Author | Freddy

Data Support | GOGU Big Data

This year, within the global AI supply chain, not only have the core giants completely triumphed, but second, third, and fourth-tier supporting small and medium-sized enterprises have also feasted on the spoils. Even some companies whose businesses seem to have little to do with AI have been wildly hyped and soared in value.

In Japanese and Korean stock markets, a group of old-school manufacturing firms have seen their gains leave many AI concept stocks in the dust.

Toto, famous for bathroom fixtures, hit a five-year stock price high, rising 145% over the past year.

What drove this revaluation wasn't its century-old mainstay toilet business.

It was the semiconductor precision ceramics it has been refining for nearly forty years.

01 Securing a Position in the AI Track

Toto's ceramics venture began in 1984. At that time, the company established a New Materials Development Department, attempting to apply the high-temperature sintering techniques accumulated over decades of making toilets to industrial precision ceramics. In 1990, it started joint development of etch chamber components with the US semiconductor equipment leader Lam Research, stepping into the semiconductor supply chain.

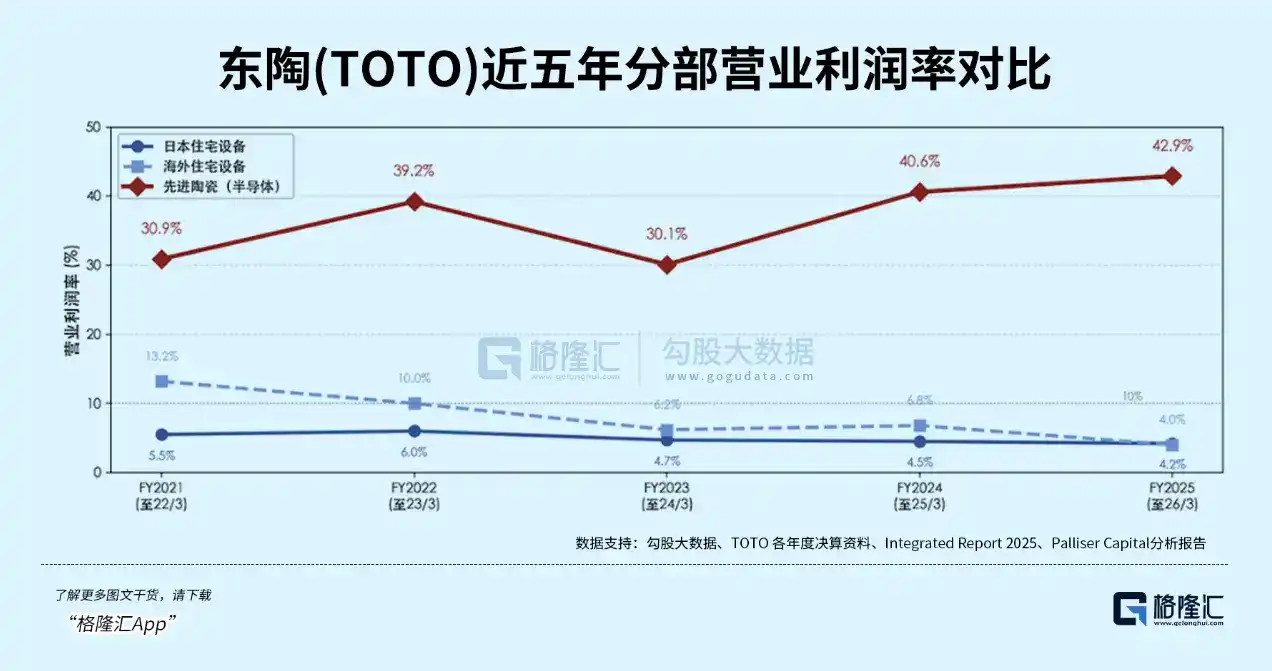

However, for the next thirty years, this business was extremely low-key. High process difficulty, low yield rates, low capacity utilization—semiconductor ceramics consistently dragged down group profits. Even five years ago, the profit margin was only 9%.

The real turning point arrived in 2020. The new factory in Oita Prefecture introduced fully automated production lines and AI quality inspection systems, significantly boosting yields. Then, at the end of 2022, AI demand exploded, NAND manufacturers frenziedly expanded production, and orders for electrostatic chucks flooded in.

The combination of these two variables completely changed the face of the ceramics business.

