Executive Summary

- Bitcoin has broken below the STH cost basis and the −1 STD band, placing recent buyers under stress; the $95K–$97K region now acts as key resistance, and a reclaim would mark an early step toward restoring market structure.

- Spot demand remains weak, with US spot ETF flows deeply negative and no incremental bid emerging from TradFi allocators.

- Speculative leverage continues to unwind, reflected in declining futures open interest and funding rates falling to cycle lows across the top 500 assets.

- Options markets have sharply repriced risk, with implied volatility rising across maturities and skew remaining deeply negative as traders pay significant premiums for downside protection.

- Put-dominant flow and demand at key strikes (e.g., 90K) reinforce a defensive positioning regime, with traders hedging more actively rather than adding upside exposure.

- DVOL has returned to monthly highs, tying together the broad repricing of risk across volatility, skew, and flow metrics and signalling expectations for elevated near-term volatility.

Bitcoin has broken below its earlier consolidation range, slipping under $97K and briefly touching $89K, marking a new local low and pulling its year-to-date performance into negative territory. This deeper contraction extends the mild bear trend we highlighted last week and raises questions about where structural support may re-emerge. In this edition, we use on-chain pricing models and short-term holder loss realization to assess how the market has reacted to this breakdown. We then turn to options, ETF flows, and futures positioning to evaluate how speculators are adjusting their sentiment amid this renewed weakness.

On-chain Insights

Breaking the Lower Band

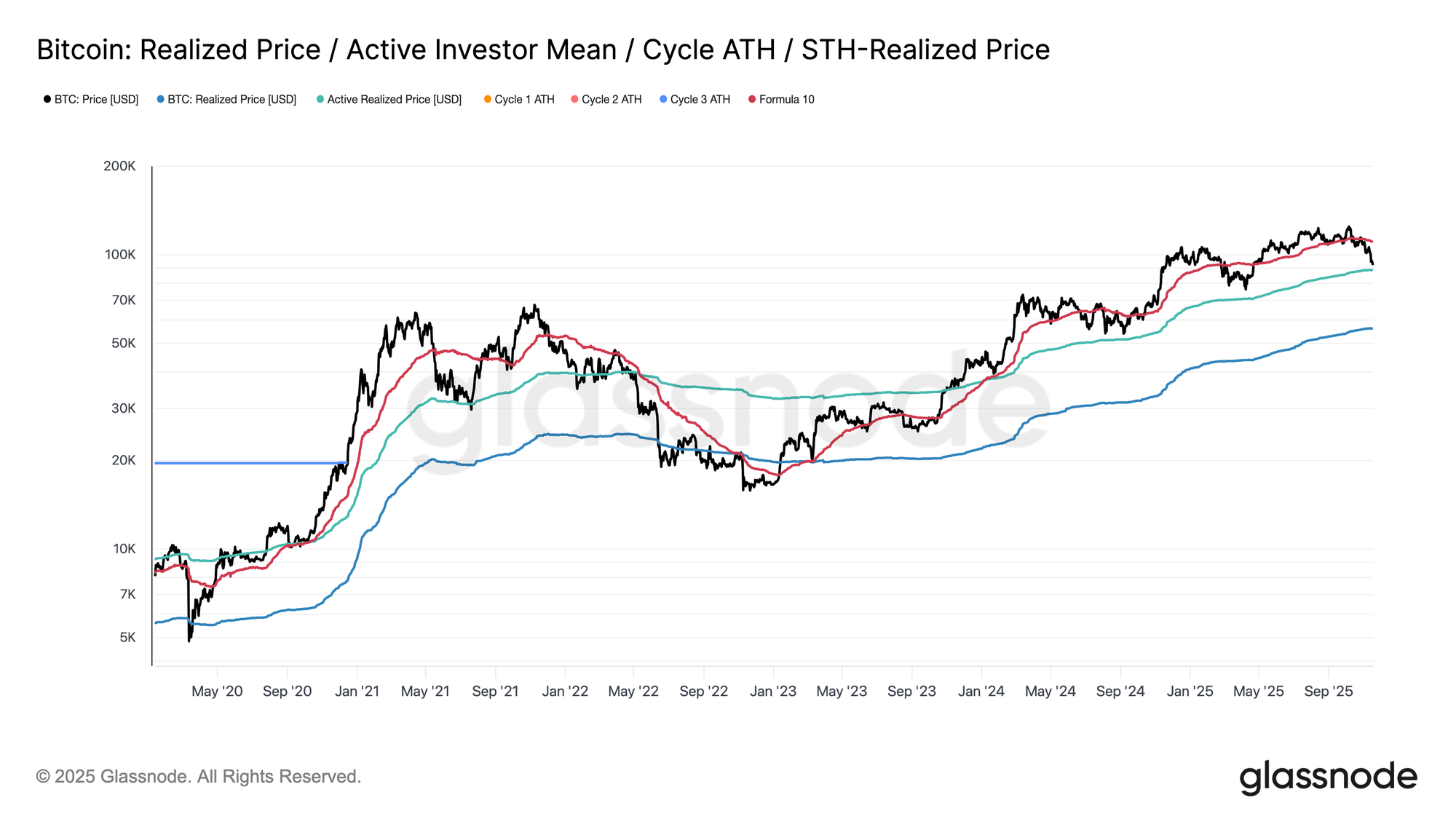

Breaking below $97K, the lower boundary of last week’s “limbo range,” signaled the risk of a deeper correction. Price then plunged to $89K, forming a new local low beyond the –1 STD level (~$95.4K) relative to the short-term holder cost basis, now near $109.5K.

This breakdown confirms that losses now dominate nearly all recent investor cohorts, a structure that has historically triggered panic selling and weakened momentum, requiring time for the market to heal. In the short term, this $95K–$97K band can act as a local resistance, and reclaiming it would be an early indication that the market is moving back toward a degree of equilibrium.

