Author: Tidal Investment

I. The Market Has Switched Scripts

Recently, the market has been both excited and a bit nervous. SpaceX completed a massive $750 billion IPO, and OpenAI and Anthropic are also rumored to be preparing for listings. At the same time, Alphabet is planning an $800 billion equity financing round, and Meta is also arranging new funding.

Honestly, seeing so many giant companies asking the market for money simultaneously can unsettle almost anyone. But interpreting this wave as the peak of AI is too simplistic; it's more like the AI drama has flipped to the next scene.

Over the past two years, the market bought into demand explosion and industry imagination, wondering if AI was viable. By 2026, the question became: How long can this massive investment intensity be sustained?

Wu Shaokang, founder of Tidal Investment, says: "The market always sees the fast-moving variables, but what determines the direction of a cycle are often the slow-moving variables."

Standing in mid-2026, we remain bullish on the AI industry chain. But today's optimism can't be sustained by imagination alone. Talking about AI two years ago, you could talk about models, AGI. But talking about the same things today may not satisfy the market.

II. Money Is Flowing In, And It's Becoming More Aggressive

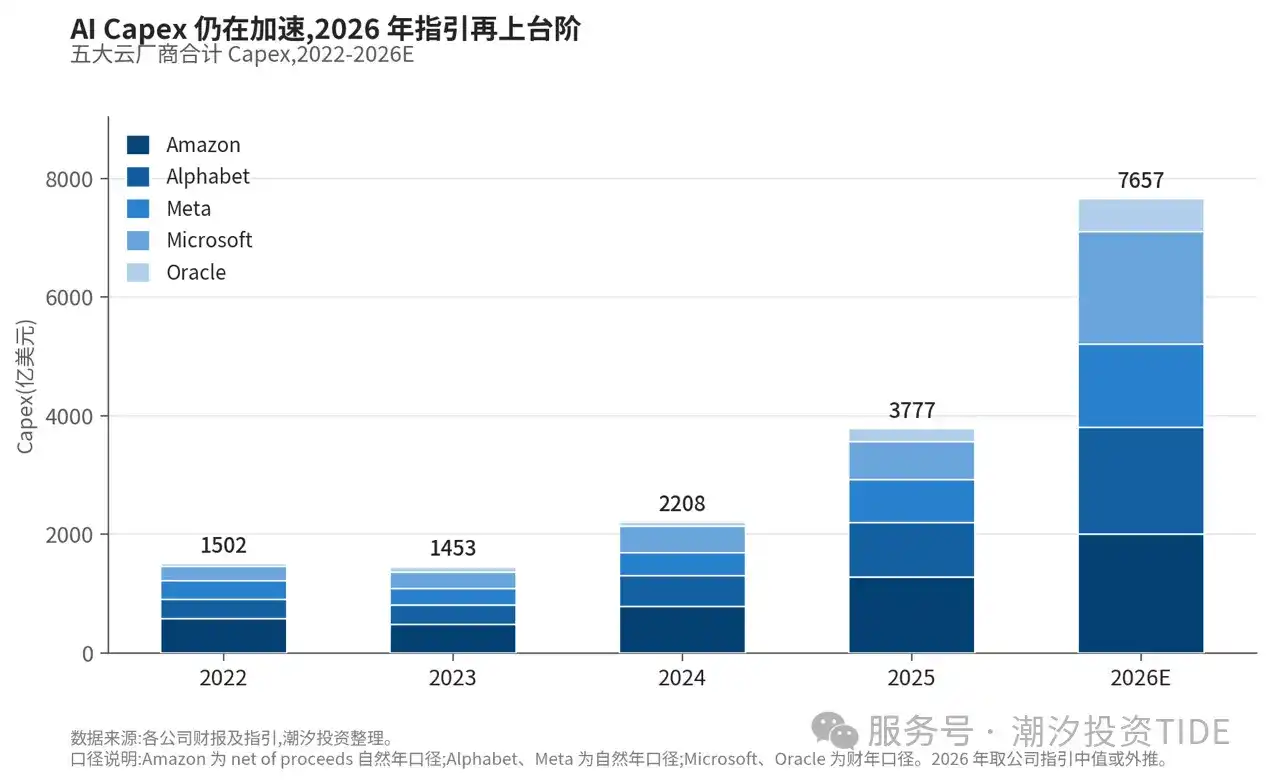

How do you judge if a cycle has run its course? See if those spending are still spending. Flipping through the books of the five major cloud providers, the answer is quite clear.