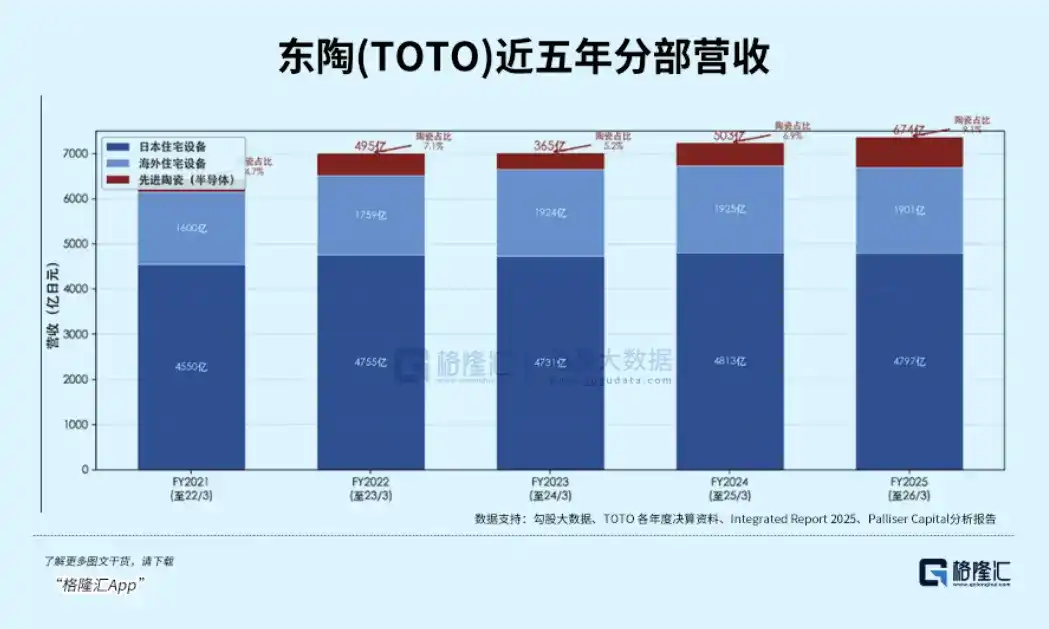

In fiscal year 2025, semiconductor ceramics sales reached 67.4 billion yen, up 34% year-on-year. Operating profit was 28.9 billion yen, up 42%. The profit margin reached 43%. The century-old bathroom fixture mainstay has a profit margin of just 5%. The ceramics business accounted for only 9% of total revenue but contributed 54% of operating profit.

Toto's identity in the capital market used to be stable—a construction materials stock, a bathroom fixture stock. Its P/E ratio hovered between 18 and 20x for a long time. During the peak semiconductor cycle frenzy in 2021, it briefly touched 39.5x, but by the end of 2024, it had fallen back to 18.8x.

The market wasn't ready to price a toilet company as a semiconductor equipment component manufacturer. However, four catalysts in 2026 shattered that perception:

-

January 22: Goldman Sachs upgraded Toto's rating from "Neutral" directly to "Buy," raising the target price from 4,800 yen to 6,100 yen. The stock price rose 11% that day.

-

February 17: Activist investor Palliser Capital issued an open letter, calling Toto "the most undervalued AI beneficiary in the market," estimating an intrinsic value exceeding 8,800 yen.

-

April 30: Annual report disclosure—EPS of 71.16 yen, 79% higher than market expectations. The stock rose 18% that day, marking the largest single-day gain in five years.

-

June 3: Management announced an 80 billion yen investment over the next five years to expand semiconductor ceramic capacity, with the semiconductor share of capex jumping from 11% to over half. The stock rose another 11%.

Following these four catalysts, the company's stock price soared. However, a major divergence from market perception had already emerged.

Is Toto a "bathroom fixture company with a semiconductor sideline" or a "semiconductor equipment component company with a bathroom fixture sideline"? This corresponds to vastly different valuation multiples.

This judgment is difficult because the position Toto occupies in the semiconductor chain is too unique.

The more advanced the chip, the harsher the manufacturing environment. EUV lithography must be performed in a vacuum, with temperature fluctuations per process step not exceeding micrometer levels. Traditional mechanical clamps can't withstand this—only ceramic electrostatic chucks can simultaneously meet four conditions: withstanding temperatures over a thousand degrees Celsius, enduring strong corrosive plasma, having ultra-high insulation, and not outgassing in a vacuum environment.

As 3D NAND stacks from 200 layers towards 500, each additional layer requires another low-temperature etching step, each using an electrostatic chuck. As chips transition from single large dies to small chiplets, thermal density soars, making ceramics the only solution.

Pushing this logic to its conclusion yields a counter-intuitive insight: The more the chip industry pursues "advanced" technology, the deeper its reliance on traditional material processes becomes.

The question then arises: Why can Toto capture this wave of demand?

While competitors can manufacture alumina ceramic parts, maintaining high purity, uniform grain structure, and precise dimensions during mass sintering—the complete set of know-how—is mastered only by Toto. From 1995 to 2026, it holds the most patent applications globally for electrostatic chucks. Counting from its joint development of chamber components with Lam Research in 1990, the two have been tied for over 35 years, with Lam awarding Toto the Supplier Excellence Award for two consecutive years.