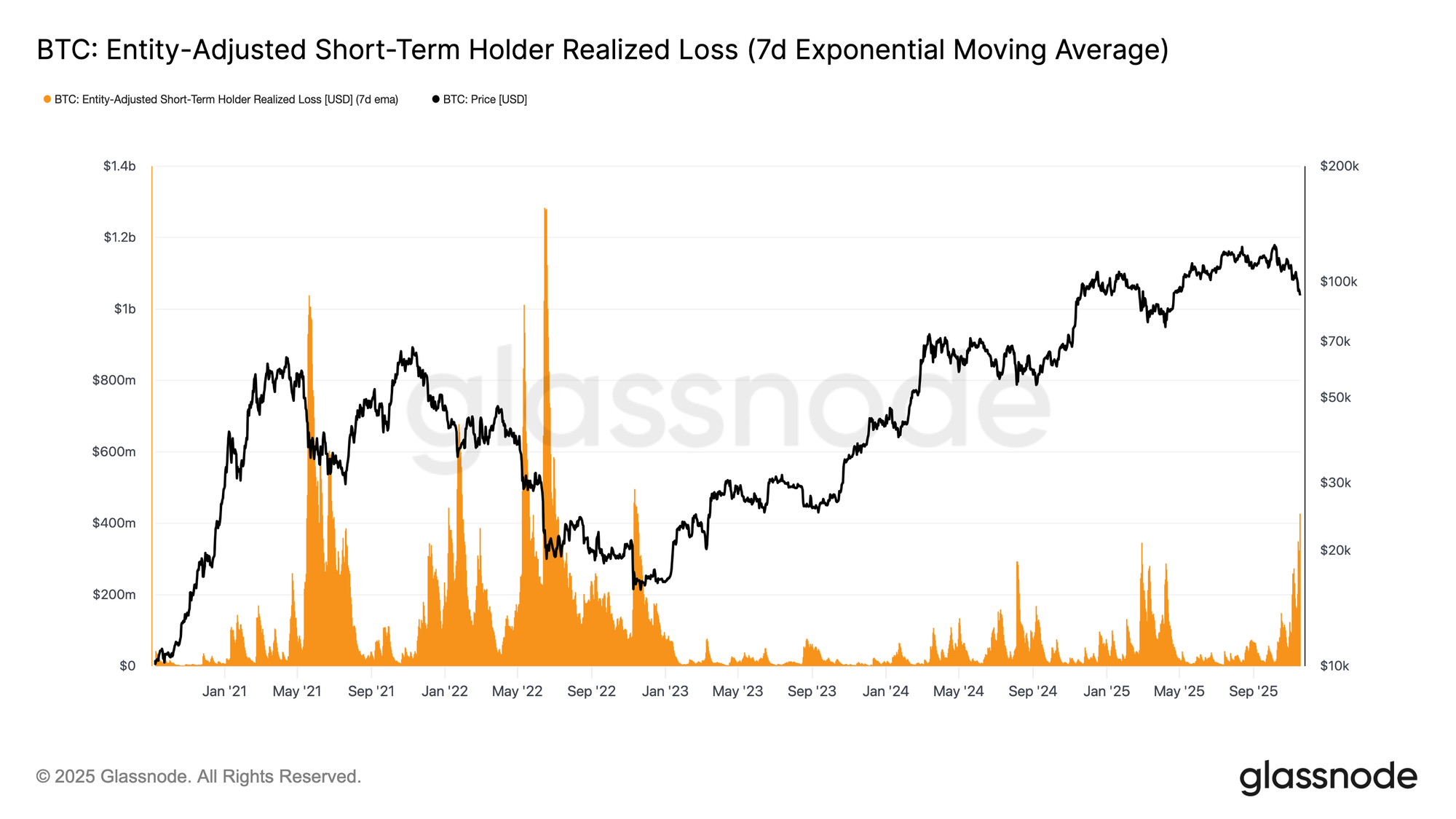

Panic Selling Peaks

Transitioning to investor behavior, this plunge marks the third time since early 2024 that price has fallen below the lower band of the short-term holder cost-basis model. However, the intensity of panic among top buyers is notably higher this time. The 7D-EMA of STH realized losses has surged to $523M per day, the highest level since the FTX collapse.

Such elevated loss realization highlights the heavier top structure built between $106K–$118K, far denser than previous cycle peaks. This means either stronger demand must emerge to absorb distressed sellers, or the market will require a longer, deeper accumulation phase before regaining equilibrium.

Testing Active Demand

Revisiting the valuation models, the market now enters uncharted territory, where speculative interest in this mild bearish phase has noticeably increased. The first major defense zone sits at the Active Investors’ Realized Price, currently around $88.6K. Trading near this level places Bitcoin at the cost basis of non-dormant holders who actively moved coins in recent months, making it a potential mid-term trading range.

However, a decisive break below this model would mark the first time this cycle that price has fallen beneath the active-investor cost basis, a clear signal that bearish momentum is dominating the market.

