Written by: Zuo Ye

Original Title: The Limits of Finance, The Channel Value of Global Markets

On-Chain Asset Management Vaults and Channels

No matter how many lies are woven, the truth will still illuminate the outline of light.

Asset management giants' interest in on-chain Vaults is growing daily, and the mainstreaming of the DeFi dream seems to be becoming a reality.

This is the best of times: BlackRock buys $UNI tokens, Apollo commits to buying hundreds of millions of dollars worth of $Morpho tokens, and Wall Street is collectively bullish on the future of DeFi.

This is the worst of times: BlackRock, Blackstone, and Blue Owl face concentrated redemption waves, and the founder of Aave warns that Wall Street is using RWA as a liquidity exit channel.

Crises always contain rare bargain prices. Faced with future asset price inflation, emerging forces are excited, completely disregarding the iceberg ahead.

No matter what it's called—DeFi/RWA/Vault—on-chain finance must eat the sugar coating and fire the cannonball back. Only by being good at breaking an old world can a new Eden possibly be built.

This sweet apple can even be made concrete—the risk-free rate.

The Dream of a Risk-Free Rate

Establish a risk-free rate market based on on-chain asset-backed stablecoins to have bargaining power against traditional asset management giants.

Let's start with a question to anchor our discussion: Why has DeFi not yet achieved a risk-free rate?

Or, reframe it as the linear narrative of how "U.S. Treasuries" became the benchmark rate for DeFi.

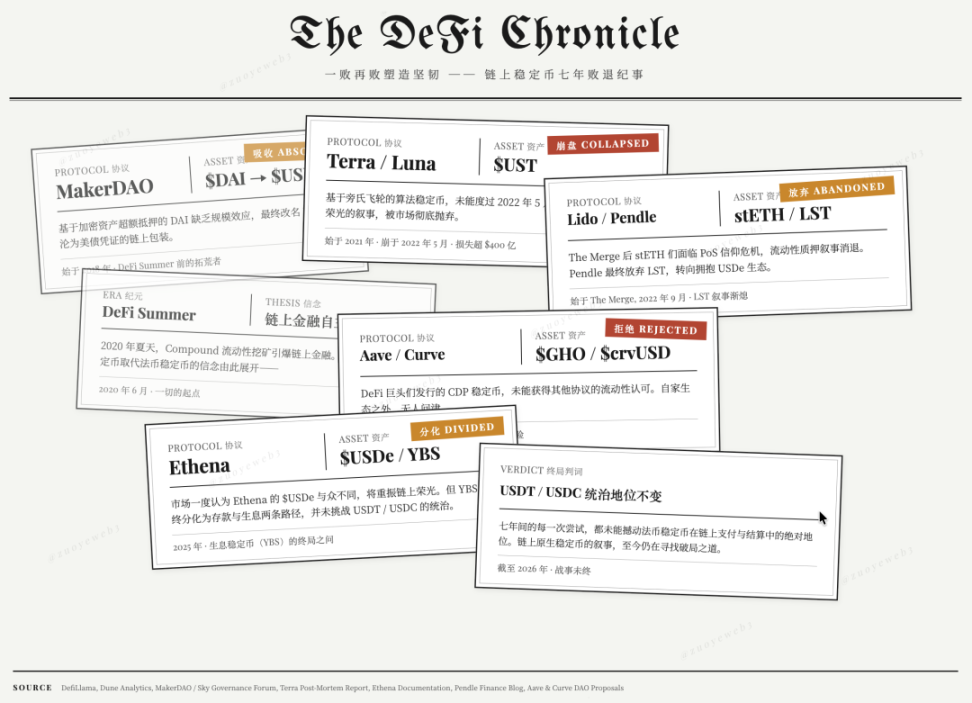

Image Caption: Stablecoin Chronicle

Image Source: @zuoyeweb3

Starting from the DeFi Summer of 2020, repeated defeats have forged resilience:

-

Starting in 2018, DAI based on crypto assets lacked scale, $USDS ultimately became a U.S. Treasury certificate

