Author: Catrina,Partner at Portal Ventures

Compiled by: Jiahuan, ChainCatcher

Crypto venture capital is at a watershed moment. Over the past three cycles, token exits have been the primary driver of outsized returns, but they are now undergoing a major reset. The definition of token value is being rewritten in real-time, yet an industry-standard valuation framework has yet to emerge.

What Exactly Is Happening?

This time, the crypto market structure is being simultaneously impacted by multiple unprecedented forces, completely upending it:

1. The emergence of HYPE awakened the token market, proving that token prices can have real revenue backing, with over 97% of its eight to nine-figure revenue generated on-chain.

This has thoroughly disillusioned the market regarding governance tokens propped up by narratives but hollow in fundamentals—think of the L1s and "governance tokens" that primarily existed to navigate the ambiguities of securities laws (which made direct revenue distribution unfeasible). HYPE reset market expectations almost overnight: revenue is now scrutinized more strictly and has become the basic ante to play.

2. Chain Reaction and Backlash on Other Token Projects

Before 2025, if you had on-chain revenue, you were considered a security; after HYPE, if you ask most hedge funds, they'll tell you that if you don't have on-chain revenue, you'll go to zero. This has left most projects, especially non-DeFi ones, in a dilemma, scrambling to adapt.

3. PUMP Brought a Stunning Supply Shock to the System.

The explosion of supply from meme coin mania, by diverting attention and liquidity, has fundamentally disrupted the market structure. On Solana alone, the number of newly generated tokens surged from about 2-4 thousand per year to a peak of 40-50 thousand. This effectively split the not-much-grown liquidity cake into about one-twentieth. Chasing alpha, the same buyer demographic has shifted its attention and capital to speculating on meme coins rather than holding altcoins.

4. Accelerated Diversion of Retail Speculative Capital.

Prediction markets, stock perpetuals (perps), and leveraged ETF trading are now directly competing for the same pool of capital that would have flowed into altcoins. Meanwhile, the maturation of tokenization technology has made leveraged trading of blue-chip stocks possible—these stocks don't carry the risk of going to zero like most altcoins, are subject to much stricter regulation, and are more transparent with lower information asymmetry risks.

The result is a severe compression of the token lifecycle: the time from peak to trough has shortened dramatically, retail willingness to "hold" tokens has plummeted, replaced by faster capital rotation.

Some Big Questions Every VC Is Asking Themselves and Their Peers

1. Are we underwriting equity, tokens, or a combination of both?

The biggest challenge here is that we have no new playbook for value accrual in token projects—even the most successful projects like Aave still face controversy between the DAO and equity.

2. What is the best practice for on-chain value accrual?

The most common is token buybacks, but that doesn't mean it's right. We have long been against the prevailing trend of token buybacks: it is toxic and puts founders with real revenue in a bind.

The incentive is completely wrong: stock buybacks happen after a company has finished investing in growth, whereas crypto buybacks are increasingly demanded immediately, driven by retail/public perception (a completely fickle and irrational thing).

You might burn $10 million that could have been reinvested for nothing, and the very next day that value could vanish due to some random market maker getting liquidated.

Public companies buy back stock when it's undervalued. Token buybacks get front-run at every turn, so they are often executed at local highs.

Especially if you are a B2B business generating off-chain revenue, this is a futile exercise. In my opinion, when your revenue is less than $20 million, there is absolutely no reason to do buybacks just to please retail instead of reinvesting the capital into growth.