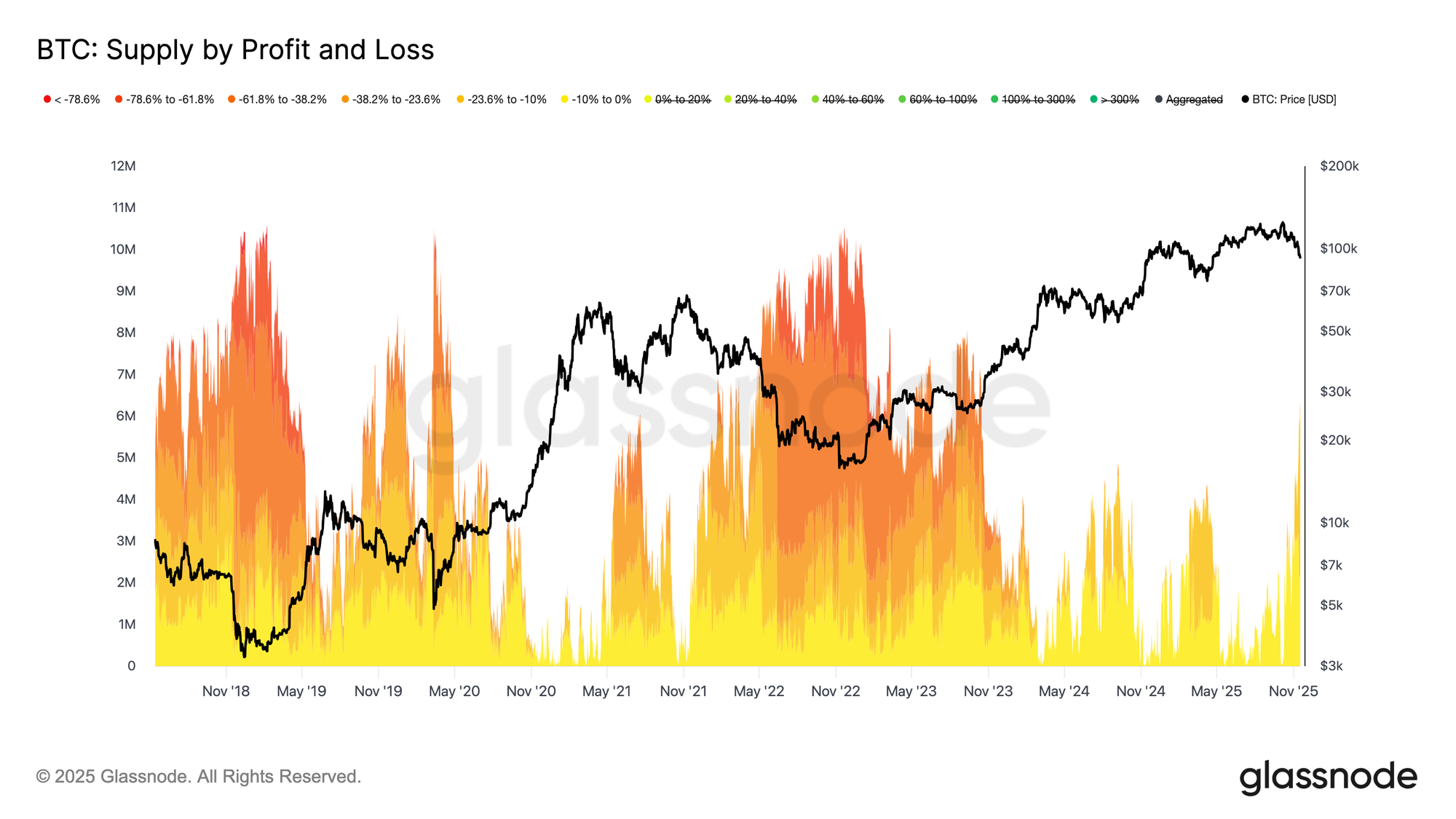

A Different Kind of Drawdown

Despite breaking below the major lower band of the short-term holder cost-basis model, the scale and intensity of investor pain remains far from the extremes seen during the 2022–2023 bear market. The chart below tracks all coins currently in loss and groups them by the depth of their unrealized drawdown. Roughly 6.3M BTC are now underwater, with the majority sitting in the –10% to –23.6% loss range.

This distribution closely resembles the Q1 2022 short-lived range market, rather than a deep capitulation phase.

This is why the price zone between Active Investors’ Realized Price ($88.6k) & True Market Mean ($82k) may serve as the definitive dividing range between a mild bearish phase and a full bear-market structure similar to 2022-2023.