-

Alphabet: 2025 Capex $90 billion, 2026 guidance raised to $180 billion.

-

Amazon: 2025 Capex $130 billion, 2026 guidance raised to $200 billion.

-

The other three are also moving in the same direction: Meta 2026 guidance raised to $140 billion, Microsoft to $190 billion, Oracle FY26 already close to $60 billion.

Laying out these numbers is a bit daunting. In the past, the greatest strength of these internet giants was considered their strong cash flow and ample reserves. But now, even they are proactively reaching out to the market for more funding in the face of AI. Besides that $80 billion equity financing, Alphabet also issued a significant amount of debt over the past year. AI infrastructure has become so large that even companies with the best cash flow need to restructure their capital.

Money is still flowing in, no doubt about that. The question is, how long can this spending continue?

III. Why This Investment Cycle Won't Stop

What are people most afraid of? Capex peaking, and this cycle running its course in two or three years like past tech hardware cycles, followed by a long digestion period. Servers, phones, PCs—many hardware cycles play out like this: demand picks up, then capacity expands, inventory piles up. Once downstream slows, the entire chain faces valuation compression.

This concern is valid in past cycles. But this AI Capex cycle might not be so simple.

First, the money is being thrown at too many places. Cloud providers' money is all labeled Capex, but when broken down, they're completely different: compute, memory, networking, power—each layer has its own expansion rhythm and bottlenecks. And with engineering, once it starts, stopping halfway is often more costly than pushing through.

More crucially, bottlenecks are shifting from chips down to more physical constraints. Chip shortages can be addressed by expanding production, but expanding production for power, transformers, high-power density cabinets isn't as fast. Just getting grid access can often mean waiting in line for years.