-

Starting in 2021, the ponzi-based $UST did not survive the 2022 bank run crisis; the story of rebuilding algorithmic stablecoin glory was abandoned

-

In 2022, stETH and others faced a PoS faith crisis post-The Merge; Pendle ultimately abandoned LST for USDe

-

In 2023/24, CDP stablecoins issued by DeFi giants like Aave/Curve were not recognized by other protocols

-

In 2025, the market once believed Ethena's $USDe was different, reviving on-chain glory, but yield-bearing stablecoins ultimately split into deposit and yield-bearing activities, failing to challenge the dominance of USDT/USDC in their respective domains.

The facts are very clear: it's not that USDT swallowed user profits, but that DeFi chose the scale effect of USDT/USDC.

Exchanging the Treasury profits generated by $300 billion for the entire market's trading foundation is not a bad deal for DeFi and the crypto market.

But at what cost?

The cost is not the evil claimed by yield-bearing stablecoin challengers that Tether takes profits, or the selfishness accused by Coinbase and Trump Jr. that banks prohibit interest-bearing accounts.

The bitter pill DeFi swallowed is that the U.S. Treasury rate, as the risk-free rate, is transmitted on-chain via stablecoins, but the U.S. Treasury is an asset of the U.S. government and its actions do not care about on-chain sentiments.

This is also the fundamental reason for the bankruptcy of tokenomics: UNI relies on A16Z, A16Z relies on USD financing, the USD is the embodiment of U.S. Treasuries, so UNI is just the fourth derivative relying on U.S. Treasuries. Why not just buy Treasuries directly, with no middleman taking a cut?

U.S. Treasuries are the de facto DeFi benchmark, but DeFi can only passively endure it, unable to interact with it bidirectionally. This is the root of all happiness or pain.