Off-Chain Insights

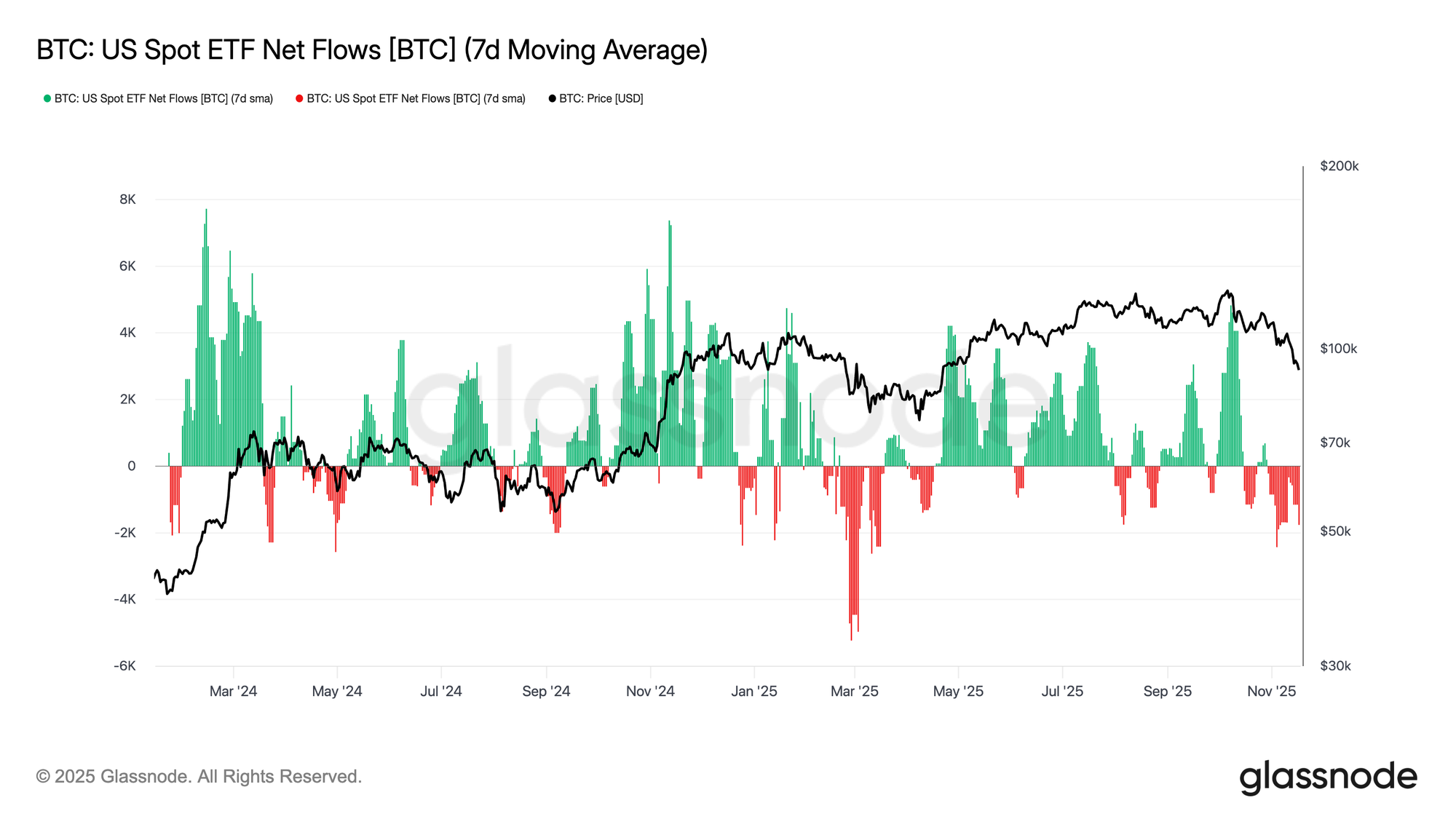

Absence of ETF Demand

US Spot ETF flows continue to reflect a pronounced lack of sustained demand, with the 7-day average remaining firmly negative in recent weeks. Persistent outflows signal a reluctance among TradFi allocators to add exposure into the current drawdown, a clear departure from the strong inflow regimes that supported prior advances. The ongoing weakness suggests discretionary appetite has cooled materially and highlights the absence of incremental bid from one of the market’s largest marginal buyer cohorts, reinforcing the broader environment of constrained demand.

The sustained absence in ETF inflows indicates that a major pillar of demand has yet to re-engage, leaving the market without a key source of demand this cycle.

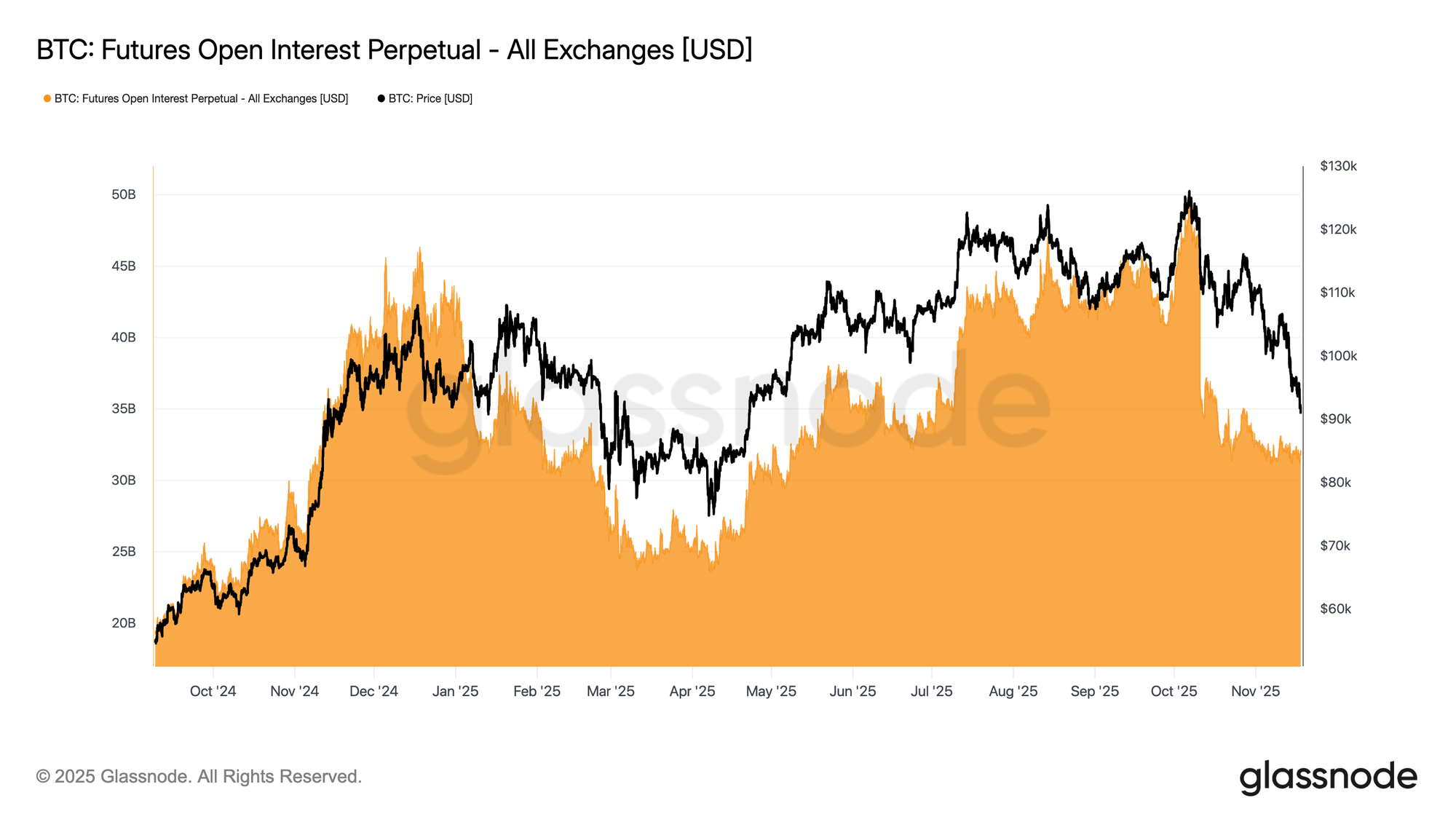

No Sign of Risk Appetite

Futures open interest continued to drift lower this week, declining in tandem with price and signalling a persistent reduction in speculative activity. Rather than adding exposure into weakness, traders have been systematically unwinding risk, leaving the derivatives market notably under-positioned compared with prior drawdowns. This absence of incremental leverage underscores a cautious stance among market participants and aligns with the broader theme of fading demand across risk-taking cohorts.