In terms of capacity, Toto's Kyushu factory is already at full production, and the new sintering workshop in Fukuoka is expected to start production in 2027. The 80 billion yen investment plan announced in June this year far exceeded market expectations.

But what truly makes competitors despair is not capacity, but time. Certifying a new supplier for electrostatic chucks takes at least five years. Even if competitors invest heavily in building factories now, it would take at least five years from starting certification to shipping qualified products.

The hype around Toto continues, and the path of shifting its valuation anchor from construction materials to semiconductor equipment components is not yet complete.

02 Not Just Toto

Toto is not an isolated case. The same logic is playing out in different industries.

Nittobo (Nittobo), a Japanese textile company that has made glass fiber for 128 years. Its stock price rose 325% last year.

Driving this surge is a material called T-glass, a low thermal expansion glass fiber fabric. As AI chip packaging substrates grow larger in area and stack more layers, the requirements for the substrate material's coefficient of thermal expansion tighten dramatically—ordinary electronic cloth can no longer meet the demands of advanced packaging, making T-glass the only choice.

Approximately 90% of the global T-glass supply is concentrated in Nittobo's hands, with capacity booked until 2027. The supply gap for high-end products exceeds 40%, directly triggering two rounds of price hikes—a 20% across-the-board increase in August 2025, and another 20% to 30% increase in April 2026. The pricing pressure traveled up the supply chain, with Apple bypassing multiple channels to directly secure capacity from Nittobo.

The same identity mismatch is happening to another, more famous Japanese company.

Ajinomoto, the world's largest monosodium glutamate producer, leveraging its amino acid chemistry expertise, developed an insulating film called ABF in the late 1990s for interlayer insulation in chip packaging substrates.

Source: Ajinomoto Official Website

For over two decades, ABF has been the industry's default standard, holding an 80% to 95% global market share. As AI chip advanced packaging substrates stack from 8 layers to 16, each additional layer requires another layer of ABF film. This business accounts for only 6% of Ajinomoto Group's revenue but contributes 30% of its profit, with a profit margin exceeding 50%.

The soaring cases of Nittobo and Ajinomoto point to the same conclusion: In the AI supply chain, high-profit-concentration positions are not always at the technological frontier; they can also be found in seemingly mundane links that are critical bottlenecks and whose capacity cannot be rapidly expanded.

The same logic is playing out in the A-share market, but the narrative differs; the A-share story is about domestic substitution combined with the time window opened by the supply-demand gap.

-

Precision Ceramics Direction

The domestic substitution rate for China's high-end electrostatic chucks is less than 1%, with 12-inch products almost entirely imported. Sinoma Advanced Electronic Materials Co., Ltd. is currently the fastest progressing domestic enterprise—its electrostatic chucks have passed machine verification by a leading domestic equipment manufacturer and entered the mass supply stage; aluminum nitride thin-film substrates have also started delivery to customers.

In Q1 2026, the company's revenue increased 79% year-on-year, and net profit attributable to shareholders grew 57%. Its stock price rose from 45 yuan to 176 yuan over 52 weeks, a gain of nearly 300%. Following closely are Comatec and Pioneer Precision, but they still need time before achieving mass shipments.

-

Electronic Cloth Direction

The price of high-end electronic cloth has risen 250% to 300% cumulatively since early 2024, with even higher increases for some extreme specifications. Honghe Technology is the global leader in ultra-thin cloth (16 microns and below), with a market share of about 26%, and has passed NVIDIA and TSMC certification. In Q1 2026, its quarterly net profit reached 140 million yuan, up 354% year-on-year.

Fellhua is the only domestic company capable of mass-producing quartz cloth, also obtaining NVIDIA certification—quartz cloth sells for 200 to 400 yuan per meter with a gross margin exceeding 60%. According to Huatai Securities, the market size for special low dielectric constant electronic cloth (Low-Dk and quartz cloth) is expected to surge from 3.9 billion yuan in 2025 to 29.2 billion yuan in 2027, with a CAGR of 173.3%. This material has become one of the fastest-growing segments in the AI hardware field.

The core tension in the A-share mirroring lies in: the supply-demand gap provides a time window; the speed of substitution determines the upside. The real test is—can capacity be released as scheduled, and can yields reach levels comparable to Japanese competitors.

03 Closing

The inertia of industry classification is powerful. A company that has made toilets for over a century won't automatically be reclassified as a tech stock just because its semiconductor business contributes over half its profits. The same logic applies to textile factories, MSG producers, and consumer goods companies—their traditional labels don't automatically fall off.

But changes in profit structure don't wait for market perception to catch up. The difference lies only in whether the market adjusts gradually amidst hesitation, or jumps to the correct valuation in one go when the logic becomes clear enough.

The structural trend of cross-industry migration will not reverse. AI's precision requirements for chips will only increase, and reliance on traditional material processes will only deepen. But the pace must be clear-eyed—logic takes time to materialize, and stock prices often run ahead of the logic. (End)