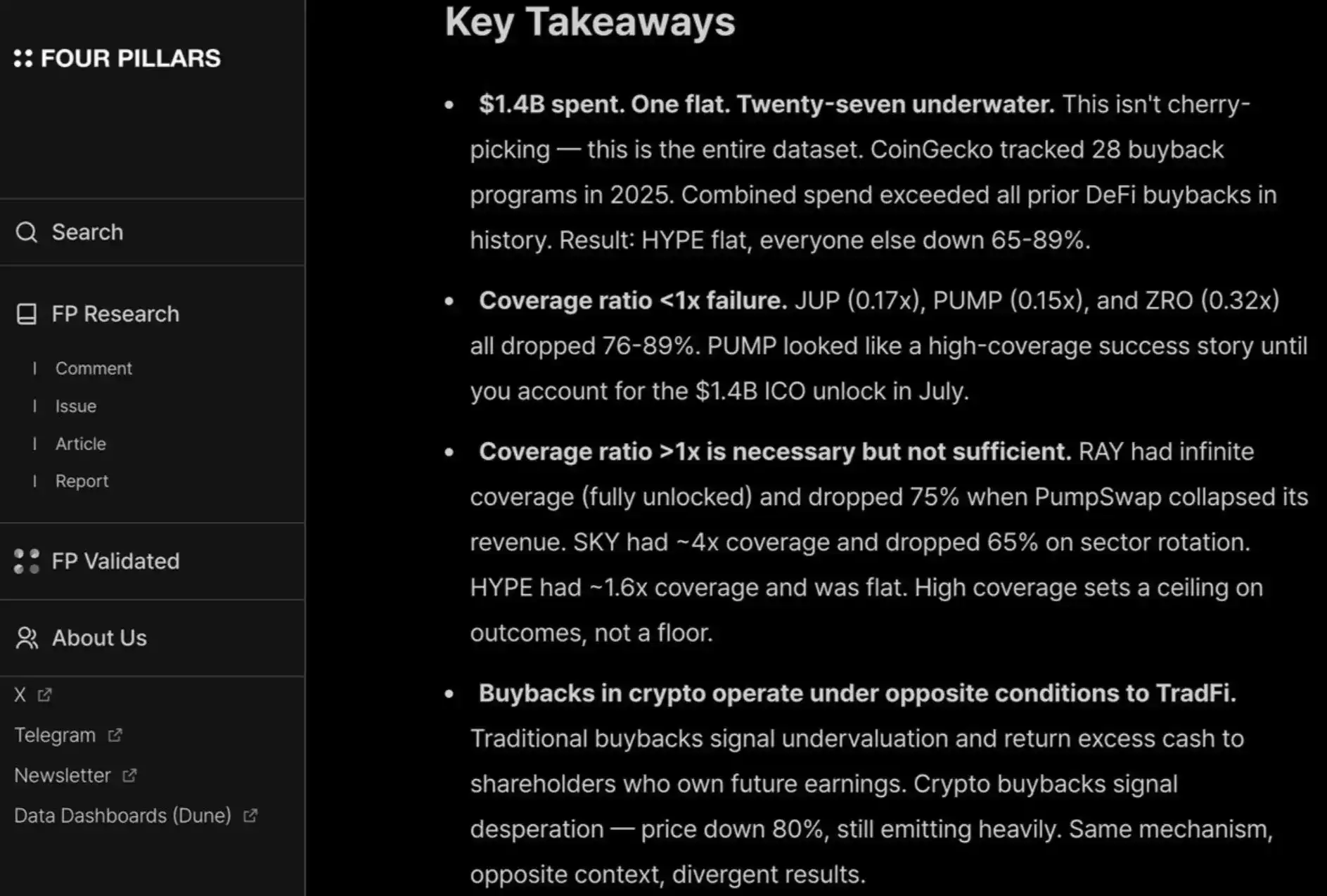

I really like this report from fourpillars, which shows that buybacks in the high nine-figures did almost nothing to help projects set a long-term price floor.

Beyond that, to keep retail and hedge funds happy, you must also conduct buybacks consistently and transparently, like HYPE does. Any failure to do so is punished, as seen with PUMP's P/E ratio (based on fully diluted valuation) being only 6x because the public "doesn't trust" them—despite the fact that they have verifiably burned $1.4 billion in revenue that could have gone to the treasury.

Here is some further reading on "on-chain value accrual mechanisms that work without burning money"