The ongoing contraction in futures positioning highlights a market still reluctant to deploy capital, reinforcing the lack of conviction behind current price action.

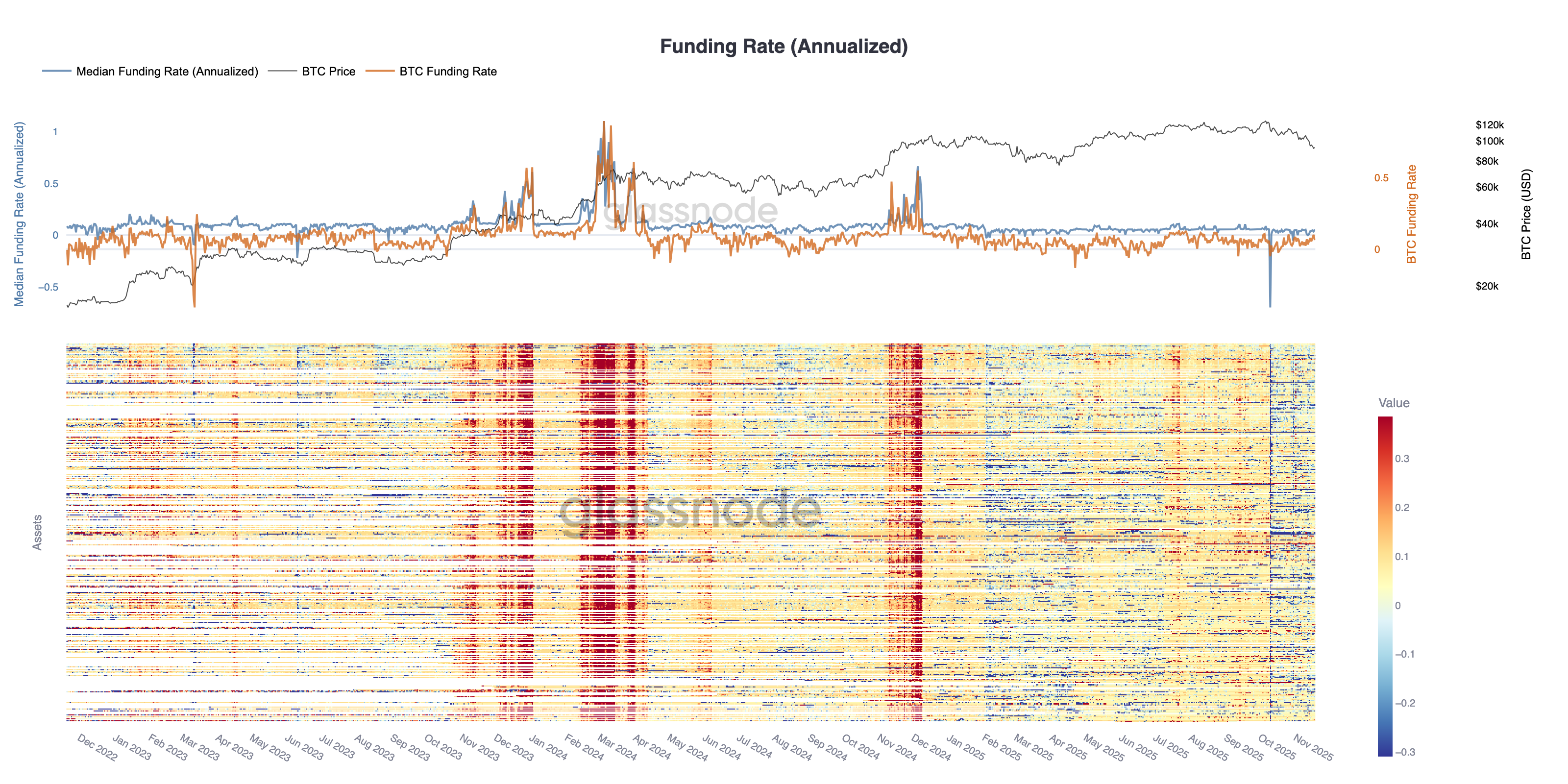

Funding Rates at Cycle Lows

With futures open interest continuing to decline, the derivatives market is signalling a clear reduction in speculative positioning. Traders are unwinding risk rather than adding exposure into weakness, leaving OI notably under-levered relative to prior drawdowns.

This dynamic is echoed in funding markets, where rates across the top 500 assets have shifted decisively into neutral-to-negative territory. The move away from the positive premia seen earlier in the year highlights a broad cooling in leveraged long demand and a turn toward more defensive positioning.

Together, falling OI and negative funding confirm that speculative leverage is being systematically drained from the market, reinforcing a risk-off backdrop.

