By: KarenZ, Foresight News

As the U Card trend extends to AI subscriptions, Plasma has found a new avenue for asset staking.

On June 12th, Plasma launched three tiers of U Cards, which will become available to all users this week.

On the surface, this is a stablecoin debit card membership system. What users see are base cashback, AI benefits, airport rebates, and Visa spending scenarios. What the project is focused on is longer-term spending frequency, token holdings, and staking.

How are the three tiers differentiated: Lite for onboarding, Core targets AI users, Platinum locks in large holders

Before dissecting the benefits, it's necessary to clarify the product scope of Plasma One. According to the official website, the Plasma One global account service is provided by Bridge, while the Plasma One card is issued by Rain, a principal member of Visa, under Visa's authorization, and is usable in countries and with merchants that accept Visa. In other words, Bridge focuses more on the account service layer, Rain on card issuance and the Visa payment channel layer, and the end-user experience is a stablecoin spending card connected to the Visa network.

Lite is the lowest barrier to entry. The website states the Lite card cost is $0, with a base cashback of 2% and 1 free virtual card. It's suitable for users who just want to try a stablecoin card and are not ready to buy or stake XPL yet.

Core targets regular AI users. It offers 3% base cashback, 5% AI spending cashback, a ChatGPT Go subscription, and up to 2 free virtual cards. Core is accessible through an annual fee of $120 or by staking 10,000 XPL for 12 months. It's important to note: The Core page specifies the 5% AI cashback applies to up to $500 in AI spending per month. This $500 is the spending cap for the cashback calculation, not the cashback amount cap.

Platinum is more akin to a premium spending card. The official page states it's designed for major XPL holders, accessible by staking 100,000 XPL for 12 months, with no additional fee. Benefits include 4% base cashback, 10% AI spending cashback, Claude Pro and ChatGPT Plus subscriptions, up to $600/year in flight ticket rebates, lounge access, Visa concierge service, car rental insurance, travel insurance, baggage delay & loss coverage, and global eSIM, among others.

The Platinum product page also promotes annual cashback and benefit values exceeding $10,000, including $7,500 in base cashback, $1,400 in AI credit, $600 in airline credit, etc. However, these are closer to marketing assumptions and do not equate to guaranteed, unconditional maximums for users.

Is it worth it: Lite is for trying, Core depends on AI spending, Platinum depends on tolerance for asset volatility

First, Lite. Its advantage is simplicity: $0 card fee, 2% base cashback, no staking. Its disadvantage is also clear: no additional category bonuses, no AI subscriptions, and no travel benefits. For most regular users, Lite is the most suitable tier for testing the waters, as it doesn't immediately expose you to XPL price volatility.

The key question for Core is: Can the $120 annual fee or the staking of 10,000 XPL be covered by actual spending? Calculating based on XPL at $0.088 (as of writing on June 15th), 10,000 XPL is roughly $880.

If not staking XPL, one needs $120 to register for the Core card. Comparing only ordinary spending between Lite and Core, Core offers 3% base cashback vs. Lite's 2%, a difference of 1 percentage point. To cover the $120 annual fee with this 1% difference, requires approximately $12,000 in annual eligible spending.

If focusing primarily on AI spending, Core's benefits should be calculated separately: The website states Core offers 5% AI cashback, applicable to up to $500 in AI spending per month; Lite explicitly has no AI cashback. Therefore, based on this specific AI cashback, covering the $120 annual fee requires $2,400 in annual eligible AI spending, roughly $200 per month. If maxing out the monthly $500 AI spending cap, Core can yield about $25 monthly in AI cashback, or $300 annually. Combined with the ChatGPT Go subscription benefit, Core is more suitable for users who already have ongoing AI tool expenses.

However, if a user chooses to stake 10,000 XPL instead of paying the annual fee, the calculation changes. The real cost of the staking-based Core version comes from XPL price volatility and the 12-month liquidity lockup; it shouldn't be simply viewed as getting the card for free.

Platinum's threshold is higher. 100,000 XPL is approximately $8,800 and requires a 12-month lockup. It suits three types of people: users already heavily invested in XPL, those with high AI and travel spending, and large holders who can accept a one-year lockup and price volatility.