3. Will the "crypto premium" disappear entirely?

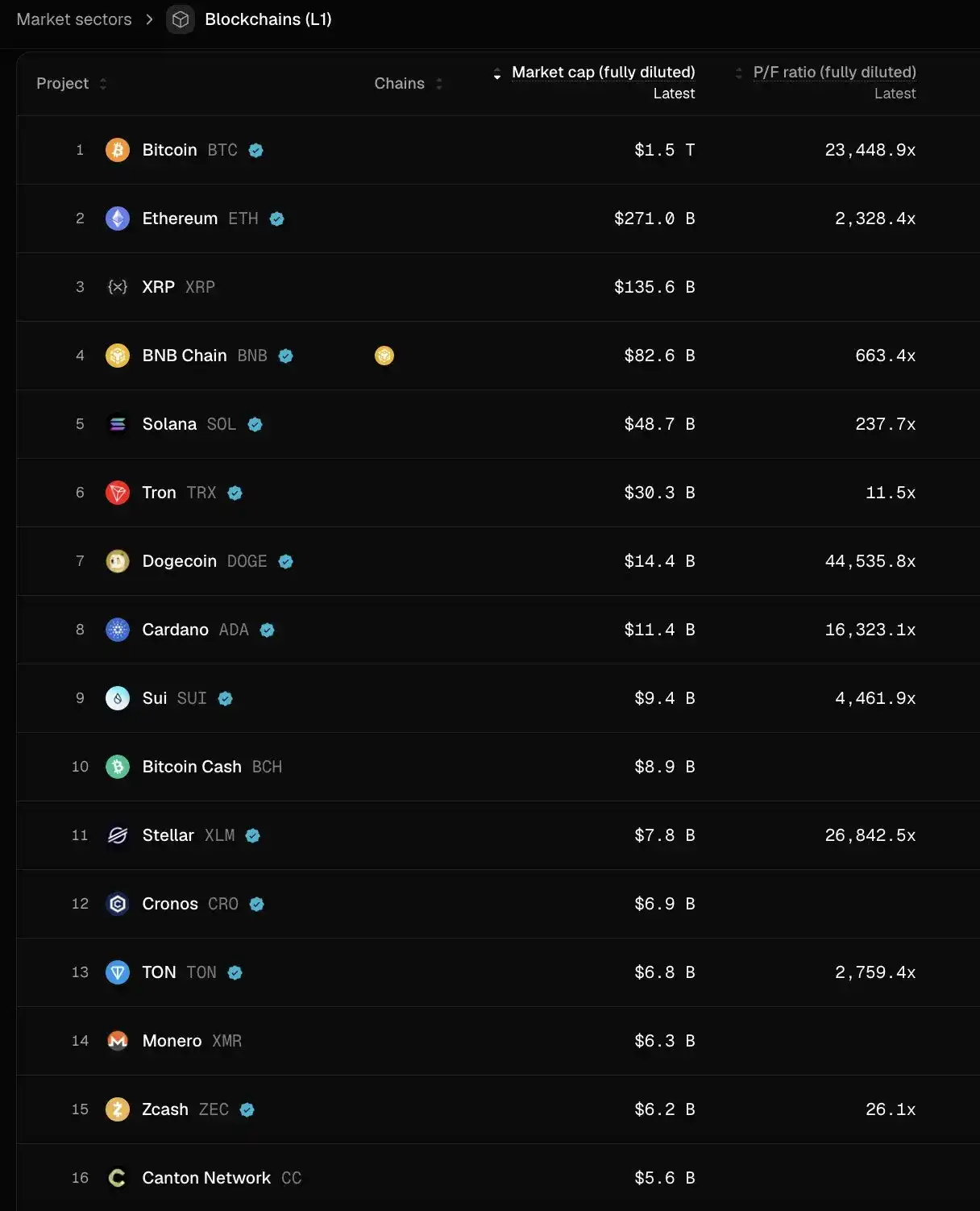

This would mean that in the future, all projects will be valued based on multiples similar to public stocks (roughly 2 to 30x revenue). Take a moment to think about what this implies—if true, we would see most L1 public chains fall more than 95% from current prices, with exceptions like TRON, HYPE, and other revenue-generating DeFi projects. And this is even without considering token vesting.

Personally, I don't think it will be like this—HYPE set an extremely exceptional expectation, making many investors impatient for "day one revenue/user traction" from early-stage startups. For sustaining innovations like payments and DeFi companies, yes, this is a reasonable expectation.

But disruptive innovation takes time to build, launch, grow, and then see revenue grow exponentially.

In the past two cycles, we had excessive patience and blind optimism for so-called "disruptive technologies"—new L1s, esoteric concepts like Flashbots/MEV raising up to Series 8-9, and now the pendulum has swung too far the other way, only willing to back DeFi projects.

The pendulum will swing back. While evaluating DeFi projects based on "quantitative" fundamentals is indeed a net positive for the industry maturity, for non-DeFi categories, "qualitative" fundamentals also need to be considered: culture, technological innovation, disruptive concepts, security, decentralization, brand equity, and industry connectivity. And these traits are not simply reflected in TVL and on-chain buybacks.

What to Do Now?

Return expectations for token projects have been significantly compressed, while equity businesses have not seen a comparable decline. This divergence is particularly evident in early-stage versus growth-stage projects.

Early-stage investors have become much more price-sensitive when underwriting projects that might exit via tokens. At the same time, appetite for equity businesses has increased, especially given the favorable M&A environment. This is completely different from the situation in 2022-2024, when token exits were the preferred liquidity path, underpinned by the assumption that the token valuation premium would persist.

Later-stage investors, those with the strongest brand equity and value-add in the crypto-native context, are increasingly moving away from purely "crypto-native" deals. Instead, they are pivoting to support more "Web2.5" companies, whose underwriting is anchored by revenue traction.

This pushes them into unfamiliar territory, competing head-on with firms like Ribbit, Founders Fund—institutions that have deeper backgrounds in traditional fintech, stronger portfolio synergies, and better visibility into early-stage deal flow outside of crypto.

The crypto VC space is entering a period of value validation. The right to survive depends on VCs finding their own PMF (Product-Market Fit) with founders, where the "product" is a combination of capital, brand alignment, and value-add.

For the highest-quality deals, VCs need to sell themselves to founders to win the right to be on the cap table, especially as some of the most successful projects in recent years have needed almost no institutional capital (e.g., Axiom) or none at all (e.g., HYPE). If capital is the only thing a VC provides, it will almost certainly be eliminated.

Those VCs qualified to remain in the game need to be very clear about what they can offer in terms of brand alignment (which is what prompts the best founders to engage in the first place) and value-add (which ultimately determines their right to win the deal).