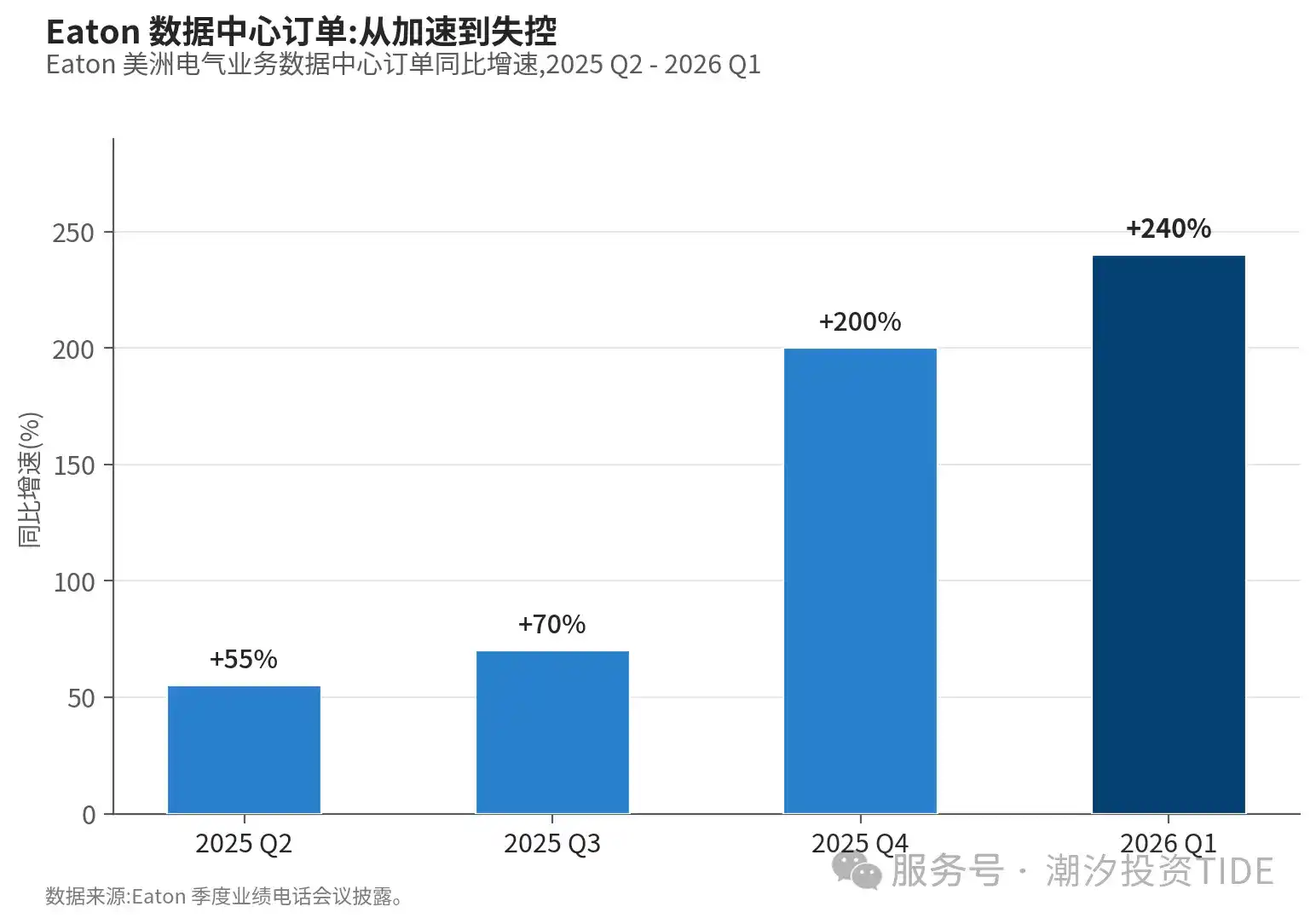

And Capex is no longer just about GPUs. Clear signals from the supply chain show this: Eaton, which makes power distribution equipment, saw a 240% year-over-year increase in data center orders in Q1 2026.

Orders for transformers, UPS, liquid cooling, thermal management, cabinet integration—these only surge in large volume when cloud providers decide to build campuses. The simultaneous explosion of these orders indicates solid construction progress underpinning this Capex cycle.

Looking at these factors together, you realize this investment cycle won't stop easily.

IV. What the Market is Actually Worried About

Bullish as we are, the market has two concerns right now we can't ignore.

