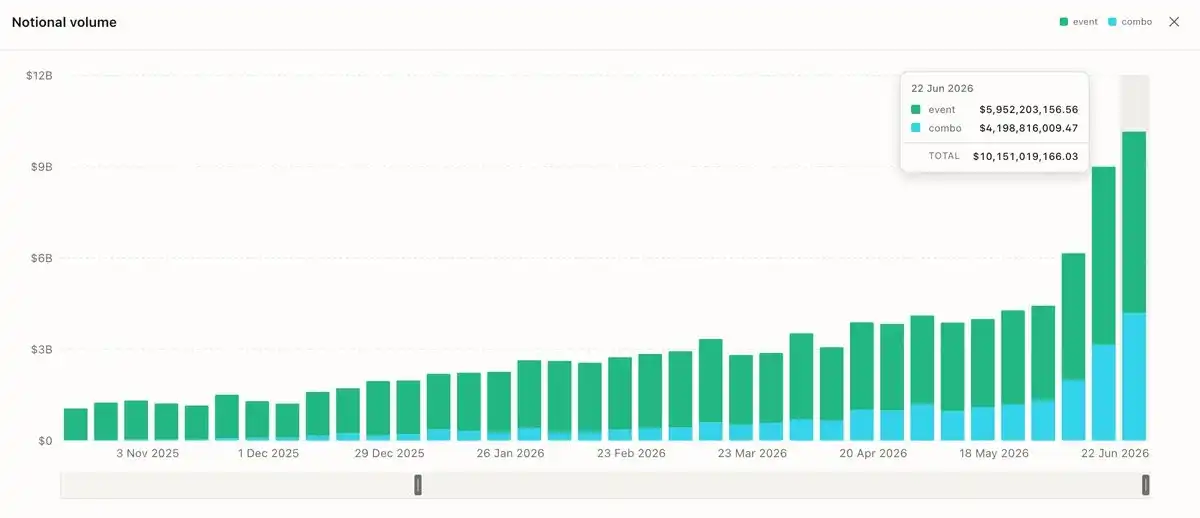

Data from a16z crypto shows that prediction market trading volume has hit record highs for three consecutive weeks. The total market trading volume reached a historic first of $144 billion last week, a significant increase from approximately $50–60 billion at the beginning of the year. The previous record high of around $100 billion was set just the week before. From the platform side, the data has also seen substantial growth:

- Latest data shows Kalshi's weekly notional trading volume surpassed $100 billion for the first time.

- Polymarket officially stated that its annualized revenue has significantly exceeded $1 billion, a development occurring just six weeks after the removal of the waitlist for its U.S. trading platform; data shows that the U.S. platform's daily trading volume grew from about $50 million in mid-May to over $200 million on June 20 (based on Dune Analytics data).

- Robinhood's prediction market platform business is growing rapidly, with annualized revenue reaching $500 million. In Q2 as of June 25, Robinhood's active contract trading volume was approximately 12.3 billion contracts. Based on a standard rate of 1 cent per contract, the prediction market revenue for this quarter is estimated to be at least $123 million. Its recently launched Rothera prediction market platform achieved over 900 million contract trades in its first week, contributing nearly 60% growth in active contract trading volume for Robinhood.

Such impressive data has also attracted the attention of stock market giant Meta. According to media reports, Meta CEO Mark Zuckerberg has urged the company to explore partnerships with prediction markets Polymarket and Kalshi. Meanwhile, Meta is developing a similar prediction market application called Arena.

All signs indicate that prediction markets have leapt from a niche sector a few years ago to a hot industry experiencing exponential expansion. In the face of this trend, regulatory authorities are unlikely to stand idly by. The recent deceptive marketing incidents at Polymarket serve as a timely and fitting 'soft knife,' providing an opportunity for regulatory intervention. The author believes that subsequent regulations may gradually clarify the boundaries for prediction market platforms regarding marketing, event contract content, and trading fees, aiming to strengthen investor protection and clearly distinguish them from traditional gambling businesses.

Simultaneously, as the investigation deepens, the power struggle between federal regulatory agencies represented by the U.S. CFTC and state-level regulators is also coming to light.

When U.S. CFTC and Nine U.S. States Lock Horns: The Battle for Prediction Market Regulatory Power

Last Tuesday, the U.S. CFTC formally filed a lawsuit against Kentucky, attempting to reaffirm the agency's jurisdiction over prediction market platforms.

In the complaint filed with the U.S. District Court for the Eastern District of Kentucky, the CFTC stated that Kentucky's attempt to shut down federally regulated designated contract markets interferes with the federal regulatory system Congress established for the national swaps market. It claims "exclusive jurisdiction" over related event contracts and prediction market products.