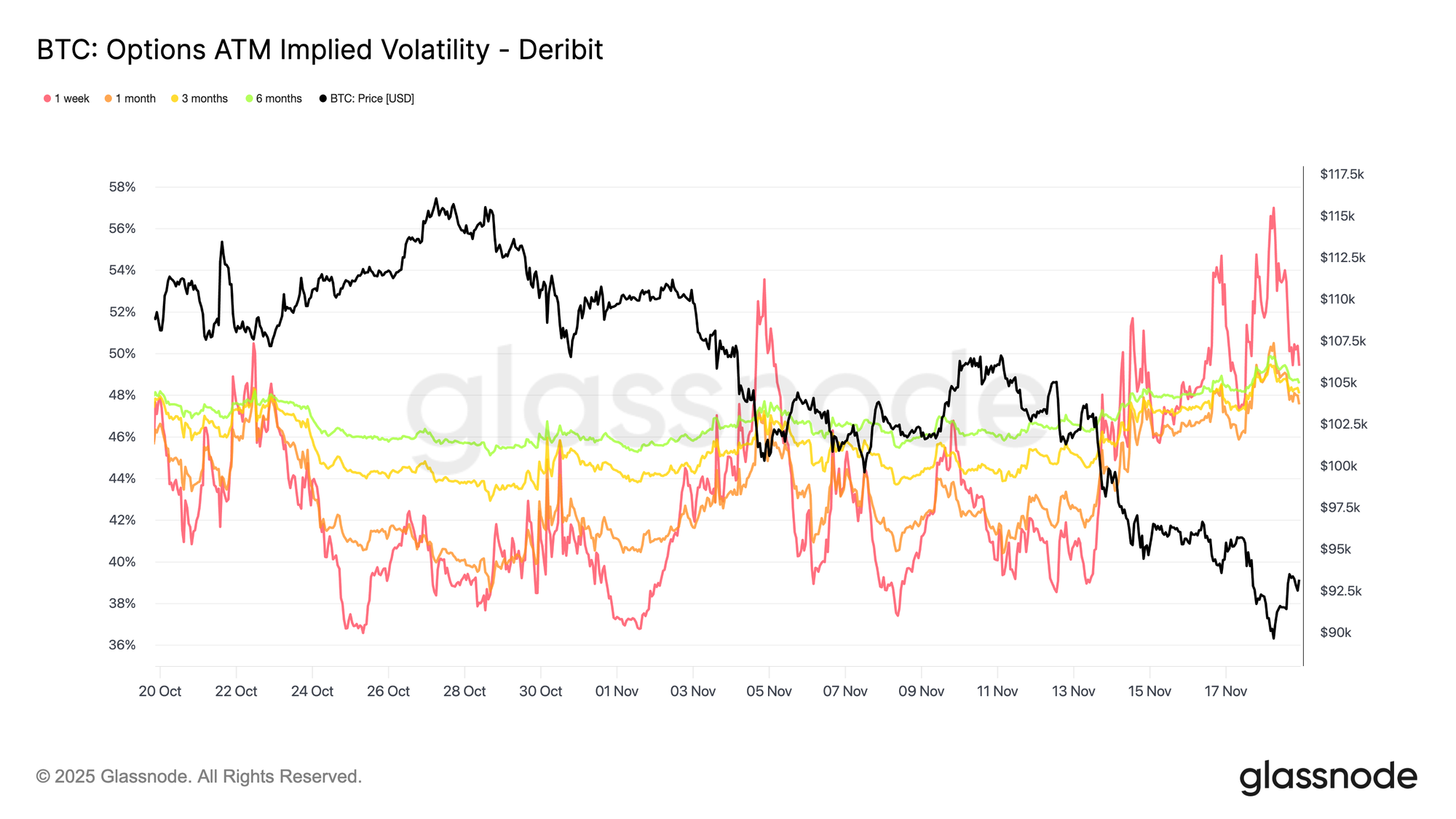

Sharp Rise in Implied Volatility

The options market is usually the earliest to reprice risk, and it did so quickly after Bitcoin briefly traded below 90,000. Implied volatility moved sharply higher across all maturities, with the front end reacting the most. The chart shows a clear lift in short-dated volatility and a broad repricing across the curve.

This increase reflects two drivers. The first is a stronger demand for downside protection as traders prepare for the possibility of a larger correction. The second is the response from short gamma desks. Many had to buy back short options and roll positions upward, which mechanically pushed front-dated implied volatility higher.

Implied volatility is now close to the levels seen during the October 10 liquidation event, showing how rapidly traders have reassessed near-term risk.