Platinum's AI benefits are also weightier: Beyond 10% AI spending cashback, it includes Claude Pro and ChatGPT Plus subscriptions. For users already long-term subscribers of Claude Pro and ChatGPT Plus, these subscriptions can be considered as actual cost offsets. But for those staking temporarily just to get the card, they are more like add-on benefits that don't offset the price volatility risk associated with locking up 100,000 XPL for a year.

To achieve the advertised $7,500 value from the 4% base cashback alone requires about $187,500 in eligible spending; the maximum $600 flight ticket rebate, calculated at 10%, also corresponds to roughly $6,000 in eligible flight ticket spending. For an ordinary user buying 100,000 XPL temporarily just for the benefits, the risk-reward ratio isn't attractive.

Another layer of risk comes from the terms. Plasma One cashback is first denominated in USD, then converted to XPL at the XPL/USD price at the time of distribution. Rewards may undergo a pending period, and transactions involving refunds, chargebacks, abnormal spending, or arbitrage-like card usage may trigger forfeiture or clawbacks. The terms also state that Plasma may adjust reward rates, monthly caps, eligibility, excluded transactions, distribution cycles, and referral reward structures. Before valuing benefits at their full-cash hypotheticals, it's wise to discount these variables.

What is the impact on XPL?

The most direct impact of Plasma U Cards on XPL is adding a membership qualification attribute to the token. Previously, XPL's narrative primarily stemmed from the Plasma chain itself and zero-fee USDT transfers. Now, Core and Platinum tie XPL to spending benefits, motivating users to hold XPL for AI subscriptions, cashback, travel perks, and card tier status.

Plasma documentation shows an initial XPL supply of 10 billion, with 10% public sale, 40% ecosystem & growth, 25% team, and 25% investors. Within the ecosystem & growth portion, 800 million tokens unlock at the Mainnet Beta on September 25, 2025, with the remaining 3.2 billion released linearly over 3 years.

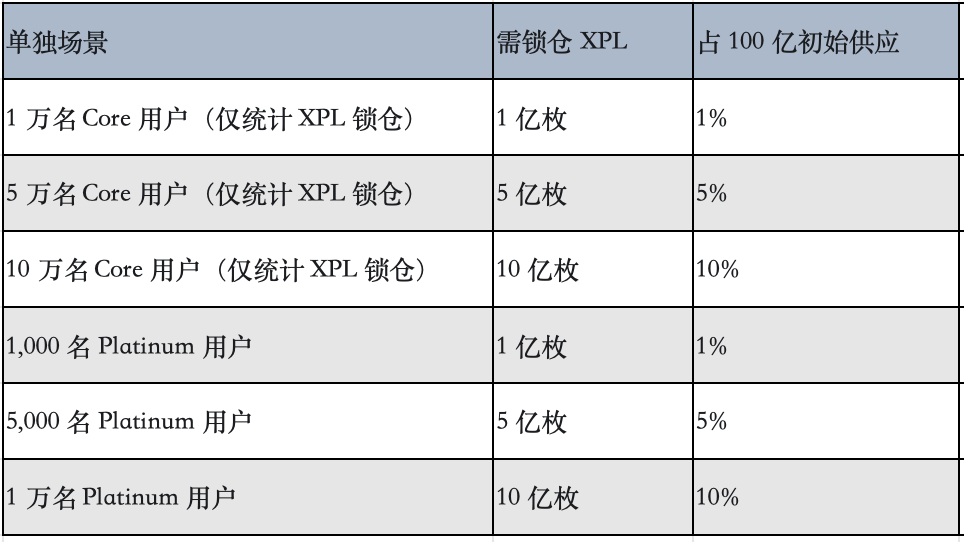

Let's examine staking effects with a few scenarios:

The implication of this table is straightforward: Core needs scale, Platinum needs large holders. With just 1,000 Platinum users, 100 million XPL can be locked; with 10,000 Platinum users, 1 billion XPL can be locked, accounting for 10% of the total initial supply.

More crucially, compare this to the unlock schedule. From the ecosystem & growth allocation, the remaining 3.2 billion tokens will be released over 3 years (fully unlocked by September 25, 2028), averaging about 88.89 million per month. To absorb one month's ecosystem release, approximately 8,889 Core users staking XPL, or 889 Platinum users, would be needed.