Previously, Kentucky sued platforms like Kalshi and Polymarket, accusing them of operating unlicensed illegal sports betting and gambling businesses within the state. As of June, over 12 U.S. states, including Kentucky and New York, have taken legal action against Polymarket and Kalshi, alleging they operate illegal sports betting. Kentucky has become the ninth state sued by the CFTC in the prediction market regulatory dispute.

This action highlights the escalating conflict between federal derivatives regulation and state-level gambling regulation.

There are two main reasons behind this dispute:

- First, the practical interests of state and local gambling industries, such as tax revenue. Traditional sports betting previously brought significant tax revenue to various states (e.g., high-tax-rate online gambling). If prediction markets completely replace the gambling industry, potential tax losses for states could amount to hundreds of millions of dollars annually (one estimate is around $600 million).

- Second, the definition of the regulatory boundary between the gambling industry and prediction markets as an emerging industry. The CFTC seeks to maintain the classification of "event contracts" as commodity derivatives, futures, or swaps, enforcing a policy of federal law preemption.

The final outcome and specific definitions may depend on the interpretation and rulings by state courts, and potentially the U.S. Supreme Court, regarding the Commodity Exchange Act (CEA).

Furthermore, the battle between exchanges and the U.S. CFTC has also ignited. The CFTC's previous approval of Kalshi's application for perpetual futures trading triggered CME's lawsuit—

Reportedly, CME has sued the U.S. Commodity Futures Trading Commission and its Chairman Michael Selig in the U.S. District Court for the District of Columbia. Regarding the CFTC's May 29th approval for prediction market platform Kalshi to launch perpetual futures contracts linked to the Bitcoin spot price, among other actions, the CFTC's treatment of "futures" with expiration dates as "swaps" violates U.S. Congressional directives and the Commodity Exchange Act. CME requests the court to overturn the related perpetual futures actions. CME also claimed that Selig acted unilaterally without the presence of the full five-member panel of commissioners.

A CFTC spokesperson responded that CME is waging a "legal war" against the agency and the government's crypto policy, stating that "the act of filing the lawsuit is extremely imprudent." (Essentially saying "your lawsuit is filed too hastily" right on its forehead.)

Of course, it's no wonder CME is so agitated. The CFTC's move to allow Kalshi to trade crypto perpetual futures contracts essentially lets prediction market platforms like Kalshi, along with crypto exchanges like Coinbase and Kraken, encroach upon CME's "trading territory." As for the driving force behind this, it might have some connection to the Trump family.

The Trump Family's Prediction Market 'Double-Down Strategy': Don Jr. Bets on Kalshi and Polymarket

Recently, it was revealed that Kalshi is negotiating a new round of funding at a valuation of approximately $40 billion, with the deal potentially closing as early as Q3. Following a $10 billion financing round in May (investors included Sequoia Capital, Andreessen Horowitz, Coatue, and Morgan Stanley), Kalshi's valuation rose from its previous $12 billion to $22 billion. Now, that number is about to double.

Kalshi CEO Tarek Mansour stated that the company is considering an IPO no earlier than late 2027 or 2028. Kalshi officially stated that as of April 2026, its annualized trading volume reached $178 billion, a 32-fold increase year-over-year.

Such remarkable market data and the high enthusiasm from capital markets are hard to separate from one of the Trump family's prominent figures, Donald Trump Jr.

It is understood that Don Jr. is essentially "hedging his bets" in the prediction market sector:

On one hand, he served as a paid strategic advisor for Kalshi in early 2025, receiving approximately $300,000 worth of company equity at a time when Kalshi's valuation was less than $2 billion. That investment alone has yielded over a 10x return;

On the other hand, he also serves as an advisor to Polymarket and has made a strategic investment in the latter through his venture capital firm, 1789 Capital, where he is a partner.

Coupled with Trump's previous emphasis on federal government regulatory authority over prediction markets, and his mention that "Kalshi and Polymarket will thrive under his leadership,"

To some extent, the conflict of interest between capital and official regulatory agencies has been eased; and the Trump family serves as the "best lubricant" in this contradictory situation.

Thus, a network of interests connecting the U.S. CFTC and other federal regulatory agencies, U.S. state governments, and Trump family investment entities gradually takes shape.

As for the U.S. CFTC's investigation into Polymarket, it may just be an inevitable step in regulating the prediction market industry.

The era of wild growth, the 'Spring of Prediction Markets,' is coming to an end, while the 'Prosperous Summer' for the prediction market industry is slowly approaching.