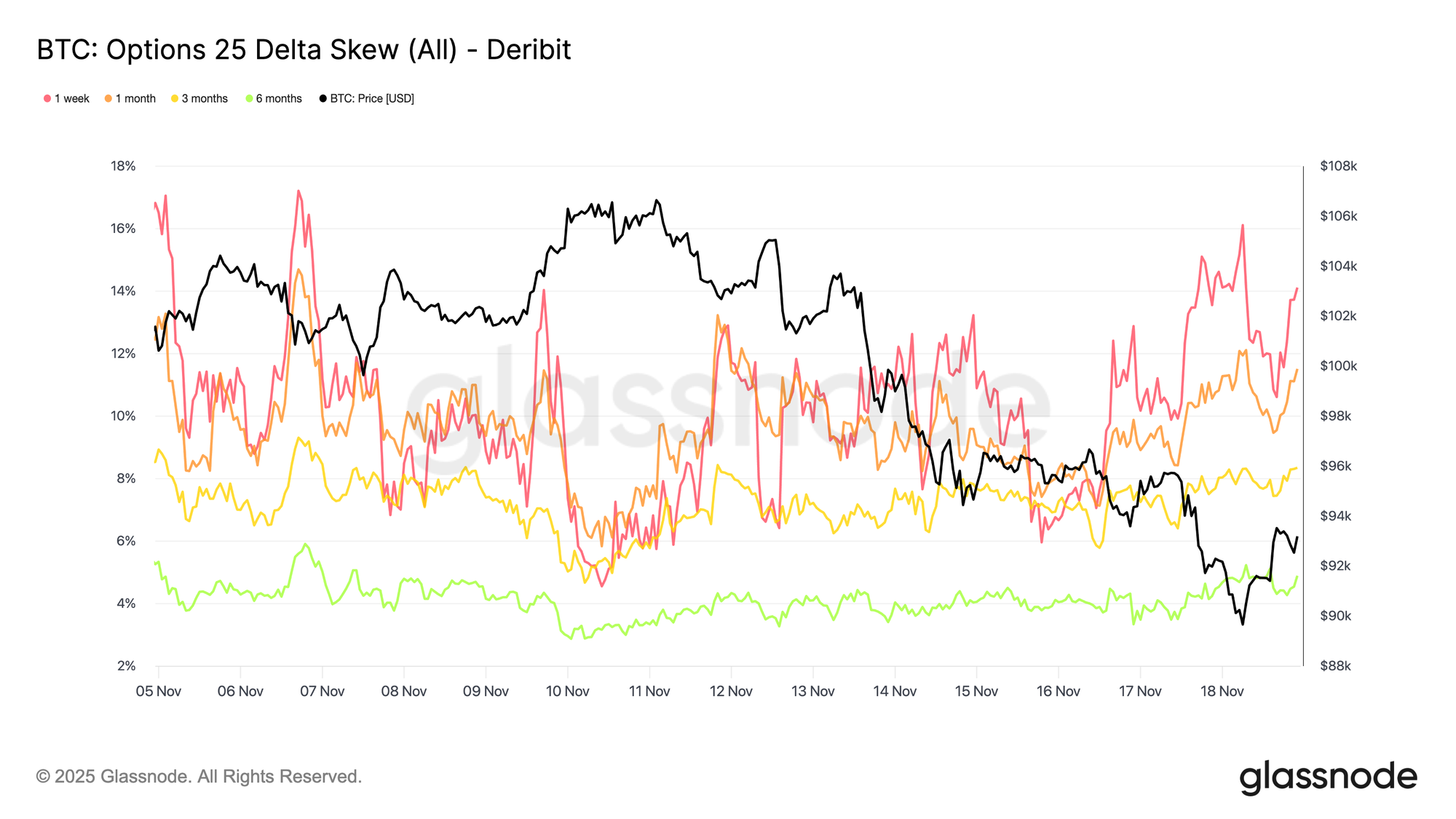

The Skew Confirms the Fear

Moving from implied volatility to skew, the options market shows the same message. The 25-delta skew remains negative across maturities, with the one-week tenor sitting near extremely bearish levels. A premium of roughly 14 percent for one-week puts shows that traders are willing to pay significantly more for downside protection regardless of spot price.

This behavior can create a self-fulfilling prophecy. When traders buy these puts, dealers often end up short delta. To hedge that exposure, they sell futures or perpetuals. This selling adds pressure to the market and can amplify the weakness that traders are trying to protect against.

Longer-dated skew also leans bearish but is less extreme. The six-month tenor sits just below 5 percent, which indicates that most of the concern is concentrated in the near term rather than across the entire maturity spectrum.

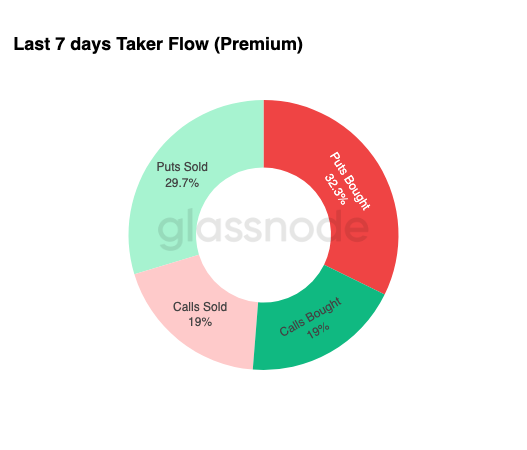

Demand for Downside Protection

Moving from skew to actual trading activity, the last seven days of taker flow underline the same pattern. Traders bought a large share of put premium, far outpacing demand for calls. This is consistent with hedging behavior and reflects a desire to protect against further weakness rather than position for upside.

The limited activity on the call side reinforces that traders are not adding meaningful risk into year-end. Calls bought and calls sold both remain low compared to put flows, which supports the view that caution rather than speculation is driving positioning.

Overall, this mix points to a market that is preparing for volatility and prefers protection over exposure.

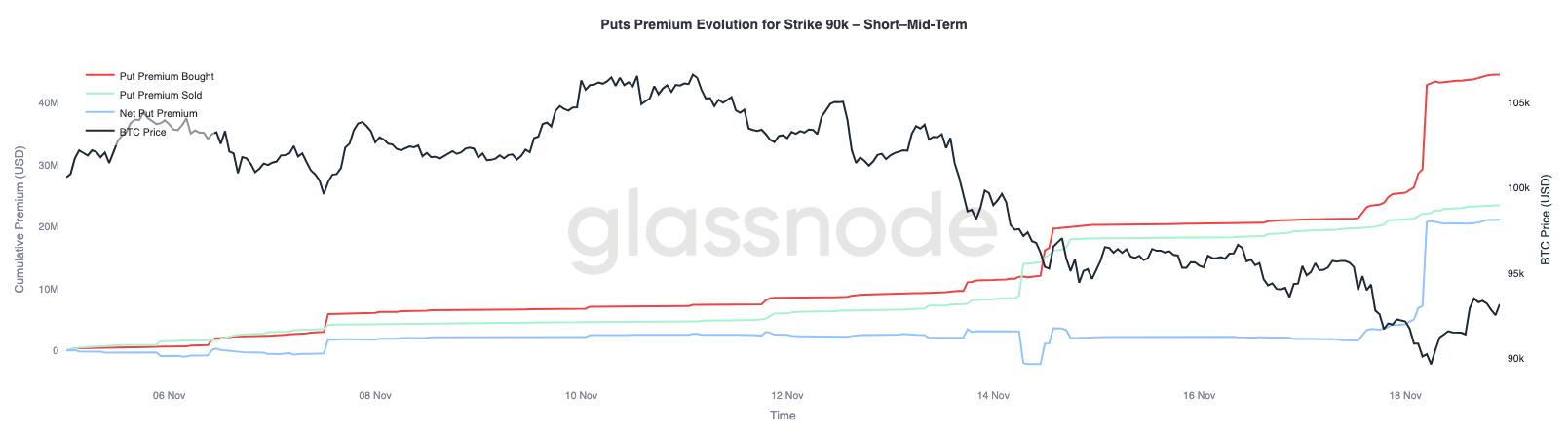

The 90K strike put premiums

Continuing from the broader flow data, the 90K strike put premiums show how protection demand accelerated as price weakened. Over the last two weeks, the net put premium at this strike stayed relatively balanced until Bitcoin broke below the 93,000 level. Once that level failed, traders lifted the offer on these puts, driving a sharp increase in premium bought at the 90K strike.