The team and investor allocations total 5 billion tokens, with a one-year cliff unlocking one-third (~1.667 billion) on September 25, 2026. To fully offset this amount with card staking would require about 166,667 Core users staking XPL, or 16,667 Platinum users. This number is already substantial, indicating that Plasma One card tiers can improve the circulating structure but are unlikely to single-handedly absorb future large-scale unlocks.

Another variable is inflation. Plasma plans to initiate validator rewards after external validators and delegated staking go live, starting with 5% annual inflation, decreasing by 0.5 percentage points each year until reaching a long-term baseline of 3%; simultaneously, a base fee burn mechanism similar to EIP-1559 aims to counteract new issuance.

Roughly calculating based on the 10 billion initial supply, 5% annual inflation corresponds to 500 million XPL. Covering this annually would require staking from 50,000 Core users or 5,000 Platinum users.

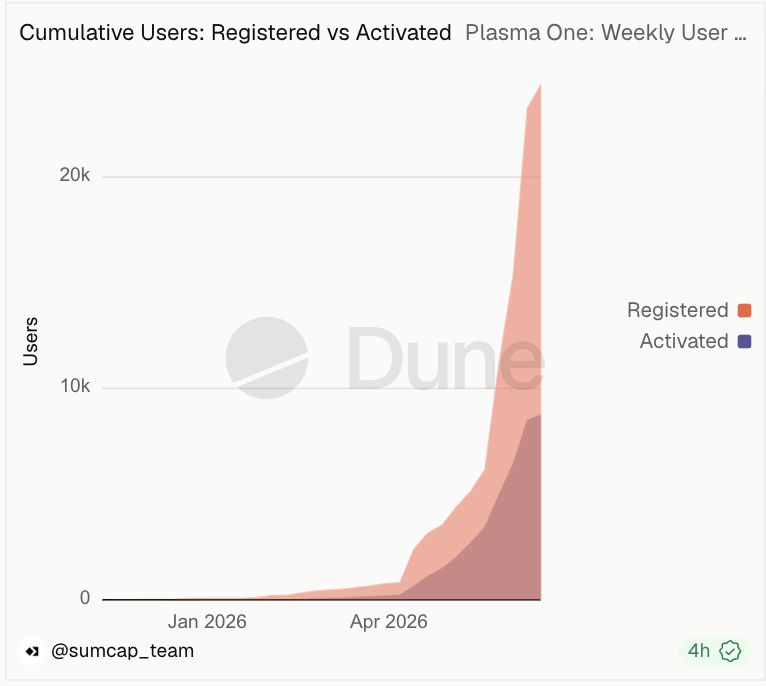

Data from a Dune dashboard built by Sumcap shows Plasma One currently has 24,000 cardholders, with 8,884 cards activated.

The positive effect of Plasma's latest move on the token lies in: Adding non-speculative reasons to hold XPL, reducing part of the circulating supply, and expanding XPL's reach.

The negative effects are also clear: Cashback is distributed in XPL, and if users treat it as cash-equivalent, they might sell immediately upon receipt. Of course, this is digested gradually.

Another point is that the official sources have not yet disclosed the specific origin of the reward XPL, which determines whether it ultimately constitutes a net buy pressure, a net distribution, or a mix of both.

Plasma's Real Experiment

The counter-intuitive aspect of Plasma is here: The smoother the zero-fee USDT transfers, the less ordinary users need to actively hold XPL to pay for Gas. The membership staking adds another demand curve for XPL. It brings users from exchanges, airdrops, and staking pages into more everyday scenarios: swiping a Visa card, receiving cashback, subscribing to AI tools, etc.

This is good for the project itself. Stablecoin Layer 1s are easily evaluated by the market based on TVL and subsidies. Plasma One provides it with a consumer finance entry point and also links XPL to real-world payment frequency. However, this path is also more challenging. Users won't swipe their cards daily because of a Layer 1 narrative; they will stay for fees, currency exchange, risk controls, customer service, regional coverage, and benefit fulfillment.

For XPL, Plasma One Tiers is a useful experiment for staking and distribution, but it cannot replace real transaction volume, stablecoin liquidity, and subsequent unlock management.

It's more like a door, handing on-chain assets to everyday spending. The door is open; the next step is to see how many people actually walk through it every day.