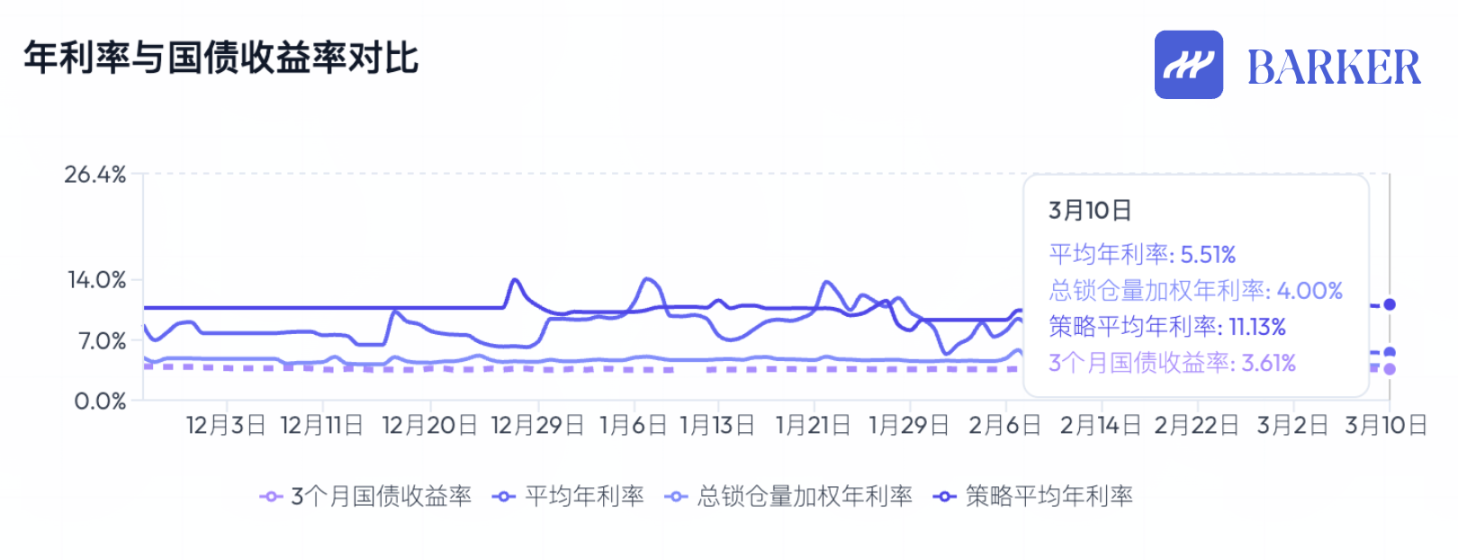

Image Caption: Comparison of On-Chain Stablecoin Yield APY and U.S. Treasuries

Image Source: @BarkerMoneyX

The salvation of DeFi never stops. Although tokenomics are bankrupt and DAO governance structures have collapsed, the overall direction of DeFi remains clear:

-

Fixed-rate investment and financing,公认 risk grading system, unsecured credit lending –> The main themes of the next stage,蕴含某种形式的 mass-market products;

-

The expansion period for public chains, exchanges, and DeFi protocols is over; new application forms are evolving into Vaults. It's not yet certain that Vaults are the form of mass-market products, but this is the starting point of the new stage.

Note here that public chains and exchanges are no longer the central links for value capture, but this does not mean their time is zero. Their period of asset price inflation is over, and only linear, steady growth remains.

This can also connect to the progressive relationship between UNI and U.S. Treasuries. Aave/Morpho are closer to asset management itself; their businesses don't have much narrative space, but are indispensable for the industry.

The real star products will definitely be Vaults used by the masses, based on public chains and DeFi protocols, utilizing分散 RWA assets, and triggering asset price inflation mechanisms.

For mass usage, Curators choose to ally with exchanges: Morpho enters Coinbase via Stakehouse, Aave expands to C-end users via Metamask and other U-cards.

Based on RWA assets, Curators partner with custodians like Galaxy to constantly maneuver between crypto and real-world assets, such as Grove buying Galaxy's CLO bonds.

But what's missing is the Vault that triggers the price inflation mechanism. Even before this wave of large-scale asset management moving on-chain, BlackRock's BUILD token was already live, and Circle's USYC also supports yield, but neither could replicate their own success.

It's not important that Vaults lack their own tokens. Asset price inflation is a mechanism. U.S. stocks, real estate, bonds, tulips, graphics cards, and Mac Minis all have their own price cycles. Current Vaults only have yield-bearing black boxes but始终 fail to solve two problems:

-

Where does the high yield actually come from?

-

How is high risk actually handled?

Towards a New Financial System

The form of channels is evolving; Vaults are not the endpoint.

The crypto industry evolves extremely fast. Before this year, we never dared to imagine that the global financial system would truly move on-chain, but today this is an undeniable ongoing process.

It's not yet time for a victory banquet. RWA can only serve as a funding source, Vaults are still boring deposit products, various Curators haven't demonstrated brand effects, and white-label Vaults like Veda are highly similar to SaaS, with the operator Curator only earning management fees.

This has no imagination for price inflation. If traditional asset management, with a scale of $2 trillion, endures cyclical煎熬, it's hard to imagine Vaults can withstand it.