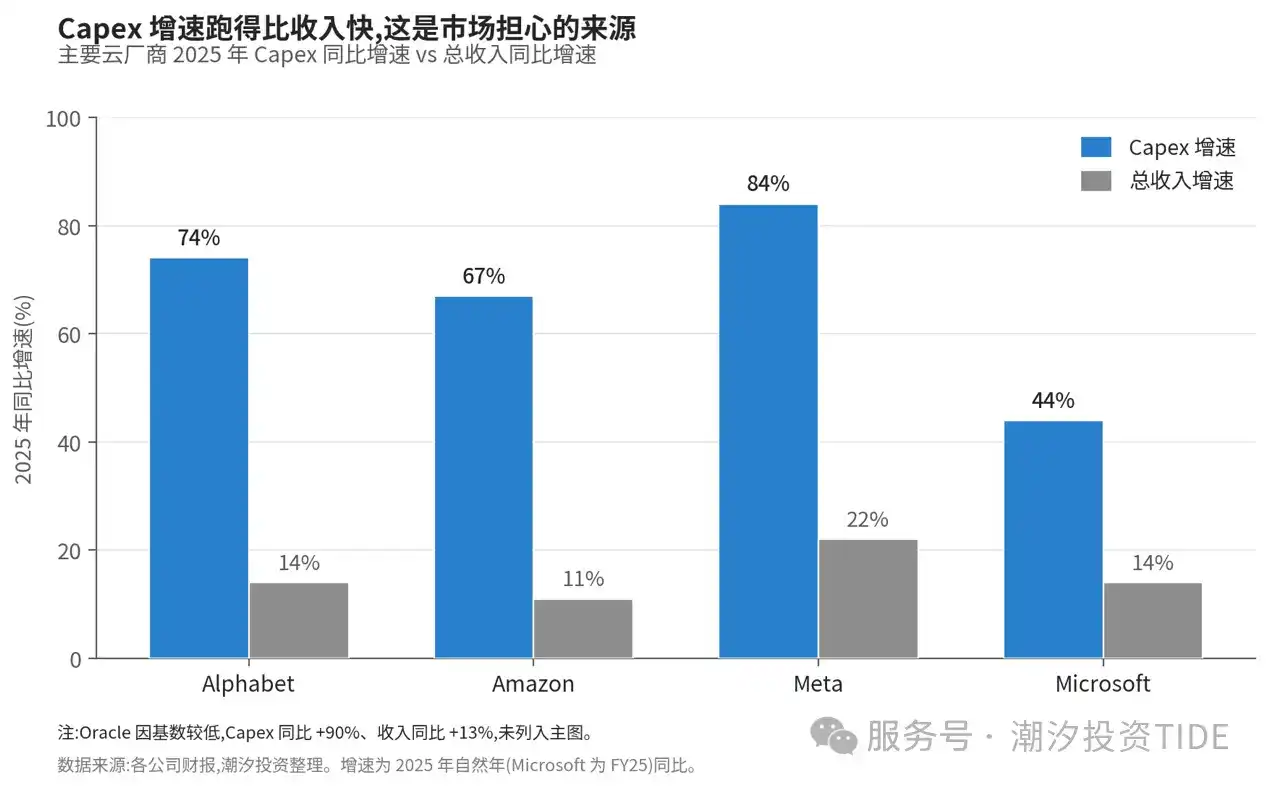

Concern 1: Capex Growth Outpacing Revenue Growth - Can ROI Be Realized?

For the five major cloud providers in 2025, Capex growth rates all outpaced revenue growth. Alphabet's depreciation rose from $15.3 billion in 2024 to $21.1 billion in 2025, a 38% increase in a year, hitting the income statement hard. Amazon spelled it out in its earnings report: FCF decline was due to AI investment driving up PPE.

A popular saying in the market is that when Capex growth exceeds revenue growth, it signals peaking ROI. This isn't wrong, but applying it to the cloud computing business is somewhat simplistic. AWS, Azure, GCP all went through phases in the early 2010s where Capex far outstripped revenue, eventually recouping the money through scale-based monetization. The difference with this AI Capex cycle is the higher capital intensity; payback depends on whether future AI workloads can be monetized.

Of course, we're not bullish with our eyes closed. To change our view, we'd need to see at least a few things happen: cloud providers start lowering Capex guidance, orders get canceled or postponed, or AI product revenue and usage fall below expectations. As of mid-2026, none of these have happened yet.

ROI risks certainly exist, but current facts lean more towards the bullish side. Wait until the data actually starts to decline before changing judgment; we're not at that point today.

Concern 2: Is This Another 2000?

How did the 2000 bubble actually burst? Back then, demand was also growing, with more people going online and traffic increasing year by year. The problem was on the supply side.

A popular saying then was that internet traffic doubled every 100 days. Telecom companies believed this curve and laid fiber furiously along railways and roads. There was a cost advantage with fiber: dig a trench once, and laying more cables didn't cost much more, so they simply filled it with capacity for over a decade. Dozens of companies dug their own trenches simultaneously, resulting in supply far exceeding demand. Consequently, the price of buried fiber crashed. By the time traffic grew to fill it, a decade had passed, and those original companies couldn't survive that long.

Of course, there are bubble elements in this cycle too. No major cycle is clean; there are always companies riding the AI wave and some investments that will seem excessive in hindsight.

But on the supply side this time, it's the opposite, because what AI needs isn't as simple as laying a pipe. Transformers are customized heavy equipment, constrained by silicon steel and lengthy approval processes. Grid access also can't be parallelized like digging trenches; you must queue behind the public grid, often for years. More importantly, electricity can't be pre-laid like fiber; you can't lay down electricity for the next decade and just wait for it.

So the 2000-style collapse is difficult to replicate this time.

V. The AI Show Isn't Over

Just recently, SpaceX plummeted from its highs, even falling below its IPO closing price, making the market nervous again. Seeing so many giants asking the market for money simultaneously easily makes one nervous, wondering if AI has peaked.

But we don't see it that way.

The reason giants are raising large funds now is that the show must go on, and the hurdles ahead are growing. Look at those five cloud providers—none have lowered their 2026 Capex guidance; all have raised it. Looking further ahead, transformers take four years to deliver, data centers wait years for grid access. These hurdles probably can't be easily overcome by just spending more money.

So a massive wave of fundraising, while daunting, is essentially just an intermission.

Don't rush to call the peak. The AI show isn't over yet; it's just switched to a different script.