This behavior shows that traders were willing to pay increasingly higher prices to secure downside protection as spot pressure intensified. The move also aligns with the rise in short-dated implied volatility seen earlier, since concentrated demand at key strikes typically pushes the front end of the curve higher.

The sharp repricing of the 90K puts highlights how quickly downside hedging activity accelerates when key price levels break.

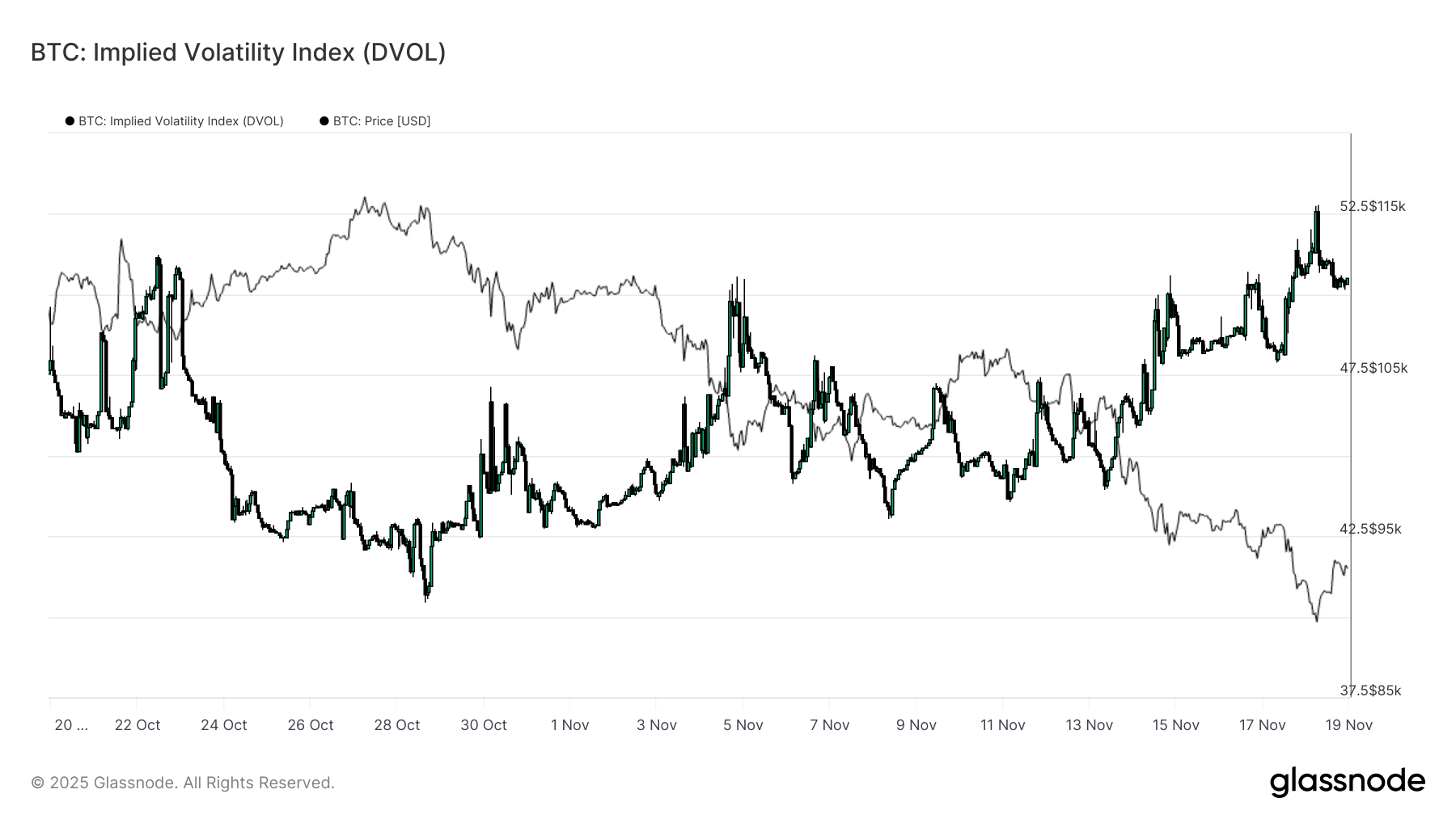

Pricing Market Fragility

Shifting from individual strikes to a broader volatility measure, the DVOL index shows how much the market has repriced risk. DVOL has climbed back toward the monthly highs near 50, after sitting closer to 40 only three weeks ago. DVOL reflects the implied volatility of a constant-maturity options basket, so when it rises, it signals that traders expect larger price swings ahead.

The move higher here ties together everything seen across the options market. Implied volatility is rising across maturities, skew remains negative, recent flows are delta negative, and traders show little interest in adding risk into year end. Together, these factors describe a market preparing for unstable price action. The key drivers are liquidation risk on perpetuals, macro uncertainty, and a lack of strong spot demand from ETF inflows.

The next event that can shift this volatility regime is the FOMC meeting in three weeks. Until then, the options market continues to signal caution and a clear preference for protection.

DVOL’s rise reinforces that the market is pricing in larger moves ahead, with traders positioning for volatility.

Conclusion

Bitcoin continues to work through a challenging market phase defined by weakening market structure, retreating speculative demand, and a decisive shift toward risk-off positioning across derivatives. Spot-based demand remains absent, ETF flows are negative, and futures markets show no appetite to add leverage into weakness. Meanwhile, implied volatility, skew, and hedging flows all point toward heightened concern for near-term downside risk, with investors paying increasingly high premiums for protection. Together, these dynamics frame a market searching for stability, where the path forward depends on whether demand can re-emerge around key cost-basis levels or whether current fragility gives way to a deeper corrective phase or bear market.