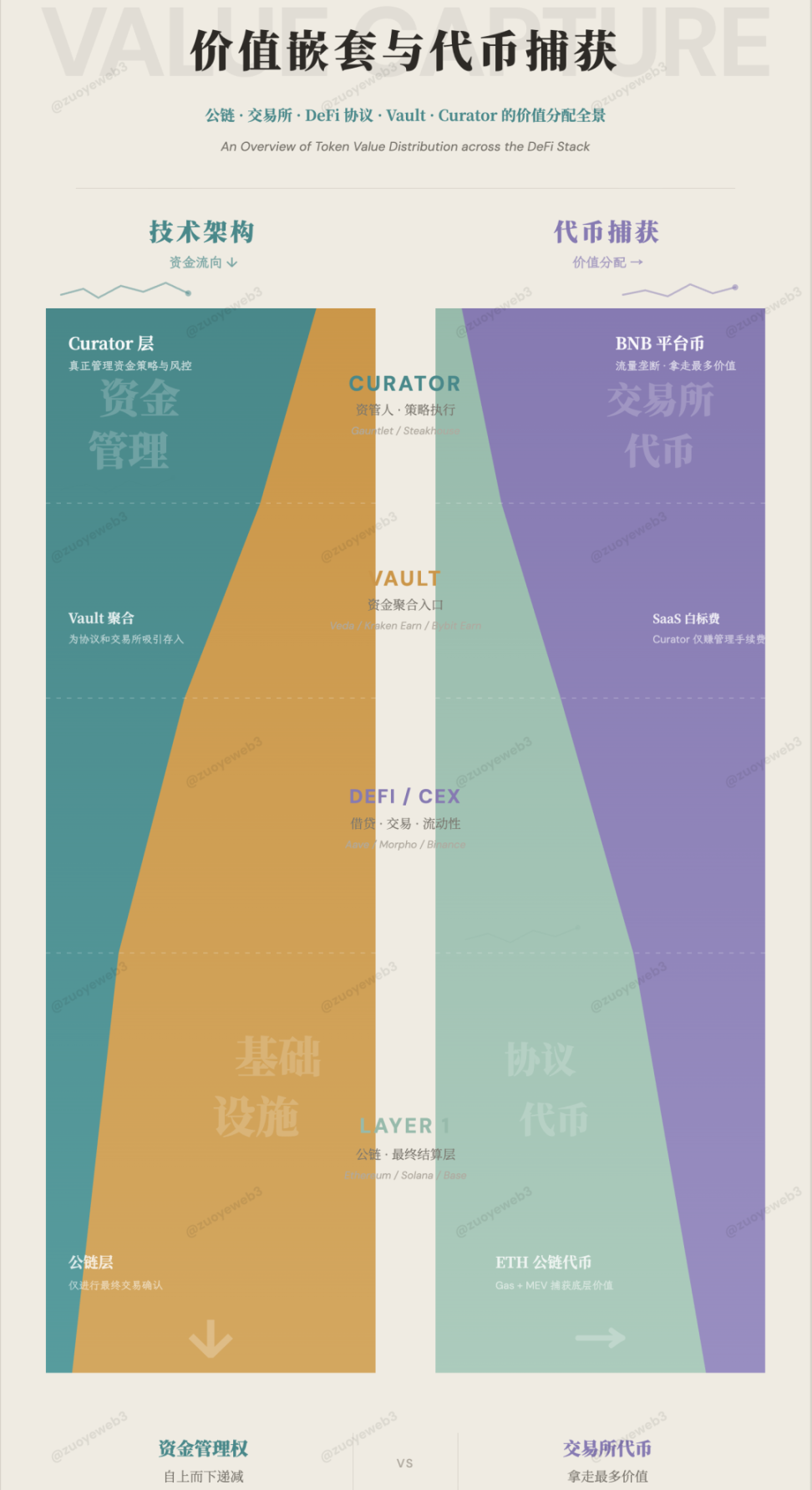

Image Caption: Fund Flows and Value Distribution

Image Source: @zuoyeweb3

Asset management moving on-chain is not driven by短暂 sentiment. In a sense, it's like the banking industry's IOE—you can't go back to the paper era. Even Spark has begun unifying the calculation of CEX/DEX position adjustment margins. DeFi is becoming the next step for TradFi.

Whether Vaults, after absorbing sufficient funds, will trigger the establishment of a risk-free rate is the biggest博弈 point of this cycle.

During the previous DeFi Summer, TVL was the decisive metric. The amount of资金 mapped to the get-rich coefficient of tokens, creating mining that continued into airdrop farming, studios, and Binance Alpha. The core logic was "projects need more funds to support token growth."

But with Vaults, for the first time, there is a huge demand for deposits but an inability to support their own tokens. Even if Morpho captures more market share from Aave, it cannot trigger a token surge.

Extending this, Hyperliquid compared to Binance, Lighter compared to Hyperliquid—their market sizes and token prices show a huge inversion. This is a great change unprecedented in DeFi.

On one hand, old infrastructure continues to吸血. For example, after the listing effect disappeared, $BNB should have declined, but CEXs still have a larger user base than the entire on-chain + DeFi. A very ironic fact: exchanges have retail users; DeFi protocols like Aave and Morpho have completely become the domain of a few professionals.

In this context, the high risk of Vault&Curator comes from code and structure:

-

Curve's immutable contract programming language can have problems; the xUSD team self-issued tokens

-

Aave ended the表面 harmony between the DAO and the development team; Re7 severely damaged on-chain asset management credibility

In this context, where does the high yield of Vault&Curator come from?

I know it's not regulatory arbitrage, HLP fees, or token incentives, but many still cling to these three, believing traditional finance's compliance creates too-big-to-fail credibility.

They completely forget that tokenomics are already bankrupt, while Vault deposits keep growing. Sky is already deeply integrated into the Morpho system, and the future of Aave V4 is also institutionalization and modularization.

Moreover, this article has always emphasized that the scale of Vault funds has not triggered some price inflation mechanism. This is the structural dilemma of Vaults.

The yield of Vaults essentially comes from the trading efficiency of global markets. If CEXs don't provide a certain Vault, then configure it on-chain. The personified Curator happens to be suitable for dealing with all sorts of people.

Even in TradFi's global markets, like U.S. stocks, one faces lengthy account opening, trading times, and process limitations. Can we really say that the gradual move towards全天候 trading for U.S. stocks and DTCC going on-chain is also for arbitrage?

The final question: What mechanism can actually trigger asset price inflation, allowing the funds沉淀 in Vaults to create a legendary price-to-dream ratio?

In other words, what is missing between Vaults and asset price inflation?

Channels are missing. Channels for funds to couple with each other. The personification of Curators hinders the programmability of DeFi Legos.

Currently, CEXs serve as a placeholder, still the fastest place for funds to intertwine.

Referencing the evolution of Perp DEXs, they are capturing market share from CEX futures. RWA funding sources are also抢夺 CEX market share.

CEXs only have存量. They themselves cannot solve user acquisition problems, let alone help Vaults expand to hundreds of millions of users. Vaults start by white-labeling, but in the future, they must build their own超级 factories.

I speculate the channel will be some form of Broker product.

Under高度 social division of labor, Super Apps like exchanges that integrate deposit/withdrawal, trading, custody, and清算 will gradually separate into different businesses. Binance's compliance framework in Abu Dhabi's ADGM is already divided into three parts.

This will fundamentally facilitate the professionalism of fund handling, utilize the unified ledger system of blockchain, and require the居中 coordination of Vault&Curator.

Referencing Neobrokers like Robinhood/Trade Republic, they attract年轻化, retail users to participate in professional trading, then build asset management, wealth management, and other business forms. The model of stablecoins at the front end and Curators managing Vaults is more efficient.

In summary, Binance monopolizes fund flow, BNB gets the strongest empowerment. Next, Brokers handle fund interaction. Some asset form, or even纯粹 business flow, could be highly profitable. After all, Robinhood is just a little disguise for a profitable market maker.

Conclusion

Compared to code and trading, regulation and tokens appear more stable.

Private credit and the RWA cycle have halted.抢先 issuing the 402 document feels prophetic. DeFi can serve as a liquidity exit channel, but it lacks the asset price inflation mechanism.

Asset Management ≈ Aave/Morpho will slowly, like public chains, end their historical mission. They will exist long-term but only with scale growth and stable token prices;

Vault&Curator ≈ Star fund managers are quickly acquiring customers and monopolizing markets. Giantization already shows preliminary signs. Whether they can continuously capture value is highly doubtful;

Channel ≈ CEX (temporary)反而 has the most innovation space. Facilitating the freedom of funds will always receive the highest reward.

A highly efficient global market is operating on a next-generation blockchain that doesn't need traditional tokens. This is the proposition of the next era, and everyone must provide an answer.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush